- What is a Second Charge Mortgage?

- How Does a Second Charge Mortgage Work?

- Who Should Consider a Second Charge Mortgage?

- Moving House with a Second Charge Mortgage

- Benefits of a Second Charge Mortgage

- Risks and Considerations

- Should I Remortgage or Opt for a Second Charge Mortgage?

- How to Qualify for a Second Charge Mortgage?

- Who Are the Second Charge Mortgage Lenders?

- How Much Can You Borrow for Second Charge Mortgages?

- Second Charge Mortgages Fees

- Legal Aspects of Second Charge Mortgages

- Alternatives to Second Charge Mortgages

- The Bottom Line

Second Charge Mortgages: The Ultimate Guide

Have you got a mortgage but need to borrow more money? A second charge mortgage could be your answer.

It’s a way to get another loan using your home as security. This might be a good choice if remortgaging doesn’t suit you or if getting a personal loan is tricky.

But remember, going for a second mortgage does come with its own risks.

In this guide, we’ll cover the ins and outs of second-charge mortgages and help you figure out if it’s the right borrowing option for you.

What is a Second Charge Mortgage?

A second charge mortgage is a loan secured against your property, on top of your existing mortgage. It’s like adding another layer of borrowing, using your home as collateral.

Think of it like this:

- You already have a mortgage (your first charge) – you owe money on your house.

- Now, you take out an additional loan with its terms and rates (the second charge) – you borrow more money, still using your house as security.

The key difference is that the first mortgage gets paid first, even if you fall behind on the second one. But if you can’t handle both repayments, you risk losing your property.

So, a second-charge mortgage is a way to access extra cash, but it’s important to remember that it’s still borrowing.

In the next section, we’ll explore how this type of mortgage works and what makes it different from other borrowing options.

How Does a Second Charge Mortgage Work?

A second charge mortgage is another loan you take out against your home. Here’s what happens:

- Equity Check. They see how much of your home you actually own – your home’s value minus what you owe on your first mortgage.

- Applying. You apply just like you did for your first mortgage. The lender looks at whether you can afford to pay both mortgages.

- Different Rates and Terms. This new loan has its own interest rate and repayment plan, which might be different from your first mortgage.

- Separate from Your First Mortgage. It’s a different loan but still in the same house.

- Remember the Risk. If you can’t pay it back, there’s a risk you could lose your home. The first mortgage gets paid off first if things go wrong.

It’s a way to borrow more without changing your current mortgage. Just remember, it means juggling two separate repayments, so you need to be sure you can handle this financially.

Who Should Consider a Second Charge Mortgage?

A second-charge mortgage might be a good fit for you in certain situations:

- If Early Repayment Charges Are High. When your current mortgage has large early repayment charges, remortgaging could be costly. In such cases, a second-charge mortgage is a viable alternative.

- When Personal Loans Aren’t an Option. You might find personal loans hard to get, especially if you’re self-employed or your financial circumstances are complex.

- Poor Credit Rating or Changed Financial Circumstances. If your credit rating has dropped or your financial situation has changed since your first mortgage, you might not get a good rate if you remortgage. A second-charge mortgage, while possibly having a higher interest rate, can still be accessible.

- Debt Consolidation. It’s handy for pulling together all your debts, like credit card bills and personal loans, into one place. But remember, this means your home is on the line if you can’t keep up with payments.

Moving House with a Second Charge Mortgage

If you’re thinking about moving and you have a second-charge mortgage, there’s something important you need to know.

When you sell your house, you’ll need to pay off both your first and second mortgages completely. This means the money from the sale will first go towards clearing these debts.

So, if you’re planning to buy another house, the amount left for your next deposit might be less than you expected. It’s a crucial factor to consider, especially if you’re looking to move soon.

Benefits of a Second Charge Mortgage

There are some real advantages to a second-charge mortgage:

- You get to keep your current mortgage with its good terms, while still getting extra cash.

- No worries about early repayment fees on your first mortgage.

- Your first mortgage stays as it is, including how long you have to pay it off.

- Some second-charge mortgages let you pay extra when you can, helping you clear the debt quicker and possibly save on interest.

Risks and Considerations

But don’t forget, there are risks and things to watch out for:

- Your first mortgage lender might need to say ‘yes’ before you can get a second-charge mortgage.

- Second-charge mortgages usually have higher interest rates than your first mortgage.

- Juggling two mortgage payments every month can stretch your budget.

- The biggest risk is losing your home if you can’t keep up with the payments.

- If you decide to move, having two mortgages could mean you don’t have much left for a deposit on your next place.

- While it might seem easier on your pocket each month, in the long run, you might end up paying more.

Should I Remortgage or Opt for a Second Charge Mortgage?

Choosing between remortgaging and a second-charge mortgage depends on your situation.

If you’ve got a great deal on your current mortgage, like a low-interest rate, and you don’t want to lose it, a second-charge mortgage could be better. It lets you borrow more money using your home as security, without touching your first mortgage.

On the other hand, if you’re not tied to your current mortgage deal, remortgaging might be a good move.

It can give you a better interest rate or different terms, which could save you money in the long run.

But, remember, remortgaging could come with fees, especially if you’re leaving your current mortgage early.

So, think about what’s most important to you: keeping your current mortgage deal or potentially getting a better overall rate with a new mortgage.

And always check the numbers to see which option is more cost-effective for you in the long term.

How to Qualify for a Second Charge Mortgage?

To be eligible for a second charge mortgage, you’ll need to meet certain criteria:

- Enough equity in your property, which is the value of your home minus the amount you still owe on your first mortgage.

- A regular and stable income to ensure you can afford the additional loan repayments.

- A good credit history, although some lenders may consider you with a less-than-perfect credit score.

- You should be at least 18 or 21 years old, but some lenders might have a higher minimum age requirement.

And for the paperwork part, you’ll generally need to provide:

- Payslips or tax returns as evidence of your income.

- Recent bank statements to showcase your financial management.

- Valid identification such as a passport or driving licence.

- A recent utility bill or similar document for proof of address.

- Information about your current mortgage, including your outstanding balance and repayment history.

Remember, lenders have their specific requirements, so it’s important to check with them directly or consult with a mortgage advisor to ensure you have everything you need.

Who Are the Second Charge Mortgage Lenders?

If you’re considering a second charge mortgage in the UK, here’s a list of lenders you might come across:

- West One

- Pepper Money

- NatWest

- Halifax and Santander

- Secta Finance

- Freedom Finance

- Revolut

- Leeds Building Society

- Barclays

- Leek United Building Society

- Metro Bank

- Nationwide

Please note, this isn’t an exhaustive list. For more details, feel free to contact us. We’ll connect you with a top broker who can explore more options and find the best deals for you.

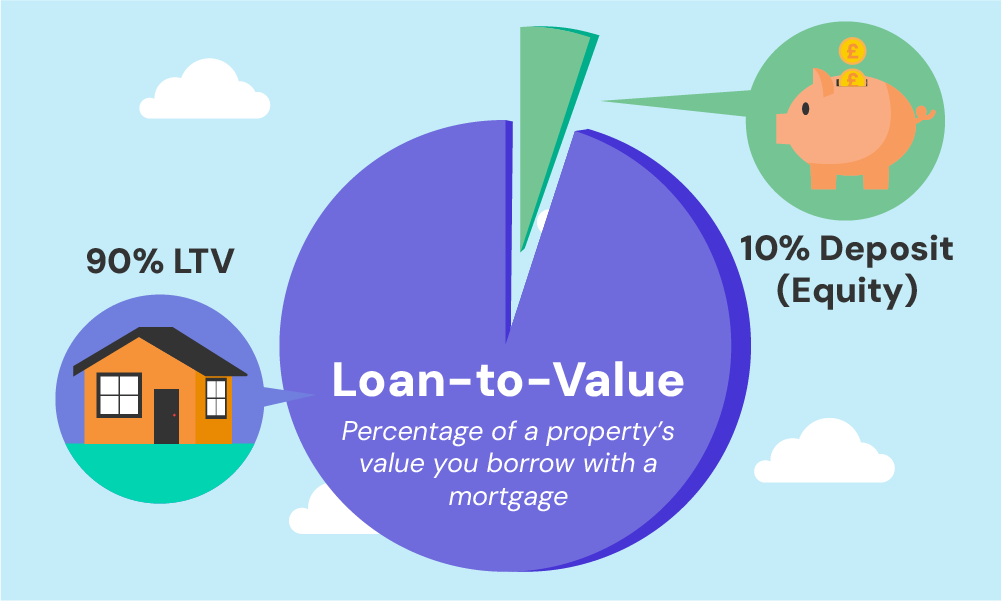

How Much Can You Borrow for Second Charge Mortgages?

Your borrowing amount depends on the equity of your home.

Equity is the value of your home minus what you still owe on your first mortgage.

Lenders have different limits, but they usually let you borrow up to a certain percentage of your home’s value, minus any existing mortgage. This is called the Loan to Value (LTV) ratio.

For instance, let’s say your home is worth £500,000 and you still owe £200,000 on your mortgage.

If a lender offers a 95% LTV, you could potentially borrow up to £275,000 as a second charge mortgage.

Here’s a table to show the calculations:

| Description | Amount (£) |

|---|---|

| Value of Home | 500,000 |

| Existing/Remaining Mortgage | 200,000 |

| Home Equity | 300,000 |

| LTV Percentage | 95% |

| Maximum Second Charge Mortgage | 275,000 |

But remember, this depends on the lender and their criteria.

The length of time you have to pay back a second charge mortgage, or the repayment term, can vary too. It’s typically between 3 to 30 years, based on what suits your financial situation.

Longer terms might mean lower monthly payments, but you’ll pay more in interest over time. Hence, it’s important to find the balance that works for you.

Second Charge Mortgages Fees

Getting a second-charge mortgage involves more than just the borrowed amount. There are several costs and fees to consider:

- Set-up or Arrangement Fees. These vary by lender and can be anything from £0 to £2,500.

- Legal Fees. Expect to pay around £500 to £1,000 for the legal work involved.

- Valuation Fees. Starting at about £150, these depend on your property’s size and value.

- Broker Fees. If you use a broker, they could charge about 1-2% of the loan amount.

Second-charge mortgages usually have higher interest rates than your first mortgage. So, it’s crucial to think about the total cost, including these fees and the interest rate.

To keep costs down, it’s smart to compare different lenders. Don’t just focus on the interest rates; consider all the fees involved.

Sometimes, a loan with a higher interest rate but lower overall fees might be cheaper.

Make sure to read all the details so you know exactly what you’re agreeing to.

Legal Aspects of Second Charge Mortgages

In the UK, second-charge mortgages are governed by a set of legal rules to ensure fairness.

These rules are enforced by the Financial Conduct Authority (FCA), just like with your primary mortgage. This means lenders must clearly outline the costs, risks, and terms of the loan to you.

As the borrower, you’re entitled to clear information about the loan, including the total cost. You also have the right to a fair process, especially if you find it hard to keep up with repayments.

However, your key responsibility is to repay the loan on time. Remember, your home is the security for the loan, so if you fail to make payments, you could risk losing it.

Alternatives to Second Charge Mortgages

If a second-charge mortgage doesn’t seem quite right for you, there are other options to consider. Here are some options:

- Remortgaging – Swapping your current mortgage for a new one, potentially with better rates or borrowing extra cash.

- Personal loans – Unsecured loans not tied to your property. Good for smaller amounts, but often have higher interest rates compared to mortgages. Think of them like credit cards but with a bigger limit.

- Saving up – The most patient and risk-free option. No borrowing is involved, but takes time and discipline.

The Bottom Line

In a nutshell, second-charge mortgages let you borrow more against your home.

They’re different from your main mortgage and come in handy when you need extra cash but want to avoid remortgaging. However, they have their costs and fees, and your home is at stake.

Before deciding, it’s crucial to think about what suits you best. Second-charge mortgages, remortgaging, and other options each have benefits and drawbacks.

If you’re unsure about the best choice for you, It’s a good idea to chat with a mortgage advisor. They can walk you through the options and help find the deal that’s right for you.

To find the right advisor without the hassle, simply get in touch. We’ll connect you with a perfect mortgage advisor who’ll simplify the process and get a deal that suits you.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do I have to tell my current mortgage provider about a new second-charge mortgage?

Yes, in most cases, you need to inform your existing mortgage lender when you take out a second charge mortgage. They have to agree to it since it affects your property, which is the security for your first mortgage.

Can I use a second-charge mortgage for my business?

Yes, you can use a second-charge mortgage to fund your business. However, lenders will want to see a solid business plan and be convinced that you can repay the loan.

Is it possible to get a mortgage for another property?

Yes, you can get a second-charge mortgage for a second property. If it’s for personal use, you’ll need a second home mortgage. If you’re planning to rent it out, a buy-to-let mortgage would be more appropriate.

How much time does it take to get a second-charge mortgage?

Getting a second-charge mortgage is generally quicker than a first mortgage. The whole process can take anywhere from a few days to a few weeks, depending on various factors like your lender and how quickly you submit required documents.

Are second-charge mortgages more costly?

Second-charge mortgages often have higher interest rates compared to first mortgages. This means they can be more expensive over time. It’s important to consider all the costs involved, including fees and interest rates, when deciding if a second-charge mortgage is right for you.

Related Articles

A Quick Guide to Find the Best Second Mortgage Rates

Second charge mortgages let you borrow money using the value of your home, on top of your first mortgage. The interest rates are usually higher because lenders take more risk—they get paid back after your first mortgage if you can’t keep up with payments. These loans are regulated to protect borrowers and are often used […]

How To Find the Right Second Charge Mortgage Lenders?

Life throws curveballs, and often, they come with a price tag. Home improvements, debt consolidation, or big life events – they all need funds. As a homeowner, you’ve got a powerful option at your disposal: second charge mortgages. These loans let you tap into your home’s equity without touching your first mortgage. The landscape for […]

Second Charge Mortgage Calculator – Get a Quick Quote

You’re looking to borrow more money using your home, and a second charge mortgage might just be what you need. In the UK, these mortgages let you borrow from a few thousand pounds up to larger amounts, depending on your home’s value and how much you still owe on your first mortgage. How much exactly? […]