In the UK, many of us struggle to find reliable financial advice. The search for the right professional is often time-consuming, stressful, and confusing. And let’s be honest, if you’re a busy person—handling finances can feel like one of those tasks you’d rather avoid. Whether it’s hunting for the best mortgage deal, sorting your taxes, […]

Blog

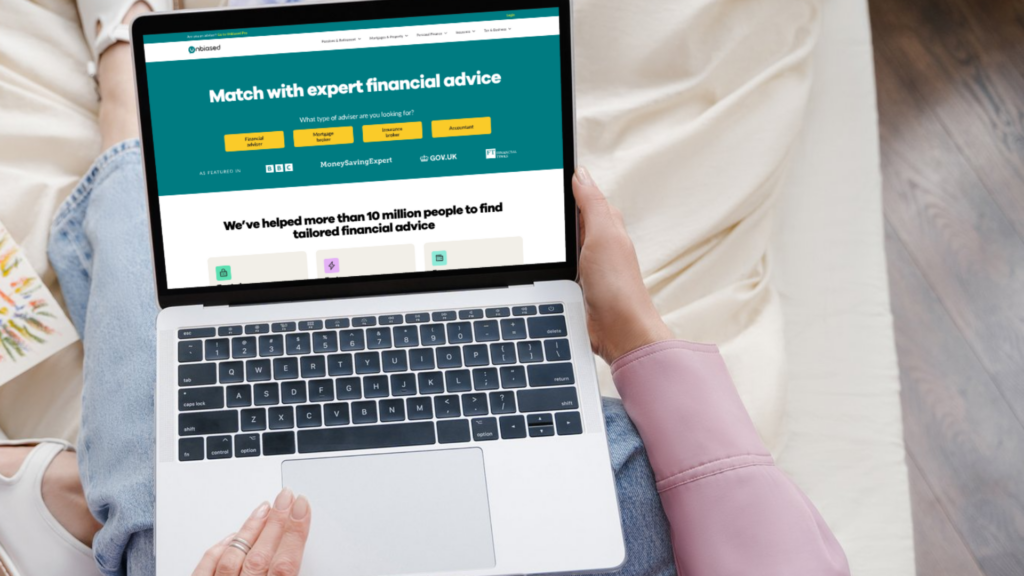

Unbiased Reviews: Honest Insights You Need to Know

Habito Review: An Honest Take on Their Digital Services

Sorting out a mortgage is never fun – especially for first time buyers. It’s often confusing, stressful, and full of endless paperwork. Thankfully, times have changed. Just like you can now order groceries or book holidays online, you can secure your mortgage online too. No more long appointments or waiting weeks for updates. Online mortgage […]

Better.co.uk Review: Honest Insights on Their Services

Let’s face it, finding the right mortgage can be a time-consuming headache. Between dealing with endless lenders and trying to decode all the jargon, it’s enough to make anyone’s head spin. Add work, family, and everything else life throws your way, and it’s no wonder it feels overwhelming. This is where mortgage brokers like Better.co.uk […]

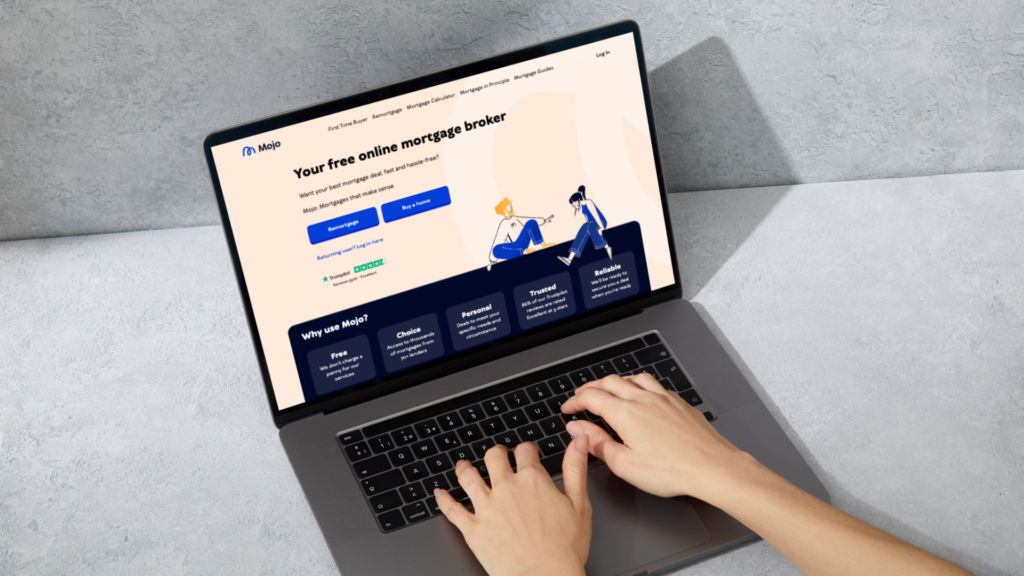

Mojo Mortgages Review: Should You Use This Free Broker?

Between work, life admin, and trying to enjoy your weekends, sorting a mortgage might be the last thing you want to spend hours on. You’ve heard about online mortgage brokers but aren’t sure which one to trust. What if there was a way to sort your mortgage from your sofa, with expert advice and no […]

Tembo Money Review: Should You Trust Them for Your Home?

Buying a home is exciting, but let’s face it—it can also feel like a real challenge, especially with the UK’s unpredictable housing market. If you’re a first-time buyer, you might already feel like the odds are stacked against you. House prices keep climbing, and saving for a deposit can feel endless. On top of that, […]

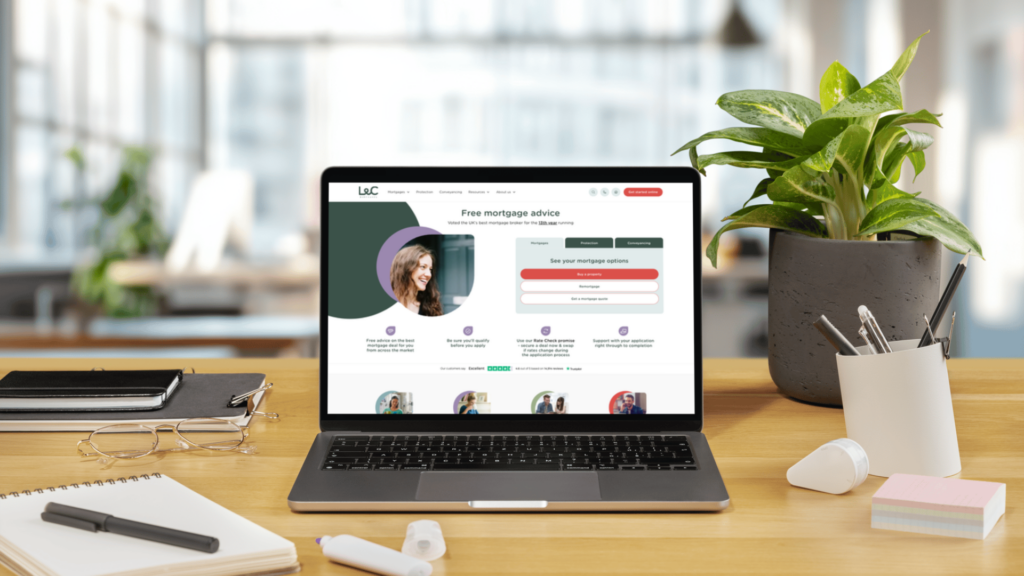

L&C Mortgages Review: Honest Look at Their Free Advice

If you’re in the market for a mortgage, you’ve probably heard of L&C Mortgages. They claim to be fee-free, boast a wide lender network, and are one of the UK’s largest mortgage brokers. But does bigger always mean better? In this review, we’ll dive deep into what makes L&C Mortgages tick, what sets them apart, […]