- Are There Special Mortgages for NHS Staff?

- Can NHS Staff Get Discounts on Mortgages?

- What Schemes Are Available for NHS Workers?

- How Much Can NHS Staff Borrow?

- What Documents Do You Need for a Mortgage?

- Do You Need a Mortgage Broker?

- Can NHS Staff Get a Mortgage With Bad Credit?

- Key Takeaways

- The Bottom Line

NHS Mortgages: What You Need to Know Before Buying a Home

If you work for the NHS, you’re no stranger to hard work. You put in long hours, manage unpredictable shifts, and care for those who need it most.

But when it comes to buying a home, the process can feel unnecessarily complicated.

Your irregular hours, varied income, and short-term contracts might make it seem like lenders don’t understand your reality.

The truth? There’s no special “NHS mortgage” waiting for you. But that doesn’t mean your job can’t help you get better mortgage terms.

This guide will show you how.

Are There Special Mortgages for NHS Staff?

No, there aren’t any exclusive mortgage products made just for NHS employees.

But, being part of a stable profession with regular income can work in your favour.

Some lenders might be more flexible with their lending criteria if you work for the NHS, especially if you’re on a permanent contract or work in a clinical role.

So, while there aren’t dedicated NHS mortgage deals, your job could still help you secure better terms than someone in a less stable profession.

Can NHS Staff Get Discounts on Mortgages?

Not exactly.

There aren’t any exclusive mortgage discounts just for NHS staff. But, some lenders and homebuilders offer perks for key workers, including those in the NHS.

These perks might include:

- Deposit contributions – Some developers could cover part of your deposit, often around 5%. This depends on their own policies and isn’t guaranteed.

- Cashback offers – Certain lenders might give you cashback after your mortgage is completed.

- New-build perks – You could get extras like free flooring or appliances when buying a new home.

These offers aren’t the same everywhere and usually depend on factors like having a permanent contract or working in a clinical role.

Speaking to a mortgage broker can help uncover what’s available.

What Schemes Are Available for NHS Workers?

There aren’t any schemes specifically for NHS staff, but several government programmes can help you buy a home.

While these aren’t exclusive to NHS employees, key workers, including those in the NHS, often get priority.

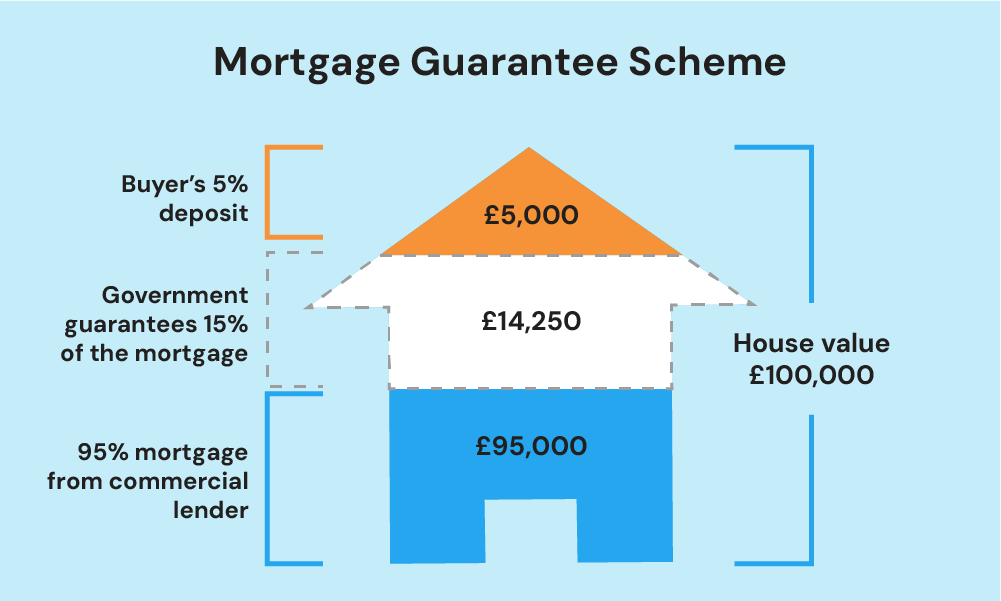

Mortgage Guarantee Scheme

Launched in April 2021, this scheme allows buyers to get a mortgage with a deposit as low as 5%.

The government guarantees 15% of the loan, encouraging lenders to approve applications from those with smaller deposits.

It’s available for properties worth up to £600,000 and can be used by both first-time buyers and existing homeowners.

The scheme has been extended and will accept new 95% mortgages until 30 June 2025.

First Homes Scheme

The First Homes Scheme gives first-time buyers and key workers, including NHS staff, a discount of 30% to 50% on selected new-build homes in England.

This discount stays attached to the property, meaning future eligible buyers will also benefit.

To qualify, your household income must be below £80,000 (or £90,000 in London), and you’ll need a mortgage covering at least 50% of the home’s price.

Local councils can set additional rules, sometimes giving priority to NHS staff, local residents, or those on lower incomes.

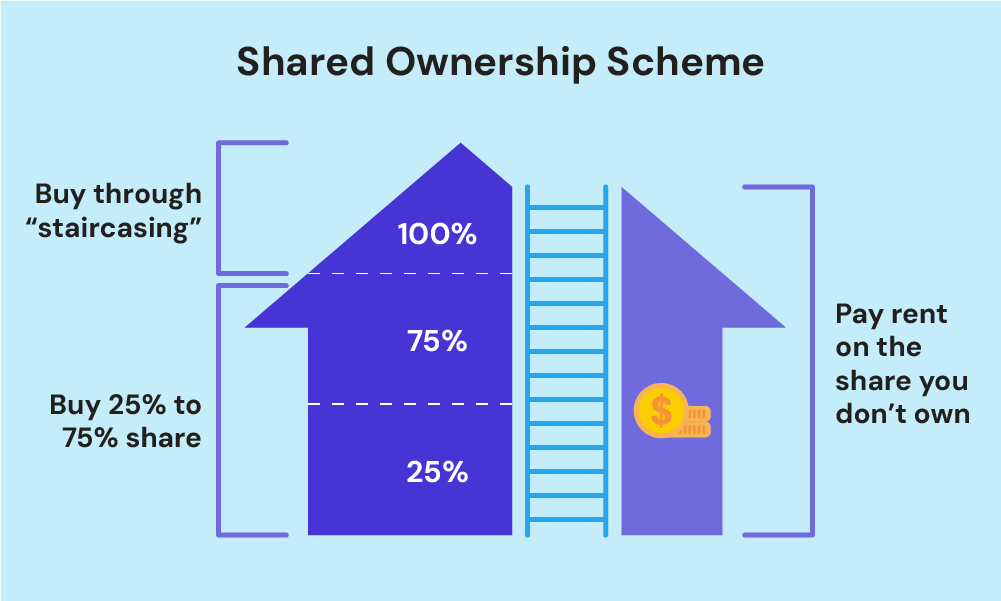

Shared Ownership

Shared Ownership allows you to buy a portion of a property, usually between 25% and 75%, while paying rent on the rest.

You can increase your share over time through a process known as staircasing.

This scheme is aimed at those with household incomes under £80,000 a year (or £90,000 in London) who can’t afford a full mortgage for a suitable home.

Right to Buy

If you’re a council tenant in England and have lived in your home for at least three years, you might be able to buy it at a discount.

In November 2024, the scheme changed. The maximum discount is now capped between £16,000 and £38,000, depending on where you live—a sharp drop from previous limits.

The discounts no longer rise with inflation. The cost floor period—which prevents councils from selling homes for less than they’ve spent on building, buying, or maintaining them—has also been extended from 15 to 30 years.

These changes are designed to protect social housing and help councils replace homes that are sold.

Before applying, check with your local council or a housing advisor to get the latest information.

How Much Can NHS Staff Borrow?

Most lenders work out how much you can borrow by multiplying your income by 4 or 5 times. The exact amount depends on the lender’s rules and your financial situation.

For NHS staff, factors like your role, contract type, and income stability can affect the amount.

For example, if you earn £35,000 a year:

- At 4 times your income, you could borrow up to £140,000.

- At 5 times, the limit could increase to £175,000.

Lenders also consider other factors:

- Expenses – Monthly bills, debts, and regular outgoings can reduce how much you’re allowed to borrow.

- Credit history – Missed payments or outstanding debts might affect your chances.

- Additional income – Overtime, bonuses, and shift allowances may count as extra income and boost your borrowing limit.

What Documents Do You Need for a Mortgage?

When applying for a mortgage, you’ll need to gather several documents to show your financial situation. Here’s a basic list:

- Proof of income: 12 months’ worth of payslips and your P60.

- Employment contract: Especially important for locum or bank staff to show income consistency.

- Proof of ID: Passport, driver’s licence, or another government-issued ID.

- Proof of address: Utility bills or bank statements.

- NHS ID: Some lenders might ask for this to confirm your employment.

- Deposit proof: Bank statements showing you have the required funds.

- Details of any debts: Credit card statements, loan agreements, or other financial obligations.

Do You Need a Mortgage Broker?

While it’s possible to go directly to lenders, working with a mortgage broker can make the process easier.

Brokers can:

- Help you find lenders who are more flexible with NHS staff.

- Suggest mortgage deals that fit your specific circumstances.

- Handle much of the paperwork and liaise with lenders on your behalf.

They can also help you understand the best government schemes for your situation and increase your chances of mortgage approval.

Can NHS Staff Get a Mortgage With Bad Credit?

It’s possible, but your options might be more limited.

Some specialist lenders cater to people with poor credit, but the trade-off is often higher interest rates and stricter terms.

If you have bad credit, it might be worth working on improving your score before applying for a mortgage.

Speaking to a specialist mortgage broker early on may also help you find lenders who are more open to working with applicants who have poor credit.

Key Takeaways

- NHS staff don’t get exclusive mortgage deals, but stable employment can lead to better terms.

- Perks like deposit contributions, cashback, and new-build extras may be available from some lenders.

- Government schemes, including the Mortgage Guarantee Scheme, First Homes Scheme, and Shared Ownership, can help NHS staff buy a home.

- Most lenders offer 4–5 times your income, but factors like contract type, credit history, and extra income can affect this.

- You’ll need documents such as proof of income, ID, an employment contract, NHS ID, and evidence of deposits or debts when applying.

The Bottom Line

Buying a home can be tricky, especially when you’re juggling a busy NHS job and trying to figure out the mortgage process.

While there aren’t any special mortgage deals made just for NHS staff, that doesn’t mean you’re out of luck.

The key is to understand your finances and set clear goals for what you can afford.

From there, a mortgage broker who understands the challenges NHS staff face can help you find better deals, manage the paperwork, and make the whole process feel a lot simpler.

Get in touch with us, and we’ll connect you with a mortgage advisor who understands NHS workers’ needs and will guide you through every part of the journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I overpay my mortgage without penalties?

Most lenders let you pay extra on your mortgage—up to 10% of what you owe each year—without charging extra fees. Paying more than this helps you clear your mortgage faster and saves you money on interest.

But if you go over the limit, you might have to pay a fee, so it’s a good idea to check your mortgage agreement first.

Will working unsociable hours affect my mortgage application?

No, working odd hours won’t hurt your chances of getting a mortgage.

In fact, if you regularly earn extra from night shifts or overtime, lenders might count that as part of your income. This could help you borrow more since your total earnings are higher.

How do zero-hour contracts affect my mortgage application as an NHS worker?

If you’re on a zero-hour contract, some lenders might be a bit unsure because your income isn’t always the same.

But if you can show you’ve earned steady money over 12 to 24 months, it’ll help your chances of getting approved.

Some lenders are also more understanding of NHS staff with flexible contracts, especially if you work with a mortgage broker who knows your situation well.

Can I get a house discount with a Blue Light Card?

There isn’t a specific mortgage deal linked to the Blue Light Card. But, having one can get you discounts on estate agency fees, letting management fees, and even some property services.

It’s always a good idea to ask if businesses offer special deals for Blue Light Card holders—you might be surprised by the savings you can find.

What is a key worker mortgage, and can NHS staff still get one?

The key worker mortgage scheme was a government initiative that once offered special mortgage options for NHS staff and other key workers.

Unfortunately, this scheme is no longer available.

That said, many lenders and brokers still offer flexible terms for NHS workers, so it’s worth exploring other options that might suit your needs.

Related Articles

Police Mortgages: A Definitive Guide in 2025

Police officers are never off duty. You put your lives on the line every day to keep us safe. But amidst your noble service, you face a unique challenge: securing a mortgage. As a police officer, time can be your enemy. The demands of your profession, the irregular shift patterns, and the sacrifices you make […]

A Complete Guide: Mortgages for Professionals

If you’ve worked hard, got yourself qualified, and are ready to buy a house, you might be wondering if there are mortgages for professionals like you. The good news is – there are! Mortgage lenders offer professional mortgages with favourable and flexible terms. As a professional, you’ve shown that you’re responsible and have a predictable […]

Mortgages for Nurses: A Simplified Guide in 2025

Most high-paid professionals can get mortgages easily. But what about nurses? As a nurse, you’re on the front lines, tirelessly caring for others. You’ve faced the challenges of long hours and immense pressure. Especially during the COVID-19 pandemic. But when it comes to getting a mortgage, does your hard work go unnoticed? The truth is, […]