Key Worker Mortgage: An Essential Guide to Housing Schemes

After years of unwavering service, you have set your sights on a new chapter: buying a home.

As a key worker, you’ve been the lifeline of our communities. You’ve kept us going through the COVID-19 pandemic with your selfless dedication to caring, protecting, and educating.

But, amidst your sacrifice, your path to securing a mortgage can be an uphill battle.

Limited savings, high living costs, and strict lending criteria can make owning a home seem impossible. On top of that, you may struggle to find a suitable scheme and identify which lenders are more likely to offer you a mortgage.

Luckily, in this guide, we’ve explored schemes available to you and provided important insights to help you make wise decisions on your mortgage.

So by the end of this, you’ll be well-equipped to take the necessary steps to get a mortgage as a key worker in the UK.

What is a Key Workers Mortgage?

Key worker mortgages are not a specific type of mortgage, but a term for mortgages offered to key workers. Technically, you can apply for the same mortgages as other borrowers, but some lenders offer you preferential treatment.

Specialist lenders in the UK recognise the invaluable contributions of key workers. As a result, you can get mortgages with more favourable terms and benefits. These may come with lower interest rates, lower deposit requirements, and reduced fees.

Even though the Key Workers Programme ended in 2019, there are still schemes available to assist you in getting on the property ladder. We’ll cover these later in this article.

It’s important to know that these schemes aren’t limited to key workers. They could also be available to other eligible borrowers.

Who are the Key Workers?

Key workers provide vital services that keep our country running, especially during times of national importance or crises. In the UK, they’re defined as those who work in the following sectors:

- Health and social care

- Doctors

- Nurses

- Midwives

- Paramedics

- Social workers

- Care workers

- All NHS staff, including administrative and cleaning staff

- Education annd Childcare

- Teachers

- Teaching assistants

- Nursery nurses

- Key public services

- Emergency services staff

- Civil servants

- Journalists

- The local and national government

- Council workers

- Government employees

- Food and other necessary goods

- Farmers

- Delivery drivers

- Shop workers

- Public safety and national security

- Military personnel

- Border guards

- Security guards

- Police and support staff

- Firefighters

- Transport

- Bus drivers

- Train drivers

- Airline pilots

- Utilities, communication, and financial services

- Electricity workers

- Water workers

- Telecommunications workers

- Bankers

Housing Schemes Available to You

With the end of the old Key Worker Programme and the Help to Buy: Equity Loan, you might be looking for housing schemes to help you afford a mortgage. So below we listed some standard schemes that might be a suitable option for you:

First Homes Scheme

Replacing the old Key Worker Programme, this scheme runs until September 2023. It allows first – time buyers and key workers to buy their first home with a discount.

How does it work?

First time buyers earning less than £80,000 per year (£90,000 in London) and eligible key workers can get a discount of 30% to 50% on new-build homes in England.

The discount stays with the property for life. So if you sell it to another eligible buyer, they’ll get the same discount.

Best for: Local first-time buyers and key workers who meet the eligibility criteria, and can’t afford a home at full price.

Shared Ownership

This scheme lets you part-buy and part-rent a property. It’s an affordable way for you to get on the property ladder, as you can buy more share of the property over time.

How Does it Work?

- You buy a share of the property, typically ranging from 25% to 75%.

- You pay rent (usually around 3%), plus monthly service charges on the remaining share to the housing association or owner.

- To finance your share, you must have a 5% to 10% deposit and a mortgage.

You can staircase your share of the home over time. This means you can buy more shares from your landlord until you own 100% of the property. As you increase your share, you’ll pay less rent.

Best for: First time buyers, and home buyers who can’t afford a full mortgage or buy a home outright.

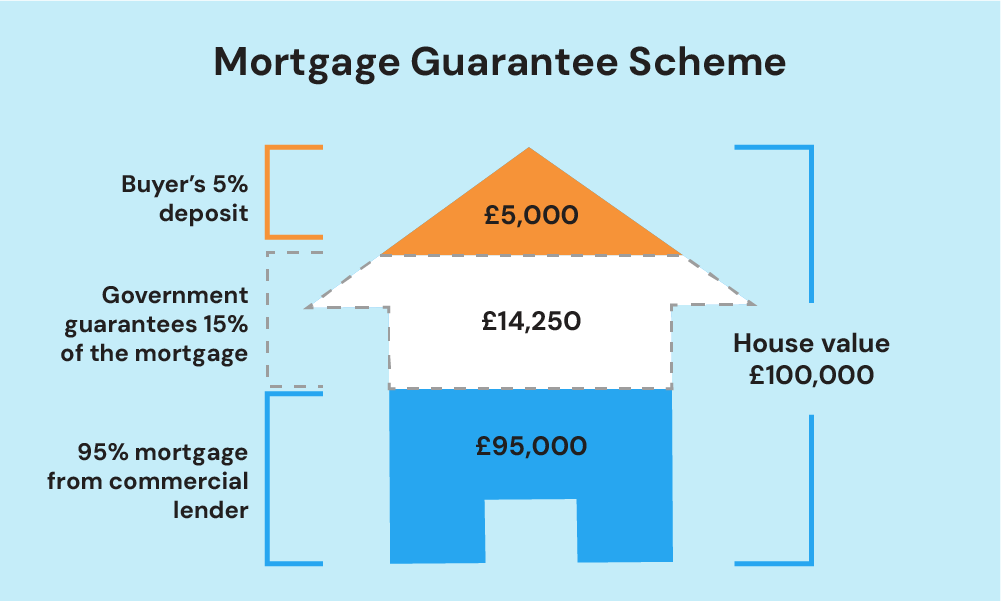

Mortgage Guarantee Scheme

This scheme makes it easier for you to buy a home with a small deposit. It’s open to all homebuyers who meet the criteria, and it’s been extended until the end of June 2025.

How Does it Work?

- This scheme is similar to a 95% mortgage, but the government will cover the lender’s losses if the borrower defaults.

- You need a 5% to 9% deposit. The lender will then give you a 95% loan-to-value mortgage.

- The government guarantees 15% of your mortgage loan, which, together with your 5% deposit, makes up 20%. This lowers the risk for lenders and easier for you to get a mortgage.

Under this scheme, your lenders also pays a commercial fee to the government for each mortgage. This might increase the cost of the loan through higher interest rates or product fees.

Best for: Home buyers who want to buy a property with a smaller deposit.

Right to Buy

This scheme lets you buy your home at a discount if you’re a council tenant for 3 years in England.

How does it work?

- You can get a discount on the market value of your home when you buy it. The discount amount varies depending on location, length of tenancy, property type, and home value.

- The maximum discount is £96,000 across England and £127,900 in London. This increases annually with the consumer price index (CPI).

- If you buy with someone else, you would count the years of the longest public sector tenant.

Best for: Eligible council tenants who no longer wants to pay rent on their homes.

Help to Buy: Equity Loan

This scheme is closed for new applications now.

How does it work?

The government allows you to borrow up to 20% (or 40% in London) of a new-build home’s price. You must have a 5% deposit and obtain a mortgage to cover the remaining 75%.

No interest will be charged on the equity loan for the first 5 years. Afterward, an interest rate of 1.75% will be applicable, increasing with inflation (CPI) plus 2% in April. When you sell your home, you must repay the entire equity loan.

Best for: First-time buyers who can afford the 5% deposit and monthly loan repayments.

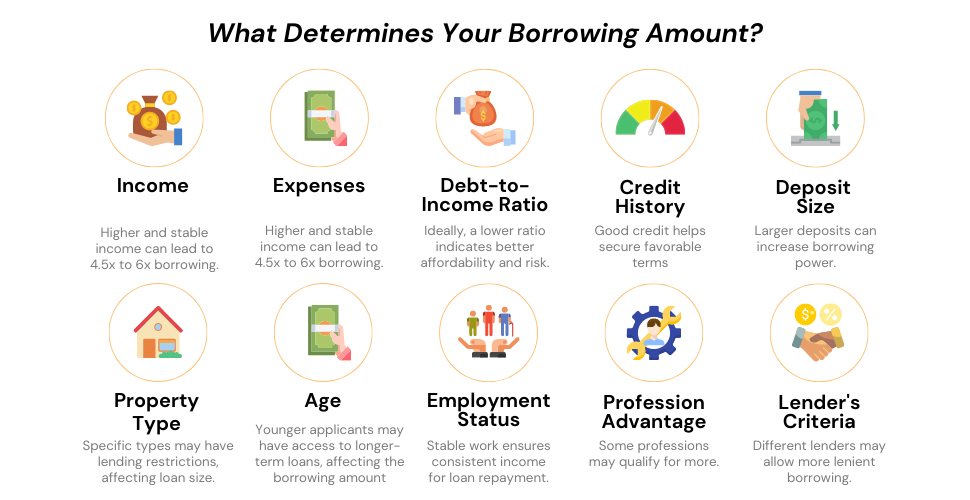

How Much Can Key Workers Borrow?

In the UK, lenders use income multiples to determine your mortgage borrowing capacity. They multiply your annual income by a specific number, usually between four and five times your salary.

For instance, the average salary of a key worker in the UK is around £31,461 per year.

- With an income multiple of 4, you can borrow £125,844 (£31,461 x 4).

- With an income multiple of 5, you can borrow £157,305 (£31,461 x 5).

Note that income multiples are just a guide. Lenders may adjust your borrowing amount based on your circumstances. They will take into account factors like your income, expenses, deposit size, and the type of mortgage you’re applying for.

Let’s say, you’re a key worker with a stable job or a good credit history. Lenders are more likely to lend you more money than an applicant with a less stable job or a poor credit history.

Ultimately, your borrowing amount will depend on your circumstances and your lender’s terms.

Documents You Need to Prepare

To speed up your mortgage application process and increase the chances of approval, ensure you have the following documents ready before you begin:

- Proof of identity – passport, driving licence, or birth certificate.

- Proof of address – recent utility bill, council tax bill, or bank statement.

- Proof of employment – a letter from your employer stating your job title, salary, and length of service.

- Proof of deposit – a bank statement showing the deposit money in your account.

- Credit report – You can get a free credit report from Experian, Equifax, or TransUnion.

- Proof of income – payslips, P60s, or bank statements.

Employed in a Permanent Contract

Key workers with permanent contracts should have no trouble obtaining a mortgage. Just like any other employed borrower, you will need to provide the following:

- 12 months of payslips to show your income

- A contract of employment to verify your job type.

- Your P60 to prove your annual income and any overtime or shift bonuses.

If you have less than 12 months of payslips or are new to your job, some lenders may hesitate to approve your application.

But, others may still consider your deposit size and other income when you apply. It’s advisable to see different lenders and consider your available options.

Short-Term Contract and Agency

Short-term and temporary workers can find it challenging to get a mortgage, but there are specialist lenders who understand these situations.

Ideally, to increase your chances of success, you should:

- Be able to have at least 12 months of payslips to prove your income is consistent. You must understand your income sources and communicate them effectively to your lender.

- Have a good credit history and a substantial deposit (at least 10%). You may need to put down a larger deposit if you have bad credit.

Self-Employed Key Workers

If you’re a self-employed key worker, lenders typically require the following to prove your income:

- 2-3 years of accounts approved by a qualified accountant

- SA302 tax returns which are official summaries of your annual income reported to the UK’s HM Revenue & Customs (HMRC).

Self-employed workers who are new to the job can still get a mortgage from specialist lenders if they have 12 months of accounts.

The Bottom Line

As a key worker, getting on the property ladder can seem daunting at first. But there are schemes that can make homeownership more affordable and accessible.

Each has its own eligibility criteria and benefits, so it’s important to do your research to find the one that’s right for you.

Going alone to find a suitable lender can be tough, especially if you have a unique situation. To make things easier, use a good mortgage broker.

With their expertise, they’ll guide you through the mortgage process, increase your chances of approval, and secure the best possible terms.

So if you’re ready to take the next step towards buying your dream home as a key worker, connect with us today.

We’ll match you with a top-notch broker who specialises in key workers mortgages and can help you find the right lender for your needs.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Can key workers with bad credit have mortgages?

Yes, it’s possible to get a mortgage with bad credit, but it can be challenging. There are specialist lenders who offer mortgages to people with poor credit histories. These mortgages often have higher interest rates and stricter terms, and you may need to put down a larger deposit.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Police Mortgages: A Definitive Guide in 2025

Police officers are never off duty. You put your lives on the line every day to keep us safe. But amidst your noble service, you face a unique challenge: securing a mortgage. As a police officer, time can be your enemy. The demands of your profession, the irregular shift patterns, and the sacrifices you make […]

NHS Mortgages: What You Need to Know Before Buying a Home

If you work for the NHS, you’re no stranger to hard work. You put in long hours, manage unpredictable shifts, and care for those who need it most. But when it comes to buying a home, the process can feel unnecessarily complicated. Your irregular hours, varied income, and short-term contracts might make it seem like […]

A Complete Guide: Mortgages for Professionals

If you’ve worked hard, got yourself qualified, and are ready to buy a house, you might be wondering if there are mortgages for professionals like you. The good news is – there are! Mortgage lenders offer professional mortgages with favourable and flexible terms. As a professional, you’ve shown that you’re responsible and have a predictable […]