- Can I Remortgage When Self-Employed?

- What Does Remortgaging Mean?

- Why Consider Remortgaging When Self-Employed?

- Remortgaging When Self-Employed: Different Scenarios

- What Should Sole Traders Know About Remortgaging?

- Insights for Company Directors on Remortgaging

- Can Contractors Remortgage?

- Top Tips for Self-Employed People Remortgaging in the UK

- The Bottom Line

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache.

Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself.

But there’s good news: With the right support, YOU can switch your mortgage without a hitch.

In this article, we’re going to break down the key things you need to know, like what paperwork you’ll need and how to find an advisor who understands the needs of the self-employed.

We’ll make it as straightforward as possible, so you can get back to running your business.

Let’s get started.

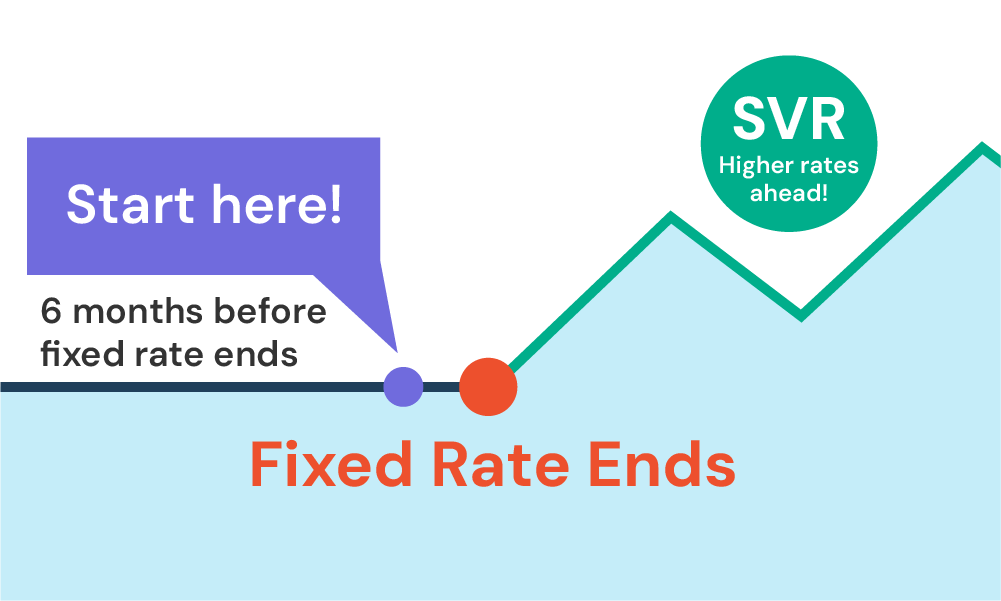

Can I Remortgage When Self-Employed?

Yes, and it’s wise to start exploring your options about 3-6 months before your existing mortgage deal wraps up.

If you’re self-employed, you might find that remortgaging comes with its own set of challenges. Standard mortgage lenders often have strict rules that can make it tough to prove you’re a reliable borrower.

But don’t worry—there’s a silver lining.

Specialist lenders are out there who focus specifically on helping self-employed people like you secure a remortgage. And there are also advisors skilled in guiding self-employed borrowers to the mortgage that suits them best.

So yes, you can remortgage when self-employed, and this article will help you understand how to go about it.

What Does Remortgaging Mean?

It’s simply the act of replacing your current mortgage with a new one. This could be with your current lender or a different one.

It’s a smart move to consider remortgaging when your initial mortgage deal is about to expire. Here’s why.

When you first secure a mortgage, lenders often offer you a discounted rate for a certain time to win you over. This is called your introductory or incentive period.

It usually lasts for 2, 3, or 5 years and offers you a lower rate than you might otherwise get.

Sounds great, but here’s the catch: once this period ends, your lender will likely increase your rate significantly.

You’ll find yourself on what’s known as the standard variable rate (SVR), and let’s be blunt—this rate is usually not in your favour.

Your monthly payments could go up without warning, and suddenly you’re paying more than you need to.

It gets worse. Many people end up staying at this higher rate simply because they don’t know any better or can’t be bothered to switch.

A study from Experian showed that 46% of mortgage holders were on an SVR, which often means they’re overpaying.

But you can avoid this trap.

Remortgaging at the end of your incentive period allows you to jump onto a new deal with another attractive rate. This could mean savings of hundreds of pounds each month and thousands for a year.

So, if you’ve been with the same mortgage for a while, it’s likely you’re on an SVR.

Our advice? Look into remortgaging soon to start enjoying those savings.

Why Consider Remortgaging When Self-Employed?

As we said, if you work for yourself and your first mortgage deal is about to end, it’s a good time to think about remortgaging. This could be a smart move if your business is doing well.

Here are some reasons why changing your mortgage could help you.

Better Loan Choices

At the beginning of your business, you might have found it hard to get a good mortgage because you were new.

Now that you’ve been running your business for a while, more lenders are willing to consider giving you a mortgage. A wider range of choices makes it easier for you to find a mortgage that suits your needs.

Chance for Lower Rates

With more lenders interested in giving you a loan, the chances of finding a lower interest rate go up.

Lower interest rates can reduce your monthly payments. This means you get to keep more of your hard-earned money.

Save Money in the Long Run

If you don’t make a change, your current mortgage will switch to what’s known as a ‘standard variable rate‘.

As discussed earlier, these rates are usually higher and can fluctuate, costing you more over time. By switching to a new mortgage, you can lock in a lower rate and save money.

Stable Payments

A new fixed-rate mortgage means your payment amount is set for a certain period.

Knowing exactly how much you’ll pay each month is a big help in planning your budget. It provides peace of mind and makes it easier to manage your finances.

By remortgaging when your business is stable and growing, you can benefit in multiple ways—from saving money to having a more predictable budget.

Remortgaging When Self-Employed: Different Scenarios

Depending on how long you’ve been self-employed, your remortgaging experience may vary. Let’s explore three common scenarios you might find yourself in.

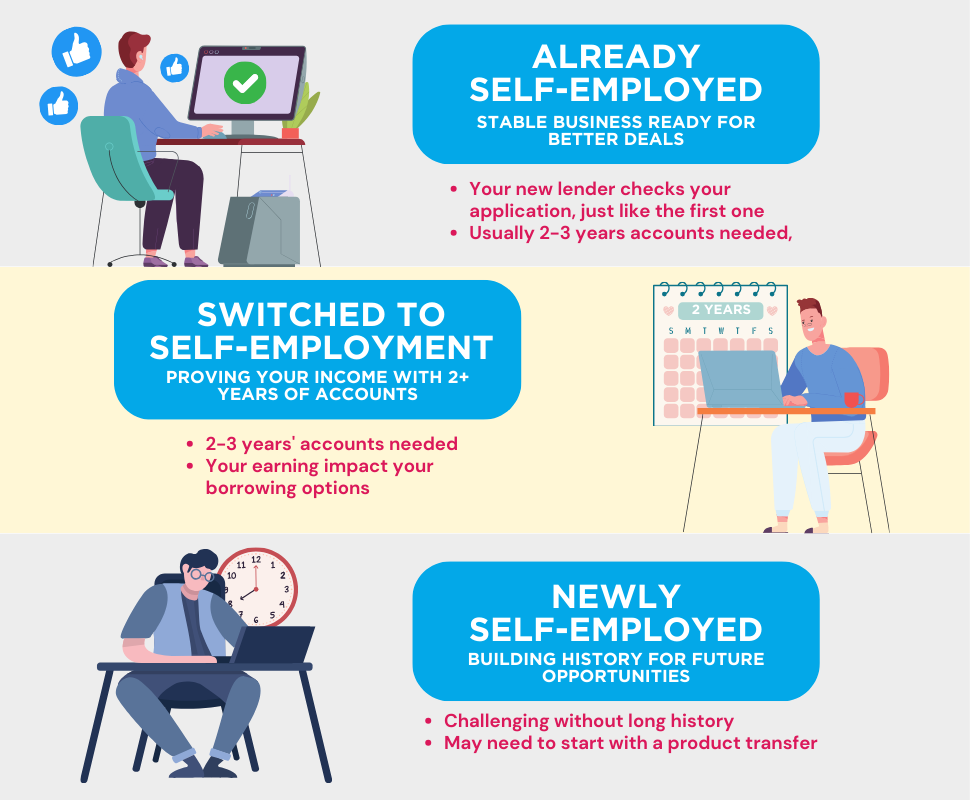

1. If You Secured Your First Mortgage While Self-Employed

If you were self-employed before you first got your mortgage, you’re ahead of the game.

A new lender will likely conduct similar checks as your initial application—such as reviewing your credit score, income, and spending habits.

With a history of being approved for a self-employed mortgage, chances are you’ll clear these checks again unless something significant has changed.

Basically, more lenders will be willing to offer you a deal, increasing your chances of landing a great mortgage.

2. If You Switched to Self-Employment After Your First Mortgage

If you’ve gone self-employed after getting your first mortgage, that’s alright. It’s especially useful if you’ve been in business for at least two years.

Being self-employed can make it trickier to show consistent income, as there’s no employer to vouch for your salary. As a result, most lenders will ask for two to three years’ worth of accounts to determine your earnings.

If you’ve been in business for at least two years, that’s a plus! Lenders are more likely to look favourably on your application.

If you’ve been self-employed for only one year, there still may be lenders willing to take a punt on you.

The catch? If you’re earning significantly less than you were before, your borrowing power might take a hit. But if you’re earning the same or even more, you should have plenty of options to nab a superb deal.

3. If You’re Newly Self-Employed

If you’re newly self-employed, you might find it challenging to remortgage with a new lender. They’ll need to perform all the usual checks on your income and expenses, which might be a problem if you can’t provide a long history of accounts.

However, if you’ve amassed a fair amount of equity in your property, some lenders might still be willing to have you.

Equity refers to the portion of your home you own outright, as opposed to the amount you owe to your lender.

Often, you might have to stick with your current lender for remortgaging.

They already know you and won’t have to scrutinise you as much, making this process known as a ‘product transfer.’

Though not ideal—you usually get better deals by switching lenders—it’s still far better than falling onto your lender’s pricier Standard Variable Rate (SVR).

So, the bottom line?

Once you’ve been self-employed for a bit longer, you can always remortgage and maybe then switch to a lender offering a sweeter deal.

To see what your potential new mortgage terms could look like, try using a remortgage calculator.

What Should Sole Traders Know About Remortgaging?

As a sole trader, you own 100% of your business and are naturally considered self-employed by mortgage lenders. These lenders usually request either:

- Detailed accounts from the past two to three years, or

- Your most recent SA302 forms, which outline your yearly tax situation.

Having a few years of self-employment under your belt can give you an advantage when looking to remortgage, as it provides lenders with a clearer picture of your financial stability.

Insights for Company Directors on Remortgaging

If you’re a company director, the remortgaging process might involve a few extra steps. Lenders commonly request:

- Business accounts or SA302 forms for tax assessment,

- Proof of dividends you’ve received, and

- Details on retained profits in your company account.

Be cautious if you keep your salary low for tax benefits, as it might make your income appear lower than it is.

Some lenders do factor in retained profits when assessing your income. If you’re in this category, find a lender who does so to get a more accurate and, often, more favourable mortgage deal.

Can Contractors Remortgage?

If you’re a contractor with a limited company, you’re in the same boat as other company directors when it comes to remortgaging.

One challenge you might face is the ups and downs of contract work. Your income might not be steady, and this can make some lenders hesitant. They worry you might miss payments if you’re between contracts.

But don’t stress. Many lenders are open to contractors. So, remortgaging might be easier than you think.

Remember, whichever category you fall into, a good mortgage advisor can help guide you to the right lender for your unique needs.

Top Tips for Self-Employed People Remortgaging in the UK

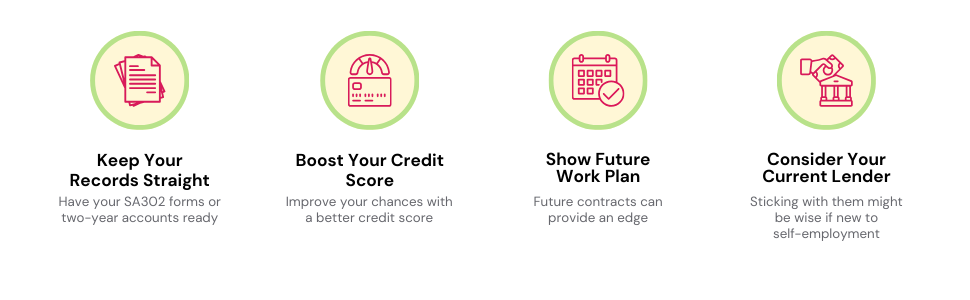

If you work for yourself and it’s time to look at new mortgage options, here are some key steps to make sure you get a good deal.

1. Keep Your Records Straight

It’s crucial to have your SA302 forms or two years of accounts ready. These papers show how much money you make.

Get them in order early, so you’re ready when you apply for a new mortgage. If you’re not sure about the paperwork, an accountant can help.

2. Boost Your Credit Score

Lenders will look at your credit score to see if you’re reliable. The better your score, the better your chances.

Pay off any debts you have and try not to take out any new loans for now. That new car might need to wait.

>> More about How to Improve Your Credit Score

3. Show Future Work Plans

If you can, show lenders contracts for future work. It may not replace the need for SA302s, but it can give you an edge. If lenders are on the fence, this could tip the balance in your favour.

4. Consider Your Current Lender

Switching lenders often gets you the best deal, especially if you have all your accounts and records in order.

But if you’re new to being self-employed, other lenders might not take the risk. In that case, you can stick with your current lender. It might not be the best deal, but it’s better than ending up on a high Standard Variable Rate.

If you follow these tips, you’re likely to get a mortgage deal that suits you well. It may sound like a lot, but the savings make it all worthwhile.

The Bottom Line

If your first mortgage deal is almost over, or you’re on a high Standard Variable Rate, it’s time to think about a new mortgage. The first step is talking to a mortgage broker.

A good mortgage broker is someone who helps you find the best mortgage for you. They look at all the options and tell you which one suits your needs. They’ll even handle most of your remortgage application, streamlining the process for you.

This is even more important if you work for yourself. Each lender has their own rules for self-employed people. A good broker knows these rules and can find the best lender for you.

So, if you’re self-employed and need to remortgage, a broker can help. They make the process easier and find the best deal for you.

Ready to take the next step? Fill out our quick form online. We’ll connect you with an advisor who knows how to help self-employed people like you. They will present you with remortgage options tailored to your income.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I remortgage without showing proof of income?

If you’re self-employed, you usually need to show income to get a remortgage. Lenders often won’t approve you if you’ve been self-employed for less than a year.

But a broker might find a lender who will start your application after you’ve been self-employed for nine months. You’ll still need to wait until you hit the one-year mark to close the deal.

Do I need to make a deposit to remortgage when self-employed?

No, you usually don’t need to make a new deposit when remortgaging. The equity you’ve built up in your home generally takes the place of a deposit. The more equity you have, the better your chances are of securing a favourable deal.

What specific documents do I need to prepare to remortgage as self-employed?

You’ll need to gather a range of documents. These typically include:

- Two to three years of tax returns (SA302 forms if you’re in the UK)

- Business accounts, usually going back 2 or 3 years

- Bank statements for both your business and personal accounts

- Identification documents, like a passport or driving licence

Having these papers ready can make the process go smoother and quicker!

Are there eligibility criteria when remortgaging if self-employed?

Yes, there are specific criteria. Lenders usually want to see a stable income and that you’ve been in business for at least 2 to 3 years. Your credit score also matters. If you’ve got a dodgy score, you may find fewer options or higher interest rates.

Is it harder to remortgage when self-employed?

Yes, it can be more challenging but it’s not impossible. Being self-employed means your income might vary, making lenders a bit cautious.

You’ll need to provide more proof of income compared to someone who is traditionally employed. But don’t worry, if you’ve got your ducks in a row, especially your financial documents, you should be able to find a lender willing to work with you.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]

Getting Self-Employed Mortgages After a Seiss Grant in the UK

If you’re a self-employed individual who’s received support from the Self-Employment Income Support Scheme (SEISS), you might be worried about how it affects your chances of securing a mortgage. With news about refused mortgages due to self-employment grants making the rounds, it’s easy to feel uncertain. However, the reality is more optimistic: receiving a SEISS […]