- What is Help to Buy?

- How Does It Work?

- Who is Eligible?

- The Benefits and Downsides of Help to Buy

- How To Apply for Help to Buy?

- Are Help to Buy Mortgages Different From Standard Mortgages?

- How Much Can You Borrow?

- Alternative Options to Help To Buy Scheme

- Can I Sell Help to Buy a Home Whenever I Want?

- Remortgaging after Help to Buy

- The Bottom Line

Help To Buy Mortgages Explained

Help to Buy is a UK government scheme helping first-time buyers with smaller deposits buy a home.

It offers two main benefits: a lower mortgage rate and a government equity loan that is interest-free for the first five years. This scheme makes buying a home more affordable for you.

This scheme has officially closed to new applicants. You can learn about other alternatives by clicking here.

What is Help to Buy?

Help to Buy is a UK government plan to help you buy your first home.

If you applied to this scheme before, you can get up to 20% of the money for a new home from the government, or even up to 40% if you’re buying in London.

You just need to pay a deposit of at least 5% and get a mortgage for the remaining 75%.

For the first five years, the government loan is interest-free.

After that, you start paying interest, which begins at 1.75% and goes up each year in April based on inflation and an extra 2%. When you sell your house, you need to pay back the whole loan you got from the government.

How Does It Work?

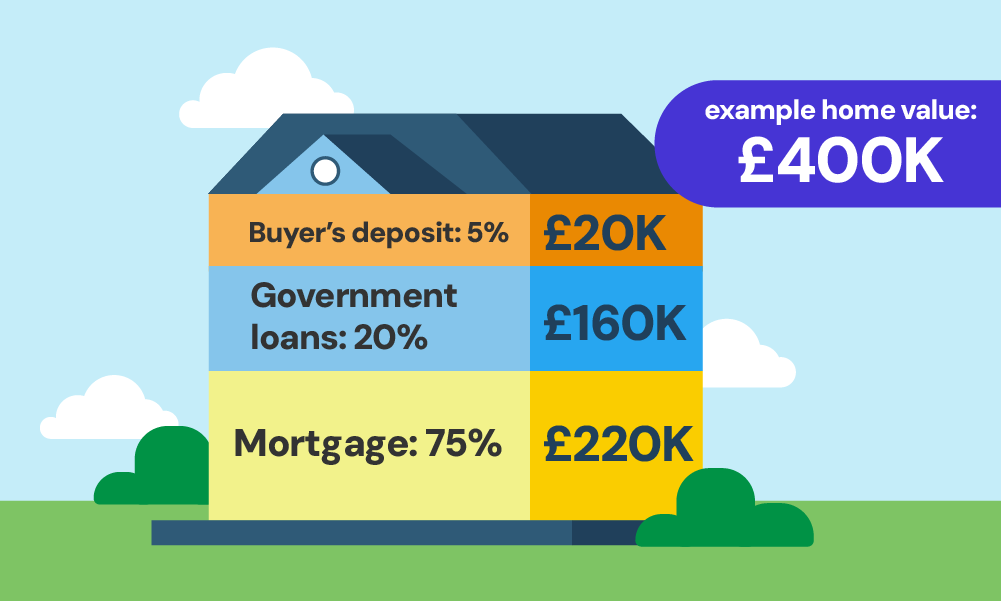

To help you understand the scheme much better, here’s an example: let’s say a house costs £250,000.

Under this scheme, you might only need to pay a deposit of £12,500, which is 5% of the house price.

The government then helps with a loan of £50,000, which is 20% of the house price. This means you only need a mortgage for £187,500, or 75% of the house price.

This helps because your mortgage is smaller and your monthly payments are less.

Who is Eligible?

To qualify for a Help to Buy mortgage, there are a few key requirements you need to meet:

- You must be at least 18 years old.

- You need to be a resident of the UK.

- This scheme is for people buying their first home.

- You must pass the mortgage lender’s affordability checks to make sure you can pay back the loan.

- You must not have had any form of Sharia mortgage finance.

- If you are married, in a civil partnership, or cohabiting with your partner (with a plan to continue living together), you must make a joint application.

The Benefits and Downsides of Help to Buy

When you’re thinking about the Help to Buy scheme, it’s good to know what’s good and not so good about it. Here’s a look at both sides.

Benefits:

- You only need a small deposit, just 5%, to buy a home.

- The mortgage rates you get might be lower than other types of mortgages.

- This scheme is open to all first-time buyers, no matter how much you earn.

- For the first five years, the government loan is interest-free, which can save you money.

- You have full ownership of your home, which is different from schemes like Shared Ownership where you only own a part of your home.

Downsides:

- You can only buy new-build homes in specific areas, so you might have fewer options to choose from.

- When you sell, you repay a share of the final selling price, not the original loan amount. This could be more than you borrowed.

- After the first five years, the interest on your loan from the government starts at 1.75% and increases every April.

- Not all lenders and builders participate in the scheme, limiting your options.

- You start with a small ownership share. If house prices fall, you might owe more on the house than it’s worth.

- This scheme often pushes up the cost of new homes compared to older ones.

- If the house you want exceeds the price limit for your area, the scheme won’t help you purchase it.

- Remortgaging can be difficult if you still have an outstanding equity loan.

How To Apply for Help to Buy?

To apply here’s what you need to do:

Step 1 – Find a Home and Apply for a Loan

Start by searching online for new homes that are part of the Help to Buy scheme. Look for the logo on home builders’ websites.

Once you find a home you like, reserve it with the homebuilder. You’ll need to pay a reservation fee, which is usually no more than £500. This fee is refunded if you’re not approved for an equity loan.

Ensure you get a signed copy of the reservation form from the homebuilder, as you’ll need this later.

Step 2 – Get Financial Advice

Before moving forward, it’s a good idea to talk to a mortgage advisor. They will give you advice about what you can afford and help you understand the process.

Step 3 – Check If Your Eligibility

A Help to Buy agent will help you see if you qualify for the scheme. They will look at your income and what you spend each month, including what you might pay on a mortgage.

Step 4 – Apply for an Equity Loan

If you’re eligible and can afford the monthly payments and interest, the Help to Buy agent will help you apply. You’ll fill in a Property Information Form with your personal and financial details.

Be honest in your application – providing false information is a criminal offence.

Step 5 – Authority to Proceed

If your application is successful, you’ll get an Authority to Proceed document. This document means you can go ahead with buying your home.

It’s valid for three months – if it expires, you’ll need to reapply.

Step 6 – Get a Repayment Mortgage

After getting your Authority to Proceed, you can apply for a mortgage. The amount you can borrow is usually up to 4.5 times your yearly income.

Discuss with a mortgage adviser if there are risks, like if your home decreases in value.

Step 7 – Work with a Conveyancer

A conveyancer will help with the legal side of things. They’ll explain the contracts you need to sign for the sale and the equity loan.

They’ll make sure your mortgage offer is correct according to your Authority to Proceed.

Step 8 – Pay the Deposit and Exchange Contracts

Now, you’ll pay at least 5% of your deposit. Then you and the seller will exchange contracts, which agree to buy the house officially.

Step 9 – Complete the Purchase

Finally, you complete the purchase. After you pay the rest of your deposit, your lender pays the homebuilder the mortgage amount.

The equity loan is also paid to the homebuilder, and you become the legal owner of your new home.

Congratulations!

Remember, both your mortgage and equity loan are secured against your home. Failure to keep up with the repayments will result in losing your home.

Are Help to Buy Mortgages Different From Standard Mortgages?

Yes, Help to Buy mortgages are different from standard mortgages in a few key ways. The main difference lies in the equity loan component of the Help to Buy scheme.

When you use a Help to Buy mortgage, you’re typically combining an equity loan from the government with a regular mortgage.

Another difference is the types of properties you can buy with a Help to Buy mortgage. These mortgages are specifically for newly built homes within the price caps set for each region.

Additionally, the eligibility criteria for a Help to Buy mortgage might differ from a standard mortgage, with specific requirements related to being a first-time buyer or not owning another property.

How Much Can You Borrow?

Knowing how much you can borrow under the Help to Buy scheme is straightforward. Here’s what you need to know:

Equity Loan Amount

The equity loan amount available to you through Help to Buy varies based on the region in the UK and is capped at a certain percentage of the property’s value:

- Most Areas: Up to 20% of the property’s value.

- London: Up to 40% due to higher property prices.

Maximum equity loan amounts based on regional price caps:

| Region | Price Cap | Max. Equity Loan |

|---|---|---|

| North East | £186,100 | £37,220 (20%) |

| North West | £224,400 | £44,880 (20%) |

| Yorkshire and The Humber | £228,100 | £45,620 (20%) |

| East Midlands | £261,900 | £52,380 (20%) |

| West Midlands | £255,600 | £51,120 (20%) |

| East of England | £407,400 | £81,480 (20%) |

| London | £600,000 | £240,000 (40%) |

| South East | £437,600 | £87,520 (20%) |

| South West | £349,000 | £69,800 (20%) |

Help to Buy Mortgage

In addition to the equity loan, you will need a mortgage to cover the remaining cost of the home.

Typically, you can borrow up to 4.5 times your annual salary. For example, with a £30,000 annual salary, you could get a mortgage up to £135,000.

Salary requirements for specific mortgage amounts based on regional price caps:

| Region | Price Cap | Mortgage % | Mortgage £ | Salary Required |

|---|---|---|---|---|

| North East | £186,100 | 75% | £139,575 | £31,017 |

| North West | £224,400 | 75% | £168,300 | £37,400 |

| Yorkshire and The Humber | £228,100 | 75% | £171,075 | £38,017 |

| East Midlands | £261,900 | 75% | £196,425 | £43,650 |

| West Midlands | £255,600 | 75% | £191,700 | £42,600 |

| East of England | £407,400 | 75% | £305,550 | £67,900 |

| London | £600,000 | 55% | £330,000 | £73,333 |

| South East | £437,600 | 75% | £328,220 | £72,933 |

| South West | £349,000 | 75% | £261,750 | £58,167 |

In general, to estimate how much you can borrow, you can use a simple calculation. Multiply your annual salary by 4.5 to get an idea of the maximum mortgage amount you might qualify for.

Add this to your equity loan amount to understand the total value of the home you could potentially buy.

For example, if you’re buying in an area outside London and earn £30,000 a year, you could get up to £60,000 as an equity loan (20% of the home’s value) and a mortgage of up to £135,000.

This means you could look for homes valued up to £195,000.

Remember, the exact amount you can borrow will depend on your circumstances and the lender’s assessment.

It’s a good idea to talk to a mortgage advisor to get a more accurate figure. They can also help you understand the repayments and any other costs involved.

Alternative Options to Help To Buy Scheme

Now that applications for the Help to Buy scheme have closed, you might be wondering what other options are available if you’re looking to buy a home.

Fortunately, several alternative government schemes can help.

- Mortgage Guarantee Scheme. This scheme encourages lenders to offer mortgages to people with a 5%-9% deposit. This scheme is helpful if you can’t afford a large deposit.

- Shared Ownership. Lets you buy a portion of a property and pay rent on the rest. This can be a good step if you can’t afford to buy a home outright.

- Rent to Buy. This scheme is where you rent a home at a reduced rate for up to five years, giving you the option to buy it later.

- Right to Buy. This allows council tenants to buy their homes at a discount.

- Lifetime ISA. If you’re saving for your first home, this can help you save money tax-free and get a government bonus on top.

- Gifted Deposits. This is where someone, usually a family member, gives you money towards your deposit.

- Guarantor Mortgages. This involves someone agreeing to cover your mortgage payments if you can’t.

Can I Sell Help to Buy a Home Whenever I Want?

Yes, you can sell your Help to Buy home at any time, but there are specific procedures and rules you need to follow.

First, when you decide to sell, you’re required to repay the equity loan you received. The repayment amount is tied to the current market value of your home, rather than the price you initially paid.

This means if the value of your home has risen, the amount you need to repay could be more than the original loan amount.

For example, if you took an equity loan of £40,000 to purchase your home and its value has increased from £200,000 to £250,000, you will need to repay £50,000, which is 20% of the current value, not the original loan amount.

Before you can proceed with the sale, you must arrange a valuation of your home by a surveyor. This valuation is crucial as it determines the exact amount you need to repay for the equity loan.

Once you have the valuation and an offer for your home, you need to notify Target – the agency responsible for administering the Help to Buy loans. They will guide you through the repayment process.

Remember, there are also administrative fees to consider. Generally, you’ll pay an admin fee of around £200 during this process.

These additional steps and costs mean selling a Help to Buy home can be a bit more involved than a standard property sale.

Remortgaging after Help to Buy

Remortgaging your home after using the Help to Buy scheme can be a bit challenging, especially if you still have an outstanding equity loan.

The main issue is that not all lenders offer remortgaging options for Help to Buy homes. This means you might have fewer choices when looking to remortgage your property.

Another thing to consider is that the fees for remortgaging can be higher if you have an equity loan.

This is because the process can be more complex, and lenders often see it as a higher risk. So, you might find that the costs are a bit more than you expected.

If you’re thinking about remortgaging your Help to Buy home, it’s a good idea to talk to a mortgage broker.

They are experts who know all about the different mortgage options and can help you find the right one for your situation.

The Bottom Line

Not all mortgage brokers have the experience in handling government mortgage schemes. It’s important to find a broker who specialises in this area.

They also have the right knowledge and expertise to guide you through the remortgaging process and help you find a suitable deal.

If you’re looking to save time and reduce stress in finding the right broker, get in touch with us. We’ll connect you with an FCA-qualified broker who specialises in government schemes. This way, you can get expert advice tailored to your specific mortgage situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What replaces Help to Buy?

As of now, the government hasn’t announced a direct replacement for the Help to Buy scheme. This means, for the time being, there isn’t a similar program set to take its place.

Do I pay stamp duty on a Help to Buy home?

Whether you pay stamp duty on a Help to Buy home depends on two things: the value of the property and if you’re a first-time buyer. Usually, first-time buyers benefit from a stamp duty relief on properties up to a certain value.

Is it hard to sell a Help to-Buy home?

Selling a home bought through the Help to Buy scheme can be a bit more complex than selling a standard property. This is mainly due to the need to repay the equity loan. The amount you repay is based on the current market value of your home, not the amount you initially paid. Plus, there are additional steps and fees involved in the process.

Is Help to Buy still available in Wales and Scotland?

Yes, the Help to Buy scheme is still available in Wales, but it’s no longer available in Scotland. However, Scotland has alternative schemes that you might find helpful if you’re looking to buy a home there.

How quickly can I buy a new home using an equity loan?

Once you get the Authority to Proceed, you have three months to exchange contracts with the seller. The entire process of buying your home must be completed within six months of exchanging contracts.

It’s important to note that if you change your mind about buying the home after exchanging contracts, you may have to pay certain costs.

Related Articles

Can Couples Open a Joint Help to Buy ISA? Find Out Here

You and your partner are serious about buying your first home, and you’re probably looking for every possible way to make it affordable. Maybe you’ve looked into joint savings accounts before, only to find the Help to Buy ISA doesn’t allow joint applications. So, where does that leave you? This article unpacks how individual Help […]

How Help To Buy ISA Works For Your House Deposit

You opened a Help to Buy ISA just before the deadline in 2019. Now you’re ready to make the most of it. You’ve been steadily saving, but with house prices still high, every extra pound counts. In this article, you’ll learn how to get the best out of your ISA. We’ll show you when and […]

Help to Buy ISA End Date Explained: Are There Alternatives?

If you’ve been saving up with the dream of owning your first home, chances are you’ve come across the Help to Buy ISA. But you might be wondering if it’s still around or if you’ve completely missed the boat. The scheme closed to new applicants back in 2019, which was a bit of a letdown […]