- Are Mortgages Available to Limited Liability Partnerships (LLP)?

- How Much Can You Borrow for LLP Mortgages?

- Other Mortgage Criteria for an LLP

- Can an LLP Secure a Buy-to-Let Mortgage?

- Can a New LLP Obtain a Mortgage?

- Can an LLP With Company Debt Get a Mortgage?

- How Do Interest Rates for LLP Mortgages Compare?

- Key Takeaways

- The Bottom Line: Your Next Steps

How To Get Mortgages in a Limited Liability Partnership?

Have you ever considered applying for an LLP mortgage for your business?

If yes, you’re part of a growing trend.

More and more companies are turning to Limited Liability Partnership (LLP) mortgages for both investment opportunities and residential needs.

But, navigating the LLP mortgage landscape isn’t always a walk in the park.

This guide is designed to simplify the complexities and offer a transparent understanding of how to get an LLP mortgage for your business. From the application process to the diverse lending criteria, we’ll cover it all.

With so many businesses successfully embracing LLP mortgages, there’s no reason why you can’t too. And remember, it’s not about going it alone.

Specialist advice can make all the difference, connecting you to the right lender for your specific needs.

Are Mortgages Available to Limited Liability Partnerships (LLP)?

Yes, mortgages are available to Limited Liability Partnerships (LLP).

But the process is more complex compared to standard mortgage applications.

When applying as part of an LLP, mortgage lenders typically consider you self-employed. This leads to a distinct set of assessments and requirements.

To secure a mortgage within an LLP, you’ll need to provide evidence of income and give detailed insights into how the LLP operates and is managed.

If the intention is to buy an investment property with your fellow partners, the complexity of the application may increase further.

While mortgages are accessible to LLPs, the path to approval may not be effortless. It is often recommended to seek the expertise of a broker who specialises in LLP mortgages.

They can help you find the right mortgage option for you and your partnership, with their knowledge and experience.

How Much Can You Borrow for LLP Mortgages?

Different lenders use different methods to calculate the maximum borrowing amount for an LLP mortgage.

They may offer between 3 and 5 times your annual income, but this range may vary depending on the lender’s policies.

To understand your eligibility and potential borrowing limit, lenders will need to carefully review your income.

Since you don’t have traditional payslips in an LLP, they will look at the company’s financial records. This can be your finalised accounts or SA302 documents from the HMRC. These documents must be verified by an accountant or other authorised professional.

It is also possible to get a personal mortgage if you are an LLP director. This may be a better option if you are buying a residential property.

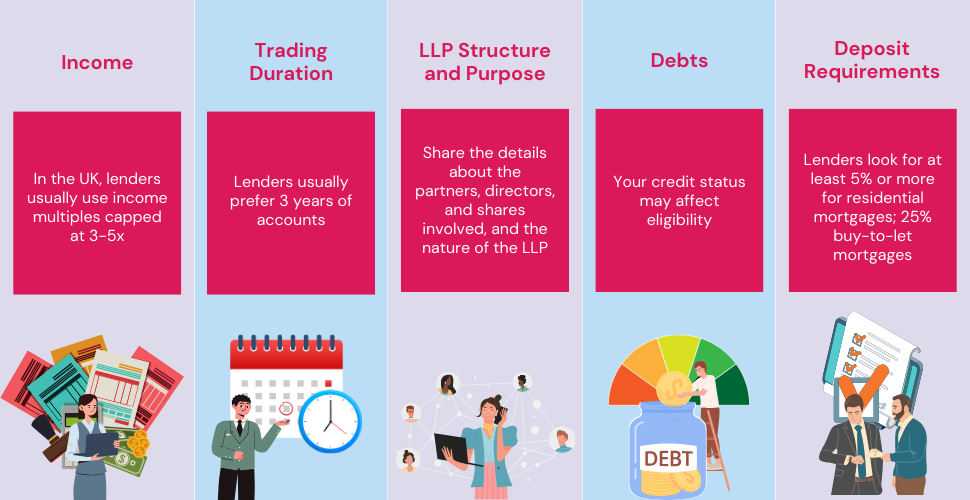

Other Mortgage Criteria for an LLP

If you’re part of an LLP and considering a mortgage, you should know that it’s not just about being in a partnership. Lenders will examine various factors to determine your eligibility:

Trading Duration

The length of time you’ve been operating as an LLP matters.

Many lenders prefer at least three years, but some may accept two years or even less with additional evidence of experience or previous employment in the sector.

LLP Structure and Purpose

You’ll need to provide details about the partners, directors, and shares involved in the LLP, including its nature.

This becomes particularly essential if the LLP was created as a special purpose vehicle (SPV) or if you’re applying for an investment mortgage within the partnership.

Debts

Any debts within the LLP can affect your eligibility for a mortgage.

Bad credit is not an outright disqualifier, but it may necessitate working with specialist lenders, a higher deposit, and potentially higher rates.

Deposit Requirements

Generally, deposit requirements for self-employed borrowers like those in an LLP align with PAYE borrowers.

This means you can have at least a 5% deposit. But a higher deposit might be required if the trading history is short. Note though that this will be different for buy-to-let mortgages.

Other Standard Factors

Factors common to all mortgage applicants, such as the property type, your age, and your outgoings, will be part of the lender’s considerations as well.

As discussed, securing a mortgage as part of an LLP involves more complex considerations than traditional applications. But understanding these factors will help you approach the process with confidence.

The specific approach of each lender will vary, depending on their risk tolerance and lending standards.

This makes it important to work with a knowledgeable mortgage broker who is familiar with LLP lending. They can guide you through the complexities and help you find the right fit for your mortgage needs.

Can an LLP Secure a Buy-to-Let Mortgage?

Yes, an LLP (Limited Liability Partnership) can secure a buy-to-let mortgage.

Some lenders specifically cater to companies looking to invest in buy-to-let properties, though it’s worth noting that the rates might be slightly higher than conventional mortgages due to the perceived increased risk.

This increased risk is linked to the nature of LLPs, where the individual members aren’t personally liable for company debts.

For example, if the mortgage were to fall into arrears, the responsibility would fall on the LLP, not the individuals.

Therefore, lenders may insert clauses holding the directors accountable if loans aren’t repaid, to mitigate this risk.

When it comes to deposits, an LLP will generally find that the requirement for a buy-to-let mortgage is higher than a residential one, whether the applicant is an individual or a business entity.

The standard expectation is a minimum 25% deposit, with mortgage rates typically starting at 60% loan to value. Some lenders might even offer mortgages with just a 15% deposit.

In the buy-to-let market, lenders tend to focus more on the property’s potential rental income rather than the applicant’s personal or business income.

This shift in focus is logical since the rent is intended to cover mortgage payments.

But, the lender will still assess whether the mortgage payments can be managed during periods without rent, ensuring a stable and secure lending arrangement.

Can a New LLP Obtain a Mortgage?

Yes, you can get a mortgage even if you’re a newly established LLP.

The trading history of an LLP plays a crucial role in mortgage eligibility, with a longer history often indicative of more stability and less risk.

While the age of an LLP matters, it’s not the sole determinant of a mortgage application’s success or failure.

Other factors such as overall financial health, net income, and existing debt can have a significant impact on the assessment.

Typically, most lenders prefer an LLP to have been trading for at least three years. They use this history to gauge the stability and income of your business.

A three-year trading record provides enough data for lenders to make a well-informed decision regarding the mortgage’s affordability.

But, this three-year requirement is not a strict rule. Specialised lenders may consider applications from LLPs with only two years of accounts or even just one year in some instances.

This flexibility is contingent on other factors such as net income and the company’s debt profile.

Every business is unique, and so each mortgage application is evaluated individually.

If you find yourself in the position of seeking a mortgage for a new LLP, it may be beneficial to consult with a knowledgeable advisor. They can guide you through the process, and help you understand your options and likelihood of success.

Can an LLP With Company Debt Get a Mortgage?

Yes, securing a mortgage with an LLP (Limited Liability Partnership) that has company debt or credit issues is possible. But it certainly can make the process more challenging.

If you find yourself in this situation, it’s important to understand that lenders might deem the LLP to be high-risk, depending on the specifics of the debt and the overall credit history of the business.

The lender will carefully evaluate factors like:

- The number of creditors involved

- The total amount of debt that the company carries

- The general credit history of the business, including any defaults or late payments

Because of the increased risk associated with lending to an LLP with bad credit, conventional lenders might be hesitant.

But, there are specialist lenders who cater specifically to this niche. They may still be willing to offer a mortgage to an LLP with credit issues, though it usually comes with certain caveats.

These specialist lenders may charge higher interest rates to mitigate the risk, or they may insist on larger deposits being made upfront. This is to compensate for the potential uncertainty that comes with lending to a business that has a history of debt or credit issues.

How Do Interest Rates for LLP Mortgages Compare?

Interest rates for LLP (Limited Liability Partnership) mortgages might be somewhat different than those for traditional mortgages, and they can sometimes be slightly higher.

Especially if the mortgage is for investment purposes. These rates aren’t set in stone and are typically decided on a case-by-case basis.

A variety of factors influence the interest rates for an LLP mortgage, including but not limited to:

- The nature of the LLP. If the partnership is set up for investment or special purposes, the rates might differ.

- Credit History. The LLP’s credit standing and financial health can affect the interest rate.

- Economic Climate. With interest rates being subject to change due to economic factors, it’s important to recognize that they can fluctuate.

Key Takeaways

- Mortgages are available to LLPs, but they require a detailed understanding of how the LLP works, and it’s beneficial to seek the expertise of a specialised broker.

- How much you can borrow varies, depending on the lender’s policies and a careful review of your income through financial documents like finalised accounts or SA302.

- New LLPs can secure a mortgage, but a longer trading history usually helps. Specialised lenders may consider shorter trading histories.

- LLPs can secure both residential and buy-to-let mortgages, with variations in rates and deposit requirements, reflecting the unique nature of LLP lending.

The Bottom Line: Your Next Steps

Now you know the basics of LLP mortgages—like how your trading history, income, and LLP structure can affect whether you’re eligible.

Some applications are simple, while others need expert advice. That’s where a skilled LLP mortgage broker comes in handy.

An expert can give you advice that fits your LLP’s situation. They’ll check if your partnership qualifies for a mortgage, connect you with the right lender, and help you with the paperwork.

They’ll also explain things like borrowing limits, credit history, and deposit needs so you’re never left guessing.

Ready to move forward with your LLP? Get in touch with us today. We’ll match you with an expert broker for free advice—no pressure, no commitment. Just fill out our inquiry form to get started.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What is an LLP in the UK?

An LLP, or Limited Liability Partnership, in the UK, is a business structure that offers the benefits of limited liability to its members while allowing flexibility in the way it’s run. It’s a common choice for businesses wanting to combine elements of partnerships with the protections of a limited company.

When applying for a mortgage, what part of my income from owning an LLP will lenders look at?

When applying for a mortgage as an LLP owner, lenders usually consider your share of the profits as your income. They’ll typically look at financial documents like finalised accounts or SA302 documents from HMRC, verified by an accountant or authorized professional, to assess your income and eligibility.

How many years should my LLP be trading to qualify for a mortgage?

Most lenders prefer your LLP to have been trading for at least three years to gauge stability and income. However, specialised lenders may consider applications from LLPs with shorter trading histories, even as short as one or two years, depending on other factors like net income and debt profile.

Can self-employed LLP owners with adverse credit history still get a mortgage?

Yes, obtaining a mortgage as a self-employed LLP owner with adverse credit history is possible but more challenging. Specialist lenders may cater to this niche, possibly requiring higher interest rates or larger deposits to offset the risk.

It’s often recommended to consult with a knowledgeable broker familiar with LLP lending to navigate this situation.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache. Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself. But there’s good news: With the right support, YOU can switch your mortgage without a hitch. In this article, we’re going to […]

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]