- What is a Secured Loan?

- How Do Secured Loans Work?

- What If I Default on a Secured Loan?

- Whatâs the Difference Between Secured & Unsecured Loans?

- What Do You Need to Get a Secured Loan?

- How Much Can You Borrow with a Secured Loan?

- Advantages of Secured Loans

- Disadvantages of Secured Loans

- Exploring Types of Secured Loans

- What are the Secured Loan Interest Rates?

- Is it Easy to Get a Secured Loan in the UK?

- What Should You Think About Before Getting a Secured Loan?

- Alternative Routes

- Can I Get a Secured Loan with a Bad Credit?

- Key Takeaways

- The Bottom Line

Secured Loans Explained: How Do They Work?

If you have something valuable, like a home or a car, did you know that you can use it to secure a loan?

This can be a lifesaver, especially if you need a large amount of money, desire a longer repayment term, or find it challenging to get approval for a personal loan.

But there’s a catch.

Secured loans do come with the risk of losing your precious assets. Therefore, you must be well informed before you take the plunge.

Let’s dive into the details.

What is a Secured Loan?

You might have heard them referred to as homeowner loans, home loans, or second-charge mortgages.

Secured loans are a way that lets you borrow a substantial sum by using your home as a sort of guarantee, often termed as ‘collateral’ or ‘security’.

It’s a pact that allows the lender to sell off your house if, unfortunately, you can’t keep up with the repayments.

Sounds a bit scary, doesn’t it? But as long as you are well-prepared, secured loans can be a solid financial choice.

How Do Secured Loans Work?

Just like most other loans, with secured loans, you’ll be paying back the amount you borrowed in fixed monthly instalments, with a bit of interest added on top. This interest rate could either remain constant or vary throughout the loan term, based on the kind of loan you’ve settled for.

And here’s the good news: as long as you’re diligent about making full repayments on time every month, your home stays yours, safe and secure.

What If I Default on a Secured Loan?

We know it’s not something anyone wants to think about, but it’s important to know what happens if things don’t go according to plan.

Defaulting on a secured loan is serious business. Your lender can legally take ownership of your home, potentially selling it to recover the money you owe them.

The silver lining here is that you usually can arrange an alternative payment plan with the lender if you get in touch as soon as you realize you’re facing difficulties.

Remember, defaulting has additional repercussions. It usually ends up marking your credit report, bringing down your credit score, and making it a bit more difficult for you to borrow money in the future. It’s always best to avoid a default.

What’s the Difference Between Secured & Unsecured Loans?

Unsecured loans, also known as personal loans, don’t involve your home or any other assets as a backup for the lender. Because of this, these loans are perceived as a higher risk by lenders, necessitating a good credit score for approval.

You see, a good credit score is like a trust badge that reassures lenders you’re pretty good at paying back what you owe.

Whether you opt for a secured or an unsecured loan, you’ll be agreeing to specific repayment terms including interest rates and the repayment duration. And just so you know, credit cards are another form of unsecured credit. They allow you a revolving credit facility where you borrow and repay varying amounts each month.

What Do You Need to Get a Secured Loan?

To get a secured loan, you first need a valuable asset that you own, such as a home, car, or piece of jewellery, which will serve as collateral for the loan. The value of this asset should be substantial enough to cover the amount you intend to borrow.

Before approving your loan, lenders will conduct an affordability check to ensure that you can comfortably meet the monthly repayments. They will assess factors like your income and credit history.

Even though your asset acts as a security net for the lender, maintaining a steady income and a good credit score can work in your favour, potentially landing you more favourable terms.

Remember, the ultimate goal is to manage the loan responsibly to avoid the risk of asset repossession in extreme cases.

How Much Can You Borrow with a Secured Loan?

The amount you can borrow with a secured loan depends on the value of the asset you use as collateral. If you use your home as collateral, you may be able to borrow a large sum, up to £100,000 in some cases.

However, it is important to remember that borrowing a large sum of money comes with risks. If you cannot make your payments, you could lose your home.

As a general rule, you should aim to borrow the least amount you need for the shortest period. This will help you minimize the costs of the loan.

Advantages of Secured Loans

Secured loans have quite a few benefits that might attract you. Let’s dive into them:

- Larger Borrowing Capacity. You can usually borrow much more than personal loans, sometimes even exceeding £100,000. Handy, isn’t it? Especially for big projects or hefty education costs.

- Extended Loan Duration. Imagine not having to worry about hefty monthly payments! You can spread your loan over several years, making the monthly fees more manageable compared to personal loans.

- Easier Approval with Bad Credit. If your credit score isn’t great, don’t worry. Secured loans could still be within your reach since your property serves as a security net for lenders.

Disadvantages of Secured Loans

However, secured loans aren’t all sunshine and rainbows. Here’s what you should be cautious about:

- Risk of Losing Your Asset. If, for any reason, you can’t keep up with your payments, the lender might take over your property to recover your money.

- Higher Overall Interest. While you get the comfort of lower monthly payments, the longer loan term means you end up paying more interest in the long run.

- Early Repayment Charges. Thinking of settling your loan earlier than agreed? Be prepared to face some early repayment fees which can sometimes be as much as 1-3 months of interest.

Exploring Types of Secured Loans

Before you settle on a decision, let’s navigate through the different types of secured loans available to you:

- Homeowner Loans – This type of loan utilises your home as a guarantee, posing a risk of losing it if you default on the payments.

- Logbook Loan – Here, your vehicle serves as the loan security, with the lending party holding ownership until you clear the debt.

- Mortgages – Primarily for buying properties or lands, where you partially pay a deposit and cover the rest through a loan. Be cautious, as failing repayments could lead to home repossession.

- Second-Charge Mortgages – This operates separately from your primary mortgage, leveraging your home’s equity to fund improvements.

- Bridging Loans – Particularly handy when transitioning between properties, allowing you to deposit on your new home while waiting for the current one’s sale.

- Debt Consolidation Loans – Simplify your financial obligations by consolidating various debts into a single payment with a potentially lower interest rate.

- Guarantor Loans – In this arrangement, a close one assures your loan repayments, potentially pledging their home as security.

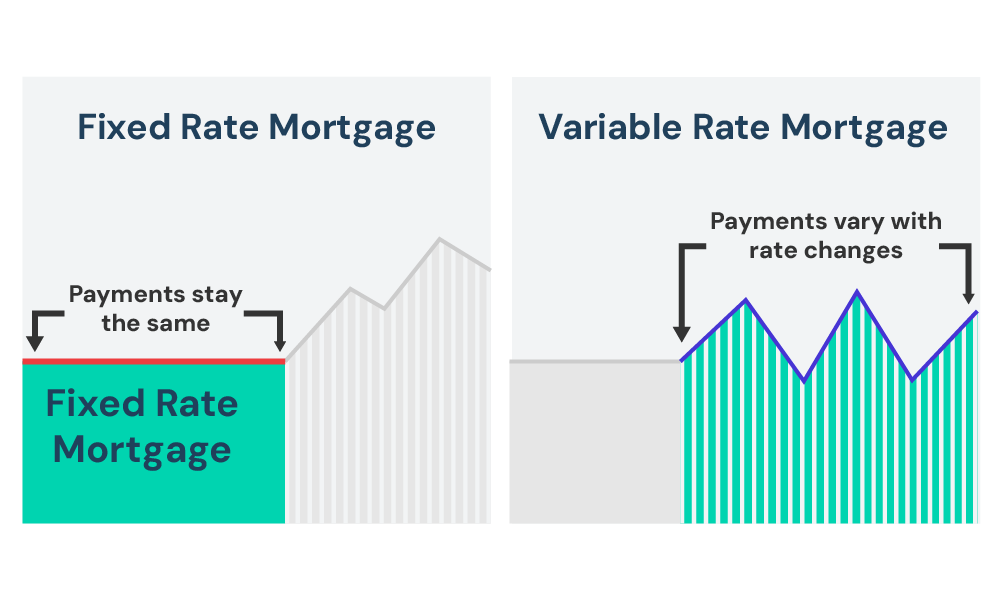

What are the Secured Loan Interest Rates?

When sifting through loan options, you generally encounter:

- Fixed for Term – Offers a stable interest rate throughout the loan period.

- Short-Term Fixed Rate – Provides a stationary interest rate for a set introductory period, later shifting to a standard variable rate.

- Variable Rate – Here, the interest rate varies, aligning with the Bank of England’s base rate, meaning it can increase or decrease.

Is it Easy to Get a Secured Loan in the UK?

Generally, yes! Since your home serves as collateral, lenders often feel more secure in loaning you the amount, even if your credit history isn’t stellar.

So, if you’ve faced rejections for other types of credit and you own a home, secured loans might be an attractive option for you.

What Should You Think About Before Getting a Secured Loan?

Secured loans are a serious commitment. Here are a few things to consider before taking the plunge:

Can You Afford It?

Take a hard look at your bank balance and potential future spending. This isn’t just about whether you can afford the monthly payments now but if you’ll be able to keep up with them in the future.

Picture your life a few years down the line – maybe with a new home or a bigger family – and make sure you can still make those payments comfortably.

How Much Is Your Home Worth?

When you ask for a secured loan, the lender will want to know the real value of your home and how much you still owe on it.

This gap, known as equity, will help them decide how much they can safely lend you. Generally, the more equity you have, the larger the loan you can ask for.

Understanding Interest Rates

When it comes to secured loans, the interest rates can go up and down. So, when figuring out what you can shell out every month, keep in mind that these rates might increase.

Also, check the Annual Percentage Rate of Charge (APRC) to understand the loan’s total cost, as it adds up all the fees and the interest rate.

Remember, the initial rate you see might not be what you get in the end; it depends on several factors like your credit score and how much you want to borrow.

Pro Tip

Before plunging into a secured loan, consult with a loan advisor to evaluate the best options for your circumstances. Additionally, maintain a healthy credit score to possibly secure better interest rates.

Alternative Routes

For hefty loans that might go up to £25,000 or sometimes even £50,000, personal loans stand as your only realistic option. Especially if you have a good credit score and steady income that demonstrates your ability to repay.

For smaller sums, you could explore options such as 0% or low-interest credit cards or overdrafts, which can serve as economical borrowing solutions when used judiciously.

Can I Get a Secured Loan with a Bad Credit?

Yes, you can.

Securing a loan is potentially easier with bad credit when compared to a personal loan. When you apply, lenders assess their risk of potential non-repayment. A lower credit score might portray you as a higher risk based on past borrowing history.

Yet, the collateral in secured loans offers lenders a safety net, making them more flexible during the affordability checks. However, they remain keen on confirming your ability to manage the monthly dues.

Another alternative is the guarantor loan, where a person with substantial credit vouches for your loan, reducing the lender’s risk and increasing your chances of approval.

Key Takeaways

- Use assets like a home or car as collateral to secure a loan, potentially allowing for larger borrowing amounts and longer repayment terms.

- Be well-informed and prepared before opting for a secured loan to avoid the risk of losing your valuable assets.

- It’s possible to arrange alternative payment plans with the lender if you face difficulties in repaying, preventing severe consequences like asset repossession.

- Compare secured loans with unsecured loans, considering your financial circumstances, borrowing needs, and credit score before making a decision.

- Consult a financial advisor to explore and understand the diverse secured loan options available, including the different types of loans and the varied interest rates.

The Bottom Line

Securing a loan using your valuable assets can be a viable financial avenue, especially if you’re looking to borrow a substantial sum.

Remember, being well-prepared and informed is the key to making smart financial decisions.

Ready to take the next step? Enquire with us today, and we’ll connect you with a secured loan advisor to guide you in making the best financial choices for your life.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What kind of credit score do I need to apply for a secured loan?

The necessary credit score for a secured loan can differ between lenders. Even with a low credit score, you might still secure a loan, but having a higher score can unlock better rates, making your loan more affordable.

Is early repayment of a secured loan possible?

Yes, you have the option to settle the loan earlier than the agreed term. However, be mindful that this could entail early repayment fees, which might negate the benefits of early settlement.

Which is the better option: a secured loan or an unsecured loan?

The better choice between a secured and an unsecured loan hinges on your borrowing needs and your current financial standing. If you are dealing with a less-than-perfect credit score, own property, and intend to borrow a significant amount, a secured loan might be worth considering.

Conversely, if your credit score is good and you need to borrow a sum less than £25,000, a personal loan might be the better route.

Can I secure a loan using my car as collateral?

Yes, these are referred to as logbook loans. To qualify, you need to fully own the car and its value should exceed the loan amount. Keep in mind, that these loans can be costly, and the lender will have ownership of the car until you clear the entire loan.

Is it possible to use my pension to secure a loan?

Yes, using your pension as collateral for a secured loan is an option. However, it’s generally a pricey borrowing method and might necessitate acquiring life insurance as part of the loan process.

Related Articles

Secured Loan Calculator – No Personal Details Required

If you’re sitting on a valuable asset like a home, why not put it to work for you? Secured loans can open doors to more funds, better repayment terms, and even loan approval when all other avenues fail. But remember, there’s a flip side: you could lose your prized asset if you don’t keep up […]

Loans for Pensioners: How to Get the Cash You Need?

Suppose you’ve reached retirement and find that, despite having assets in property or a robust pension plan, your daily cash flow isn’t quite as fluid. In that case, you may contemplate taking out a loan for things like home renovations, a new car, or even a well-deserved holiday. And why not? If you have a […]

How To Get a Secured Loan If You’re Self Employed

Starting a business takes courage, hard work, and, let’s be honest, money. Whether you want to launch a new product, buy better tools, or make your workspace bigger, a secured loan could help you make it happen. Finding a loan when you don’t have a regular job can feel tricky. But here’s the good news: […]