- What Counts As A High Deposit for a Mortgage?

- How Large Deposits Get You a Better Mortgage Deal

- What Are The Advantages Of a Large Mortgage Deposit?

- Can I Get a Mortgage with a High Deposit but Low Income?

- How Much Mortgage Costs Do I Save With A Larger Deposit?

- How Much Can I Borrow With a 25% or More Deposit?

- What If I Have a Bad Credit and a Higher Deposit?

- Can I Get a Mortgage No Job But With a High Deposit?

- Key Takeaways

- The Bottom Line

Why High Deposits Mean Better Mortgages: A Must-Read Guide

If you’re one of the fortunate homebuyers who can put down a higher deposit, then you’re in a great spot. With a larger deposit, you can unlock better mortgage rates and more borrowing options.

This guide will walk you through what counts as a high deposit and how it could be a game-changer for you.

What Counts As A High Deposit for a Mortgage?

When we talk about a ‘high’ deposit, we usually mean anything above 25%.

For many, a 10% deposit is more common, but if you can stretch to 25%, 50%, or even more, you’re in a stronger position.

A larger deposit does more than just unlock better rates. It can also make it easier for you to get approved for a mortgage.

With a bigger deposit, lenders see you as less of a risk, which can mean better terms for your loan. So, if you’re able to save more before you buy, it can really pay off.

How Large Deposits Get You a Better Mortgage Deal

The bigger the deposit, the smaller the debt.

This makes you an attractive borrower to many mortgage lenders. Hence, this opens up more chances to get their approval and better interest rates.

Let’s break down how your deposit influences your mortgage approval chances.

For a 25% Deposit

It’s quite common among buyers to put down a 25% deposit, especially for home improvements in their first home. And if you’re in this position, then you’re doing well.

More lenders will accept your application because it reduces their risk. With this deposit, you can expect better interest rates and more loan options.

Some first-time buyers can achieve this level of deposit through gifted funds or inheritance. This boosts their borrowing power and mortgage options.

For a 50% Deposit or More

If you can put down 50% or more, you’re in an excellent position. Perhaps you’re downsizing or selling a family home, it shouldn’t be hard to get a mortgage lender’s approval.

They view you as very low risk, which might secure you even better mortgage terms. This strong position makes the mortgage process smoother and straightforward.

Before you apply, always consider getting the right financial advice to make sure it’s the best use of your money.

While a big deposit is great, lenders look at other things too. This includes:

- Your credit score to see how you handle money.

- Your income and debts to make sure you can afford the monthly payments.

- Your age to ensure you can reasonably expect to repay the loan.

- Your employment history to check if you have consistent income.

- The condition and type of the property you’re buying.

- Your savings or bank accounts to make sure you can handle unexpected costs.

All these things together help them decide if they can give you a loan.

In short, a large deposit can boost your chances of getting a mortgage, but it’s just part of the picture. You need to keep your finances in good shape all around to get the best mortgage deal.

What Are The Advantages Of a Large Mortgage Deposit?

Having a large deposit when you apply for a mortgage has many advantages. Here’s why you should put down more:

- You unlock better mortgage products not available to those with smaller deposits.

- Your monthly repayments are lower because the loan amount is reduced.

- You might save a significant amount on interest payments over time.

- You’re in a stronger position to negotiate favourable terms on your mortgage.

- You own more equity in your home, enhancing financial security.

- You’ll find more lenders willing to offer you mortgages with cheaper rates and better terms.

Can I Get a Mortgage with a High Deposit but Low Income?

Yes, you can get a mortgage even if your income isn’t very high but you have a large deposit.

A large deposit can help balance out your low income when lenders decide if they can give you a mortgage. As we’ve talked about, a larger deposit means a lighter loan burden –and lesser risk for the lender.

Some specialist lenders might offer you mortgage products specifically designed for situations like yours. These products often have more flexible criteria for income.

But, remember, even with a high deposit, lenders will assess your debt-to-income ratio (DTI). You need to provide proof that your income can comfortably pay the mortgage repayments on top of your monthly expenses.

Ideally, aim for a DTI at least 36% to 46%. A lower DTI increases your chances of getting a mortgage approval.

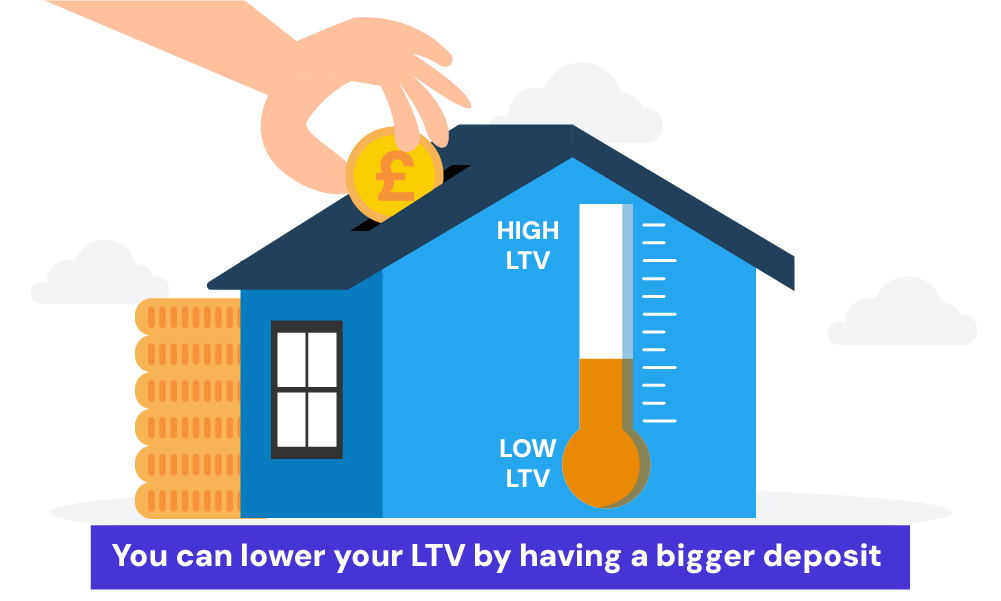

How Much Mortgage Costs Do I Save With A Larger Deposit?

Increasing the amount of your deposit decreases your loan-to-value (LTV).

LTV shows how much you’re borrowing for a property compared to its value.

For instance, if you borrow £300,000 for a house worth £400,000, your LTV is 75%—meaning you’ve covered 25% of the home’s price upfront, owning 25% equity outright.

This puts you in a strong position as it reduces the amount you need to borrow.

To make things clear, here’s a comparison of a 25% deposit versus a 10% deposit and their financial impact:

| Deposit Percentage | Deposit Amount | Loan Amount | Monthly Repayment | Total Interest Paid |

|---|---|---|---|---|

| 10% | £40,000 | £360,000 | £1,706 | £151,800 |

| 25% | £100,000 | £300,000 | £1,423 | £126,900 |

By increasing your deposit from 10% to 25%, you decrease your monthly repayments by about £283 and save about £24,900 in total interest. This significant saving shows how beneficial a larger deposit can be.

You can also choose shorter loan terms to reduce your total interest rates. But this option will increase your monthly mortgage repayments.

Buying a house is the biggest commitment you’ll ever make, so getting the right financing is key.

We highly recommend consulting a mortgage advisor to make a sound financial decision for your mortgage.

How Much Can I Borrow With a 25% or More Deposit?

A 25% deposit gives you more borrowing options. However, the amount you can borrow depends on your income, existing debts, and the lender’s criteria.

Lenders use income multipliers (typically 4-5 times your annual income) to estimate how much they’ll lend.

For example, with a £50,000 annual income, you might borrow £200,000-£250,000. A 25% deposit can make lenders more flexible with these multipliers, especially if it reduces their risk.

They will also consider your overall financial situation to ensure you can afford repayments.

Different mortgage products and lenders have varying criteria. Some might offer larger loans with bigger deposits, particularly niche or private lenders who don’t strictly follow traditional income multipliers.

To get an estimated amount of how much you can borrow, use the mortgage affordability calculator.

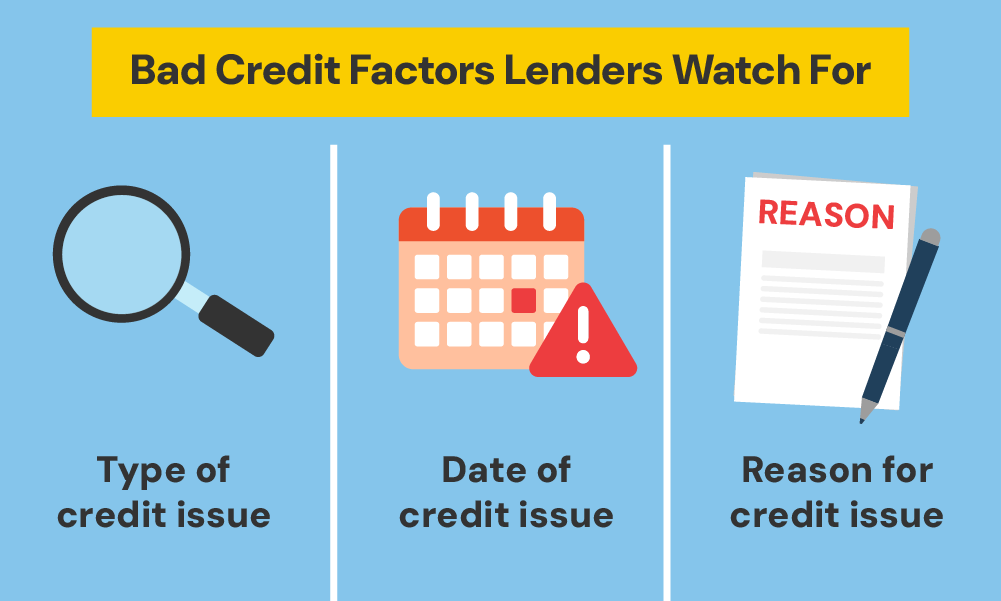

What If I Have a Bad Credit and a Higher Deposit?

If you have bad credit and want to apply for a mortgage, the lender will look at the details of your credit problem.

This includes things like how much the issue was for, what type it was, how serious it was, and how long ago it happened.

Having a bigger deposit can make things easier because it means less risk for the lender. This could make your application stronger and might give you access to more mortgage deals that people with smaller deposits can’t get.

Some lenders have special deals for people who have bad credit but can put down a big deposit. These deals might offer better terms, like lower interest rates, compared to regular bad credit mortgages.

But remember, getting approved isn’t always guaranteed—it still depends on your overall situation and the lender’s rules. It’s always a good idea to check with a mortgage advisor to see what your options are.

Can I Get a Mortgage No Job But With a High Deposit?

Yes, you might be able get a mortgage even if you don’t have a regular job but do have a big deposit.

Lenders assess your overall finances, not just your salary. A hefty deposit proves strong savings, offsetting the lack of regular income.

However, you might need to show alternative income sources. This could include investments, rental income, pensions, or even some benefits. These sources need to be reliable and sufficient to cover your monthly mortgage repayments.

Key Takeaways

- If you can put down more than 25% as a deposit, it’s considered ‘high,’ which makes it easier to get a better mortgage deal.

- Bigger deposits mean you don’t have to borrow as much money, which means lower monthly payments and less interest to pay over time.

- Putting down a 25% deposit usually means you get better interest rates and more choices for your loan.

- If you can put down 50% or more, getting approved for a mortgage is much easier because lenders see you as less risky.

- A big deposit can make up for having a lower income, but lenders still need to check that you can afford the monthly repayments.

- If you have bad credit but a big deposit, you might still get a better deal because the lender feels less at risk.

- Even if you don’t have a regular job, a big deposit can help you get a mortgage, as long as you can show you have other reliable ways to pay.

The Bottom Line

Having a large deposit makes you an attractive homebuyer. While getting a mortgage is highly likely, finding the right one can be tricky.

This is because comparing lenders alone is difficult and time-consuming. Moreover, understanding complex mortgage terms can be confusing.

With a mortgage broker, you can get help to simplify this process. They’re experts who can find deals not available online or from high-street lenders. They can also assess your finances and recommend the best mortgage option for your situation.

Using a broker saves you time, stress, and potentially money in the long run.

Need a broker? Get in touch with us. We can connect you with a skilled mortgage broker who can search the entire market and find a mortgage that fits your financial situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is there a limit to how much deposit I can give?

There’s no upper limit to the amount you can put down. You could even pay the entire price and become a cash buyer.

However, keep in mind that having a very large deposit while only needing a small loan might deter some lenders, as it may not be profitable for them. Most lenders have a minimum loan value, typically between £25,000 and £50,000.

Related Articles

How To Save For A Mortgage Deposit?

Saving for a deposit on your first home can be tough, but a clear plan will help you reach your goal. Your first step? Figure out how much you need to save. 💷 In the UK, a typical mortgage deposit is at least 5% of the house price. With average UK house prices sitting at […]

What Is Proof Of Deposit For A Mortgage?

When you’re buying a house, one of the first things you need is a deposit. This is a chunk of money you pay upfront. 💷 Most mortgage lenders ask for at least 5% to 20% of the property’s value. However, it’s not enough to simply have the deposit amount ready. You must also show where […]

Can I Really Get a Mortgage With No Deposit in the UK?

While saving a deposit is the traditional path to home ownership, the dream of buying a house with no money down is very tempting. With soaring property prices, can you really get a 100% mortgage and avoid years of gruelling savings? 🤔 What Is a No Deposit or 100% Mortgage? A no deposit or 100% […]