- What Is Debt Consolidation?

- The Benefits Of Debt Consolidation

- The Potential Downsides Of Debt Consolidation

- Who Should Think About Debt Consolidation?

- What Fees And Charges Apply?

- Debt Consolidation Lenders To Consider

- The Debt Consolidation Process Explained

- What Debts Should You Prioritise Consolidating?

- Consolidation Loan Warning Signs To Be Aware Of

- How To Safeguard Your Finances After Consolidating

- Debt Management Plans Compared To Consolidation Loans

- Is Debt Consolidation Right For You?

- The Bottom Line

The Pros And Cons Of Debt Consolidation

If you’re struggling with multiple credit card, loan or overdraft payments every month, debt consolidation may seem an attractive option.

The idea is to roll all your debts into one new loan, with lower interest, simpler repayments and potential long-term savings.

But consolidation carries risks too. This direct guide examines the key pros, cons and alternatives you need to consider before deciding if consolidating debts is right for your situation.

What Is Debt Consolidation?

Debt consolidation involves taking out a new loan to repay multiple existing unsecured debts like credit cards, store cards, overdrafts and personal loans.

The aim is to merge numerous debts into one easy monthly repayment. Consolidation loans are usually unsecured, meaning no assets are used to guarantee the borrowing.

As a result, interest rates are higher than secured lending like mortgages, but can still be lower than expensive credit card rates.

The most common debt consolidation solutions are:

- Personal loans – Offered by banks, building societies and online lenders from £1,000 up to £25,000 or more.

- 0% balance transfer credit cards – Shift credit card balances to a new card offering 0% interest for a set period, usually 6-29 months.

- Secured loans – Using property equity to guarantee a lower-interest consolidation loan. Risks of losing your home if repayments are missed.

- Peer-to-peer loans – Borrowing from investors via online platforms. Often higher rates than banks.

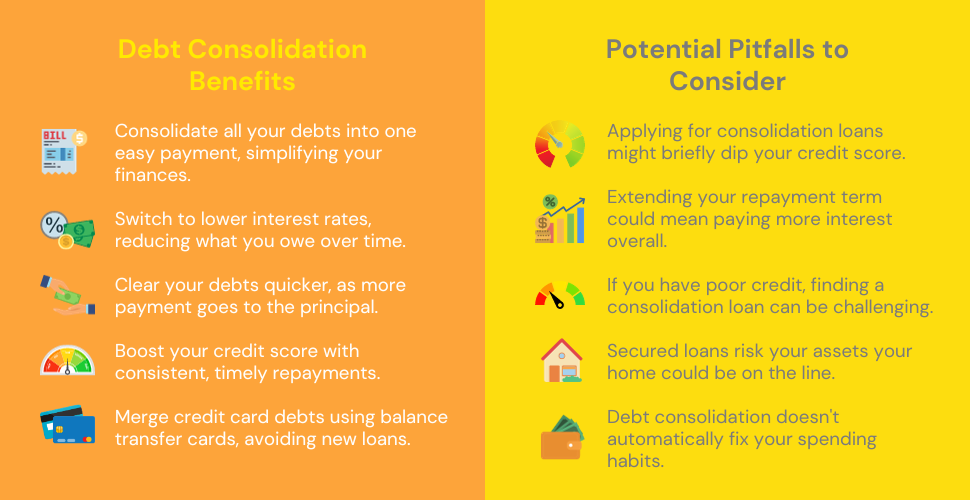

The Benefits Of Debt Consolidation

Simplifying Multiple Payments Into One

Juggling lots of credit card and loan payments every month can be a real headache and mess up your budgeting.

Debt consolidation rolls all these debts into just one repayment plan with one lender.

This means you only have to remember one payment date and deal with one lender, which makes things a lot simpler and helps you avoid missing payments that can hurt your credit score.

Grabbing a Lower Interest Rate

One big plus of consolidation loans is getting a better interest rate than what you’re paying on credit cards or overdrafts.

For instance, moving a credit card debt with a 22% APR to a loan with a 9% APR can save you loads of interest over the loan’s life. This means you’ve got more cash to chip away at the actual debt quickly.

But remember, it’s smart to shop around for interest rates.

Paying Off Debts Quickly

With lower interest rates, more of your monthly payment goes towards knocking down the debt, not just paying interest. This means you can clear your debt faster.

And if you’ve got extra cash, many lenders let you pay off more or even settle the whole loan early. Just check the terms of your loan first.

Protecting Your Credit Rating

Missing a bunch of credit cards and loan payments can damage your credit score. This makes getting loans in the future tougher and more expensive.

A consolidation loan that you can comfortably pay back each month helps you avoid missed payments and can even boost your score over time.

Consolidating Without Extra Borrowing

Consolidation often means getting a new loan, but balance transfer credit cards let you combine credit card debts without extra borrowing.

These cards pay off your old debts, and you can get deals with 0% interest for up to 29 months. This helps you pay back what you owe without interest piling up during the offer period.

The Potential Downsides Of Debt Consolidation

Credit Score Damage From New Applications

Applying for loans or credit cards means a ‘hard’ credit check, which can drop your score a bit. If you get turned down a lot, it gets worse.

You can check your chances with ‘soft’ checks that don’t hurt your score. Or, try to improve your credit rating before applying.

Paying More Interest in the Long Run

Even though consolidation loans have lower rates, stretching out payments over several years can mean paying more interest overall than you would on credit cards.

Always work out the total interest you’ll pay over time, not just the main rates. Paying more each month can cut down on interest costs.

Loan Rejection With Poor Credit

If you’ve missed payments or have defaulted in the past, getting a consolidation loan might be tough, even with an average credit score.

There are loans for bad credit applicants, but they often come with higher interest rates. Improving your credit score is key to getting better loan terms.

Secured Loan Risks Losing Your Home

If you take a secured loan, using your house as collateral, you might get a lower interest rate. But be careful – if you can’t keep up with payments, you could lose your home.

Doesn’t Fix Spending Habits

While simplifying repayments, debt consolidation alone does not address the overspending habits that caused debt in the first place.

Without changing spending behaviour, you risk racking up new credit card debts.

Who Should Think About Debt Consolidation?

Debt consolidation isn’t a one-size-fits-all solution, but it does work wonders for certain types of people in the UK. Here’s who it suits best:

- Folks Who Struggle with Lots of Small Payments. If you find it tough to keep track of all those minimum payments every month, rolling them into one could make your life a lot easier.

- Those with a Good Credit Score. Having a decent credit rating boosts your chances of getting approved for a consolidation loan.

- People Who Can Handle the Monthly Payments. It’s important that you can realistically afford the monthly repayments based on what you earn.

- Keen on Cutting Down Interest Costs. If you’re more interested in reducing what you pay in interest over time, rather than just getting a loan with a low APR, consolidation could be a smart move.

- Ready to Change Spending Habits. It works well for people who are willing to close the accounts they’ve paid off and are serious about cutting back on spending.

Remember, while debt consolidation can give you a bit of breathing space in the short term, it’s not a magic fix.

To get on top of your debts in the long run, you’ll need to live more frugally, keep a tight leash on your spending, and maybe even find ways to boost your income.

What Fees And Charges Apply?

While a consolidation loan often has lower interest costs than individual debts, watch out for these common fees:

- Arrangement fee – One-off upfront admin fee added by lenders (1-2% of the loan amount).

- Early repayment charge – Exit penalty if you repay the loan faster than scheduled.

- Missed payment fee – Around £12+ for each late monthly repayment.

- Balance transfer fee – Approx 1-5% to shift credit card debt to a 0% deal.

- Consultation Fees – Some places charge a fee just for setting up your loan.

Remember, these fees can add up, so make sure consolidating your debt saves you money in the long run. Always check the small details of the loan to understand all the costs.

Debt Consolidation Lenders To Consider

Most major banks, building societies, credit card providers and online lenders offer debt consolidation loans if you meet their affordability criteria. Interest rates and fees vary by lender. Here are some lenders to consider:

- HSBC – Offers personal loans ranging from £1,000 to £25,000 for non-Premier customers and up to £50,000 for Premier customers, with repayment terms of 1 to 8 years.

- Barclays – Provides personal loans with a maximum repayment term of 5 years.

- Halifax – Offers loans up to £50,000 for current account holders and up to £25,000 for non-account holders, with repayment periods from 1 to 7 years.

- NatWest – Provides loans ranging from £1,000 to £50,000, with repayment periods varying from 1 to 10 years, depending on the loan amount and purpose.

- Nationwide – Offers loans from £7,500 to £25,000, with a repayment period of 1 to 7 years.

- MBNA – Offers 0% interest on balance transfers for 27 months, with a representative APR of 23.9% (variable).

The Debt Consolidation Process Explained

Getting approved for a consolidation loan depends on your creditworthiness and income. Here are the key steps:

- Check Your Credit Report First. Before starting, check your credit report for any errors. Mistakes can impact your loan eligibility, so it’s important to fix them before applying.

- Work Out How Much You Owe. Total up all the debts you’re planning to consolidate. This figure will be the amount you need to borrow through the consolidation loan.

- Shop Around for the Best Rates. Research interest rates offered by various lenders, including banks, building societies, credit card companies, and online lenders. Comparing these will help you find the most cost-effective option.

- Pick a Lender and Apply. After comparing rates and fees, select one or two lenders that offer the best terms. Complete their application forms accurately, providing all the necessary financial information.

- Get the Money and Pay Off Debts. Once approved, the lender will deposit the loan amount into your bank account. Use this money to pay off all the debts you’re consolidating. Remember to close these accounts once they’re cleared.

- Understand the Terms and Conditions. It’s crucial to fully comprehend the terms of the loan, including repayment schedules, interest rates, and any fees or penalties.

- Create a Repayment Plan. Develop a strategy for making the monthly payments. Setting up direct debits can help ensure timely payments, which is vital for maintaining or improving your credit score.

- Consider Seeking Financial Advice. If you’re uncertain, consider consulting a financial advisor. They can guide whether debt consolidation is suitable for you and assist in navigating the process.

- Monitor Your Finances After-Consolidation. After consolidating, keep a close watch on your financial situation. It’s essential to avoid accumulating new debt, so stick to a budget and save where possible.

- Evaluate Your Spending Habits. Finally, use this opportunity to assess and adjust your spending habits. Sustainable financial health requires not just consolidating debts but also adopting responsible spending behaviours.

What Debts Should You Prioritise Consolidating?

With a consolidation loan limited to an amount you can realistically repay each month, you may be unable to consolidate every debt. Prioritising is key:

- Focus on high-interest debts – Pay off credit cards, overdrafts and loans over 15% interest first to maximise savings.

- Pay minimums on low-rate debts – Leave out student, car and mortgage loans under 10% interest.

- Clear recent missed payments – Get up-to-date on newly missed credit card or loan payments to aid credit rating recovery.

- Consider emotional debts – Repay nagging debts causing stress like payday loans first, even if rates are lower.

Consolidation Loan Warning Signs To Be Aware Of

While consolidation appears a logical solution for many people on paper, there are warning signs indicating it may be unwise or risky:

- Monthly repayments remain unaffordable based on disposable income.

- Loan rates offered are higher than current debt interest rates.

- You may be tempted to rack up card balances again after consolidating.

- Loan rejection seems likely due to credit history issues.

- Overspending issues remain unresolved.

If one or more apply to you, debt consolidation may not be advisable until you get expert debt advice.

How To Safeguard Your Finances After Consolidating

Consolidation provides temporary relief. Avoid spiralling back into debt by:

- Sticking to a strict monthly budget.

- Building an emergency savings fund.

- Avoiding unnecessary spending and impulse purchases.

- Freezing and closing paid-off credit card accounts.

- Tracking loan repayment progress.

- Increasing income with a second job if possible.

Debt consolidation alone is not a long-term solution. Changing money habits is critical.

Debt Management Plans Compared To Consolidation Loans

Debt management plans (DMP) from non-profit agencies offer an alternative way to combine debts into one lower monthly payment, compared to consolidation loans:

Pros

- No loan or credit checks are required.

- Interest is frozen on debts in a DMP.

- More affordable payments tailored to income.

- Free debt counselling services are included.

Cons

- Debts take longer to fully repay (5-7 years typically).

- Missed DMP payments show on the credit file.

- Creditors must agree to the proposed DMP terms.

- Limited types of debt can be included in a DMP.

For some, the pros of DMPs make them a safer debt solution versus taking out consolidation loans.

Is Debt Consolidation Right For You?

There is no one-size-fits-all answer about debt consolidation being right for you or not. It requires weighing up the pros and cons of your unique situation.

The decision depends entirely on your circumstances – your income, debts, credit score and willingness to curb overspending.

But by understanding the key benefits, risks and alternatives covered here, you are now armed with the knowledge to make an informed decision about debt consolidation.

The Bottom Line

Debt consolidation can provide short-term relief but is not a total solution. For ongoing debt support tailored to your specific situation, speak to a qualified mortgage broker for free and personalised advice.

To discuss mortgage options that could help long term with reducing debt repayments, get in touch to be matched with a specialist mortgage broker.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Does debt consolidation damage your credit rating?

Consolidation won’t damage your credit rating provided you maintain monthly repayments. Repaying on time can improve it over the long run.

The only risk is short-term score drops from applying for new credit like loans and cards to consolidate debt.

When is debt consolidation advisable?

If you have good credit, affordable repayments, high-interest debts and are motivated to tackle overspending, consolidation can help. Seeking expert debt advice first is still recommended.

Are there alternatives to consolidation loans?

Yes, options like 0% balance transfer cards, debt management plans, debt charities and changing money habits can also provide debt relief.

Can I consolidate with very poor credit?

You can still potentially consolidate with poor credit through subprime lenders. However, this carries risk with higher interest rates. Non-profit debt advice is recommended first.

Related Articles

Should You Get A Santander Debt Consolidation Loan?

If you’re thinking about consolidating your debts, you’re probably on the lookout for a reputable lender. You may have come across Santander’s debt consolidation loans and wondered about their trustworthiness, especially given their recent troubles with the Financial Conduct Authority (FCA). Santander UK was fined a hefty sum for shortcomings in its anti-money laundering controls. […]

Should You Get an RBS Debt Consolidation Loan? A Closer Look

Managing debt can be an overwhelming task. With bills piling up and interest accumulating, it’s easy to feel like you’re drowning financially. But, RBS offers debt consolidation loans that could provide you with a life raft. By rolling multiple debts into one manageable payment, these loans aim to rescue borrowers from choppy credit waters. This […]

Should You Get a NatWest Debt Consolidation Loan?

Debt consolidation provides temporary relief by reducing chaotic payments into one. But loans must still be repaid. If you’re considering this path to simplify your debts, NatWest’s Debt Consolidation Loan might be on your radar. As you navigate the complex world of financial decisions, it’s crucial to have all the facts at your fingertips. This […]