What Happens on a Mortgage Credit Check? A Complete Guide

Imagine walking into a bank or mortgage institution, and they already have an insight into your financial habits.

That’s precisely what a credit history does—it paints a picture of your financial reliability.

So, when you knock on the doors of a mortgage lender, they’ll closely study this ‘picture’ to see how reliable you’ve been with finances.

It’s their way of ensuring they’re investing in the right person.

So, what do they look for?

Questions like: “Does this person pay on time with repayments?” or “Is their debt situation manageable?” become crucial.

That’s the essence of credit checks.

In this complete guide, we’ll explain the entire concept of mortgage credit checks in the UK. Learn about the nuances of ‘hard searches’ and how they differ from ‘soft checks’.

Whether you’re gearing up to get a mortgage or just aiming to get a clearer understanding, we’ve got you covered.

What is a Mortgage Credit Check?

A mortgage credit check is an assessment conducted by a lender to evaluate your creditworthiness or how likely you are to repay the mortgage loan.

Lenders do this by examining your credit history, which includes your past borrowing behaviour and any outstanding debts.

There are two types of credit checks that you might encounter during the mortgage application process: hard checks and soft checks. Let’s examine each.

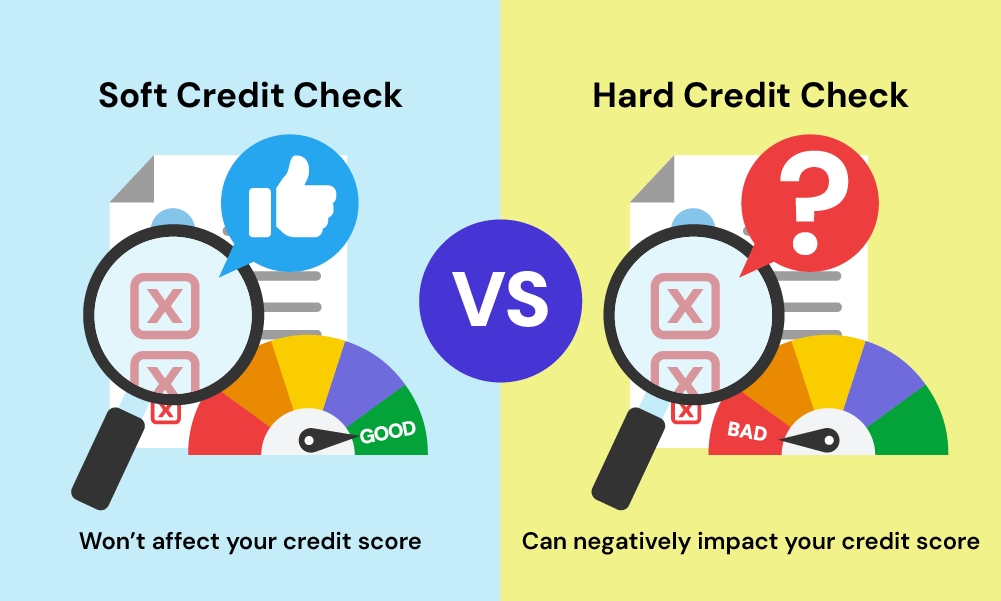

Hard Credit Check: The Full Financial History Examination

A hard credit check is a deep dive into your credit history. This check is comprehensive and involves evaluating your complete financial history. It uncovers every instance where you’ve applied for credit and any issues you’ve had with repayments.

Here’s what you need to know about hard credit checks:

- They leave a ‘footprint’ on your credit report. This means future lenders, for a mortgage, credit card, or another type of loan, will see that you’ve applied for credit.

- Too many hard credit checks in a short period (generally within a six-month window) could be viewed negatively by mortgage providers. It might reduce the number of lenders willing to consider your application.

- The details of a hard check typically remain on your credit report for 12 months.

Soft Credit Check: The No-Impact Check

A soft credit check, unlike its hard counterpart, is more of a light perusal of your financial history. It provides a basic overview of your financial standing and can indicate your creditworthiness.

Here are a few key facts about soft credit checks:

- They don’t leave a footprint. That means future lenders won’t know you’ve had one unless you tell them. They are invisible to everyone except you and the company that carried out the check.

- Soft checks are often used for initial assessments. They can indicate how likely you are to be accepted for credit without the need for a full hard check.

- You can have as many soft checks as you like without it affecting your credit rating or your chances of being accepted for a mortgage in the future.

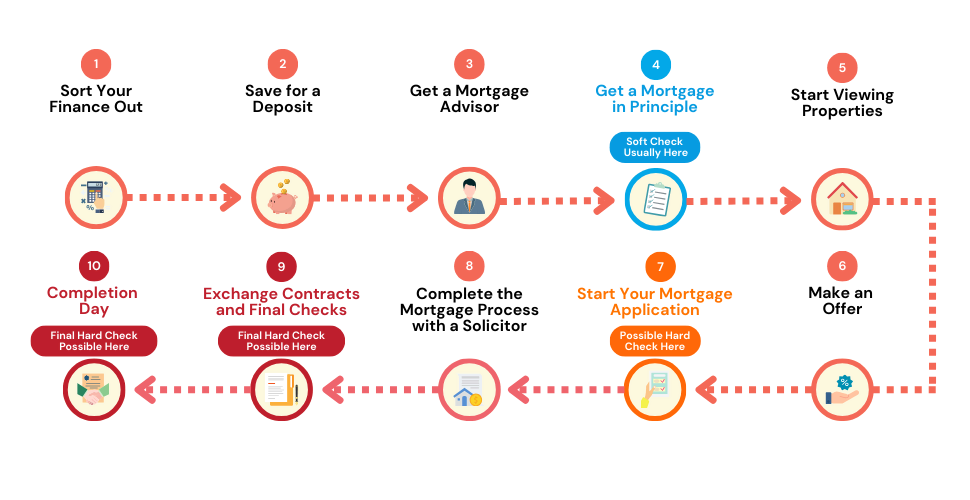

When and Why Mortgage Lenders Run Credit Checks?

One of the earliest steps in the mortgage application process is a credit check. This is done to assess your financial reliability.

Lenders usually conduct a credit check on the ‘mortgage in principle’ stage. This pre-approval is crucial as it gives you confidence in how much you can afford and makes you more appealing to property sellers.

While this early check is typically a soft check, some lenders might choose to do a hard check right away. Towards the end of the buying process, lenders often conduct a final hard check.

This could occur:

- Just before exchanging contracts

- On the day of exchanging contracts

- After exchanging contracts

- Close to the completion day

In these checks, lenders are looking for consistency in your financial behaviour.

They’re assessing your income, your expenditure, your age, and how many dependents you have. They’re checking to ensure that your circumstances haven’t changed since your first application.

How To Check Your Credit Report

It’s a good idea to check your credit report before applying for a mortgage, as it can give you a better understanding of your credit standing.

Here are simple steps on how to check your credit report:

1. Identify the Credit Reference Agencies (CRAs). In the UK, there are three main CRAs. These are Experian, Equifax, and TransUnion. They all hold information about your credit history and provide credit reports.

2. Request Your Credit Report

You can request your free statutory report from each agency. You can do this online through their websites or if you want a paper copy, you can contact them directly:

- Access your Experian Credit Report

- Access your Equifax Credit Report

- Access your TransUnion Credit Report

3. Fill Out the Required Information. You will need to provide some personal details to verify your identity. This may include your full name, date of birth, current address, and past addresses from the last five years.

4. Review Your Report. Once you receive your report, go through it thoroughly. Look for any errors or unusual activity. It will contain a list of your credit accounts, repayment records, and any public records like bankruptcies.

5. Report Errors, if Any. If you find mistakes or suspect fraudulent activity, contact the CRA to have it corrected. This could involve providing further evidence or documents.

Remember, checking your credit report is a good habit to develop. It helps you understand your financial health and ensures there are no surprises when you’re applying for a mortgage or other forms of credit.

How Mortgage Checks Impact Your Credit Rating

Mortgage checks, particularly hard ones, can have an impact on your credit rating. These checks leave a footprint on your credit file, which other lenders can see when they carry out their checks.

- Single hard check. A single hard check can have a minor impact on your credit score. But, this usually recovers over a few months if you keep up with your other credit commitments.

- Multiple hard checks. When multiple hard checks are carried out in a short period, this can signal to lenders that you’re in financial distress or are not managing your finances well. This can impact your chances of being approved for credit.

- Duration on file. In the UK, hard credit checks stay on your credit file for a year. If you have a lot of hard checks in a short space of time, lenders might see this as a negative sign. This could mean that fewer lenders will be willing to consider your application.

Do Mortgage Brokers Run Credit Checks?

A good mortgage broker may run a credit check to get a clear view of your finances. They could ask you to share your credit report or, with your approval, they might get one themselves.

Having a full overview of your financial past allows them to offer advice that’s specific to you. Good brokers, especially those well-versed in managing poor credit cases, are good at understanding what lenders are looking for. They use this knowledge to pinpoint the most fitting lender for your needs.

Key Takeaways

- A mortgage credit check shows lenders how reliable you are with money. Hard checks are detailed and can affect your credit score, while soft checks are basic and don’t leave a mark.

- Lenders usually perform credit checks early in the application process (often a soft check) and again later (a hard check) to ensure your financial stability hasn’t changed.

- Too many hard credit checks in a short time can lower your score and make lenders hesitant, but soft checks don’t have this effect.

- Checking your own credit report and working with a good broker can help avoid unnecessary hard checks and improve your chances of approval.

The Bottom Line

Mortgage checks can affect your credit file, so it’s important to understand their impact when you’re applying for a mortgage.

Take charge of your credit score, manage it carefully, and reach out for expert advice to make buying a home easier.

Here’s how a good mortgage broker can help you boost your credit score:

- Check your credit report for mistakes and help fix them.

- Give advice on how to use your credit more effectively.

- Negotiate with creditors to resolve debts.

- Represent you to lenders and support your application.

If you’re ready to improve your credit score, get in touch with us, and we’ll arrange a consultation with an experienced mortgage broker.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

How does a mortgage payment holiday reflect on my credit report?

Although a mortgage payment holiday doesn’t directly damage your credit rating, it appears on your credit report. This could alter future loan eligibility, as some lenders may view it as a sign of increased risk. Keep this in mind when considering a payment holiday.

What is the effect of a mortgage in principle on my credit rating?

When a lender processes a mortgage in principle, it may require a credit check. A soft check doesn’t affect your credit rating. However, a hard check can leave a trace on your credit file, which may negatively influence your rating.

Can multiple mortgage applications impact my credit?

Yes, having many mortgage applications can have a knock-on effect on your credit rating, particularly if each one involves a hard credit check. An excess of applications could lead some lenders to see you as a potential risk. To avoid this, try to space out applications or work with a good broker.

Do all lenders run hard credit checks?

While it’s common for lenders to run credit checks, some use soft checks that leave your credit rating untouched. Examples include Kensington and Principality Building Society, which conduct soft searches when checking credit. It’s crucial to do your research or engage a mortgage advisor to explore your options.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage With a Bad Credit: A Complete Guide

Thinking of renovating the kitchen, building an extension, or finally booking that dream family holiday? If bad credit’s been holding you back from remortgaging to free up cash, you’re not alone. Many people worry that their past financial mistakes might prevent them from using their home’s value. But good news: it’s possible to remortgage even […]

How To Improve Mortgage Credit Score? 10 Best Tips in 2025

When you’re applying for a mortgage, your credit score is like a summary of your financial behaviour. It shows how well you’ve managed credit in the past, and lenders use it to decide if they’ll approve your application. Your credit score doesn’t just affect approval—it also impacts the interest rate you’ll be offered. A higher […]

How To Get Subprime Mortgages in the UK: A Complete Guide

History has a funny way of shaping where we end up, and mortgages are no exception. If you remember the subprime mortgage crisis of 2007-2008, it was a huge shake-up that left lenders no choice but to tighten their rules and be far more careful. These days, things are a lot different. While borrowing money […]