- Can Legal Professionals Get Better Mortgage Deals?

- Why Do Some Legal Professionals Find it Hard to Get a Mortgage?

- What Mortgage Deals are Available to You?

- How Much Can You Borrow as Barristers, Lawyers, or Solicitors?

- Mortgages for Self-Employed Lawyers or Partners in a Law Firm

- Mortgages for Barrister or Solicitor Trainees

- The Bottom Line

Legal Professional Mortgages: A Guide Made Easy For Lawyers

Thinking of buying a home as a legal professional?

We know your life can be hectic. You’re always juggling your busy schedule, working long hours, and dealing with stress in the courtrooms.

The last thing you want to do is spend hours trawling the internet about mortgages. To save you from that, we’ve done the research and made this guide for you.

In a few minutes, you can learn everything you need to know about mortgages for legal professionals. Whether you’re employed, a partner, or a trainee, this guide has you covered.

So without further ado, let’s get started.

Can Legal Professionals Get Better Mortgage Deals?

Yes. As a legal professional, you are in a strong position to secure a mortgage. Lenders see your profession as a safe bet with high earning potential and job security.

This means that they are more likely to lend you money over other professions.

There are no specific mortgage products aimed at barristers, lawyers, or solicitors. But you can get better mortgage deals with more flexible underwriting and terms. You might even get lower fees or a better interest rate.

When applying for a mortgage, lenders may offer you the following benefits:

- Higher-income multiples to borrow more money

- Improved overpayment terms without penalty to pay

- Ability to borrow back so you can access the equity in your home

- Mortgage repayment holidays for more flexibility

- Lower fees and better rates

- Lower deposit requirements

- A smoother application process

Mortgage deals vary and some lenders are strict with their criteria, especially if they don’t understand how legal professionals earn money.

You might struggle to find a lender who’ll give you a a better mortgage deal, if your circumstances aren’t common.

Why Do Some Legal Professionals Find it Hard to Get a Mortgage?

Lenders can sometimes find it tricky to work out the complex income streams of legal professionals, which can make getting a mortgage a bit of a pain.

Normally, they multiply your annual salary or average earnings by four or five to determine how much they can lend you. Not too complicated, right?

But this isn’t always the case for legal professionals, who often have variable and unpredictable incomes.

For example, a legal professional could earn money from self-employment, based on billable hours. They could also have multiple income streams from different aspects of their work, such as earnings in foreign currencies, royalties, bonuses, dividends, profit-sharing, and other legal services.

Most high street lenders don’t count these variable incomes, which can reduce your potential to borrow. You might’ve been turned down in the past, even though you could afford the repayments.

And if you’re a trainee, you might struggle to get a mortgage, as you’re on a short-term contract and have a big student loan.

Still, there are specialist lenders who’ll lend to lawyers like you. They have a more flexible approach to assessing your mortgage application and will consider all aspects of your income.

If you don’t want to miss out on that opportunity, it’s worth speaking to a good mortgage broker who knows the market and has experience with mortgages for legal professionals. They can help you find the right lender and get a better deal that’s best for your profession.

What Mortgage Deals are Available to You?

Legal professionals have access to all types of mortgages. It all comes down to what you prefer. Here are the options that might be suitable for you:

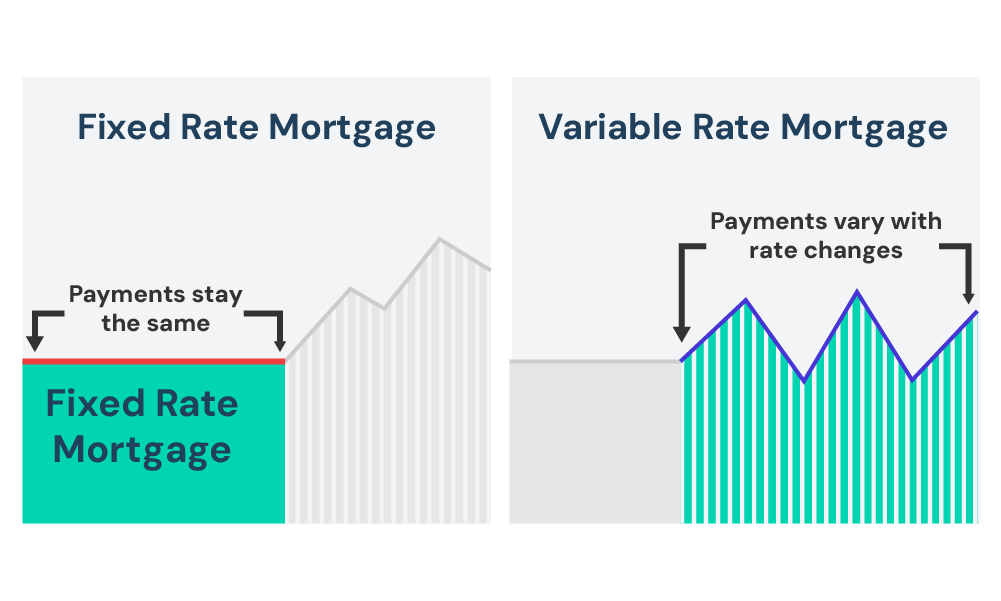

- Fixed-Rate Mortgages

- Variable-Rate Mortgages

- Flexible Mortgages with Payment Holiday Option

- Flexible Mortgages with Option to Overpay

Let’s say, you like to budget carefully, a fixed-rate mortgage could be a good option. This will give you certainty and peace of mind, as your monthly payments and interest rates will not change for a period of usually 2 to 10 years.

If you think interest rates are likely to fall soon, a variable-rate mortgage might be the way to go. Be aware that the interest rates could rise, so it’s important to consider the risks as this mortgage type is more unpredictable.

And if you earn income irregularly, you can opt for a flexible mortgage with payment holiday options. This will allow you to pause your mortgage payments for a period of time, giving you some financial breathing space.

When you’re shopping around, you might find flexible mortgages that let you overpay, which can help you pay off your debt quicker and save more money.

Make sure you read your mortgage agreement carefully before making any overpayments, as some lenders might charge a fee.

No matter what your needs are, there’s a mortgage deal out there that’s right for you. It’s best to know your options and choose the deal that suits your financial situation.

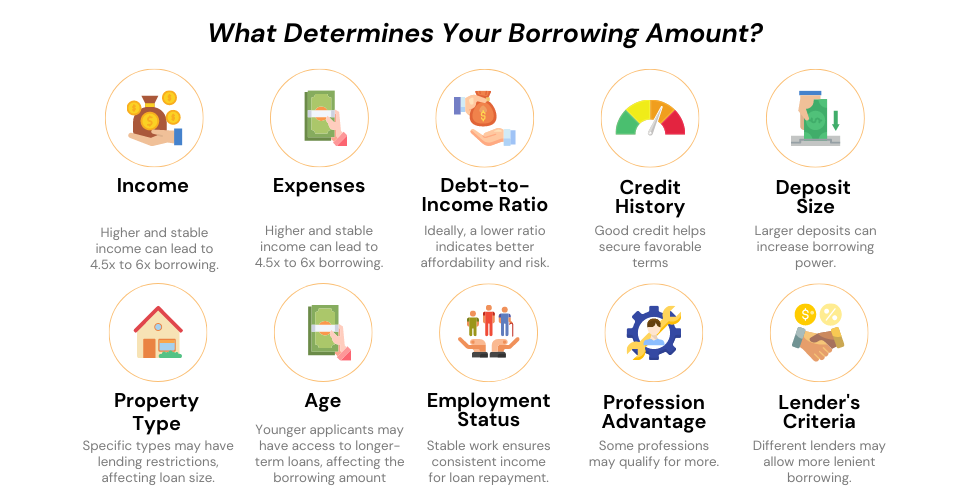

How Much Can You Borrow as Barristers, Lawyers, or Solicitors?

The amount you can borrow will depend on your lender’s affordability assessment. They’ll look at your income, outgoings, debts, credit score, employment history, family situation, and the nature of your income.

They also consider the size of your deposit. A 5% deposit is the minimum, but a bigger deposit could get you a better deal. So, it’s a good idea to be fully prepared before applying for a mortgage.

Generally, legal professionals are high-earners and low-risk borrowers. This means you could get better deals and borrow more money than others. But it’s still best to make yourself attractive to mortgage lenders.

As mentioned earlier, lenders in the UK usually use income multiples to determine how much they will lend you. This is capped at 4 or 6 times your annual salary.

It’s relatively straightforward if you earn income through PAYE. However, if you earn income through other means like freelancing, dividends, or share profits, lenders may find it more challenging to work out how much they can lend you.

Mortgages for Self-Employed Lawyers or Partners in a Law Firm

As a self-employed lawyer or law firm partner, getting a mortgage can be a bit more tricky than for a salaried lawyer.

Despite being able to afford the property you want, lenders may require more evidence of your earnings due to the complexities of your income.

Ideally, here’s what lenders need as proof of your income:

- 2 or more years of certified accounts, preferably prepared by a qualified accountant.

- 2 – 3 years of SA302 forms or a tax year overview from HMRC.

- Other supporting documents such as future contracts, or profit-sharing proof if any.

Having a good understanding of your income can help you explain it to your lender. They might take all your income into account when deciding on your loan.

For example, some specialist lenders may be willing to consider your income in foreign currency, as long as they understand your income structure and you can provide proof.

If you’re a new partner in a newly formed law firm, you might struggle to get a mortgage. Some lenders may allow at least one year’s accounts, but it can be tough to find one who’ll accept this.

That’s where a good mortgage broker comes in. They can find you the best deal and take the hassle out of the process.

Plus, as you’re in a prestigious and respected industry, lenders are more likely to offer you flexible lending criteria.

Mortgages for Barrister or Solicitor Trainees

You’ve completed your legal practice course and started training. Now, you’re thinking about getting on the property ladder sooner. But how likely are you to get a mortgage?

You’re likely to get a mortgage as a trainee, but some lenders may be hesitant as you’re on a 2-year fixed-term contract and don’t have much work history. This means you may not get the same benefits as a fully qualified solicitor.

Don’t let this put you off though. Lenders will still consider your future earnings and stability, which can give you an edge and lead to better deals.

There’s no need to rush into getting a mortgage. You can wait until you’re fully qualified.

But, if you’re keen to get on the property ladder sooner, you could get a guarantor mortgage. Once you’ve qualified, you can then remortgage to make the most of the perks.

As a trainee, your mortgage options will depend on many factors. It’s best to speak with a good mortgage broker first for tailored advice.

Will Having Student Loan Debt Affect My Mortgage Application?

Yes, student loans can affect your mortgage application, but it won’t stop you from getting one. Lenders view student loans as lower-risk debts, as they often lead to well-paid careers.

They will most likely be more interested in your monthly repayments than the total amount you owe. This is to assess your ability to pay and your track record of repaying debt.

In your application, lenders will typically consider your future earnings, savings, and credit score.

You’ll need to provide at least 3 months of bank statements, proof of your deposit, and a copy of your training contract or projected income, if any.

Working with a good mortgage broker who has experience can introduce you to the right lender to help you step on the housing ladder earlier.

The Bottom Line

Barristers, solicitors and lawyers are in an advantageous position to get a mortgage in the UK. Your high earnings and job security make you attractive to lenders.

You can often borrow more than other borrowers.

It’s worth noting that mortgage deals can vary, and your borrowing amount will depend on many factors. Generally, the higher your income, the more you can borrow.

Your credit score and deposit size will also play a part. So, make sure you have saved enough before applying.

Don’t waste time looking for a mortgage. Let a good mortgage broker do the work for you. They’ll find the best deal and handle all the paperwork, just like having your own personal assistant. With them, you can relax and enjoy the house-buying process.

To seize this opportunity, get in touch with us today. We’ll match you with an excellent mortgage broker who specialises in mortgages for lawyers.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Am I eligible for a solicitor, lawyer, or barrister mortgage?

There are no pre-made mortgage products for solicitors, lawyers, and barristers. But your professional status as a lawyer gives a better chance of getting a mortgage with flexible underwriting and terms.

Every lender has their own eligibility criteria, but they will usually consider your income stability, credit score, debt-to-income ratio, and deposit size. It’s best to be prepared before applying for a mortgage.

Who are the best mortgage lenders for lawyers and how can I get a mortgage from them?

Some high street banks and mainstream lenders offer mortgages for professionals, but the best option for you will depend on your individual circumstances. Professional mortgages from private lenders and mortgage specialists are often more attractive, as they offer lower interest rates and fees.

Once you’ve sorted your finances, got your documents in order, checked your credit rating, and saved for a deposit, you can start shopping around for quotes from different lenders. Make sure you compare each deal before accepting one.

Having a good mortgage broker can make this process a breeze, they will put you in touch with the right lender, and negotiate on your behalf.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Police Mortgages: A Definitive Guide in 2025

Police officers are never off duty. You put your lives on the line every day to keep us safe. But amidst your noble service, you face a unique challenge: securing a mortgage. As a police officer, time can be your enemy. The demands of your profession, the irregular shift patterns, and the sacrifices you make […]

NHS Mortgages: What You Need to Know Before Buying a Home

If you work for the NHS, you’re no stranger to hard work. You put in long hours, manage unpredictable shifts, and care for those who need it most. But when it comes to buying a home, the process can feel unnecessarily complicated. Your irregular hours, varied income, and short-term contracts might make it seem like […]

A Complete Guide: Mortgages for Professionals

If you’ve worked hard, got yourself qualified, and are ready to buy a house, you might be wondering if there are mortgages for professionals like you. The good news is – there are! Mortgage lenders offer professional mortgages with favourable and flexible terms. As a professional, you’ve shown that you’re responsible and have a predictable […]