- Is a Mortgage Accessible for Sole Traders?

- How Long Do You Need to Be a Sole Trader to Apply for a Mortgage?

- What Documents Do You Need for a Sole Trader Mortgage?

- How Are Sole Trader Mortgages Assessed by Lenders?

- Can Sole Traders Obtain Commercial Mortgages?

- Can Sole Traders with Bad Credit Get a Mortgage?

- What Are the Mortgage Rates for Sole Traders?

- Key Takeaways

- The Bottom Line: For Your Next Stepsâ¦

Mortgages for Sole Traders Explained

Are you a sole trader in the UK searching for the right mortgage?

The process may feel both exciting and overwhelming. With countless lenders catering to various needs, including those with bad credit or unique self-employed situations.

It’s common to feel a bit lost.

Your position as a sole trader is special. It’s not the same as a director or a limited company, so picking the wrong lender could lead to unnecessary difficulties.

But here’s some good news: This article is here to help.

We will break down the essential factors that you need to consider when searching for a sole trader mortgage. We’ll also provide clear and concise guidance on how to select the best lender for your needs.

Is a Mortgage Accessible for Sole Traders?

Yes, you can.

Many lenders offer mortgages to sole traders and partnerships. Some lenders even allow you to borrow based on your gross income or remittance slips, and you can get a mortgage with just 6 months of trading history.

If you’re a sole trader or in a business partnership, it’s a good idea to find a lender who specialises in these types of cases. This will help you get the best possible deal on your mortgage.

Seeking out a mortgage broker who possesses the right knowledge and expertise about sole traders can be immensely beneficial.

They know which lenders can offer you custom mortgages with the most favourable rates, taking the complexity out of what might seem like a daunting task.

How Long Do You Need to Be a Sole Trader to Apply for a Mortgage?

If you want a mortgage as a sole trader, you usually need at least one (1) year of trading history. Lenders look at this history to see if you can afford the mortgage, based on the income you’ve declared.

In general, lenders usually assess for at least 3 years of accounts. The longer your trading history, the better your chances.

For contractors, especially those in the construction industry, the rules can be more flexible. Under the government’s Construction Industry Scheme (CIS), it’s possible to obtain a mortgage with just six (6) months of trading history.

What’s more, lenders under this scheme calculate affordability based on gross income, not net profit. This can significantly enhance your borrowing power.

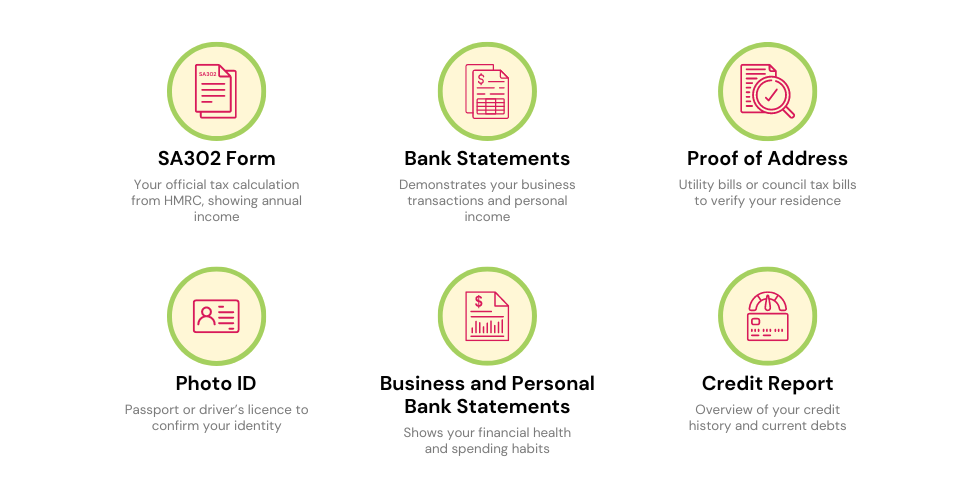

What Documents Do You Need for a Sole Trader Mortgage?

To get a mortgage as a sole trader, you’ll need to show your latest tax returns.

This is usually an SA302 form. If you’ve filed your income with HMRC through self-assessment, this should work for most lenders.

Lenders use the SA302 to see if you can afford the mortgage. You can get this document online from HMRC or by post.

While lenders usually assess affordability based on the net profit declared, if you’ve declared less to lower your annual tax bills, some lenders may consider gross income or total income received.

Beyond this, standard documents required for any mortgage include proof of address (like utility bills or council tax bills), photo ID, and bank statements.

Your proof of address and ID generally won’t impact your mortgage application. But your bank statements can, especially if your outgoings are high compared to your income.

Lenders may also scrutinise your credit card debts and any outstanding loans. So make sure you have a clear understanding of your financial position when applying.

How Are Sole Trader Mortgages Assessed by Lenders?

Lenders evaluate sole trader mortgages based on several criteria:

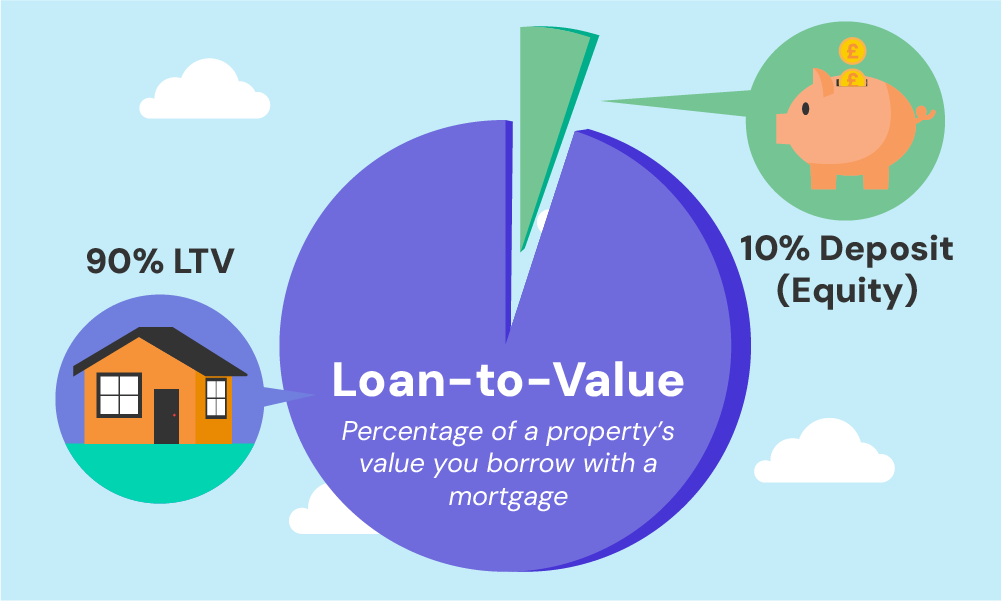

Loan to Value (LTV)

Loan-to-value (LTV) is a measure of the risk a lender takes when lending you money to buy a home. It is calculated by dividing the amount of the loan by the appraised value of the home.

A higher deposit generally appears favourable to lenders because it means you are taking on more of the risk yourself. This can lead to better terms on your mortgage.

The amount of the deposit you need to make will vary depending on the lender and the LTV of the loan.

For example, a lender may require a 20% down payment for a loan with an LTV of 80%. But, some lenders offer loans with lower down payments, such as 5% or 10%.

If you are self-employed or have a low credit score, you may need to make a larger down payment to qualify for a mortgage. This is because lenders view these borrowers as being more risky.

No matter what your financial situation, it is important to talk to a lender to find out what LTV you qualify for and what terms you can expect.

You can check you LTV using our loan-to-value ratio calculator.

Trading History

Lenders often ask for at least 12 months of trading history, sometimes up to 3 years. This helps them gauge the sustainability of your self-employment and their confidence in lending.

A longer trading history often translates into more confidence from the lender, as it demonstrates a stable income stream.

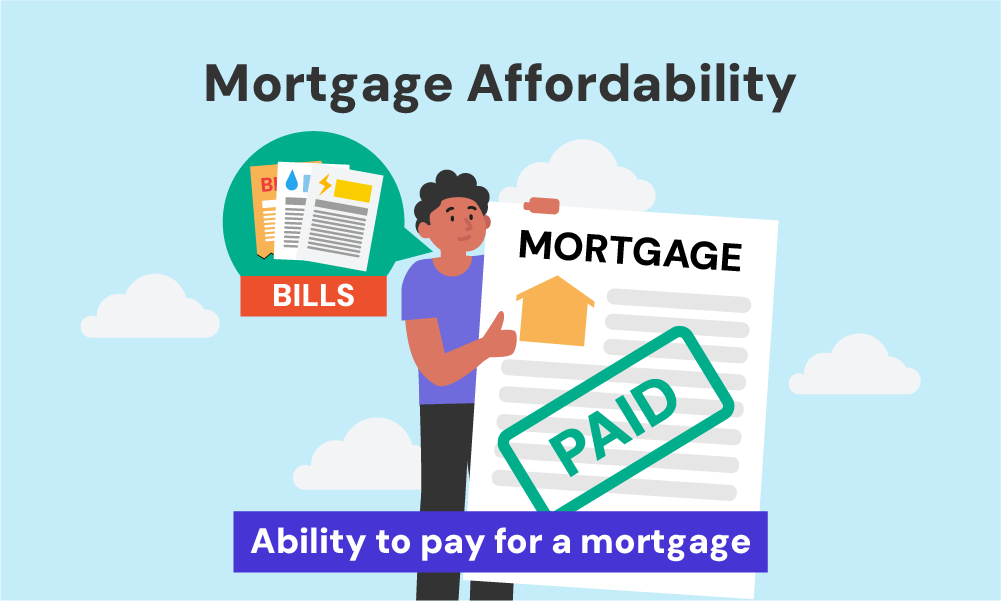

Affordability/Income

Lenders must ensure you can repay the mortgage. The income for sole traders is often calculated from an SA302 form. Different lenders also use various methods to average your income over 2 or 3 years.

This takes into consideration fluctuations in income that are typical in self-employment, aiming to arrive at a fair assessment.

To check how much you might be able to borrow, use our self-employed calculator.

Credit History

Your credit score and credit history can play a significant role in the decision-making process. Lenders may look at how you’ve managed debts in the past to evaluate your reliability in repaying the mortgage.

Type of Lender

Since lenders differ in their assessment methods, they might offer various deals. Some may lend up to 5x your income, while others may go less or more, depending on factors like your deposit amount and their security.

Special Considerations for Sole Traders

Lenders may also consider the nature of your business, the industry you’re in, and the market conditions. Some industries might be seen as riskier, impacting the lender’s decision.

Pro-Tip

If you’re a sole trader looking for a mortgage, working with a specialist in self-employed lending can make a difference. Organise your financial records and find guidance tailored to your unique needs.

Ready to take the next step? Simply fill out this quick form, and we’ll do the legwork to connect you with a self-employed advisor.

Can Sole Traders Obtain Commercial Mortgages?

Yes, securing a commercial mortgage as a sole trader is possible and doesn’t need to be difficult.

A commercial mortgage can assist you in purchasing a commercial property or funding your business venture.

If you are a sole trader in need of a personal mortgage, keep in mind that this is distinct from a commercial mortgage, and this article pertains specifically to personal mortgages.

Can Sole Traders with Bad Credit Get a Mortgage?

Yes, having poor credit does not necessarily bar you from getting a mortgage as a sole trader. Specialised lenders offer adverse credit mortgages, and your status as a sole trader may not put you at any disadvantage.

You might even qualify for the same rates as traditionally employed applicants. With just 12 months of trading history, lenders may still consider your application.

If this sounds like your situation, enquire. A self-employed lending specialist will get in touch to explore your financial position and mortgage requirements.

What Are the Mortgage Rates for Sole Traders?

Being a sole trader doesn’t usually impact the mortgage rates you receive. Qualifying sole traders can expect the same rates as others, regardless of employment status.

However, there are cases where specialist self-employed lenders might be needed, such as when dealing with low-income, minimal account history, or bad credit.

In such instances, the rates might be higher than average. These specialist lenders cater to unique applications, ensuring that even those with complex circumstances can find a suitable mortgage solution.

Key Takeaways

- Sole traders can qualify for mortgages, even with as little as six months of trading history, though specialist lenders often offer better deals and flexibility.

- A longer trading history, ideally two to three years, improves your chances of approval and may help secure better rates from lenders.

- Required documents typically include your SA302 tax form, proof of income, ID, bank statements, and evidence of address to assess affordability and financial stability.

- Lenders evaluate factors like your loan-to-value ratio, trading history, income consistency, and credit score when assessing your mortgage application.

- Even with bad credit or minimal trading history, specialist lenders may still offer mortgage options tailored to your financial situation.

The Bottom Line: For Your Next Steps…

When exploring mortgages specifically designed for sole traders, you’re in the right spot. Even if conventional lenders or brokers have turned you away, our expertise is here to guide you.

Every situation is different, so it’s worth connecting with a mortgage advisor tailored to sole traders.

They can help you find the best mortgage for your needs and get it approved quickly. They know the ins and outs of the mortgage process and can help you avoid any problems.

With a clear understanding of the unique challenges and solutions for sole traders, they make the entire process simpler and more accessible for you.

Thinking about moving forward? Get in touch with us today. We’ll match you with an expert broker who knows the ins and outs of mortgages for sole traders.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How does being a sole trader or in a partnership affect my mortgage rates?

Being a sole trader or in a partnership typically doesn’t affect the mortgage rates themselves. Lenders assess self-employed applicants based on the same key criteria as employed individuals, such as credit history, LTV, and affordability.

If you meet the lender’s criteria, you should have access to the same mortgage rates. However, specialist lenders catering to complex cases or adverse credit may offer different rates, so professional advice is recommended to find the best fit for your situation.

What are the available options if a sole trader or partnership has fluctuating income?

Sole traders or partnerships with fluctuating income can explore lenders who specialise in self-employed mortgages.

These lenders might consider a broader range of income evidence, such as:

- averaging income over 2 or 3 years,

- using the latest year’s figures, or even considering retained profits.

A mortgage broker with expertise in self-employed lending can guide you to the best option tailored to your unique situation.

What are the common challenges faced by sole traders when applying for a mortgage, and how can they be overcome?

Common challenges include:

- providing a stable income,

- meeting trading history requirements, and

- potential credit issues.

Overcoming these challenges involves:

- maintaining detailed and accurate financial records,

- building a robust credit profile, and

- consulting a mortgage broker specialising in self-employed clients.

How can a sole trader or partnership improve their chances of mortgage approval?

Improving chances of mortgage approval for sole traders or partnerships involves:

- maintaining clear and organized financial records,

- building a strong credit rating,

- saving a larger deposit, and

- seeking professional guidance from a mortgage broker specialising in self-employed mortgages.

Demonstrating stability in business and having a clear understanding of the lender’s criteria can also make the application more appealing.

What is the best mortgage for self-employed people?

The best mortgage for self-employed individuals, including sole traders and those in partnerships, varies according to circumstances and financial profiles. There’s no one-size-fits-all solution.

Lenders have different criteria for assessing income, trading history, and credit rating. It’s essential to consider factors like the Loan to Value (LTV), your trading history, affordability, and the type of lender that suits your specific situation.

It is best to explore different options. You can also seek professional advice tailored to your needs to find the mortgage that offers the best terms and rates for you.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache. Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself. But there’s good news: With the right support, YOU can switch your mortgage without a hitch. In this article, we’re going to […]

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]