- What’s The Difference Between Secured and Unsecured Loans?

- What is a Bridging Loan?

- What Can You Secure a Bridging Loan Against?

- What Else Can Secure a Bridging Loan?

- Exploring Other Secured Loans

- Can You Get an Unsecured Bridging Loan?

- Is Unsecured Borrowing a Risk-Free Choice?

- What You Need to Qualify for a Bridging Loan

- How Much Money Can You Get?

- Types of Bridging Loans Available

- Are Bridging Loans Regulated?

- Why Do Bridging Loans Always Need Collateral?

- The Bottom Line

An In-Depth Guide To Secured and Unsecured Bridging Loans

If you’re in the UK and planning a big move—maybe you’ve found your dream home or you’re eyeing a property investment—you’ve got some financial decisions to make.

One of them is choosing between a secured and an unsecured loan.

Why does this choice matter? The loan you choose impacts your interest rate, borrowing limit, required collateral, repayment terms, and even your credit score.

In this guide, we explain everything about bridging loans, which are typically secured, so you can see if they align with your needs and financial planning.

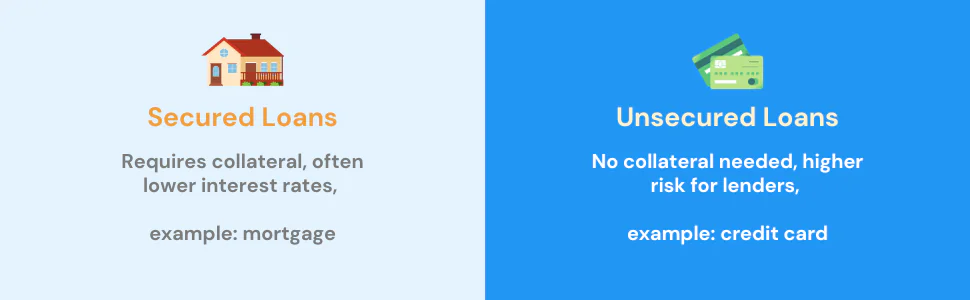

What’s The Difference Between Secured and Unsecured Loans?

First things first. When exploring borrowing options, you’ll encounter two kinds: secured and unsecured.

Unsecured loans include credit cards and personal loans. They’re usually smaller and don’t require collateral, but missing a payment can hurt your credit score.

On the flip side, secured loans involve larger amounts and longer repayment periods. You’ll need to offer an asset like your home as collateral. This makes them riskier but also easier to get approved for.

What is a Bridging Loan?

A bridging loan is a fast way to secure cash for short-term needs. If you’ve got your eye on a new property but haven’t managed to sell your current one, a bridging loan can fill that financial gap efficiently.

The approval process is often quicker than other types of loans, which is crucial when you’re up against the clock.

However, remember that these loans are secured. You’ll have to offer an asset, usually your home, as collateral. While they come with their own set of risks, bridging loans can be incredibly useful in certain situations.

Reasons People Opt for Bridging Loans:

- Quick Property Purchase. If you’ve found a property you want to snap up before someone else does, a bridging loan allows you to act swiftly.

- Sale and Completion Gaps. When there’s a delay between selling your property and completing the purchase of a new one, a bridging loan keeps you covered.

- Auction Buys. If you’re buying property at auction, you usually need to pay in full, quickly. A bridging loan can provide the required funds.

- Renovation Projects. If you’re flipping a property, a bridging loan can give you the quick cash needed to complete renovations before reselling.

- Business Cash Flow. Companies often use bridging loans to manage short-term cash flow gaps, especially if they’re waiting for funds to come in.

What Can You Secure a Bridging Loan Against?

Property is the most common collateral for a bridging loan, but it’s not your only option. Some lenders accept other assets.

First, second, and even third charge options are available. Keep in mind that opting for a second or third charge comes with higher interest rates and a lower Loan-to-Value (LTV) ratio.

For residential bridging loans, you usually use a property you or a family member lives in or plans to live in. They’re commonly used to buy a new home while waiting for your current property to sell.

If you want a 100% bridging loan, you’ll need extra assets. Lenders are more likely to approve your loan if you offer multiple forms of security.

What Else Can Secure a Bridging Loan?

When it comes to bridging loans, property isn’t your only ticket. Lenders often welcome a range of valuable items as collateral. Here’s a list to give you an idea:

- Commercial Equipment (Office machines and tools)

- Plant Machinery

- High-Value Vehicles

- Jewellery

- Watches

- Art (Valuable paintings or sculptures)

- Boats (Speedboats, or yachts)

If you’ve got something valuable that’s not on this list, don’t hesitate to speak with a financial broker skilled in bridging loans. There’s a good chance you’ll find a lender willing to work with you.

Exploring Other Secured Loans

If a bridging loan isn’t your cup of tea, there are other secured options to consider:

- Secured Loans – These are simpler but take longer to get approved. They usually have lower interest rates compared to bridging loans but are more expensive than a standard mortgage.

- Remortgaging – If you have enough equity in your property, remortgaging can release the funds you need. But watch out for early settlement fees if you’re in a fixed-term agreement.

Can You Get an Unsecured Bridging Loan?

Simply put, no. Bridging loans always require at least one asset as collateral. If you don’t have assets or don’t want to risk them, here are your unsecured options:

- 0% Money Transfer Credit Cards – For smaller amounts, these cards let you move funds to a bank account for a small fee. Generally, you won’t pay interest for the first 18 months, making it a cheap option if you pay off the balance in that time frame.

- Personal Loans – These don’t require collateral and are easier to get. You could borrow up to around £25,000 even with a bad credit history, but expect higher interest rates

Is Unsecured Borrowing a Risk-Free Choice?

While unsecured loans may seem less daunting because they don’t require collateral, it’s crucial to remember that no financial decision is entirely devoid of risk. Defaulting on an unsecured loan won’t result in losing your home, but it will tarnish your credit rating.

Moreover, a poor credit score not only makes future borrowing more difficult but also means you’ll likely face higher interest rates and additional fees.

Essentially, today’s financial missteps could lead to more costly and restricted borrowing options down the line.

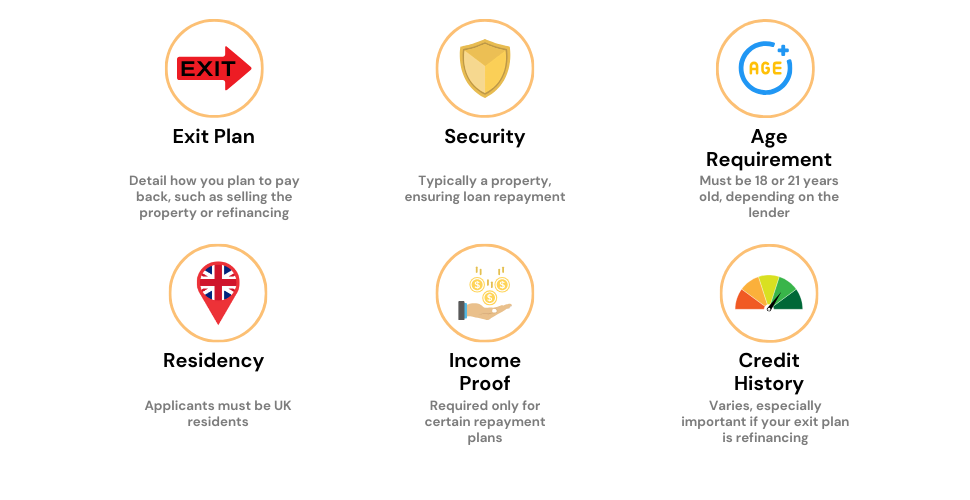

What You Need to Qualify for a Bridging Loan

If you’ve decided to take out a bridging loan, here are the two important things that lenders usually look for:

- Solid Exit Strategy – You must show how you’ll repay the loan.

- Collateral – Lenders require you to put up something valuable, often property, in case you fail to repay the loan.

Additional Requirements You Should Know

- You need to be at least 18 or 21, depending on the lender.

- You must reside in the UK.

- Income proof isn’t required unless you plan on repaying through refinancing or renting out property.

- Credit scores are flexible. If refinancing, however, you need evidence that you’ll get approved.

It’s important to note that rules can change depending on the lender, so always check their specific requirements.

How Much Money Can You Get?

Bridging loan amounts vary widely, from £5,000 to a staggering £25 million. This depends on your property’s value and your financial health.

Generally, you could borrow up to 75% of your property’s worth. If it’s a first-charge loan, you might get even more.

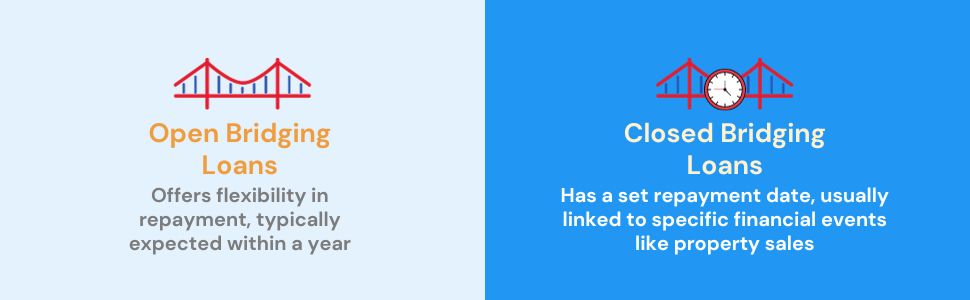

Types of Bridging Loans Available

When considering a bridging loan, you generally have two main options to choose from:

- Open Bridging Loans – These don’t have a specific repayment deadline, but lenders usually want the money back within 12 months. Some lenders may extend this period if you have a compelling reason.

- Closed Bridging Loans – These loans come with a predetermined repayment date, generally linked to a forthcoming financial event, like the sale of a property.

Regardless of the type you opt for, you’ll be required to outline your exit strategy, essentially laying out how you plan to settle the loan.

Are Bridging Loans Regulated?

The answer varies; bridging loans can either fall under regulatory oversight or operate outside it, based on their intended use.

Regulated Bridging Loans

These loans come into play when the loan is connected to a residential property you either currently own or intend to live in. For example, if you’re purchasing a new home and haven’t yet sold your existing one, you’ll likely opt for a regulated bridging loan.

Unregulated Bridging Loans

These are primarily used for business-related transactions. Regulatory bodies like the Financial Conduct Authority usually do not oversee these loans. The assumption is that businesses are aware of the inherent risks and are capable of conducting due diligence.

>> More about Commercial Bridging Loans

Why Do Bridging Loans Always Need Collateral?

You’ve already learned that collateral is a must-have for bridging loans. But what makes this requirement so crucial?

Firstly, it’s all about reducing risk for the lender. When you offer an asset, say your home, as collateral, you’re essentially giving them a fallback option. If you default on the loan, they can seize this asset to recoup their losses.

Secondly, let’s talk speed. Time is often of the essence in property transactions or other situations where you might need a bridging loan. Collateral streamlines the approval process. Lenders feel more secure, so they can fast-track your loan.

Finally, a secure loan often equates to a better interest rate for you. It’s a win-win: the lender feels safer, and you pay less over the life of the loan.

To sum it up, collateral isn’t just a box to tick; it’s a cornerstone of the bridging loan process. It’s what makes these quick, large-sum loans feasible for both parties involved.

The Bottom Line

A bridging loan might not be your go-to option, but it could be the perfect solution if you need money quickly.

Mainstream lenders often avoid bridging finance due to its high-risk nature. However, specialised lenders are more flexible and don’t follow the strict rules that traditional banks do.

Your choice of lender and financing method will depend on several factors: the asset you’re putting up as collateral, how much risk you’re comfortable with, and what you’re using the loan for.

To make the best choice, consult a bridging loan broker who knows the industry inside and out. They can evaluate your application and exit strategy, guiding you on whether a bridging loan suits your needs or if you should look for another way to secure the funds you need.

If this feels like too much to take in, let us help you out. Reach out to us, and we’ll set up a free, no-obligation chat for you with an experienced bridging loan broker who can direct you to the right lenders and snag you better rates.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How much does a bridging loan cost?

The cost of a bridging loan can vary widely based on the lender, loan amount, and the terms agreed upon. Generally, you can expect a monthly interest rate ranging from 0.5% to 2%.

Additionally, there may be other fees involved such as arrangement fees, typically around 1-2% of the loan amount, and possibly exit fees. It’s crucial to factor in all these costs to get a complete picture of the loan’s expense.

What are the typical deposit requirements for a bridging loan?

The deposit requirements for a bridging loan generally range from 20% to 40% of the loan amount, depending on the lender’s terms and the risk involved. A higher-value property or a strong exit strategy may allow for a lower deposit.

Is getting a bridging loan more expensive than a mortgage?

Yes, bridging loans are typically more expensive than traditional mortgages. They come with higher interest rates, usually calculated monthly rather than annually, as well as additional fees like arrangement and exit fees.

How quick can I get a bridging loan?

The process for securing a bridging loan is generally faster than getting a mortgage. Depending on the lender and the complexity of your situation, you could receive the funds within 48 hours to two weeks from the application date.

>> More about Quick Bridging Loans

What is the typical duration for repaying a bridging loan?

Bridging loans are generally short-term financing options, with most requiring repayment within a year. However, the exact duration can vary. Always confirm the terms with your lender to ensure they align with your exit strategy.

What benefits do secured loans provide?

Secured loans give you the ability to borrow more money because you’re putting up something valuable, like your home, as a safety net for the lender. If you need to borrow more than £20,000, secured loans are often your best bet.

The amount you can borrow usually starts at £5,000 and can climb all the way up to £100,000 or more, depending on your home’s value and your equity in it. Your interest rate isn’t set in stone; it’ll vary based on your personal financial history. But remember, getting approved for a secured loan is generally easier than getting an unsecured one.

Is an unsecured loan a better choice for me?

An unsecured loan might be right for you if you have a solid credit score and don’t want to put any assets on the line. These loans are also available to you even if you don’t own property.

However, the amount you can borrow is usually less, ranging from £1,000 to £25,000. Interest rates can differ a lot depending on the lender.

Also, you’ll have less time to pay back an unsecured loan. The repayment terms usually span from one to five years, which is shorter than the terms for secured loans typically offered to property owners.

Related Articles

Second and Third Charge Bridging Finance Explained

When cash flow gets tight and traditional loans aren’t cutting it, you don’t have to hit the panic button. Second or third charge bridging loans can be your financial lifeline. Now, you might be thinking, “That sounds great, but what’s the catch?” Well, there are a few nuances you should be aware of, like varying […]

Fast Bridging Loans: How to Apply and What You Need?

Imagine you’ve spotted the perfect property investment—fantastic location, huge potential, and it’s a steal. There’s just one hitch: your assets are tied up, and the clock is TICKING. You’ve been down this road before—missing out because the cash wasn’t there when you needed it. But what if there was a way to make your assets […]

Large Bridging Loans: Quick Cash for High-Value Properties

If you’re considering a big financial step and need quick access to a substantial amount of money. Large bridging loans might be your answer. However, let’s be clear: This is big money we’re talking about. Taking out such a loan is a serious commitment. In this guide, we’ll break down what large bridging loans are, […]