- What are Mortgages for Directors?

- How Long Has Your Business Been Running?

- How Much Deposit is Needed for a Directorâs Mortgage?

- What Are The Documents Needed to Prove My Income?

- How Much Can a Company Director Borrow for a Mortgage?

- Getting a Mortgages as a Limited Company Director

- Is Retained Profit Considered for a Mortgage in a Limited Company

- Can I Get Mortgages for Directors with Bad Credit?

- Mortgages with Recent Company Losses

- Mortgages with Recent Company Changes

- Is Remortgaging an Option for Company Directors?

- Key Takeaways

- The Bottom Line: For Your Next Stepsâ¦

Mortgages For Directors: A Guide For The Self-Employed

On paper, getting a mortgage as a company director should be easy—you run a business, you earn money, and you’re responsible with your finances.

But lenders don’t always see it that way.

If you’re self-employed, banks often consider you a riskier borrower.

And if you’re like many directors who legally reduce their earnings to save on taxes, that can make it even harder to prove you can afford a mortgage.

This isn’t about how successful your business is; it’s about how lenders measure risk. Their rules vary.

Some want three years of trading history, others ignore retained profits altogether. The system isn’t designed with directors in mind.

That’s where this guide can help. You’ll learn how to present your financial situation in the best light, understand what lenders are really looking for, and get practical steps to improve your chances of securing a mortgage.

What are Mortgages for Directors?

Mortgages for company directors operate in the same manner as standard mortgages. The goal is to prove to the lender that you can manage the repayments.

But, as a company director, you might face challenges. Some traditional lenders might view your position as more risky. They might not fully grasp the nature of your income or have concerns about the financial stability of your company.

This perspective can lead to rejection, even when you feel confident about your ability to handle the mortgage.

Fortunately, specialist lenders are available. They understand the unique financial structures of company directors. These lenders employ a flexible and practical approach.

They will assess your situation, considering all aspects of your income and the nature of your business.

So, if you are a company director in need of a mortgage, remember: rejection from a traditional lender is not the end of the road.

With persistence and guidance from the right experts, you can find a lender willing to accommodate your specific needs.

How Long Has Your Business Been Running?

Your trading history isn’t just a record of your business journey; it’s a pivotal factor that lenders scrutinize when assessing mortgages for company directors.

Let’s delve into how this aspect influences your mortgage prospects.

Under 1 Year

If you’ve been trading for fewer than 12 months, locating a mortgage provider might be tough. Yet, with proper documentation of future work contracts, you may find a suitable mortgage.

Between 1-2 Years of Trading

Your tax records might span two different years. While some lenders could hesitate, holding off until your accounts for the next year are filed, there are those willing to work with you right away. Selecting the right lender becomes crucial in this stage of your business.

Over 2 Years

Trading for two years or more puts you in a favourable position with most lenders. Especially if other aspects, such as your credit file and loan-to-value, of your application are in order.

If you’ve reached the three-year mark, your options broaden significantly, enabling you to access virtually all lenders.

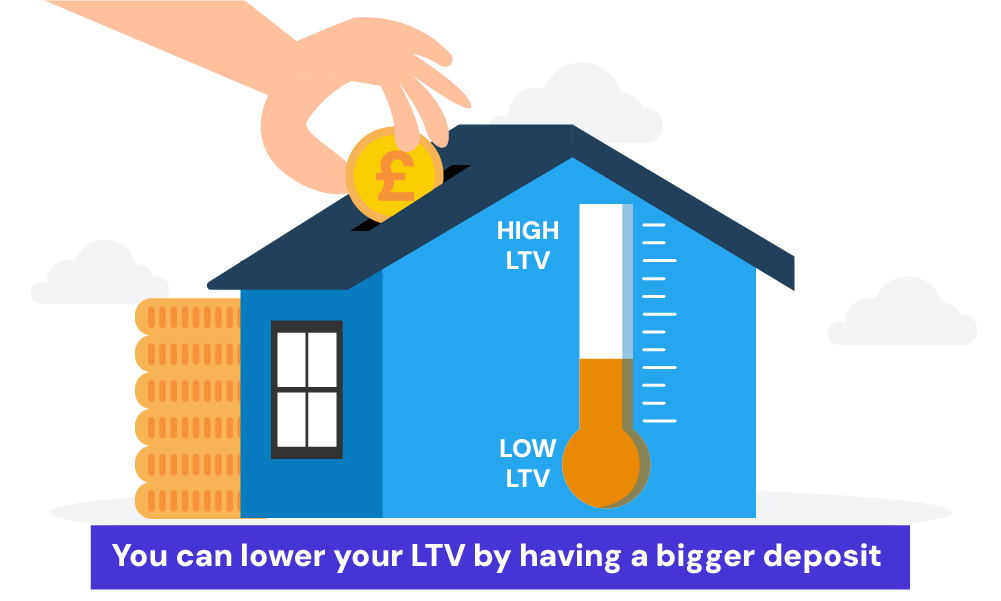

How Much Deposit is Needed for a Director’s Mortgage?

The situation with mortgages for directors can sometimes be more complex. But, in general, you have access to the same deals as everyone else.

If you’ve been trading for over 2 years and have good credit, you might only need a 5% deposit for a residential purchase. This is subject to your requested loan amount meeting the necessary affordability checks.

If you can manage to save a higher deposit, your Loan-to-Value ratio (LTV) will be lower. This puts your application in a strong position. You can potentially qualify for some attractive rates and have access to more lenders.

A 15% deposit could land you a good deal, but if you’re able to put down as much as 40%, you will find yourself with the best available mortgage rates.

On the flip side, if your credit isn’t as strong or your trading history is lacking, expect to need at least a 15-20% deposit.

Remember, these are general guidelines, and each situation is unique. If you need advice tailored to your specific circumstances, specialist advisors are available to guide you through the process.

What Are The Documents Needed to Prove My Income?

If you’re a self-employed director, it’s necessary to provide evidence of your income when applying for a mortgage.

The required documents might differ from lender to lender, but here’s a general list you’ll likely encounter:

- SA302 forms – These can be requested or downloaded online from HMRC.

- Finalised accounts – This could be in the form of a spreadsheet or details from a qualified accountant.

- Latest 3 months’ bank statements – Both personal and business accounts may be needed.

Some lenders might ask for all the items listed above, while others might only require a portion. One crucial document, the SA302 form, will likely be requested by every lender.

You can download it from the HMRC portal or request it via post, but postal requests may take up to 14 days.

How Much Can a Company Director Borrow for a Mortgage?

Determining how much a company director can borrow for a mortgage involves looking at both income and expenses.

Since the Mortgage Market Review, the process has become more detailed. It’s not only about how much you earn but also about your regular spending.

This complete picture allows lenders to make a well-informed decision about what they can afford.

The balance between your income and spending not only shows whether you can manage monthly mortgage repayments. It sets the initial limit for what you can borrow.

By taking both aspects into account, lenders ensure that the mortgage suits your financial situation.

You can use our self-employed mortgage calculator to get an estimate of how much you might be able to borrow.

Getting a Mortgages as a Limited Company Director

If you’re a director of a limited company, lenders will assess your income based on the salary, dividends, or share of net profit you take from the business.

Many directors opt to draw a base salary up to the tax-free threshold and then take additional income as dividends, retaining the rest of the profit within the company.

Although this strategy can save on taxes and help grow the business, it might complicate the mortgage application.

For example, if you only withdrew £25k from a company profit of £100k, high street lenders will only consider the £25k figure for your mortgage assessment. This can create challenges with mainstream lenders.

But, this problem isn’t insurmountable.

By working with a mortgage advisor who has access to a market of specialist lenders, you can find a mortgage that goes beyond considering just your withdrawn income. This approach can increase your borrowing potential across the market.

If you’re interested, we can connect you with these advisors to explore your options further.

Is Retained Profit Considered for a Mortgage in a Limited Company

Mainstream lenders often ignore retained company profit, but specialist lenders will take it into account. This can significantly increase the mortgage amount you can obtain.

If your company has profits of £100k, specialist lenders may approve you for a mortgage of £500k, rather than the £100k based on a net profit of £20k.

If you need a larger mortgage than your net profit allows, or if other lenders have declined your application, specialist advice can make a difference.

Can I Get Mortgages for Directors with Bad Credit?

Getting a mortgage as a director with bad credit can be challenging, but it’s not impossible. The availability of lenders will shrink, and credit issues will be assessed based on their recency and severity.

But, not all lenders view bad credit in the same way. Some specialist lenders might be willing to consider your application, taking into account the entire financial picture, such as the profitability of your company and your overall financial responsibility.

It’s also worth considering that improving your credit score, even by a small margin, can open up more options for you.

Regularly checking your credit report, paying bills on time, and reducing existing debts are a few ways you can take control of your credit situation.

Remember, each lender has a different approach, and the support of a knowledgeable advisor can make all the difference in finding the right mortgage for you.

If this sounds like something you need, we work with mortgage advisors who specialise in this area, and we can connect you with them to discuss your options.

Mortgages with Recent Company Losses

Securing a mortgage after your company has filed a loss in the last three years can be a tricky affair. Most high-street lenders might see you as a high-risk applicant and decline your application.

Why does this happen? A recent company loss creates doubt in lenders’ minds about the ability to repay the mortgage, particularly if your business seems to be in distress.

But don’t worry; there’s still hope. If your company experienced a loss two or three years ago but has since turned a profit, some specialist lenders may consider your case.

It’s even more beneficial if you have an expert broker. They can guide your application to the right lender and liaise with underwriters if any concerns arise.

What’s more, if the loss is linked to drawing a salary from the company, lenders might overlook it, acknowledging that you’ve maintained an income.

This situation might require an experienced broker’s insight to explain to the underwriter and possibly additional documents. But with the right guidance, securing a mortgage after a company loss is indeed achievable.

Mortgages with Recent Company Changes

Changing your trading type or having inconsistent profits in recent years might seem like obstacles in securing a mortgage, but they don’t have to be.

Switching from a sole trader to a limited company doesn’t have to be a hindrance if done three or more years ago.

But, changes made within the last three years could limit your options. Lenders will likely focus on your current company and its related accounts, requiring typically three years of accounts.

A specialist lender may be needed in this situation, who would consider accounts under your previous trading style.

Is Remortgaging an Option for Company Directors?

If you’re a company director considering remortgaging, there are different paths you can take, depending on your goals.

For personal uses such as home improvements or buying a property to let out, many high street lenders are supportive. These options are generally accessible and could be a great solution if they fit your needs.

However, if you’re looking to invest in your business, the process may become more complicated. Mainstream lenders often see this as a higher risk and may be hesitant to offer a remortgage for this purpose.

But don’t worry, there are specialist lenders who may be willing to help. They understand the unique needs of company directors and might be open to offering a remortgage for business investment.

Key Takeaways

- Directors can get mortgages, but income assessment is trickier. Lenders often view company directors as higher risk, making it harder to prove stable income.

- Specialist lenders offer better options. They understand business finances and consider factors like retained profits, not just salary and dividends.

- A solid trading history boosts your chances. Two years or more in business opens up more lender options and improves approval odds.

- A bigger deposit unlocks better rates. Saving 15–40% can lower your loan-to-value ratio and secure more attractive mortgage deals.

- Bad credit or past losses aren’t deal-breakers. Specialist lenders look at your full financial picture, offering solutions where traditional banks may not.

The Bottom Line: For Your Next Steps…

When it comes to mortgages for self-employed directors, you’ve come to the right place. Even if mainstream lenders or brokers have declined you, we have the expertise to help.

Each case is unique, so don’t hesitate to reach out to a mortgage advisor. They can provide you with the best route to secure the right mortgage, often turning disappointments into approvals within days.

They understand the intricacies involved, making the process smoother and more manageable for you.

Considering taking this step? Contact us today. We’ll pair you with a knowledgeable broker who can provide the guidance you need. Complete our inquiry form for a free, no-obligation consultation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it possible for a director whose company has been liquidated to secure a mortgage?

Generally, your personal and business finances are distinct, so liquidation shouldn’t affect your credit file. However, there may be exceptions, such as if you have provided a personal guarantee for business funding. Consulting a broker before applying for a mortgage would be a wise move if your company has been liquidated.

Can a director obtain a buy-to-let mortgage?

Absolutely. If you meet the required eligibility and can demonstrate affordability, obtaining a buy-to-let mortgage should be feasible. Specialist lenders often provide the best deals. For a comprehensive overview, please refer to our guide on buy-to-let mortgages tailored for self-employed individuals.

Can a company purchase a residence on behalf of a director?

Yes, this is doable, though it introduces an additional level of complexity. If you are contemplating this option, engaging a specialist broker at the outset is crucial to understanding the intricacies involved.

How are mortgages assessed for sole traders?

For sole traders, the mortgage assessment will be based on net profit. Since many sole traders legally minimise their net profit on tax returns to reduce tax bills, lenders consider the net profit rather than turnover. The average net profits from the last 2-3 years are typically used, if available.

What's the approach for partnerships when it comes to mortgage assessments?

If you’re in a partnership, your share of the net profit will form the basis for your mortgage assessment. In an LLP (Limited Liability Partnership), the income assessment will relate to the LLP’s income if the business itself is applying for a mortgage.

Please note that circumstances might necessitate consulting a mortgage professional to understand your specific borrowing capacity as a director.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache. Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself. But there’s good news: With the right support, YOU can switch your mortgage without a hitch. In this article, we’re going to […]

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]