- Why is it Hard to Get a Mortgage when youâre Self-Employed?

- How Can You Get Mortgages as Self-Employed?

- Will Mortgage Lenders Consider You Self-Employed?

- Do Self-Certification Mortgages Still Exist?

- How Much Can You Borrow for a Self-Employed Mortgage?

- Do Self-Employed Mortgages Come with Higher Interest Rates?

- Can You Get a Self-Employed Mortgage Without Proof of Income?

- Can You Get a Joint Mortgage with a Self-Employed Worker?

- How to Boost My Mortgage Chances While Self-Employed?

- Tips for Finding the Best Mortgage Deals

- Key Takeaways

- The Bottom Line: Your Next Steps

Self Employed Mortgages: A Complete Guide

Being self-employed gives you freedom, but when it comes to mortgages, lenders see you as a higher risk. Without a fixed salary, proving your income is stable takes more effort.

You might have heard it’s harder to get approved, but it’s not impossible.

Lenders just need extra proof that you can afford the repayments. The key is knowing what they’re looking for and preparing the right documents.

This guide will walk you through how self-employed mortgages work, what lenders expect, and how to improve your chances of approval—without the jargon.

Let’s get started!

Why is it Hard to Get a Mortgage when you’re Self-Employed?

As discussed, owning your own business and being your boss has its perks, but when it comes to getting a mortgage, you may find a few more challenges in your path.

Lenders are often cautious when it comes to self-employed individuals, as there’s no guaranteed salary to fall back on. But fret not; it’s not an impossible task.

The real challenge lies in proving that your income is steady and reliable. Lenders might require more documents from you than a traditional salaried applicant, such as business accounts, tax returns, and bank statements.

You’ll also have to show future earning potential, and that might mean presenting contracts or client agreements.

Remember, it’s important to be prepared. If you’re well-organised and have all your documents in place, you’ll find that securing a mortgage isn’t as hard as it seems. It just takes a bit more effort on your part.

How Can You Get Mortgages as Self-Employed?

Getting a self-employed mortgage is about showing lenders that you have a reliable income to meet the mortgage repayments. Here’s what you’ll need to do to prove your financial stability and secure a mortgage:

1. Provide Official Company Accounts

Lenders usually ask for 2 years’ accounts, though some might approve with just 1 year.

A qualified accountant should certify your accounts to verify their authenticity. If you have three or more years of accounts with increasing profits, that will bolster your application.

2. Submit SA302 or Tax Year Overview

If you lack official company accounts, lenders may accept your SA302 documents or tax year overviews from the HMRC. These documents outline your annual income and the tax paid.

3. Show Evidence of Regular and Future Work

Having a consistent income and documented future work can strengthen your application, especially for contractors.

4. Include Retained Profits or Dividends

If you’re a company director, lenders may want to see evidence of retained profits or dividends. These financial aspects can increase your borrowing capacity.

5. Highlight Additional Income Streams

Include any other income, such as buy-to-let investments or other investments like trusts or overseas income, to enhance your affordability. Lenders may require supporting documents like tenancy agreements for additional verification.

6. Prepare a Sizeable Deposit and Maintain Good Credit

Having a substantial deposit and a good credit history is not only helpful for self-employed individuals but can positively influence any lender.

7. Ensure Correct and Up-to-Date Documents

Preparation with the right documents can save crucial time in the property-buying process, making everything smoother and faster.

By following these steps, you’ll position yourself well to obtain a self-employed mortgage. Even though the process may seem complex, proper preparation and understanding will enable success.

Working with a knowledgeable broker who specialises in self-employed applications can simplify the process.

They know what lenders are looking for and can guide you through the paperwork, helping you find the right mortgage for your situation.

Will Mortgage Lenders Consider You Self-Employed?

The way mortgage lenders perceive your employment status depends largely on your ownership stake and business structure.

If you own over 20% of a business that provides your primary income, most lenders will categorise you as self-employed.

Here’s how different business structures might affect your mortgage application:

Limited Companies

If you’re a director of a limited company, lenders typically consider your director’s salary or dividends, or both, when assessing your income.

Sometimes, they might also evaluate your company’s net profit, especially if there are significant finances retained in the business or any unusually large expenses.

This business structure is relatively straightforward, as you retain all profits.

When applying for a mortgage, make sure to present your profits in accounts and SA302 documents. These will effectively demonstrate your income to lenders.

Partnerships/LLP

Being in a partnership means profits are generally shared. Your share of the profits, reflecting how the company shares are divided, will be what lenders look at.

It’s crucial to show your exact share so that your annual income is transparent in your application.

Director of a Limited Company

Your position within the company structure will be important.

If you have a role such as a director or company secretary, the way you take income from your business, whether through salary, dividends, or both, will be closely scrutinized by lenders.

Do Self-Certification Mortgages Still Exist?

Self-certification mortgages, also known as “self-cert” mortgages, were once a unique option for self-employed individuals. These mortgages allowed you to declare your annual earnings without the need to furnish evidence.

However, in 2014, self-cert mortgages were entirely banned. The decision was driven by concerns that people were obtaining mortgages they couldn’t realistically afford.

Now, if you’re self-employed, the process to apply for a mortgage is identical to that for traditionally employed individuals.

The ban on self-cert mortgages has led to a more regulated and standardized approach to lending, ensuring both lenders and borrowers adhere to responsible borrowing practices.

How Much Can You Borrow for a Self-Employed Mortgage?

If you’re self-employed, your income and deposit size mainly determine how much you can borrow for a mortgage.

Generally, lenders might offer a loan up to 4.5 times your annual income, but this can vary based on your situation.

The deposit you set aside plays a significant role too. A substantial deposit gives you more options when you choose a mortgage deal.

Lenders have different ways to assess mortgage affordability. Some use your most recent income, while others use an average of your last two or three years’ accounts.

If you run a limited company and take a small salary while keeping more profit in the business, the calculation can become more complex.

Do Self-Employed Mortgages Come with Higher Interest Rates?

One of the common myths circling the mortgage world is that self-employed individuals face substantially higher mortgage rates.

While it’s undeniable that getting a mortgage can be a more complex process when you’re self-employed, that doesn’t mean you’ll be hit with higher interest rates automatically.

The rates depend on various factors such as your credit score, deposit, loan term, and income stability—not merely your employment status.

Lenders are in the business of assessing risk, and they’ll look at the whole picture.

If you, as a self-employed person, present a stable and low-risk profile, there’s no reason you should be offered higher rates than a traditionally employed borrower.

Can You Get a Self-Employed Mortgage Without Proof of Income?

Being self-employed without proof of income doesn’t necessarily close all doors to obtaining a mortgage.

Some lenders are willing to offer secured loans, even without standard income verification. They’ll assess your ability to repay the mortgage, ensuring responsible lending.

If you’re in a situation where you’ve accounted for only one year or haven’t filed accounts yet, it’s wise to speak with an advisor.

They can help guide you to lenders whose criteria align with your unique situation, providing you with the best opportunity to secure a mortgage.

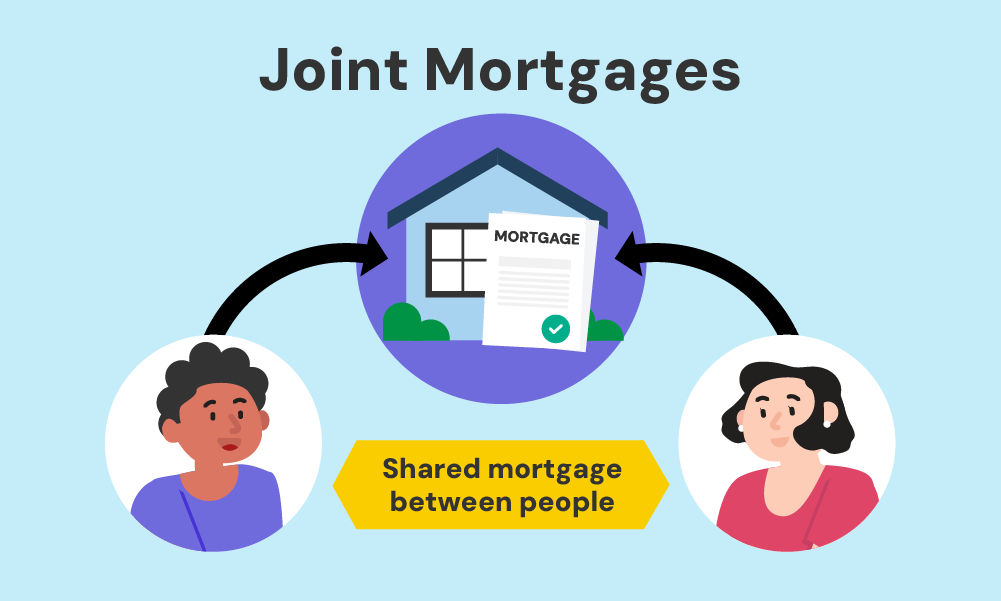

Can You Get a Joint Mortgage with a Self-Employed Worker?

Yes, obtaining a joint mortgage with a self-employed person is possible.

In a joint mortgage, both names appear on the mortgage documents, and both parties are responsible for making the payments.

Both incomes, including the income of the self-employed person, are considered when assessing the ability to buy.

The self-employed individual will need to show proof of earnings and expenses, following the same process as if applying alone.

It’s a straightforward way for both of you to work together towards homeownership.

How to Boost My Mortgage Chances While Self-Employed?

Here’s a list of practical, actionable steps you can take. Following these tips might just turn that mortgage dream into a reality:

- Keep Your Financial Records Up to Date. Consistent and clear financial records make lenders happy.

- Build a Strong Credit Score. Pay bills on time and manage your credit wisely.

- Consider a Larger Deposit. More equity means less risk for the lender.

- Show Stable Income. If possible, provide evidence of a steady income over a few years.

- Avoid Big Purchases Before Applying. Big spending might alter your debt-to-income ratio.

- Seek Professional Guidance. Mortgage brokers with experience in self-employed lending can be invaluable.

- Consider Different Lenders. Some lenders are more flexible with self-employed borrowers.

Tips for Finding the Best Mortgage Deals

Start by understanding your needs. Consider what type of mortgage fits you best, and evaluate interest rates and repayment structures. This understanding will guide you in narrowing down your choices.

Don’t overlook the power of online comparisons. Utilise websites with comparison tools that allow you to view various offers from different lenders.

Remember, the best deal doesn’t just rely on the interest rate but also factors like fees, flexibility, customer service, and a lender’s experience with self-employed borrowers.

Make sure to ask around as well. Word-of-mouth recommendations from friends or colleagues who’ve navigated similar paths can offer valuable insights.

Finally, don’t hesitate to engage with a specialist broker, especially if you’re self-employed. These experts possess the know-how and connections to navigate the complex mortgage market.

Communicate your specific requirements, and they’ll assist you in securing the deal that’s just right for you.

Key Takeaways

- Getting a mortgage when you’re self-employed can be harder because lenders need proof of stable income, but it’s not impossible with the right preparation.

- Lenders typically ask for at least one to two years of business accounts, SA302 tax forms, and bank statements to assess your income.

- A larger deposit and a strong credit score can improve your chances of getting approved and accessing better mortgage rates.

- Different business structures, such as sole traders, limited companies, and partnerships, affect how lenders calculate your income.

- Self-certification mortgages are no longer available, so all borrowers must provide proof of earnings to secure a mortgage.

The Bottom Line: Your Next Steps

Remember, there’s no one-size-fits-all solution, but these tips can undoubtedly pave the way for a successful mortgage application.

Your unique situation deserves personalised attention and tailored solutions.

If you’re ready to take the next step towards your dream home. Enquire with us or fill out this quick form, and we’ll match you with a self-employed mortgage broker who understands your needs and will guide you towards the best mortgage deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a mortgage if I'm self-employed?

Yes. While it may be a bit more challenging, many self-employed individuals successfully secure mortgages. You’ll need to provide more evidence of income, but with proper planning, it’s entirely possible.

Are the interest rates higher for self-employed mortgages?

Not necessarily. Interest rates depend on various factors like your credit score, deposit size, and the lender’s criteria. Being self-employed alone doesn’t mean higher rates.

What if I have only one year's worth of accounts or less?

Having only one year’s worth of accounts can make getting a mortgage trickier, but not impossible. You can strengthen your case by showing proof of regular work or upcoming commissions. However, your choices may be limited. Speaking with a specialist broker or your lender can reveal more options.

Can I get a mortgage when self-employed if I have bad credit?

Being self-employed with bad credit makes obtaining a mortgage harder, but it’s not out of the question. Lenders will review your credit issues and income stability before deciding. The nature of your credit issues will play a significant role in their decision.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache. Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself. But there’s good news: With the right support, YOU can switch your mortgage without a hitch. In this article, we’re going to […]

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]