- Can I Remortgage to Fund Home Improvements?

- How to Borrow More Through Remortgaging?

- How to Remortgage to Fund Home Improvements

- How Much Can I Borrow?

- How Does Remortgaging for a Property Extension Work?

- Do I Need Official Approval?

- Should I Remortgage After the Home Improvements or Before?

- Exploring Various Home Improvements

- Other Things to Consider Before Remortgaging

- Remortgaging After Home Renovations

- Should I Consider Remortgaging?

- What are the Alternatives to Remortgaging?

- The Bottom Line

Remortgaging for Home Improvements

Ever sat at home, thinking of that stylish kitchen or the perfect conservatory you saw in a home magazine?

Like many others in the UK, you’re probably eager to put some new life and personality into your home. But let’s face it, home renovations can be a bit hefty on the pocket.

One way to fund home improvements without draining your savings is to remortgage. This means swapping your existing mortgage for a new deal.

By doing this, you can unlock the funds you need to make your home improvement dreams a reality.

In this guide, we will walk you through the process of remortgaging for home improvements. We will explain how to get the best deals, avoid common pitfalls, and make the right decision for you and your home.

Can I Remortgage to Fund Home Improvements?

Yes, certainly.

To recap, remortgaging is the process of switching your mortgage to a new lender or product. This can be done to get a better interest rate, shorten your repayment term, or access more funds.

If you have sufficient equity in your home and can manage the additional repayments comfortably, you may be able to remortgage and borrow more money. This can be used to finance home improvements, such as a kitchen extension, bathroom renovation, or loft conversion.

When remortgaging for home improvements, it is important to consider the following factors:

- The cost of the home improvements

- The amount of equity you have in your home

- The interest rate on the new mortgage

- The early repayment charges on your current mortgage

- Your ability to afford the monthly repayments

How to Borrow More Through Remortgaging?

First, decide on the specific home improvements you want to make. This could include:

- Installing a new bathroom or kitchen (usually the most expensive)

- Building an extension

- Renovating multiple rooms at once

- Landscaping or adding new outbuildings

Then, get a clear idea of the total cost of your project to see if remortgaging to release equity is the right option for you. You will need to consider the following:

- Your current mortgage balance

- The estimated value of your property

- The projected cost of the improvements

Let’s illustrate this with a scenario and a table to help you understand better:

| Details | Amount in £ |

|---|---|

| Current Mortgage Balance | 60,000 |

| Current Property Valuation | 200,000 |

| Equity in Home [Property Valuation – Mortgage Balance] | 140,000 |

| Projected Cost of Improvements | 30,000 |

| New Mortgage Balance [Current Mortgage + Improvement Cost] | 90,000 |

| Loan-to-Value Ratio [(New Mortgage Balance / Property Valuation) x 100%] | 45% |

In this scenario, your remaining mortgage balance stands at £60,000 and the current market valuation of your home is around £200,000. This gives you with £140,000 equity in your home.

If your improvement projects are estimated to be £30,000, then after renovation, your loan-to-value ratio would be about 45%.

Once you have this information, you can start to compare remortgaging deals to find the best one for you. When comparing deals, be sure to factor in the following:

- The interest rate

- The early repayment charges

- The length of the term

It’s also important to get professional advice from a mortgage broker or financial adviser before remortgaging. They can help you to understand your options and make the best decision for your individual circumstances.

How to Remortgage to Fund Home Improvements

Follow these clear steps if you are considering remortgaging to fund home improvements:

Step 1: Calculate Your Equity and LTV

First, work out the available equity in your home and your loan-to-value (LTV) ratio. This is done by deducting your current mortgage balance from your property’s current market value.

Step 2: Check for Planning Permissions

Find out if you need planning permissions for the home improvements you have in mind. If yes, initiate the necessary procedures to obtain the approvals.

Step 3: Improve Your Credit Reports

Before reaching out to lenders, ensure your credit reports are pristine. Settle any outstanding debts and update your financial records to portray a reliable credit standing.

Step 4: Gather Necessary Documents

Next, assemble all the required documents for your application, including proofs of income and identity, and details about your existing mortgage and the proposed improvements.

Step 5: Find the Best Mortgage Lender

Now, start your search for the best mortgage lender who can offer favourable rates to fund your home improvements. Do a comparative analysis of different lenders and their offerings to choose the best one.

Step 6: Think About Using a Broker

If you find the process challenging, consider consulting a broker with expertise in remortgages. They can provide guidance and connect you with the right lenders.

If you prefer an easier and well-informed route, send us an enquiry. We will pair you with a remortgage advisor to guide you through these steps, helping you secure a favourable deal for your home improvements.

How Much Can I Borrow?

Homeowners often wonder how much equity they can use from their homes to renovate or improve them.

Different mortgage providers have different rules, and some allow you to access a significant portion of your home equity.

To get an estimate of how much equity you can release, you can use our calculator. It will show you the maximum amount you could potentially borrow, as well as the estimated monthly repayments.

This will help you make an informed decision about whether remortgaging to release equity is the right option for you.

How Does Remortgaging for a Property Extension Work?

A property extension can be a wise way to increase the value of your home without having to move. It may be possible to fund it entirely or partly with the equity released when you refinance.

Before you start down this path, there are some important steps and considerations to keep in mind to ensure a smooth process.

Do I Need Official Approval?

Contrary to popular belief, most property extensions do not require planning permission because they fall under permitted development – unless, of course, you are planning a two-story addition.

However, obtaining building regulations approval is often required. You can get comprehensive information from the government’s website and perhaps speak with your local council to double-check the details to smoothly navigate this area.

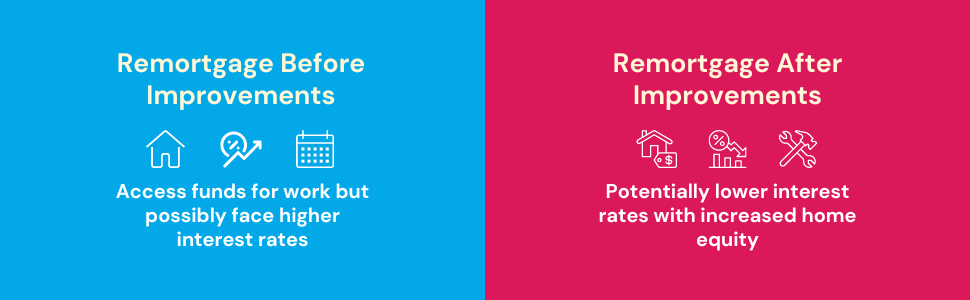

Should I Remortgage After the Home Improvements or Before?

It is common for homeowners to wonder whether they should remortgage before or after they start home improvements.

Remortgaging before home improvements can give you the money you need to pay for the work. However, it can also mean that you will have to pay higher interest rates, as you will be borrowing more money.

Remortgaging after home improvements can be a better option if you can afford to pay for the work upfront.

This is because the value of your home will likely increase after the improvements are complete, which means that you will have more equity to borrow against. This could give you access to lower interest rates and better mortgage deals.

Ultimately, the decision of whether to remortgage before or after home improvements is a personal one. You should weigh the pros and cons of each option carefully to decide what is best for you.

Exploring Various Home Improvements

Remortgaging can be used to finance other types of home improvements besides extensions, which could improve your living space and potentially increase your property value.

Here are some additional options to consider when you refinance your home:

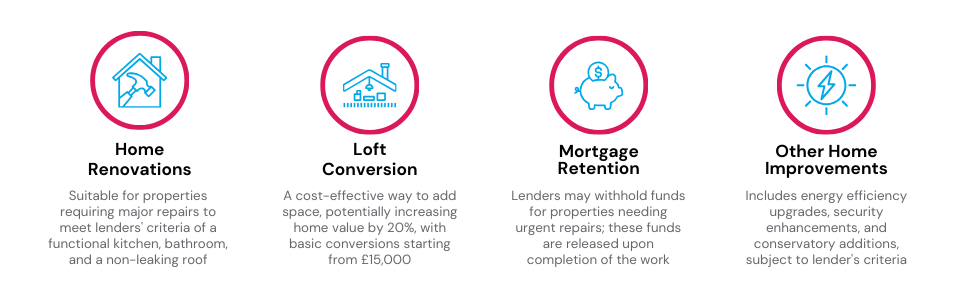

Home Renovations

Home renovations are a good option if your property needs major repairs. Remortgaging can be a strategic way to secure the funding you need for these renovations.

There are two main types of renovation scenarios:

- The property is liveable but could benefit from modernization.

- The property is considered uninhabitable by the mortgage lender.

To meet the basic criteria of a mortgage lender, a property must have a functional kitchen and bathroom, as well as a roof that does not leak.

Remortgaging for Loft Conversion

If you want to add some extra space to your home, a loft conversion might be the right answer.

First off, the cost. Basic loft conversions can start from around £15,000. If you’re planning for something more grand, like adding a large bedroom with an en-suite, it might cost you between £35,000 and £45,000.

It’s important to set a clear budget to make sure you’re adding value to your home without spending too much.

A common strategy among homeowners is to remortgage their homes before kicking off the loft conversion. This approach not only furnishes the necessary funds to get the job done but often does so at a more attractive interest rate compared to other borrowing methods.

Lastly, consider remortgaging after the conversion is done. The good news? A loft conversion could increase your home’s value by about 20%.

If that happens, you’d owe a smaller percentage of your home’s new value. This could give you access to lower remortgage rates, saving you money in the long run. It’s a smart move to consider.

Mortgage Retention

A lender may withhold some of the money they initially planned to lend you if a property valuation reveals serious issues, such as outdated electrical systems.

This is called mortgage retention, and it is done to ensure that the necessary repairs are completed. The lender will release the withheld amount once you have fixed the problems.

When planning home improvements, it is important to remember that renovations can take months or even years. During this time, your current mortgage deal may expire.

However, you can still remortgage your property even if it is still under renovation. The options available to you will depend on whether the property is habitable at that time.

Successfully completing home improvements can significantly increase the value of your property. At this point, you may want to remortgage after the renovations are complete.

This can give you access to a wider range of remortgage deals, potentially with better rates, as the loan will then represent a smaller percentage of your property’s new value.

Here are some additional things to keep in mind about mortgage retention:

- The amount of retention will vary depending on the severity of the problem.

- The lender may also require you to take out building insurance to cover the cost of any repairs.

- You may be able to negotiate with the lender to reduce the amount of retention or waive it altogether.

Other Home Improvements

In addition to extensions and renovations, remortgaging can also be used to finance other home improvements, such as:

- Energy efficiency improvements

- Security upgrades

- Adding a conservatory

The specific home improvements you can finance will depend on the lender’s criteria. It is important to speak to a mortgage broker to find out more about your options.

Other Things to Consider Before Remortgaging

If you’re considering remortgaging to finance a home extension, loft transformation, or other renovations, it’s essential to keep certain factors in mind.

Here’s a breakdown of what you should think about:

Your Equity Amount

To kick off the remortgage process, you’ll need to understand the equity you have in your home. You can determine this by deducting your outstanding mortgage from your property’s total value.

More equity can open up a broader spectrum of lenders to approach. Remember, specific lenders set a maximum loan-to-value ratio for home improvement remortgages, so familiarising yourself with these limits can help in making a well-informed choice.

Type of Property

While a majority of lenders are open to standard construction properties, those who own non-traditional homes might face restrictions.

This includes homes like studio apartments, former council flats, high-rise building flats, or properties built with unconventional materials like timber or concrete.

If your home is unique, like a barn conversion, ensure you’ve secured all necessary permissions. If in doubt, consult a broker who can link you up with specialist lenders equipped to handle unique properties.

Credit History

Having a bad credit history doesn’t mean you can’t remortgage. There are many options available, even if you’ve faced credit issues in the past.

However, the terms and deals you’ll access depend on the severity and age of these credit issues.

>> More about Remortgaging with Bad Credit

Your Age

Most lenders have a minimum age of 18 for remortgaging, but there is an increasing trend to cater to older applicants.

Some lenders do not have an upper age limit, and instead focus on your ability to manage repayments, especially if they extend into your retirement years. They will likely assess your repayment capacity against your expected retirement income.

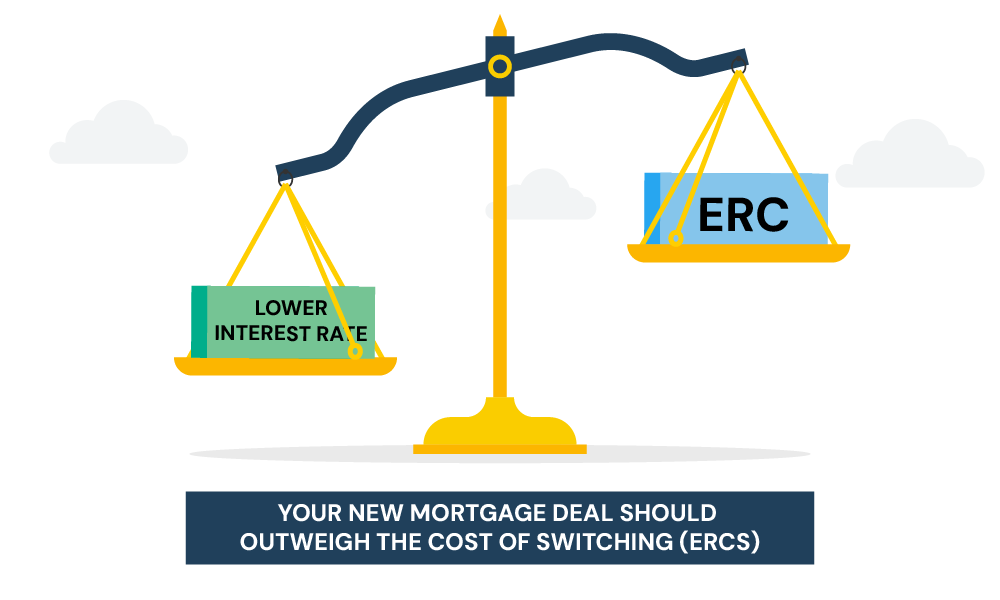

Potential Early Repayment Fees

You may remortgage while early repayment fees apply to your existing mortgage, but this may come with a hefty price tag.

That’s why it’s important to weigh up whether paying these fees now is worth it, or if it is more economical to wait until they no longer apply.

By taking these factors into account, you can navigate the remortgaging process with your eyes open and set yourself on the right track towards your home improvement goals.

Remortgaging After Home Renovations

If you have recently renovated your home, remortgaging can be a good option to borrow more money, given the increase in your property’s value.

However, there are a few things you should consider before you proceed.

First, you need to check if remortgaging is possible shortly after refinancing for renovations. Different lenders have different rules, so it is important to understand their requirements.

Second, you need to assess the changes in your loan-to-value (LTV) ratio after the renovation.

The changes in your LTV ratio may affect the types of deals available to you. It’s important to find a favourable deal that is aligned with your new LTV ratio.

It’s advisable to engage a mortgage broker who specialises in remortgaging. They can help you find the right solutions, answer your questions, and make informed decisions based on your unique circumstances.

Remortgaging after renovations is a big decision, and being well-informed can help you make the best decision for you.

Should I Consider Remortgaging?

As discussed earlier, if you have substantial equity in your property and meet the criteria for a remortgage, it may seem like a straightforward way to finance your home improvements.

However, there are some factors to consider before remortgaging, such as:

- Early repayment charges. You may have to pay early repayment charges if you remortgage before your current mortgage deal ends.

- Higher loan-to-value ratio. The higher your loan-to-value ratio, the higher your interest rate will be.

- Repayment terms. The new repayment terms may be more difficult to afford.

- Unexpected costs. There may be unexpected costs associated with the home improvements, which could require you to borrow more money.

It is important to weigh all of these factors before deciding whether to remortgage.

If you can avoid early repayment charges and you have enough equity in your property, remortgaging can be a viable option for financing home improvements.

However, it is not the only option available, and it is important to explore all of your options before making a decision.

What are the Alternatives to Remortgaging?

If remortgaging doesn’t align with your current circumstances or preferences, don’t fret.

There are other routes you might consider for securing the necessary funding and discussing these options with your broker can be beneficial. Here are a few alternatives you might contemplate:

This option acts as a supplementary mortgage, functioning as a second-charge debt behind your main mortgage.

It generally permits you to borrow a heftier sum than a remortgage would, given that the lender is assured of your ability to manage both debts.

Suitable for those unable to secure a remortgage in the immediate future but anticipate the possibility in the coming months.

This option can also serve as a contingency plan if you aim to refurbish your home to sell it or if a quick arrangement is necessary — bridging loans typically have a faster setup process than remortgages.

If you’re over 55, tapping into your home’s equity to secure tax-free funds for home enhancements might be a viable route.

Personal Loans

For individuals not keen on remortgaging or finding themselves ineligible, personal loans can serve as a handy alternative, especially if your renovation budget ranges between £25,000 and £50,000, and you can comfortably shoulder the debt.

By considering these alternatives, you can make an informed decision that suits your financial circumstances and renovation goals.

The Bottom Line

Not all remortgage deals are created equal. It’s important to do your research, crunch those numbers, and come up with the best remortgaging strategy to suit your needs.

Once you’ve made your informed move, it won’t be long till you’re sipping champagne in your stunning new home, and the dust and rubble will be but a distant memory!

Having a broker on your team can make everything smoother. They understand the market inside and out and can help find a deal that suits you perfectly, saving you time and hassle.

If you are considering remortgaging, there is no need to go it alone. Simply fill out this short form and we will connect you with a reputable remortgage broker who is skilled at simplifying the process and finding the best deal for you.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a remortgage to finance my buy-to-let property renovations?

Yes, you can remortgage your buy-to-let property to get funds for renovations. The amount you can borrow depends on the projected rental income of the property and your personal financial situation.

Lending criteria can vary, but generally, for individuals taxed at the basic rate (20%), the rental income should ideally exceed the mortgage repayments by at least 125%, assuming a 5.5% mortgage rate. This percentage may be higher for individuals in higher tax brackets.

How to remortgage my home to finance a new build?

If you have adequate equity in your home, you can remortgage it to help fund the construction of a new property. Should the equity not fully cover the building costs, it can act as a deposit, with an additional loan making up the difference.

The specific loan you’ll need hinges on your project’s scope. Typically, a deposit of 15% to 20% is expected for such ventures. If remortgaging doesn’t cover the necessary amount, you might want to consider a self-build mortgage.

Can I remortgage my fully paid house for home improvements?

Absolutely, you have the option to do this. In this scenario, you’d be looking at acquiring an unencumbered mortgage, which is essentially a loan for individuals who fully own their property but wish to free up some equity, often for the purpose of home improvements.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Do I Need To Pay Solicitor Fees When Remortgaging?

Remortgaging your home can be a smart way to reduce your monthly mortgage payments or tap into your property’s equity. But the process isn’t always straightforward. One potential cost that often confuses homeowners is solicitor fees. Do you actually need to pay for a solicitor when remortgaging? Let’s take a closer look. When Do You […]

Unencumbered Mortgage: How To Remortgage a Fully Owned Home?

Owning a property without any debts hanging over it – sounds liberating, doesn’t it? And with that freedom, you might be thinking about the different ways to make the most of your fully paid property. Maybe it’s time to fix up the house or invest in a new opportunity? In this article, we’ll break down […]

How to Remortgage to Buy a Car: A Complete Guide in 2025

Car financing options like auto loans and leasing agreements typically come with scary double-figure interest rates. This coupled with the escalating car costs can discourage you from even dreaming of buying a new vehicle. But whether you’re eyeing a sleek electric sports car or a vintage camper van, getting behind your dream wheels isn’t out […]