Fast Bridging Loans: How to Apply and What You Need?

Imagine you’ve spotted the perfect property investment—fantastic location, huge potential, and it’s a steal.

There’s just one hitch: your assets are tied up, and the clock is TICKING.

You’ve been down this road before—missing out because the cash wasn’t there when you needed it.

But what if there was a way to make your assets work for you, swiftly and without fuss? That’s where fast bridging loans come into play.

In this guide, we will walk you through the ins and outs of fast bridging loans—how QUICKLY you can get one, what influences the time it takes to get approved, and tips to speed up the entire process.

How Quick is a Fast Bridging Loan?

When you need quick access to funds, a bridging loan often comes to the rescue.

Speed is one of the most enticing features of a bridging loan. Although every application varies, you can typically expect approval within 5 to 10 days.

Don’t worry, there are exceptions. In specific scenarios, you could even get a loan sorted in under five days. It all boils down to finding a lender that matches your unique needs and circumstances and can deliver the service swiftly.

Can You Get a Bridging Loan in a Day or Two?

While it’s a possibility, it’s not typical. If you’re thinking of buying at auction, plan your bridging loan. That said, you can often receive an initial decision within a day.

If you’re buying property at an auction, for instance, it’s a good idea to set up your bridging loan well in advance. However, many lenders do offer a ‘Decision in Principle’ within the first 24 hours, giving you a preliminary yes or no on your application.

If you’re aiming for this kind of speed, communication is key. Make sure your broker and lender know that you’re in a hurry.

But keep in mind that you might end up paying a premium for this fast-track service.

Why Choose a Fast Bridging Loan?

There are several compelling reasons to opt for a fast bridging loan.

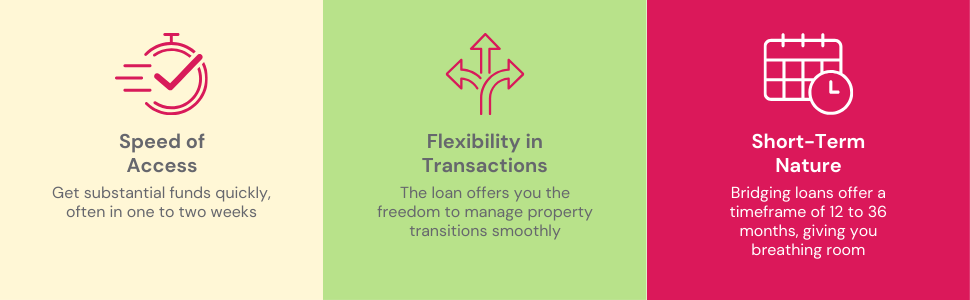

First and foremost, speed. You can get your hands on substantial funds in as little as one to two weeks, particularly helpful when you’re juggling between selling an old property and buying a new one.

Bridging loans generally have a term range of 12 to 36 months, offering you both speed and a bit of breathing room.

When you’re crunched for time, a fast bridging loan can provide you with the flexibility you need to sift through your options and nail down the best deal.

What Affects How Fast You Can Get a Bridging Loan?

When you apply for a bridging loan, you want that cash fast. But how quickly you get approved depends on several things, some of which you can’t control.

Here’s a rundown of factors that could make your application a sprint or a marathon.

The Amount You Need

The more money you want, the longer it might take to get it. Small loans could get a quick green light, but if you’re asking for millions, prepare to wait a bit.

Regulated vs. Unregulated Loans

If you’re buying a house to live in, that’s a regulated loan and it takes longer due to extra checks by the Financial Conduct Authority (FCA). But if the loan is for business, it’s unregulated and usually quicker to get approved.

The Lender’s Own Rules

Different lenders have different ways of doing things. Even if you’ve got all your papers ready and a simple case, some lenders take their time checking you out more thoroughly, which slows things down.

Valuation and Checks

Most lenders will want a property appraisal and some legal work done. This can eat up time, especially if problems pop up. If you’re in a hurry, ask your broker to find lenders who can speed this part up. But brace yourself for higher fees if you go this route.

What You’re Buying

The type of property you’re investing in matters. A loan for a hot commercial property will likely get a quick yes. But if you’re buying a rundown building, you might need a special lender and more time.

Your Situation

Factors like your exit strategy, your experience with property, and even your credit history can influence how fast you get the loan. For instance, a solid exit strategy can make lenders more comfortable and speed things up.

So, when you’re looking to lock down a bridging loan swiftly, remember that these factors can either slow you down or speed you up.

Having a knowledgeable broker can help you navigate these elements to get your loan approved as quickly as possible.

How Do You Apply for an Urgent Bridging Loan?

When you’re in a financial pinch and need money swiftly, a bridging loan can come to your rescue. The good news is the application process remains straightforward, no matter how urgently you need the funds. So, what do you need to prepare?

- Required Security – You’ll often secure the loan against a property or a high-value asset.

- Solid Repayment Plan and Exit Strategy – This is non-negotiable, as lenders want assurance you can pay back the loan. Usually, this involves selling the property used as security or refinancing it.

- Credit History Matters, but Not Much – A good credit score is beneficial, but not usually a deal-breaker.

- Income Checks Are Often Skipped – Don’t worry about providing proof of income; most lenders are more interested in the value of your collateral.

Speed Up Your Approval: Four Simple Steps

- Talk to an Experienced Broker – They can point you towards lenders known for quick approvals.

- Have a Solid Exit Strategy – A well-thought-out plan will help the lender make a quick decision.

- Be Prepared – Have all necessary documents at hand, from property details to any development plans.

- Accelerate Valuation – If possible, have your property valued before you apply, and keep the reports ready. An experienced solicitor can also speed things up.

What Are Non-Status Bridging Loans?

If you’re looking to buy an asset, like a property, non-status bridging loans focus on that asset, not your personal money situation. These loans are a favourite among property developers who own lots but are short on cash.

Because they’re flexible, these loans come together fast, often in just 3-7 days. Sometimes, you can even get one almost immediately!

Things You Should Know

While they sound awesome, these loans come with their own rules. Here’s what you should know:

- Lower LTV – These loans usually offer a lower loan-to-value ratio.

- High-Interest Rates – You’ll likely pay more in interest.

- Not Always Available – Newer lenders usually don’t offer these.

But, if you need money fast, the perks might just outweigh these points. They include:

- Quick Approval – You get the money faster.

- More Lenient – These are easier to get, even if you have bad credit.

- Flexible Collateral – Sometimes, you can even use soft assets like pensions or investments as security.

Other Ways to Get Quick Cash

Bridging loans is fast, but there are other options, too. Check these out:

- Fast House Buying Companies – If you need to sell your home quickly, these companies can help. But they usually don’t offer more than 75% of your home’s value, making it pricier in the long run.

- Personal Loan – These can also be fast but usually cap out at about £25,000.

- Secured Loan – If you already own a business or property, this can be another quick and sometimes cheaper route.

- Private Investors – If you’re eyeing a property that’s a good investment, a private investor might chip in. But, be warned, it’s a bit of a wild card.

Remember, each option has its ups and downs. But if speed is what you’re after, a non-status bridging loan might be just what you need.

The Bottom Line

If you’re after quick cash, fast bridging loans are a solid choice. They’re quick and flexible, ideal when you’re up against the clock.

But let’s be honest, they can be a bit tricky to figure out. This is where a trusted bridging loan broker steps in.

These experts give you access to a wide range of lenders you might not find on your own. They help sharpen your exit strategy and can even get you better interest rates by creating a bit of competition among lenders.

They’ll handle all the paperwork and make you look good to the lenders. Sure, they charge a fee, but the speed and ease they bring often make it a price worth paying.

In a nutshell, if you’re considering a fast bridging loan, it’s smart to get expert help. For a free, no-obligation chat, reach out to us. We’ll connect you with a skilled bridging loan broker who will make sure you’re clued up and get the best deal going.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

How big a bridging loan can I get?

Loan sizes can range from smaller sums to amounts up to £50 million or more, depending on the lender’s terms and your financial situation.

Furthermore, the size of a bridging loan you can secure largely depends on several factors. The most significant is the value of the asset or property you’re using as security. Lenders also consider your financial situation, the property’s location, and the loan term.

The Loan-to-Value (LTV) ratio—your loan amount divided by the property’s value—also plays a role. In general, the higher the asset value and the stronger your financial standing, the larger the loan you can get.

What deposit is required for a fast bridging loan?

The deposit amount needed for a fast bridging loan can vary widely based on the lender’s requirements and the specifics of your situation.

Typically, lenders look for a deposit that is around 20% to 40% of the property’s value. However, if you have a strong exit strategy or additional assets to offer as security, some lenders may be more flexible on this.

It’s essential to discuss this upfront with your lender to understand what you’ll need to provide for a fast and smooth loan process.

What could slow down my bridging finance application?

Several things can make your bridging loan application take longer. Different lenders have different speeds; some are faster than others.

The trade-off often lies between getting a loan quickly and securing lower interest rates. Fewer checks mean quicker approval but at a higher cost.

Detailed property valuations and legal searches can slow things down. Some lenders skip these steps by accepting alternatives like title insurance, which speeds things up but increases your repayment amount because of the higher risk to the lender.

How can I make my application process faster?

One of the keys to a faster process is clear communication with your lender or broker from the get-go. Ask specific questions to avoid any delays. For instance:

- Do you need a full valuation report? If so, when can it be scheduled and how long will it take?

- Are detailed legal searches required, or will title insurance be enough?

- What proof do you need for my exit strategy?

- When can you provide a complete list of underwriting requirements?

By getting answers to these questions early on, you’ll save time and make the whole process smoother.

Related Articles

An In-Depth Guide To Secured and Unsecured Bridging Loans

If you’re in the UK and planning a big move—maybe you’ve found your dream home or you’re eyeing a property investment—you’ve got some financial decisions to make. One of them is choosing between a secured and an unsecured loan. Why does this choice matter? The loan you choose impacts your interest rate, borrowing limit, required […]

Second and Third Charge Bridging Finance Explained

When cash flow gets tight and traditional loans aren’t cutting it, you don’t have to hit the panic button. Second or third charge bridging loans can be your financial lifeline. Now, you might be thinking, “That sounds great, but what’s the catch?” Well, there are a few nuances you should be aware of, like varying […]

Large Bridging Loans: Quick Cash for High-Value Properties

If you’re considering a big financial step and need quick access to a substantial amount of money. Large bridging loans might be your answer. However, let’s be clear: This is big money we’re talking about. Taking out such a loan is a serious commitment. In this guide, we’ll break down what large bridging loans are, […]