- What is a First Time Buyer?

- Is Now a Good Time To Buy a House?

- How Do First Time Buyer Mortgages Work?

- Can I Afford a Mortgage?

- Am I Eligible for a First-Time Buyer’s Mortgage?

- How Much Should I Save for a Deposit as a First-Time Buyer?

- Which Mortgage is Right for Me?

- What Mortgage Fees Will I Pay?

- How to Apply for a First Time Buyer Mortgage?

- Government Schemes Available to Help First-Time Buyers

- Getting Into Property Ownership With Another Person

- Benefits of Having a Professional Mortgage Advisor

- Tips to Boost Your Chances of Getting a Mortgage

- Key Takeaways

- Glossary

- The Bottom Line

Cracking the Mortgage Code: A Definitive Guide for First Time Buyers in 2025

Buying your first property in 2025?

We know it can be a bit of a minefield. There’s so much to think about, and it can be hard to know where to start.

But don’t worry; we’ve got YOU covered.

This is the most comprehensive guide for first time buyers in the UK.

The best part?

We’re going to give you tips that are working right now to boost your chances of getting an affordable mortgage.

In short: if you want to take that exciting first step up the property ladder, you’ll love this guide.

Let’s get started.

What is a First Time Buyer?

If you’re buying your first home, you’re a first-time buyer!

A first-time buyer is someone who has never owned a residential property in the UK or abroad, whether it’s a house, flat, or any other dwelling.

You are a first time buyer if:

- You have never owned a residential property, whether as a sole or joint owner, at any time, anywhere in the UK or abroad.

- Your property ownership history is limited to commercial properties without any living space attached.

You are not a first time buyer if:

- You’ve inherited or received property as a gift, even if you’ve never lived in it.

- You’re buying a home with someone who already owns, or has previously owned, a residential property.

- A parent or guardian is buying a house for you, and they already own one.

Source: Finance Act 2018, part 3, UK Public General Acts

If you’re still not sure whether you’re a first-time buyer or not, we recommend speaking to a mortgage advisor. They can help you get the best deal and guide you through the process.

While they may charge a fee, their expertise and access to a wider range of deals can often outweigh the costs.

If you’re looking to make the process as easy as possible, a mortgage advisor is a great option.

Is Now a Good Time To Buy a House?

The UK housing market is going through some changes.

In 2024, house prices saw a 4.6% increase, with the average property now costing around £ £268,087.

This rise suggests the market is beginning to steady, even though uncertainty around the economy still lingers.

As of February 6, 2025, the Bank of England cut its base rate to 4.5%.

This move could ease borrowing costs and make mortgages a little more affordable for buyers. Lower rates might also encourage more people to jump back into the market.

But there’s still a lot of movement happening.

According to Rightmove, house prices went up slightly—by 0.5%—between January and February 2025. It’s not a huge jump, but it shows that sellers are testing if buyers are willing to pay more.

There’s also a change in property purchase taxes coming in April 2025. Because of this, some buyers are rushing to buy now to avoid paying extra later.

Since borrowing is becoming cheaper, more buyers might return to the market soon. Some sellers are already accepting lower offers, but house prices overall seem stable.

This means buyers can negotiate for better deals, though it’s not fully a buyer’s market yet.

So, is it the right time to buy? That depends on your situation.

If you’ve saved up a good deposit and can handle the monthly payments, it might be a smart time to buy—especially if mortgage rates drop even more.

First-time buyers also have an advantage.

Government schemes, tax breaks, and mortgages with lower deposit requirements are still available, making it a little easier to get a foot on the property ladder.

We’ll explain all of this in more detail later on. 😊

How Do First Time Buyer Mortgages Work?

Before we get into the nitty-gritty, you need to know two things:

What is a Loan?

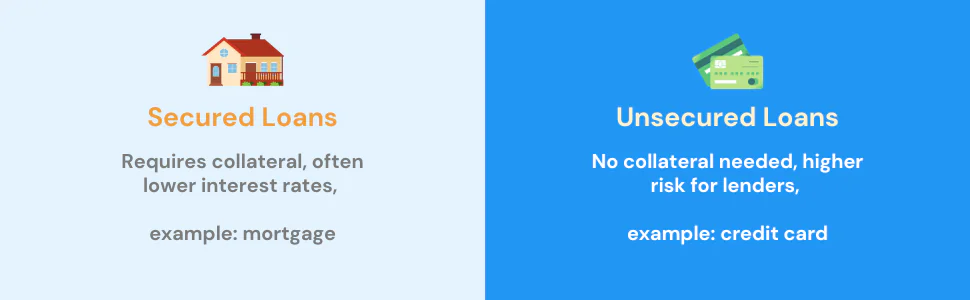

A loan is a financial agreement where a lender lets you borrow money with an agreement to pay it back, plus interest, over a set period. There are two types of loans: secured and unsecured.

When you take out a loan, you will be given a loan agreement that outlines the terms, such as the interest rate, repayment period, and any fees.

Lenders make their money in several ways, including charging interest, fees, and repayment penalties. All of these are explained in the following sections of this guide.

What is a Mortgage?

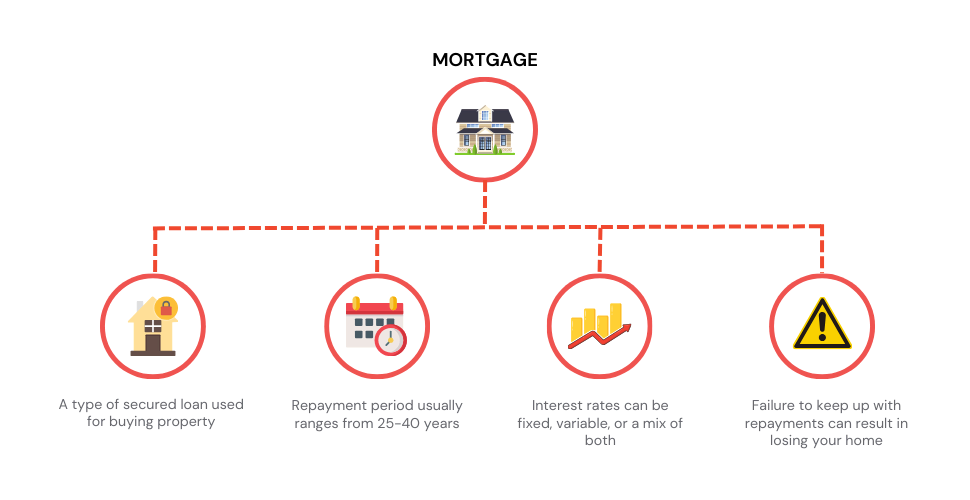

A mortgage is a type of loan that lets you buy a property. It is a secured loan, which means the lender has the right to take back and sell the property if you cannot keep up with your monthly repayments.

A typical mortgage lasts for 25 – 40 years.

Think long and hard before you use your home as security for a mortgage loan. If you don’t keep up with the repayments, you could lose your home.

Having said that, mortgages are a common way to buy a home, but lenders won’t lend you one if they think you’ll struggle to pay it back. So make sure you’re financially ready before you apply.

The ultimate decision to buy your first home and get a mortgage is yours.

You’re the one who’ll live with it, so it’s worth taking the time to learn about mortgages – the process, types, and fees involved so you can ask the right questions when you start the homebuying process.

To simplify things for you, here’s a quick guide to getting a mortgage:

- Sort your finances out. Make sure you can afford the monthly payments and that you’re eligible for a mortgage.

- Save for a deposit. No deposit, no mortgage.

- Get a mortgage advisor. They can help you find the best mortgage for your needs.

- Get an agreement in principle. This will show sellers that you’re serious about buying a home.

Can I Afford a Mortgage?

The most important thing to work out is whether you can afford a mortgage.

When working out affordability, it’s important to be realistic and think about your long-term financial goals.

Affordability is more complicated than just multiplying your income. Lenders consider a lot more than your salary when deciding how much you can borrow.

Here are some of the factors that lenders consider when assessing affordability:

- Your income, employment history, and stability;

- Your debts, such as car loans, credit card debt, and student loans. They will also look at your debt-to-income ratio;

- Your monthly expenses including your housing costs, food, transportation, and other essential expenses; and

- Your credit score to assess creditworthiness.

Your goal is to get a mortgage that’s within your financial comfort zone. Here are some tips for analysing your affordability before getting a mortgage:

- Calculate your monthly income and expenses. This will give you an idea of how much money you have coming in and going out each month.

- Think about your debt-to-income ratio. This is the percentage of your monthly income that goes towards debt payments. Lenders typically prefer a debt-to-income ratio (DTI) of 36% of below for the best deals. A lower debt-to-income ratio shows lenders that you can afford payments. You can calculate your DTI by using our debt-to-income calculator here.

- Get a mortgage pre-approval before you start looking at properties. This will give you an idea of how much you can borrow and what your monthly payments will be. You can get a pre-approval from a lender by providing them with proof of your income, assets, and debts.

- Use an affordability calculator. This digital tool will give you an estimate of how much you can afford to borrow, based on your income.

It’s important to remember that affordability is a complex issue.

There’s no one-size-fits-all answer to the question of how much you can afford to borrow. The best way to determine your affordability is to speak with a qualified mortgage advisor

Am I Eligible for a First-Time Buyer’s Mortgage?

Here are some of the things you’ll need to consider to help you prepare for the big decision of buying your first home:

- You need to be at least 18 years old.

- You need to save up at least 5% of the purchase price of the property you want to buy.

- You must have a legal right to live in the UK.

- You can afford to get a mortgage. The best deals will depend on your employment status, monthly income and outgoings, savings for a deposit, and credit history.

Take note that these qualifications may vary among lenders and can change over time. So, it’s advisable to consult with a mortgage broker or check with lenders for specific eligibility criteria.

In today’s market, it’s also important to make yourself attractive to lenders so you can get the right mortgage for you.

Typically, you must have:

- good credit score,

- stable job,

- enough deposit, and

- correct documents like payslips, bank statements, and proof of identity as evidence.

How Much Should I Save for a Deposit as a First-Time Buyer?

A deposit is a down payment on a property you’re buying. It’s usually a percentage of the purchase price, and most lenders require it.

It shows that you’re financially stable and have good money management skills.

So, how much do you need as a first-time buyer? There’s no easy answer. It depends on the:

- Lender’s criteria,

- The cost of the property,

- Your financial situation, and

- Your credit score.

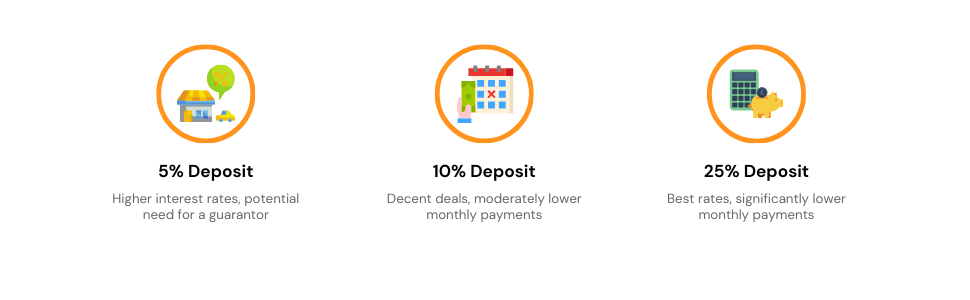

Nowadays, some lenders offer 95% mortgages, which means you only need a 5% deposit. But, these mortgages usually come with a higher interest rate or require a guarantor to reduce the lender’s risk.

A bigger deposit usually means lower monthly payments and interest rates. This is worth considering when deciding what property you can afford.

You should be able to get a decent deal with a 10% deposit, but the best rates are usually available to those who can put down 25% or more.

Paying off a mortgage is usually better than paying rent. So, if you want to get on the property ladder quicker. We generally recommend saving up to a 10% deposit.

Of course, if you can afford a larger deposit, that’s even better! You’ll likely be offered more favourable loan terms.

The rule of thumb is: no deposit, no mortgage. The more you save, the less you need to borrow, and the better your mortgage terms will be.

Here’s how different deposit percentages affects your rates and monthly payments:

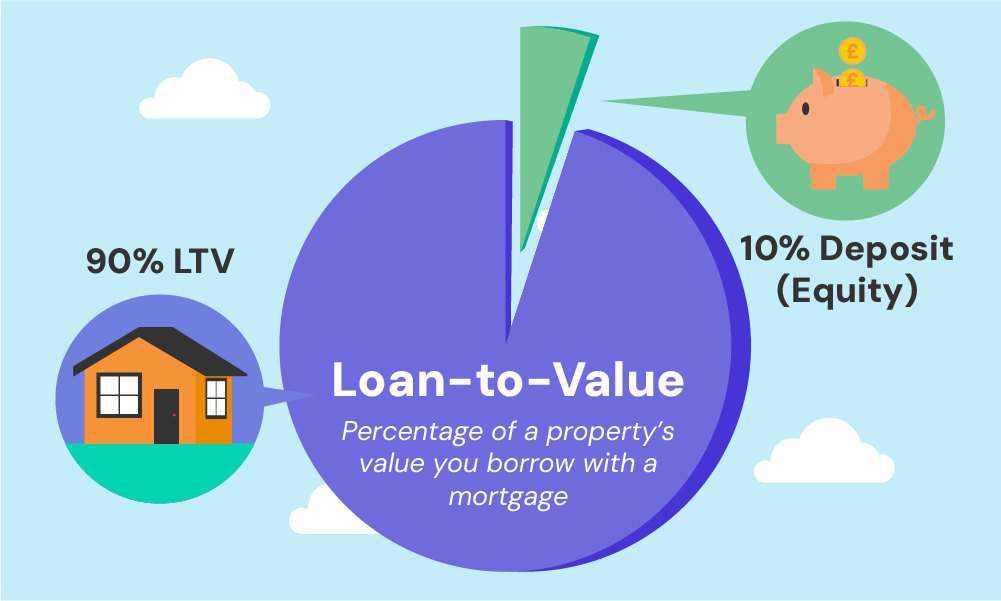

What is a Loan-To-Value (LTV)?

Loan-to-value Ratio (LTV) is the percentage of a property’s value that you borrow as a mortgage.

For example, if you buy a property worth £200,000 with a deposit of £40,000, you’ll borrow £160,000. This gives you an LTV of 80%.

But, the LTV ratio isn’t always calculated based on the purchase price. Lenders will use the lower of the purchase price or the valuation

If the property is valued at less than the agreed price, this could mean you need a larger deposit than expected. In this case, you may ask the seller to lower the price and see if they are willing to renegotiate.

It is important to be aware of the LTV ratio and to try to save as much money as possible for a deposit.

Which Mortgage is Right for Me?

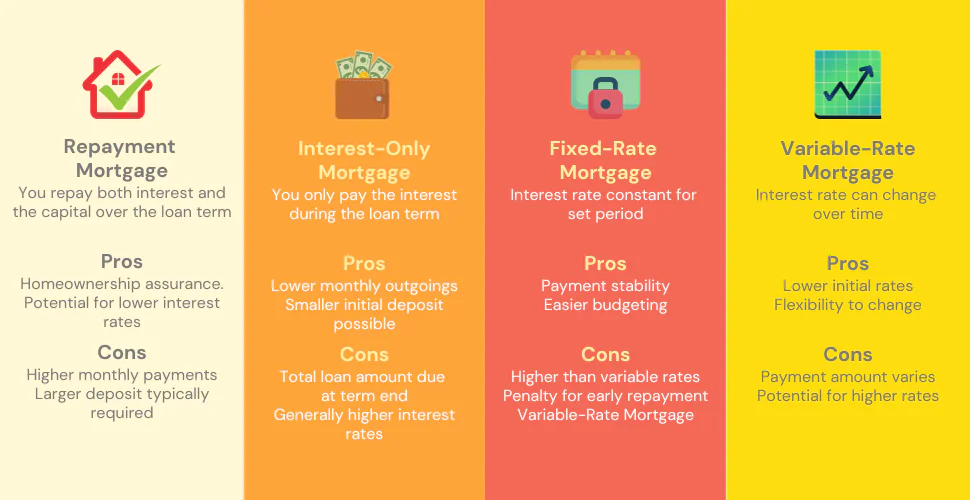

Choosing the best mortgage deal can be tricky, but it’s important to know your options. As a first-time buyer, you’re more likely to get a repayment mortgage than an interest-only mortgage.

Interest-only mortgages are very rare these days, and they’re not really suitable for most first-time buyers.

Repayment vs. Interest-only Mortgage

Repayment Mortgage

A repayment mortgage is a loan where you pay back two things each month: the interest (the fee the bank charges for lending you money) and the capital (the actual money you borrowed).

Over time, as you make payments, the loan amount gets smaller. By the end of the mortgage term, you’ll have fully paid off the loan and own your home completely.

Pros

- You’ll own your home outright once all the payments are made.

- Every monthly payment reduces your debt bit by bit, so you owe less over time.

- Usually, you can get a lower interest rate than with an interest-only mortgage.

- Lenders prefer this type of mortgage, so you’ll have more options to choose from.

- There’s less financial risk since you’re always paying down the actual loan amount.

- You’re less likely to end up in negative equity (when your home is worth less than your loan).

Cons

- Monthly payments are higher because you’re paying off both the loan and the interest.

- You might need a bigger deposit upfront, often between 5%–20% of the home’s value.

- Less flexibility with your money, as higher payments leave you with less to spend elsewhere.

- You’ll have less cash available for other investments or expenses.

- If you want to pay off the loan early, you might face extra fees called early repayment charges.

Interest-only Mortgage

An interest-only mortgage means you only pay the interest each month, not the actual loan itself.

This type of mortgage is popular with buy-to-let landlords (people who rent out homes).

The loan amount doesn’t shrink over time, so by the end of the mortgage term, you’ll still owe the full amount you originally borrowed.

To pay it off, many people sell the property or use savings.

Pros

- Monthly payments are lower because you’re only covering the interest.

- More flexibility with your money—you’ll have extra cash to spend or invest elsewhere.

- Landlords can sometimes get tax benefits by deducting mortgage interest from rental income.

- You can invest the extra money in other things that might give you better returns.

- It’s a good option if you expect to earn more money in the future.

Cons

- You’ll still owe the full loan amount at the end of the term.

- Over time, you might pay more in interest than with a repayment mortgage.

- Lenders usually want a bigger deposit—around 25% or more of the property’s value.

- It’s harder to qualify, as lenders have stricter requirements (like a higher income).

- If house prices drop, you could owe more than your property is worth (negative equity).

- You’ll need a solid plan to repay the loan at the end, like selling the property or using savings.

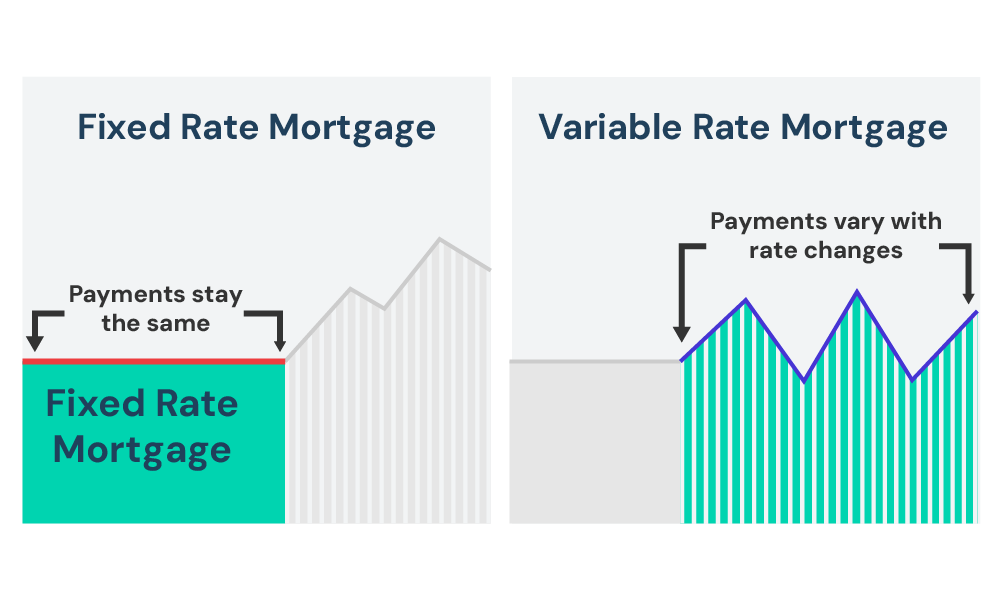

Fixed-Rate vs. Variable-Rate Mortgage

There’s a whole load of mortgages out there, but the most common are fixed-rate and variable-rate. Each one has its own pros and cons, so it’s important to choose the one that’s right for you.

Fixed-Rate Mortgages

Fixed-rate mortgages are the most popular type. Your interest rate and monthly payment stay the same for a set period, usually two, three, five, or ten years.

Pros

- Stability can give you peace of mind

- Easier budgeting

- Protection against interest rate rises that affects variable-rates.

Cons

- More expensive than variable-rate mortgages

- You may be stuck with the higher rate if interest rates fall

- You’ll usually have to pay an early repayment charge if you switch to another mortgage deal before your current deal ends.

Variable-Rate Mortgages

Variable-rate mortgages have an interest rate that can change over time. This means that your monthly payments could go up or down.

These mortgages are typically cheaper than fixed-rate mortgages, but you’re taking on more risk.

Pros

- Less expensive than fixed-rate mortgages

- Pay less if interest rates are particularly low

- Less likely to have early repayment charges, so if you want to switch mortgage deals or pay in advance, you won’t be charged for doing so.

Cons

- Uncertainty.

- Paying more if interest rates are high

To make things more complex, you should know that there are more types of variable-rate mortgages.

Here are the 4 main types of variable-rate mortgage deals:

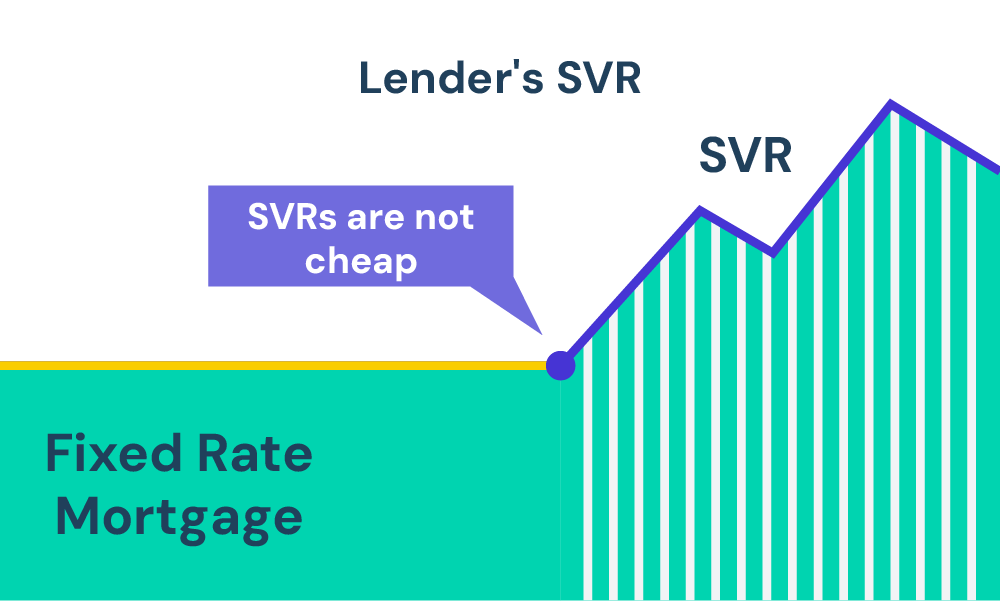

Standard Variable Rate Mortgage (SVR)

Your lender will usually move you onto an SVR once your introductory deal ends. The interest rate will change depending on the market, and your lender will decide when to change it.

SVRs are typically more expensive than other types of mortgages, so you may want to consider switching to a new deal if yours is about to end.

Discounted Rate Mortgage

A type of variable-rate mortgage that gives you a discount on the lender’s standard variable rate (SVR) for a set period of time.

The amount you pay each month can change if the lender changes their SVR, which they can do at any time.

Works by tracking the movements of another interest rate, usually the Bank of England base rate, plus a set percentage.

This means your monthly repayments will move up and down in line with changes to interest rates.

Some tracker deals have a ‘floor’, known as an interest rate collar, which the rate won’t go below, even if the Bank of England base rate falls below this level.

Capped Rate Mortgage

Variable-rate mortgages with a cap are not as common as they once were.

These mortgages have a maximum interest rate that they can charge, which gives borrowers some protection against rising interest rates.

Special Features of a Mortgage

Cashback Mortgages

A cashback mortgage is a type of mortgage that gives you a lump sum of money when you take it out.

The amount of cashback you get can be a percentage of the amount you’re borrowing or a fixed amount. You’ll get the cashback when you complete your purchase, not before.

Pros

- You can use the cashback to help with the costs of buying a home, such as furniture, repairs, or stamp duty.

- Cashback mortgages can be a good option if you’re struggling to save a deposit.

Cons

- Cashback mortgages often have higher interest rates than other types of mortgages.

- You may have to pay early repayment charges if you want to pay off your mortgage early.

Offset Mortgages

An offset mortgage is a type of mortgage where your savings are linked to your mortgage. This means that the amount of money you have in savings is used to reduce the amount of interest you pay on your mortgage.

For example, if you have a £200,000 mortgage and £50,000 in savings, you will only pay interest on £150,000 of your mortgage.

It can be a good option for people who have savings and a reasonable bank balance every month. They can help you to save money on your mortgage payments and pay off your mortgage faster.

Pros

- You can still make withdrawals from your savings account at any time.

- You can save money on your mortgage interest payments.

- You can pay off your mortgage faster.

Cons

- You may not earn as much interest on your savings as you would if you had a separate savings account.

- You may not be able to access discounted rate deals.

Mortgages with Flexible Features

Option to Overpay

You can often overpay your mortgage, which can help you pay off your debt quicker. Check your mortgage agreement to see if there’s a limit on how much you can overpay each year.

It’s usually 10% of the mortgage.

Paying back your mortgage before the end of its term can be a great way to save money, but you may be charged an early repayment fee.

Check your mortgage agreement to see if there are any fees involved.

Option for Payment Holidays

Some mortgages allow you to take a break from your mortgage payments for a limited period. This is called a payment holiday.

If you’re struggling to make your mortgage payments, a payment holiday could be a good option. It can give you some breathing space to get back on your feet financially.

To find out if your mortgage has this option, you’ll need to check your mortgage agreement. If it does, you’ll need to contact your lender to apply for a payment holiday.

So, which mortgage is right for you? It really depends on your situation. If you’re not sure, it’s a good idea to speak to a mortgage advisor. They’ll be able to help you find the best deal.

What Mortgage Fees Will I Pay?

Don’t forget about the hidden costs of getting a mortgage! There’s more to it than just the monthly repayments and interest.

You’ll also need to pay for fees like valuations, surveys, solicitors, and taxes like Stamp Duty. Many people underestimate how much these extra fees and costs can add up.

The last thing you want is to be caught out by unexpected costs when you’re trying to buy your dream home.

Mortgage fees can vary depending on your personal situation and the type of mortgage you choose. Be sure to ask your lender about any fees that aren’t listed here.

Here’s a guide to what you can expect to pay

Fees and charges before completion:

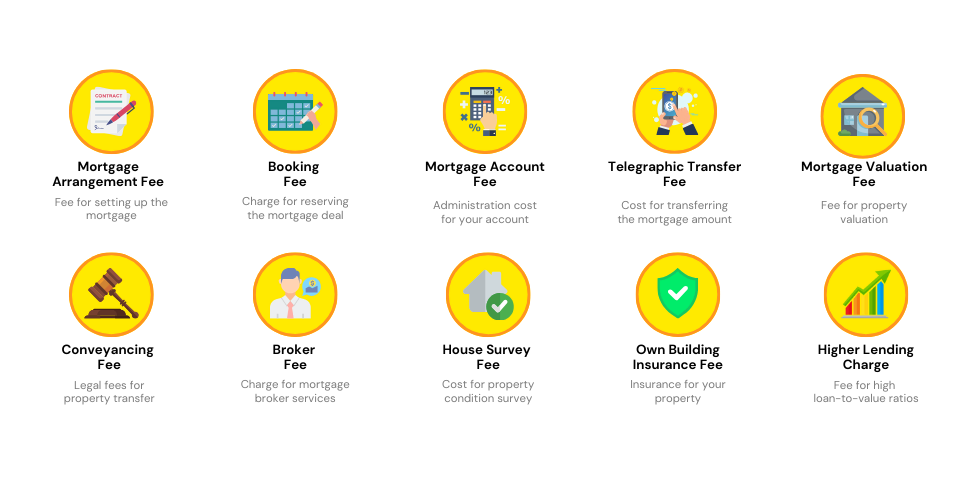

Mortgage arrangement fee

A mortgage arrangement fee is a fee that lenders charge for setting up a mortgage. It is the highest charge by far, and you need to look at it as part of the price of a mortgage.

- Typical cost: £0 to £2,500

- Paid to: Your lender

- You don’t always need to pay this fee, so it’s important to check with your lender.

- You can pay the fee upfront or add it to your mortgage.

Booking or Reservation Fee

Some lenders charge a fee to reserve a fixed-rate, tracker, or discount mortgage. It is usually payable upfront and is non-refundable.

- Typical cost: £100 to £300

- Paid to: Your lender

- You don’t always need to pay this fee, as most lenders don’t charge it.

- Always paid upfront.

Mortgage Account Fee

This fee covers the lender’s costs of setting up, maintaining, and closing your mortgage. If you’ve already paid this fee, you’re probably not going to have to pay the exit fee (see below).

However, you may still have to pay an early repayment charge (see below) if you close your mortgage early.

- Typical cost: £100 to £300

- Paid to: Your lender

- You usually pay this once you’ve accepted a mortgage offer (it may be added to your mortgage balance).

Telegraphic transfer fee

The telegraphic transfer fee, also known as the CHAPS (Clearing House Automated Payment System) fee, covers the cost of your mortgage lender transferring the mortgage funds to the seller’s solicitor. It’s usually added to the mortgage amount or taken off the balance received.

- Typical Cost: £25–£50

- Paid To: Your Lender

- You’ll usually pay this fee once you’re ready to complete the deal.

Mortgage Valuation Fee

Lenders charge a fee to inspect your property. This is not the same as a survey, which is a more thorough inspection of the property that is optional but a good idea if you’re buying an old property. A valuation is for the lender’s benefit, while a survey is for your benefit.

- Typical cost: Around £300, but it can be more.

- Paid to: Your lender.

- You don’t always need to pay – some lenders will pay it for you.

- Always paid upfront.

Conveyancing Fee

Conveyancing covers the cost of all the legal work associated with buying a home, such as searching local authority data to check for hidden issues like poor drainage.

- Typical cost: £800 and £1,500.

- Paid to: Your solicitor throughout the process and on completion.

- You usually need to pay, but some lenders will pay it for you.

- Always paid upfront.

Broker Fee

If you’re using a broker, be sure to ask about their fees upfront. Be wary of brokers who ask for the fee upfront, as you could lose it if you change your mind later.

- Typical cost: £0 and £500, but it could be more.

- Paid to: Your broker.

- Some brokers are fee-free, so it is worth comparing fees before you choose a broker.

House Survey Fee

A survey is a detailed inspection of a property’s condition. It’s worth getting one done, as it will tell you what maintenance and repairs are needed now and in the future. It must be conducted by a trained professional, like a member of the RPSA, RICS, or ISVA.

Having a survey done is optional, but it’s worth it for the peace of mind that you’re buying a property in good condition.

- Typical Cost: £400–£2,000 depending on the level of survey.

- Paid to: Your surveyor (or lender if they arrange it)

- You usually pay this between when the property is taken off the market and when the contracts are exchanged.

Own building insurance fee

Your lender might charge you an own building insurance fee, also known as a freedom of agency fee if you don’t take out their building insurance and instead choose a policy from another provider.

This is to cover the cost of checking that the policy is comprehensive enough to protect them if your property is damaged.

It’s worth comparing quotes to see if it’s cheaper to pay the fee and find a better deal, or to just go with your lender’s cover.

- Typical Cost: £25–50

- Paid to: Your lender

- Usually for payment once you’ve accepted the mortgage offer.

- You don’t always need to pay this as not all lenders charge this fee

Higher lending charge

You might need to pay a higher lending charge if you have a small deposit. This insurance will protect your lender if you can’t afford to pay back your mortgage and they have to sell your house for less than you owe.

Not all lenders charge this, but if they do, it’s usually applied to loans of more than 85% or 90% of the property’s value.

- Typical Cost: Usually 1.5% of the mortgage

- Paid to: Your lender

- Usually for payment once you’ve accepted the mortgage

Fees and charges after completion:

Just because you’ve bought a home and got a mortgage doesn’t mean the fees and charges are over. Some of these are avoidable, but others aren’t.

Here are some of the fees and charges you need to be aware of after getting a mortgage:

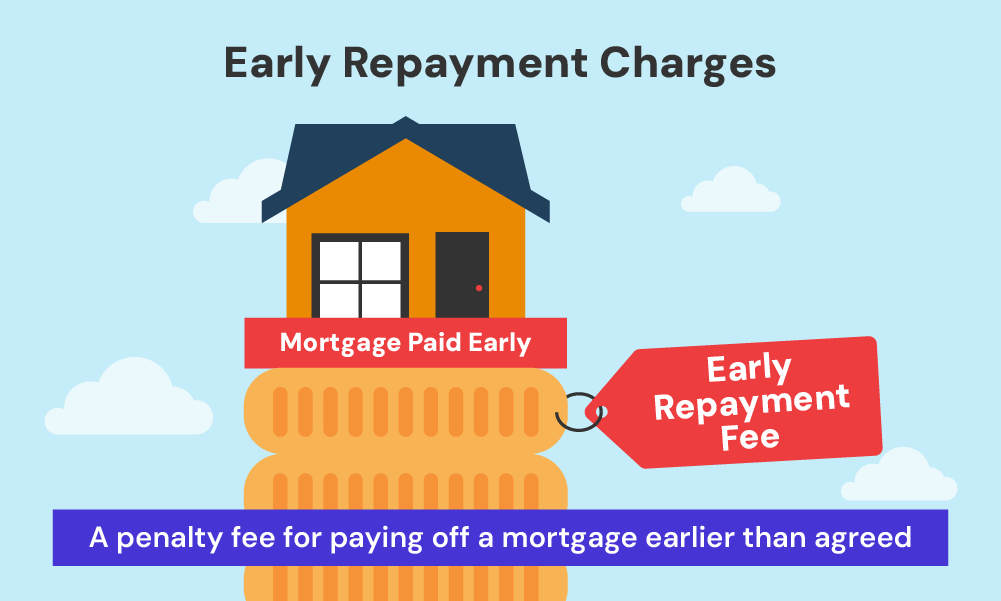

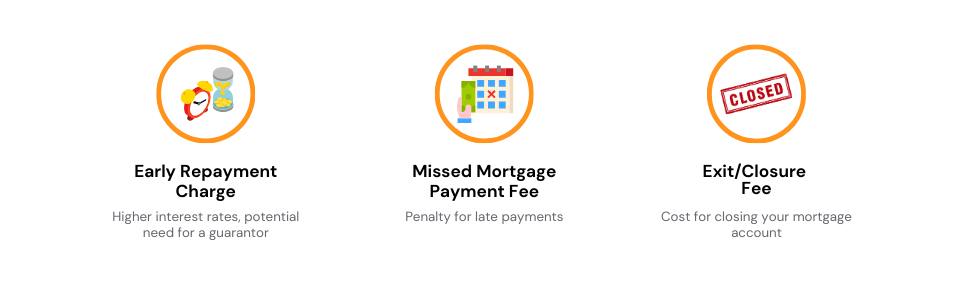

Early repayment charge for mortgage (ERC)

If you pay off your mortgage early, switch lenders, or exit a fixed-rate deal, you might have to pay an early repayment charge (ERC). This is to protect the lender from losing money.

The charge is usually between 1% and 5% of the amount you repay early, but it can be higher depending on your circumstances.

Most lenders have an overpayment limit, which is the maximum amount you can pay off your mortgage each year without incurring an ERC.

The overpayment limit is usually around 10% of your mortgage balance, but it can be lower or higher. Once your fixed-rate deal ends, you’ll usually be able to repay as much of your mortgage as you like without an ERC.

- Typical Cost: Depends on the lender, but typically 1–5% of the value of the early repayment.

- Paid to: Your lender

- You usually pay this when you pay off all or some of your mortgage early, exit an introductory deal, or wish to switch lenders.

- Some lenders don’t use these charges

Missed mortgage payment fee

If you miss a mortgage payment, your lender might charge you a late payment fee. The amount of the fee will depend on your lender’s rules. If you miss too many payments, your lender could repossess your home.

Don’t be afraid to reach out to your lender if you’re struggling to make your mortgage payments. They may be able to help you come up with a plan to get back on track.

- Typical Cost: Depends on the lender’s rules.

- Paid to: Your lender.

Your lender might charge you an exit or closure fee when you close your mortgage account. This is sometimes known as a redemption fee, deeds release fee, or mortgage completion fee.

You won’t usually have to pay this fee if you’ve already paid the mortgage account fee, as this usually covers setup, maintenance, and closure costs.

- Typical Cost: £75-£300

- Paid to: Your lender

Government Fees and Charges

Alongside the fees you’ll pay to your mortgage lender and the service providers you hire to help you buy a home, you’ll also need to budget for government fees and taxes.

Here are the most common costs you’ll need to keep in mind:

Land Registry Fee

The Land Registry is responsible for registering properties under their owners’ names.

When you buy a property from someone else, the Land Registry charges a fee to transfer their registration into your name.

- Typical cost: £0 to £500, but it could be more depending on the property price.

- Paid to: Land Registry (via your solicitor) after completion.

- You will always have to pay this fee when you buy a property.

Stamp Duty Land Tax (SDLT)

You’ll usually pay Stamp Duty Land Tax (SDLT) on a residential property if it costs more than £250,000. This tax applies to houses and flats, whether you’re buying them outright or with a mortgage.

The amount you pay depends on when you bought it, how much you paid for it, and if you’re eligible for any relief or exemptions.

Here’s an example to provide you an idea:

| PROPERTY PURCHASE PRICE | SDLT RATE |

|---|---|

| £0 to £250,000 | Zero |

| £250,001 to £925,000 | 5% |

| £925,001 to £1,500,000 | 10% |

| Over £1,500,000 | 12% |

Let’s say you bought a house in May 2023 for £300,000. You’re SDLT will be calculated as follows:

- 0% on the first £250,000 = £0

- 5% on the final £50,000 = £2,500

- total SDLT = £2,500

But if you’re a first-time buyer, you can get tax relief on your SDLT.

First Time Buyers (SDLT) relief

First-time buyers can get a discount (relief) on Stamp Duty Land Tax (SDLT) if you buy a house or flat for £425,000 or less.

You won’t pay any SDLT on the first £425,000 and 5% SDLT on the portion from £425,001 to £625,000.

Both you and anyone else you’re buying with must be first-time buyers to be eligible. If the property is more than £625,000, you can’t claim the discount and will have to pay SDLT at the standard rate.

| PROPERTY PURCHASE PRICE | SDLT RATE |

|---|---|

| £0 to £425,000 | Zero |

| £425,001 to £625,000 | 5% |

For example, you’re a first-time buyer and you just bought a property for £520,000. The SDLT you owe will be calculated as:

- 0% on the first £425,000 = £0

- 5% on the remaining £95,000 = £4,750

- Total SDLT = £4,750

On the other hand, if you’re a first time buyer and you purchase a property for £920,000. Your SDLT shall be calculated using the standard rate:

- 0% on the first £250,000 = £0

- 5% on the remaining £670,000 = £ 33,500

- Total SDLT = £33,500

Get to know more about Stamp Duty Land Tax (SDLT).

Check how much you’ll owe in SDLT, using our stamp duty calculator.

How to Apply for a First Time Buyer Mortgage?

At this point, you’ve got a good idea of your budget, mortgage options, and the type of property you’re looking for.

You can use online property search portals to find properties that match your criteria. Once you’ve found a few properties that you’re interested in, here’s what you need to do next:

Step 1: Get an Agreement in Principle (AIP)

Step 2: Start viewing properties

Step 3: Make an offer

Step 1: Get an Agreement in Principle (AIP)

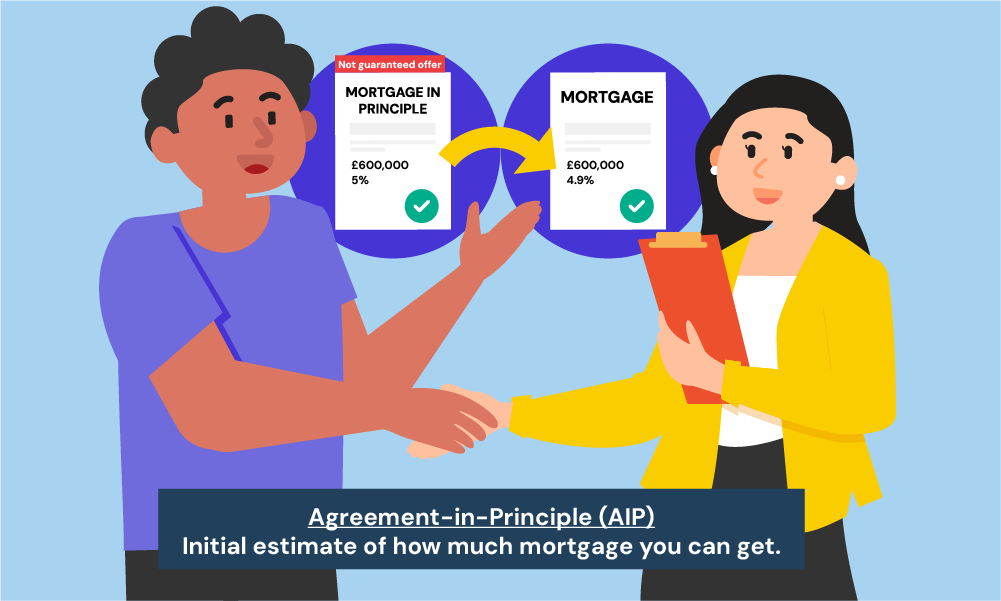

Getting a mortgage is a big commitment, so it’s important to take it seriously. One of the first things to do is get an Agreement in Principle (AIP).

An AIP is a non-binding document that shows how much money a lender is willing to lend you. It’s not a guarantee that you’ll get a mortgage, but it can give you an idea of how much you can afford to borrow.

To get an Agreement in Principle (AIP), you need to provide the lender with information about your income, outgoings, and assets.

Make sure you’ve sorted out your accounts, checked your credit score, and gathered the necessary documents. The lender will use this information to calculate how much money they’re willing to lend you.

An AIP can be a helpful tool for first-time buyers. It can help you:

- Determine how much you can afford to borrow.

- Get an idea of the interest rates you’ll be offered.

- Give you a competitive edge when making an offer on a property.

It’s important to be aware that too many credit checks may affect your credit rating and damage your mortgage application.

Since most lenders’ credit checks will leave a mark on your file. Some provide a ‘soft’ credit check that is not visible.

So, before you agree to one, make sure you know which one it is.

Step 2: Start viewing properties

Once you’ve got a mortgage in principle, you’re good to start viewing properties. It’s important to view as many as you can to find the one that’s right for you.

When viewing properties, take your time, and don’t feel pressured to make an offer on the spot. Ask the seller any questions you have.

This is your chance to find out everything you need to know about the property, so don’t be afraid to ask questions.

Here are some questions you might want to ask:

- How long has the property been on the market?

- Why is the seller selling?

- What renovations have been done?

- Are there any major repairs that need to be done?

- How many viewings has it had?

- How many offers has it had?

- What are the local amenities like?

- How far is it from public transport?

- What are the schools like in the area?

It’s also a good idea to take notes to list your thoughts and impressions as you view properties. This will help you remember what you liked and didn’t like about each property.

Once you’ve viewed a few properties, you’ll start to get a feel for what you’re looking for. You’ll also start to get a sense of what a good price is for a property in your area.

If you find a property that you love, don’t be afraid to make an offer. The worst that can happen is that the seller says no.

But if the seller says yes, you’ll be one step closer to owning your dream home. Remember, buying a property is a big decision, so take your time and don’t rush into anything.

Step 3: Make an offer

Have you found a property you like? It’s time to make an offer!

The seller will decide whether to accept it or not.

How much to offer can be tricky. It’s common to offer below the asking price, but it depends on the individual property.

If other people are interested or the market is hot, you may need to offer the asking price or more.

Once you’ve decided, give the estate agent a call or pop in to see them. It’s also a good idea to put your offer in writing.

The offer should include the price you’re willing to pay, the date you’re willing to move in, and any other terms you’re willing to negotiate.

Step 4: Begin with the mortgage application

If your offer is accepted, it’s time to apply for a mortgage!

You can do this directly with your lender or hire a mortgage broker.

We’d highly recommend using a good mortgage broker. They can save you a lot of time and hassle by comparing deals from different lenders and finding the best one for you.

Of course, you can always do this yourself, but if you’re not sure where to start, a broker can be a great help.

During your mortgage application, your lender will do a mortgage survey on the property and check your affordability to make sure they’re happy lending you the money to buy it.

They might think you’re paying too much, in which case you might need to put down a bigger deposit or negotiate a lower price with the seller.

Make sure you’ve completed all the paperwork, answered your lender’s questions, and had a ‘hard’ credit check. This can all take up to 4–6 weeks.

If everything goes to plan, you’ll get a mortgage offer. Check the offer carefully.

Once you’re happy with it, sign it and work with your solicitor to exchange contracts.

Step 5: Complete the process with a Solicitor

Now, you need to appoint a solicitor or conveyancer to handle the legal side of the deal. They’ll check the property for any legal issues and draw up the contracts.

You’ll need to give them the details of the property you’re buying and the mortgage you’ve been approved for.

They’ll do searches on the property and check for any planning restrictions or environmental hazards.

The solicitor will then prepare the legal contracts for transferring ownership of the property. Once they’re ready, you’ll need to sign them and pay a deposit.

Finally, exchange the signed contracts with the seller to make the sale legally binding.

Congratulations! You’re now officially committed to buying the property.

Government Schemes Available to Help First-Time Buyers

Mortgage interest rates have gone up in 2024, making it more expensive and harder to borrow money.

But there are government schemes that can help you buy your first home, like the Lifetime ISA, Help to Buy, Right to Buy, and Shared Ownership.

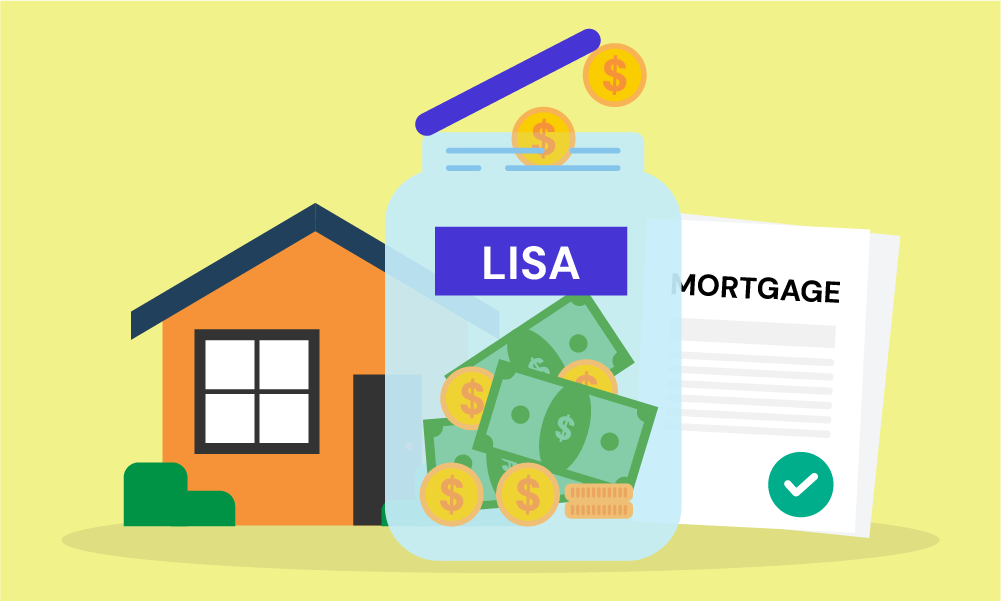

Lifetime ISA (Individual Savings Account)

A Lifetime ISA (Individual Savings Account) is a great way to save for your first home or retirement. You can open one if you’re:

- Aged between 18 and 39,

- A UK resident, or a crown servant (for example, a member of the armed forces serving abroad).

Here’s how it works:

- You can save up to £4,000 a year in a Lifetime ISA until you’re 50.

- The government will add a 25% bonus to your savings, up to a maximum of £1,000 a year.

This means that if you save £4,000 in a LISA, the government will add an extra £1,000 (4,000 x 25%), giving you a total of £5,000.

You can hold cash or stocks and shares in your Lifetime ISA, or have a combination of both. The amount you pay into a Lifetime ISA is linked to your annual ISA allowance.

For the tax year 2023 to 2024 tax year, this is £20,000. For example, if you pay £1,000 into a Lifetime ISA, you can still pay £19,000 for other ISA products.

You must make your first payment before you’re 40. Once you hit 50, you can’t pay into a Lifetime ISA or get the government bonus. But your account will stay open and your savings will still earn interest or investment returns.

If you are to use Lifetime ISA to buy your first home, there are a few things you need to consider:

- The property must cost no more than £450,000.

- You must have opened your Lifetime ISA and made at least one payment at least 12 months before you buy the property.

- You must intend to live in the property as your main home.

- You must use a conveyancer or solicitor to act for you in the purchase.

- You must use a traditional repayment mortgage.

If you’re buying your first home with someone else, you can both use your LISA savings and bonus.

You’ll have to pay a 25% penalty if you withdraw money from your LISA for any other reason, unless you are – over 60 years old, buying your first home, or terminally ill, with less than 12 months to live. The penalty is designed to recover the government bonus you received on your original savings.

Overall, if you are thinking about saving for your first home, a Lifetime ISA is a great option. You can open one online or at a bank or building society.

Learn more about Lifetime ISA.

Help to Buy ISAs

Help to Buy ISAs are no longer available to new applicants.

If you already have one, you can use it to buy a home worth up to £250,000 outside London (£450,000 in London).

You can keep saving into your account until November 2029, and claim the government bonus by November 2030.

You can get a better rate by changing providers or transferring your Help to Buy ISA to a Lifetime ISA.

Read more about help to buy ISAs.

The Help to Buy: Equity Loan

This scheme is closed to new applications. If you missed it, don’t worry, there are other government schemes you could consider to help you buy a home.

The Help to Buy scheme in England offers equity loans to first-time buyers to buy a new home. It can’t be used to buy a second home or a buy-to-let property.

The scheme lets you borrow up to 20% (or 40% in London) of the price of a new-build home from the government. You’ll need to make a deposit of at least 5% and take out a mortgage for the remaining 75%.

For example, if you wanted to buy a £200,000 home, you’d need a deposit of £10,000 (5% of the purchase price) and a mortgage for £150,000 (75% of the purchase price). The government would then lend you £40,000 (20% of the purchase price).

You won’t have to pay interest on the equity loan for the first 5 years. After 5 years, you’ll start paying interest at 1.75%.

The interest rate will be reviewed every year in April and will be increased by the Consumer Price Index (CPI) plus 2%. You’ll pay back the equity loan in full when you sell your home.

Keep in mind that the maximum purchase price for a Help to Buy property varies depending on the region of England you reside in. Check the specific limits for your area to ensure you can use Help to Buy for properties that don’t exceed these limits.

Learn more about Help to Buy: Equity Loan.

First-Homes

If you’re a first-time buyer with a household income of less than £80,000 (£90,000 in London) and you can get a mortgage for at least half the price of the home, you could be eligible for the First Homes scheme.

The scheme was launched in June 2021 to help first-time buyers get on the property ladder. You can get a discount of 30% to 50% on new-build homes in England, and homes bought as part of the scheme.

Homes under the scheme can’t cost more than £420,000 in London or £250,000 elsewhere in England, after the discount.

You can only sell the house to another first-timer, and you must give them the same discount you got. The discount is based on the home’s market value at the time of sale.

The local council might also set some rules about who can get the discount, like giving priority to essential workers, people who live in the area, and people on low incomes.

If you’re keen to apply, get in touch with the developer or estate agent of a previous First Home buyer. They’ll be able to tell you more about it and how to apply.

Find more about the First Home Scheme.

Right to Buy and Right to Acquire

Right to Buy and Right to Acquire are schemes that allow council or housing association tenants to buy their homes at a discount.

Right to Buy

Right to Buy allows council tenants to purchase their homes at a reduced price. But as of November 2024, the maximum discount has been cut down to:

- Up to £38,000 in most areas of England

- Up to £16,000 in areas with lower property values

Your discount depends on:

- How long you’ve been a tenant with a public landlord

- Where you live in the UK

- The type of property you’re buying

- The market value of your home

You can apply if:

- You’re the main tenant.

- You’ve rented from a public landlord (like the council) for at least three years (this doesn’t have to be consecutive).

- You plan to live in the home after buying it.

- Your home isn’t newly built—new-build council homes are now excluded from the scheme.

You can’t apply if:

- You’re facing eviction.

- You have large debts or are bankrupt.

- Your home is specifically designed for elderly or disabled tenants.

- There’s a shortage of council homes in your area.

One major change: Local councils now keep 100% of the sale proceeds and must reinvest the money into building new affordable housing

Right to Acquire

If you rent from a housing association instead of the council, you might qualify for Right to Acquire, which offers smaller discounts.

Depending on where you live, you could get between £9,000 and £16,000 off the purchase price.

You can apply if:

- You’ve been renting from a housing association for at least three years.

- You want to keep living in the home after buying it.

- Your home was built with government money for social housing or was transferred from the council to a housing association after 31 March 1997.

- Your landlord is officially registered as a social housing provider.

You won’t be able to apply if:

- You’re at risk of eviction or have large unpaid debts.

- You already have the preserved Right to Buy from before the housing association took over your property.

If you’ve used Right to Buy or Right to Acquire before, your discount may be lower the next time you apply.

Your discount might be reduced if you’ve used Right to Acquire or Right to Buy in the past.

If you’re buying with someone else, you can count the tenancy years of whoever has been a public sector tenant the longest.

But keep in mind: If you sell your home within five years, you might have to pay back some or all of the discount.

Learn more about Right to Buy and Right to Acquire.

Shared ownership

This is a scheme that allows you to buy part of a property and rent the rest. It’s a good option if you can’t afford to buy a whole property outright.

You can buy a share of a property between 10% and 75% with a mortgage or your savings. You’ll still need to put down a deposit, which is usually between 5% and 10% of the share you’re buying.

Once you’ve bought a share of a property, you’ll need to pay rent on the remaining share to the housing association or owner.

You’ll also pay monthly service charges, which cover the cost of maintaining the property and communal areas.

Some housing associations let you staircase, which means buying a bigger slice of your home over time until you own it all. This can help you get on the property ladder and build up equity in your home over time.

Find out more about Shared Ownership and check your eligibility here.

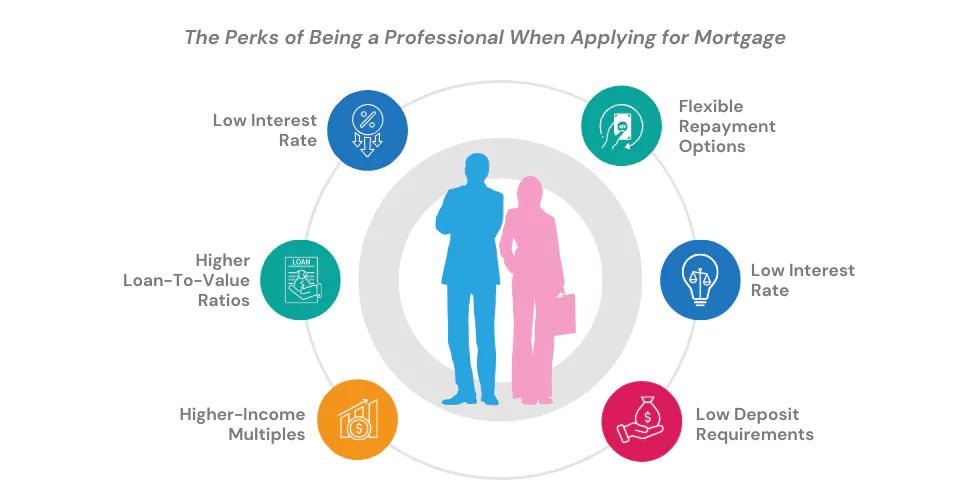

Mortgages for professional and skilled workers

Mortgages for professionals and skilled workers are a type of loan designed for people in certain jobs. These jobs tend to have high salaries and job security, which makes them attractive to lenders.

As a result, professionals often get better interest rates and terms on mortgages.

Here are some examples of professions that are typically eligible for mortgages for professionals and skilled workers:

- Medical professionals such as doctors, pharmacists, optometrists, dentists, vets, and nurses.

- General professionals such as solicitors, barristers, accountants, architects, and surveyors.

- Key workers such as police officers, firefighters, members of the military, teachers, social workers, and civil servants.

- High earners such as those earning over £100,000 per year; company directors and executives; investment bankers; and asset-rich individuals.

It is important to note that not all lenders offer mortgages for professionals and skilled workers. If you are interested in this type of mortgage, you should speak to a mortgage advisor to find out more about the different lenders that offer them.

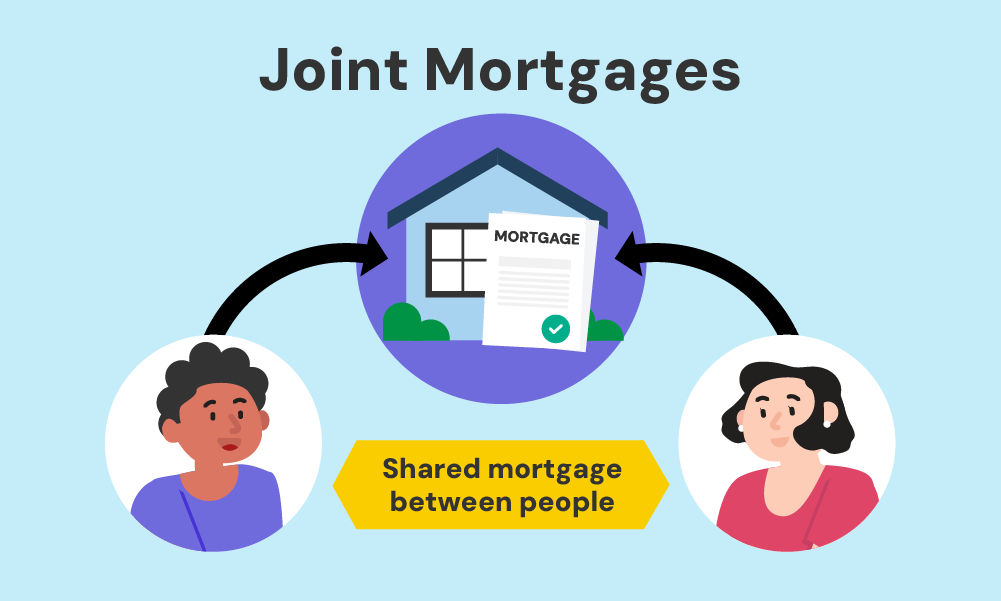

Getting Into Property Ownership With Another Person

Many first-time buyers get a joint mortgage, which can help them raise a higher deposit and share the cost of the mortgage. Let’s take a look at how these different structures work.

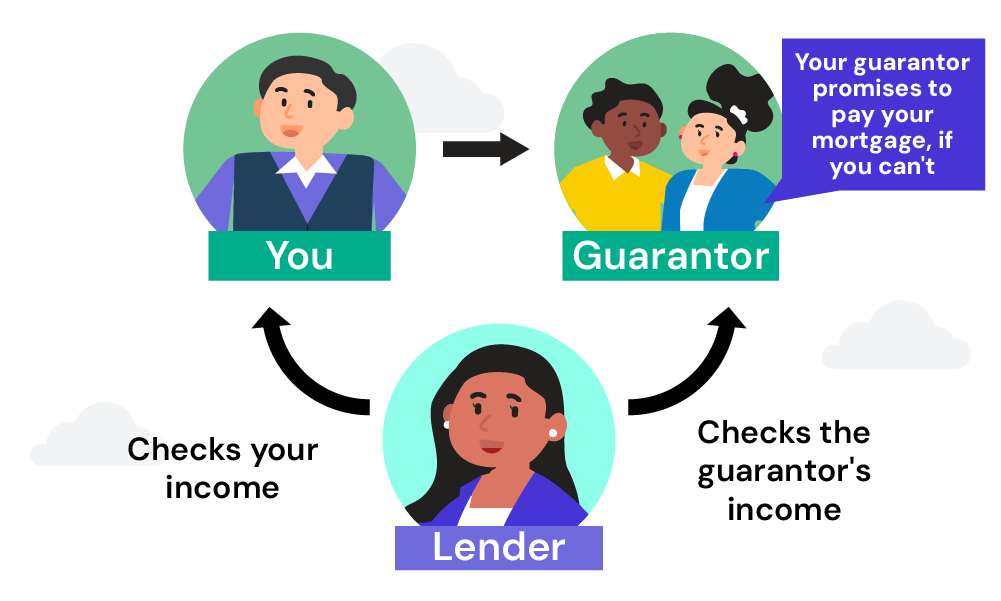

Guarantor Mortgages

A guarantor mortgage is a type of home loan where a close relative, usually a parent, agrees to be responsible for the mortgage payments if the borrower defaults.

This usually means they put up their home or money as security for your mortgage and promise to pay the mortgage if you don’t.

Some guarantor mortgages let you borrow the full value of a property by using your parents’ assets as security instead of a deposit.

The main advantage of a guarantor mortgage is that it can help you borrow more money if you’re struggling to get a mortgage on your own.

The main disadvantage is that the guarantor is liable for any shortfall if you default on your mortgage, which could mean losing their assets or even their home.

If you’ve got a good relationship with a family member or friend who’s willing to be your guarantor, a guarantor mortgage could be a good option for you. But it’s important to understand the risks before you commit.

Joint Mortgages

Tenants in Common vs. Joint Tenants

When you buy a property with another person, you can choose to be either joint tenants or tenants in common.

The difference between the two is that joint tenants own the property equally, while tenants in common can own different shares.

Take a couple buying a property with a 50/50 share: they’d be joint tenants, meaning they’d be equally liable for the mortgage repayments and each own a 50% share of the property.

A couple buying a property with a 70/30 share would be tenants in common, each liable for 70% and 30% of the mortgage repayments respectively. They’d also need a mortgage with a declaration of trust to specify the different shares in the property.

With joint tenancy, you can’t leave your share of the house to anyone who isn’t already a joint tenant in your will. With tenancy in common, you can leave your share to anyone you want.

To qualify for a mortgage, you will need to meet the same criteria as you would for any other type of mortgage. This includes having a good credit score, a stable income, and a deposit of at least 5% of the property value.

Trust is key when taking out a joint mortgage, as you’ll both be equally responsible for the repayments.

If one of you doesn’t make a payment, the other will have to cover it. So make sure you’re both aware of the risks and requirements before you commit.

Benefits of Having a Professional Mortgage Advisor

Mortgage brokers are qualified and regulated advisers who can help you find the best mortgage deal for your needs.

With so many different deals available and the market changing all the time, it can be difficult to know where to start.

A whole-of-market broker can take the stress out of the process and help you find the best deal possible.

They can quickly find a mortgage that suits your needs and credit history. They can also offer you extra protection if things go wrong, and they have more clout with lenders, which can help you get a mortgage that you might not otherwise be able to get.

When choosing a professional mortgage advisor, make sure to ask about their qualifications, what lenders they have access to, their fees, and how they will support you after you get a mortgage.

If you want an easy way to find the right broker, get in touch with us. We’ll set up a free, no-obligation chat with a top mortgage advisor who can help you solve your mortgage situation and get the best deal.

Tips to Boost Your Chances of Getting a Mortgage

Check Your Credit File, Before the Mortgage Lender Does

You need to show mortgage lenders that you’re good for the money.

They’ll want to see that you’ve got a steady income, a good credit score, and a history of making your payments on time.

It’s free to get a copy from each of the three credit reference agencies: Experian, Equifax, and TransUnion.

Once you have your credit file, check it carefully for any errors. If you see anything wrong, contact the credit agency immediately.

Make sure your personal details and account information are all up to date. If you see anything suspicious, contact your creditor right away.

Sort Out Your Accounts

Make sure you don’t have any unused credit cards or inactive accounts. It’s best to have all your active accounts linked to the same address.

Sort Out Your Financial Ties with Your Ex

If you’re still financially linked to your ex, their credit history will be considered when you apply for a mortgage.

This means that if they have a bad credit history, it could make it more difficult for you to get a mortgage.

To delink from your ex, you’ll need to contact the credit reference agencies. You can do this online or by mail.

Be on the Electoral Roll

It helps prove your residency, which can boost your credit rating. Head to this government website to register or check your status.

Ensure that You Pay All of Your Bills on Time

It’s a surefire way to show lenders you’re a reliable borrower.

Missed payments can damage your credit score, so it’s important to make all of your payments on time.

If you’re struggling to make payments, contact the company as soon as possible to see if you can make payment arrangements.

Tighten Your Belt Before You Take Out a Mortgage

This means that you should reduce your spending before you apply for a mortgage. This will make it more likely that you will be approved for a mortgage and that you will be able to afford the monthly payments.

Lenders will want to see your bank statements to see how much you spend each month. This is because they have to ‘stress test‘ borrowers to make sure they can afford the monthly payments even if interest rates go up.

A stress test is a financial analysis that lenders use to assess a borrower’s ability to repay a loan under difficult economic conditions.

It typically involves increasing the borrower’s interest rate and decreasing their income.

Avoid Dipping into Your Overdraft if You Can

If you’re constantly using your overdraft, it could be seen as living beyond your means. Some lenders may not lend to you if you’ve been in your overdraft in the last three months.

So it’s best to stay out of it if you’re thinking of getting a mortgage.

Get Your Paperwork in Order to Speed Up the Process

Lenders need proof of your income before they can offer mortgages, so it’s a good idea to get your paperwork together in advance.

Don’t Apply for a Mortgage After Being Rejected

Too many rejections can damage your credit score and make you look desperate. After being rejected, the first thing you should do is check your credit file again.

If everything looks good, it’s worth asking the lender for the reason they turned you down. You can also try speaking with a good mortgage advisor.

Key Takeaways

- You’re a first-time buyer if you’ve never owned a residential property in the UK or abroad.

- To qualify for a first-time buyer mortgage, you need a 5% deposit, legal UK residency, and meet specific lender criteria.

- A larger deposit often means better mortgage terms; aim for at least 10% if possible.

- Repayment mortgages are the most common for first-time buyers; consider fixed-rate for stability or variable-rate for potentially lower costs.

- Be aware of additional mortgage fees, such as arrangement fees, Stamp Duty, and early repayment charges.

- Government schemes like the Lifetime ISA and Shared Ownership can help with buying your first home.

- Improve your chances of approval by checking your credit score, organising your finances, registering to vote, and maintaining a steady income.

Glossary

Asking price – the price that someone wants for something they are selling. It is also known as the sale price or the asking rate.

Bankruptcy – the legal process that is used to deal with people who are unable to pay their debts.

Buy-to-let Landlords – people or companies who buy properties to rent out to tenants. They typically borrow money to buy the property and then use the rent to repay the mortgage and make a profit.

Council home (also known as social housing or public housing) – a type of rental accommodation that is owned and managed by a local authority.

Credit score – a number or rating that lenders use to assess your creditworthiness.

Declaration of Trust – a legal document that sets out the ownership of the property and the rights of each person.

Estate agent – a person or company that helps people buy, sell, or rent property.

Exchange of contracts – when the buyer and seller sign a legally binding agreement to sell and buy a property. This is the point of no return, as neither party can back out without facing legal consequences.

Guarantor – a person who agrees to be responsible for repaying a loan if the borrower cannot. Guarantors typically offer their own assets as security against the loan

House association – a type of non-profit organisation that provides affordable housing to people in need.

Independent Surveyors and Valuers Association (ISVA) – a national body for independent chartered surveyors who provide impartial expert advice on residential and commercial property.

Lender – a person or organisation that lends money to another person or organisation.

Mortgage Survey – a check by the lender to make sure the property is worth what you’re paying for it. It can also help you decide if you’re paying too much or too little.

Overdraft – a type of loan that allows you to borrow money from your bank when you don’t have enough money in your account

P60 – a document that shows how much tax you’ve paid on your salary in the UK tax year (April to April). You’ll get a separate P60 for each job you have each tax year.

Public Sector landlord – a landlord that is owned and managed by a public body, such as a local authority or a housing association. They are regulated by the government.

Preserved Right to Buy – means that if you’re a secure council tenant and your home was sold or transferred to another landlord, like a housing association, while you were living there, you may have the right to buy.

Residential Property Surveyors Association (RPSA) – a non-profit organisation that represents independent residential surveyors. These surveyors are the leading experts in reporting on the condition of residential properties for homebuyers.

Royal Institution of Chartered Surveyors (RICS) – a globally recognised professional body for surveyors founded in 1792.

SA302 – a summary of the income you’ve reported to HMRC. It’s only issued to people who submit their tax returns by October 31st (for paper returns) or January 31st (for online returns).

Secured loan – a business or personal loan that requires the borrower to put up some kind of collateral, such as a car or house, as security for the loan.

Solicitor or Conveyancer – a legal professional who helps to transfer the ownership of land or buildings from one person to another. They must take reasonable care when carrying out their work.

Stress test – a financial analysis that assesses the ability of a borrower to repay a loan under adverse economic conditions.

Surveyor – is a term to refer to a person who inspects buildings to make sure they are in good condition.

Threat of eviction – a warning from a landlord that they may evict a tenant from their home. Eviction is the legal process of removing a tenant from their home. It can happen for many reasons, such as non-payment of rent, breach of the tenancy agreement, or antisocial behaviour.

Unsecured loan – a loan that does not require the borrower to put up any collateral.

The Bottom Line

That’s it. We’ve cracked the mortgage code! 😀

As a first time buyer, the journey towards homeownership may feel like a rollercoaster. But, we hope this guide has helped you.

To make things easier, we highly recommend consulting an experienced mortgage broker.

Want to save time and effort? Get in touch. We’ll connect you with a trusted broker who can help you find the perfect mortgage.

Good luck with your house hunt!

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What documents do I need before applying for a mortgage as a first-time buyer?

Different lenders will request somewhat different documents, but almost all of them will ask about:

- Proof of identity (e.g., passport, driver’s licence)

- Proof of address (e.g., utility bills, bank statements)

- Proof of income (usually the last 3 months of payslip and P60 for a full-time employee. And SA302 tax returns and accounts from the last 3 years, if self-employed.)

- Bank statements demonstrating your savings and deposit

- Details of any outstanding debts or financial commitments

Can I still get a mortgage if I am Self-Employed?

Yes, you can. But you might need to show lenders more proof of your income than someone who has a regular job. Lenders will consider you as self-employed if you’re a freelancer, contractor, sole trader, or limited company director/partner.

It’s a good idea to talk to a mortgage broker who specialises in helping self-employed people get mortgages. They’ll be able to help you find a lender who’s willing to give you a mortgage and who understands your unique situation.

Can I still get a mortgage if I have bad credit?

Yes, it’s possible, but it’ll be harder. Lenders will be more cautious about lending to you, so you’ll need to show them that you’re a good risk. To give yourself the best chance of getting a mortgage, take the time to improve your credit report before applying for a mortgage.

Don’t overstretch yourself when getting a mortgage. You can only afford a mortgage if you can comfortably afford the monthly payments.

>> More about How To Get a Mortgage with a Bad Credit?

What is the mortgage APRC?

APRC stands for Annual Percentage Rate of Charge. It shows you the total cost of a mortgage, including fees, over the entire term of the loan. This means that you can compare different mortgages and see which one is the cheapest overall.

For example, a mortgage with a low-interest rate might seem like a good deal, but if it has high fees, it could end up being more expensive than a mortgage with a higher interest rate but lower fees. By paying attention to APRC, you can get the full picture of what you’ll be paying and make sure you’re getting the best deal possible.

Related Articles

What Is Classed As A First Time Buyer In The UK?

Buying a home is both exciting and daunting, especially if it’s not your first rodeo. The rules around who qualifies as a true “first-time buyer” can be confusing. Getting this wrong could cost you valuable money through missed tax reliefs and prime mortgage deals. Whether you’re just stepping onto the property ladder or boomeranging back […]