- What is a Commercial Mortgage?

- Why Opt for a Commercial Mortgage?

- What Are The Types of Commercial Mortgages?

- Do You Qualify?

- How Much Deposit Do You Need for a Commercial Mortgage?

- How Long Does It Take To Pay Commercial Mortgages?

- What Interest Rates Should You Expect in the UK?

- What Are The Costs Involved?

- How Much Can You Borrow for a Commercial Mortgage?

- Your results

- Commercial Mortgage Lenders in the UK

- How to Prepare for a Commercial Mortgage Application?

- Steps To Apply for A Commercial Loan

- Should I Get a Commercial Mortgage for My Business?

- Alternatives To Commercial Mortgages

- Key Takeaways

- The Bottom Line

A Complete Guide To Commercial Mortgages for Businesses

You’ve poured your heart (and wallet) in your business, and now it’s time for the next BIG step: buying a space.

With rising rents and upkeep costs, owning your commercial space might make sense. But let’s be real—buying a building can be scary, especially when it comes to money.

So, here’s some good news: there are loans specifically designed for this, called commercial mortgages.

This guide has everything you need to find the perfect commercial mortgage to fuel your business’s growth.

Ready?

What is a Commercial Mortgage?

A commercial mortgage (also known as a “business mortgage”) is a type of secured loan used to buy, improve, or refinance commercial properties or land.

This includes office buildings, retail spaces, warehouses, industrial sites, and other types of commercial real estate.

This loan is backed by the property itself, meaning if you can’t pay the loan, the lender might take the property.

It works similarly to residential mortgages but is used for business properties instead.

Why Opt for a Commercial Mortgage?

Choosing a commercial mortgage over renting has several benefits. Here’s why it’s worth considering:

- Get Your Own Business Space. With a commercial mortgage, you’re on your way to owning your business space outright. Every payment you make is an investment in your future, not just money out the door.

- Lower Borrowing Costs. These mortgages often come with lower interest rates compared to other unsecured loans. This means you can save money over time, making it a smart financial choice for your business.

- Watch Your Property’s Value Grow. As you pay your mortgage over the years, your property might become more valuable. This is great news for your business, as it adds to your assets and wealth.

- Make Your Space Yours. Owning your property means you can change it however you like to fit your business perfectly—no need to ask a landlord for permission.

- Extra Money from Renting Space. If you have space you’re not using, you can rent it out. This extra income can help pay the mortgage or fund other business needs.

- Flexibility for Your Business. Life changes, and so might your business. Owning your property gives you options, like selling it or changing it to meet new needs.

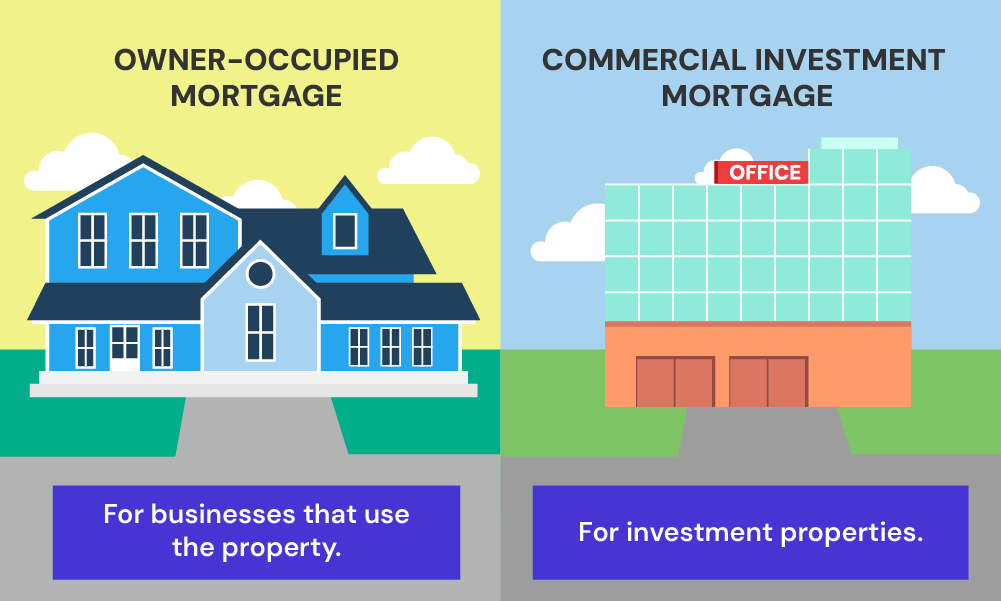

What Are The Types of Commercial Mortgages?

There are two types: Owner-occupied mortgage and Commercial investment mortgage. Here’s the difference:

Owner-occupied mortgage

This is when you get a mortgage to buy a property where your business will operate.

Choose this mortgage if you want to get space for your commercial shop, office, or factory, where your business will run.

Commercial investment mortgage

This type is for buying property as an investment, not for your business to use.

You might buy a building to rent out to other businesses and earn income from those rents.

Which Type Should You Choose?

This depends on your business goals.

Do you need a place to run your business? Then you might need an owner-occupied mortgage.

But, if you want to rent out the property to make money, a commercial investment mortgage might be ideal for you.

If you’re still unsure, consult a commercial mortgage advisor. They can offer advice tailored to your situation, helping you make the best choice.

Do You Qualify?

To get a commercial mortgage, you need to meet certain criteria.

Here’s what lenders usually look for:

- You must have a solid business plan.

- Your business should be earning a steady income to show you can afford the mortgage payments.

- A healthy credit history to prove you’re a reliable borrower.

- Business experience in your industry to show you can handle fluctuations in the business.

- Your business’s projected income shows that you can afford the loan in the long run.

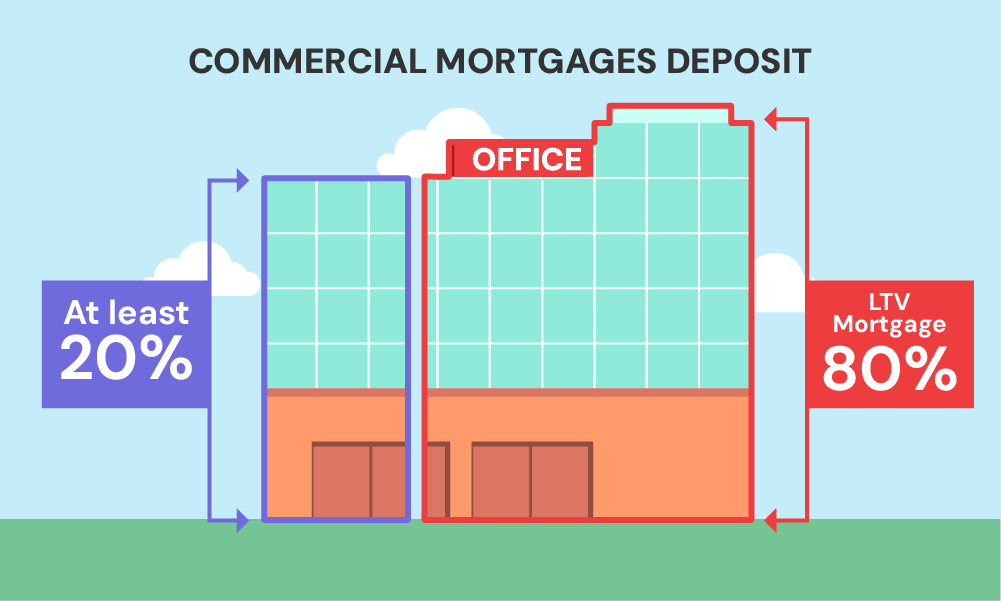

- A deposit, usually 20% to 40% of the loan’s value.

- Your business earns income from renting out property that boosts your overall cash flow.

Overall, lenders will take a close look at your financial health.

To help you get started, you may check your financial health here.

How Much Deposit Do You Need for a Commercial Mortgage?

The deposit you need for a commercial mortgage varies. However, generally, you’ll need between 20% to 40% of the property’s value.

The exact amount can change based on how risky the lender thinks the loan is.

A bigger deposit usually means better interest rates and terms for your mortgage. It shows lenders you’re serious and reduces their risk.

So, saving up for a bigger deposit can really pay off in the long run.

How Long Does It Take To Pay Commercial Mortgages?

Paying off a commercial mortgage usually takes between 3 to 25 years.

The right term for you depends on a few things – such as your business plans and your monthly repayments.

Shorter terms mean higher monthly payments, but you’ll pay less interest overall.

Longer terms spread out the payments, making them smaller, but you’ll pay more interest over time.

Our tip? Find the balance in your cash flow. You want to keep enough money in your business while paying off the mortgage efficiently.

What Interest Rates Should You Expect in the UK?

Interest rates on commercial mortgages in the UK can vary.

They depend on your business’s situation, the property, your credit profile, the economy, and the lender’s terms.

Generally, rates may start from 3% higher than the Bank of England’s base rate and can go up to 12% per annum.

For example, with the Bank of England’s base rate currently sitting at 5.25%. The lowest rate you might get for a commercial mortgage would be 8.25% (that’s the base rate + 3%).

This rate can go as high as 12%, depending on your situation and the lender’s terms.

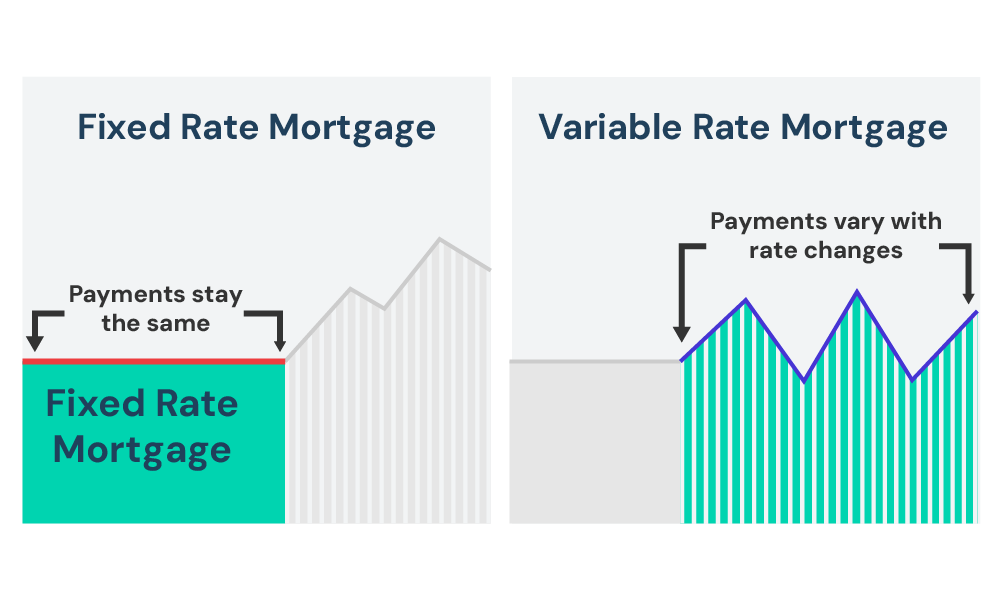

There are two types of rates: fixed and variable.

- Fixed rates stay the same throughout a period, making budgeting easier since your payments won’t change.

- Variable rates can go up or down based on the market, which might save you money when rates are low but could cost you more if rates rise.

The choice depends on what you’re comfortable with and your outlook on future rates.

What Are The Costs Involved?

When you get a commercial mortgage, there are costs both at the start and during the loan. Here’s what to expect:

- Arrangement Fee – Lenders charge this for setting up your mortgage. It’s often 1% to 2% of the loan amount, sometimes payable upfront or added to your mortgage balance.

- Valuation Fee – This covers the lender’s cost to assess the property’s value. It can range from £500 to £1,500, depending on the property size and complexity. This fee is usually paid upfront.

- Legal Fees – You’ll need to cover the cost for a solicitor to manage the legal aspects. Expect to pay between £500 and £5,000, significantly varying based on transaction complexity. This is paid upfront.

- Surveyor’s Fee – If a detailed survey is needed, it could cost you from £400 to over £1,000, paid upfront. This fee ensures the property’s condition is thoroughly evaluated.

- Booking Fee – Some lenders might ask for a booking fee to lock in a mortgage deal, typically around £100 to £250, paid upfront.

- Early Repayment Charge – Paying off your mortgage early might incur a charge, often a percentage of the loan amount. This can vary widely, so check with your lender.

- Broker Fee – Using a mortgage broker might add a fee of £500 to £1,000 to your costs, though some brokers are paid via commission from the lender instead.

- Exit Fee – When you pay off your mortgage or switch to another lender, an exit fee of around £100 to £300 may apply.

Planning for these costs means you won’t be surprised later. It’s always good to ask your lender or broker about any fees so you can budget accordingly.

How Much Can You Borrow for a Commercial Mortgage?

The amount you can borrow depends on your business profit, the value of the property you’re buying, and your overall financial health.

The main factor here is that lenders want to see if you can afford the repayments. Having a large deposit, a good credit score and a strong business and financial situation may increase your borrowing amount.

Wondering how much you might be able to borrow?

Try using a commercial mortgage calculator. It can give you a clear picture before you dive into the application process. But, remember this is just an estimate based on your details.

General Mortgage Calculator

Your results

Based on the figures you provided, here are your results:

Get started with an expert broker to find out how much they could help you save on your

mortgage repayments.

Get Started

Get Started

Commercial Mortgage Lenders in the UK

While this list is not exhaustive, here are some commercial mortgage lenders in the UK you can choose from:

- ABC Finance offers up to 80% loan-to-value (LTV) with terms of up to 30 years.

- Aldermore provides mortgages up to 75% LTV, with a maximum term of 20 years and loans up to £25 million.

- Assetz Capital also has a 75% LTV limit, 20-year terms, and offers loans up to £10 million.

- Barclays doesn’t state its maximum LTV but offers terms of up to 25 years.

- Clydesdale Bank goes up to 70% LTV, with 20-year terms.

- Cambridge & Counties Bank offers up to 70% LTV, 25-year terms, and loans up to £15 million.

- Cumberland Building Society provides up to 75% LTV, with the longest term of 30 years and loans up to £2 million.

- And many more, including HSBC, ICICI Bank UK, InterBay, Landbay, Lloyds Bank, NatWest, Paragon Bank, Proplend, Rangewell, Redwood Bank, Royal Bank of Scotland, Satellite Finance, State Bank of India (UK), Together Business Finance, TSB, West One Loans, and Yorkshire Bank.

Every lender is different. The best one will offer you terms that align with your financial situation and goals. It’s also worth taking the time to consult with a mortgage advisor to explore your options thoroughly.

>> Source: Top 26 UK Commercial Mortgage Lenders | Business Financing

How to Prepare for a Commercial Mortgage Application?

Getting ready for a commercial mortgage application means gathering lots of documents and making sure your business looks its best.

Here’s what you’ll need:

- A solid business plan that maps out your company’s future.

- Financial statements, including profits, losses, and cash flow, from the last 2-3 years to show how your business has been doing.

- Both your personal and business tax returns for the last 2-3 years to verify income.

- Recent bank statements, usually for the last 6-12 months, give a current picture of your business’s finances.

- Detailed info on the property you’re looking to buy or remortgage, like its address, size, and the income it generates.

- Your personal and business credit reports show lenders your track record with managing debt.

- A list of what you own and owe, to show your financial stability.

- Proof that you can cover the deposit, which affects your loan terms.

To improve your application:

- Make sure your documents are up-to-date and accurate.

- Improve your credit score by paying down debt and correcting any errors on your report.

- Have a solid down payment to lower the lender’s risk.

- Be ready to explain how you’ll use the property and how it fits into your business plan.

Steps To Apply for A Commercial Loan

Let’s say you’re a business owner looking to buy a new space for your growing company.

You’ve set your eyes on a property priced at £500,000.

Here’s how a typical commercial mortgage process might unfold for you:

- Initial Consultation – You speak with a mortgage broker to understand what you can afford. They advise you on what documents you’ll need and how to prepare your application.

- Application Submission – With your broker’s help, you apply to a lender. You’re hoping to borrow £400,000, which is 80% of the property’s value, meaning you’ll need a £100,000 deposit.

- Property Valuation – The lender arranges for the property to be valued to ensure it’s worth the £500,000 price tag. This costs you around £1,000.

- Approval and Offer – The lender likes your business’s financials and the property’s valuation. They offer you a £400,000 mortgage at a 5% interest rate over 20 years.

- Legal Checks and Finalisation – Your legal team and the lenders go through the final checks. This involves some legal fees, let’s say £3,000.

- Completion – Everything checks out, and the deal is done. You now have a £400,000 mortgage, and you pay around £2,639 per month for the next 20 years.

Here’s a simple table to break down your costs:

| Description | Cost (£) |

|---|---|

| Property Price | 500,000 |

| Deposit | 100,000 |

| Mortgage Amount | 400,000 |

| Valuation Fee | 1,000 |

| Legal Fees | 3,000 |

| Monthly Repayment | 2,639 |

Remember, this is just an example. Your real situation can vary based on the property, your business, and the market conditions.

For accurate advice, it’s best to talk to a good mortgage broker. They can guide you through the process and help find the best deal for your circumstances.

Unsure where to begin? Reach out to us. We can set up a free, no-obligation consultation with a commercial mortgage advisor who can help you get started in building your dream commercial space.

Should I Get a Commercial Mortgage for My Business?

Again, this decision depends on you. But here are some pros and cons to help you make a smart choice about this:

Pros

- You gradually own more of your property, which could go up in value, boosting your business’s worth.

- Having a permanent spot means no surprise rent increases, giving you financial stability.

- Renting out part of your space can bring in extra cash.

- You might get tax deductions for paying mortgage interest and other property-related expenses.

- Full control over the property lets you tailor it to exactly what your business needs.

Cons

- There are quite a few costs you’ll need to pay upfront–deposit and other fees – which can add up.

- Paying back the loan plus interest can take a big chunk out of your budget.

- If property values drop, you might end up with a property worth less than you paid.

- All repairs and upkeep are your responsibility, which can be both expensive and time-consuming.

- The process can be complex and slower due to extra-legal checks involved in your business.

- If you need to move or adjust quickly due to changing business needs, owning a property can tie you down.

Alternatives To Commercial Mortgages

If a commercial mortgage doesn’t seem right for you, there are other ways to finance your business property:

- Leasing. Opting to lease or rent a property gives you the flexibility of not being tied down by a mortgage. While you won’t own the space, it’s often a less financially heavy option in the short term.

- Bridging Loans. These can be a lifeline if you need to purchase a new property quickly but haven’t sold your current one yet. They’re short-term, giving you the breathing space to sell without rush.

- Short-term Loans. Ideal for when you need a cash injection but don’t want to commit for the long haul. These can help with immediate expenses like cash flow or capital needs, offering a temporary financial cushion.

- Personal Loans. If your business’s financing needs are on the smaller side, a personal loan might work. You can borrow a sum, typically up to £25,000, without needing to own a home.

Key Takeaways

- A commercial mortgage is a secured loan for buying or refinancing business properties, using the property as collateral.

- You can choose between an owner-occupied mortgage (for your business) or a commercial investment mortgage (for renting out).

- Expect to need a 20-40% deposit, a solid business plan, steady income, and good credit to qualify.

- Commercial mortgage terms range from 3 to 25 years, with interest rates generally starting 3% above the Bank of England’s base rate.

- If a commercial mortgage isn’t right for you, alternatives include leasing, bridging loans, and short-term loans.

The Bottom Line

Applying for a commercial mortgage can seem daunting, but it’s a step toward growth for many businesses.

The KEY to success is to present a strong, financially sound business.

Also, being familiar with the types of mortgages, risks, and paperwork needed can make the process smoother.

If you’re considering a commercial mortgage, it is always wise to team up with a good commercial mortgage advisor. They can guide you through the application, find the best rates, and increase your chances of approval.

Thinking about taking the next step with a commercial mortgage? Reach out to us.

We’ll match you with a top-notch commercial mortgage advisor who can help turn your business goals into reality.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What is a part-commercial mortgage?

A part-commercial mortgage is for properties that have both commercial and residential parts, such as buildings with shops on the ground floor and apartments above. This type differs from a purely commercial mortgage because it involves living space too.

The interest rates for these mortgages can change, but if you’ve got experience with commercial property or have been a landlord for a while, you’re likely to get a better deal. This is because lenders prefer working with people who know the ropes of managing or renting out property.

Are there restrictions on the type of business I can operate?

Yes, lenders have rules on the types of businesses they’re willing to finance. This is because some businesses are considered riskier than others. Always check with your lender to see if your business type fits their criteria.

Can I change my residential mortgage to a commercial mortgage without extra fees?

Remortgaging from a residential to a commercial mortgage can involve some costs. The exact process and fees depend on your lender and your current mortgage agreement. It’s important to talk to your lender first to understand any penalties or fees involved.

Is it possible to get a commercial mortgage on property held on lease?

Yes, you can get a commercial mortgage on a leasehold property, but there are extra considerations.

Lenders will look at the length of the lease – the longer (usually 70 years left on the lease), the better, as it reduces their risk. Make sure your lease is long enough to cover the mortgage term.

Can I get a mortgage for a residential purpose on a commercial property, or vice versa?

In some cases, yes, but it’s complicated. You might be able to convert a commercial property for residential use or secure a residential mortgage on a property with commercial potential.

However, this involves meeting specific criteria and possibly getting planning permission. Always consult with a mortgage advisor and check local regulations to see what’s possible for your situation.

Related Articles

Can You Change From Commercial Mortgage To Residential?

Since 2015, it’s been easier to switch your mortgage from commercial to residential, all thanks to the UK government’s major changes to the General Permitted Development Order (GPDO). These rules have simplified changing a building’s use from commercial to residential, offering developers more opportunities to turn unique business spaces into homes. You might be considering […]

Should You Get A Semi-Commercial Mortgage? A Guide

If you want to own a building with a shop on the ground floor and flats above, you’re the perfect candidate for a semi-commercial mortgage. This option is also great for investors looking to buy such mixed-use properties and for developers aiming to create spaces that blend living and commercial areas. Curious? This article explores […]

How To Buy A Pub With Commercial Mortgages? A UK Guide

Pubs are more than just places to drink. They’re the soul of British culture – a haven where locals gather to unwind, celebrate, or simply enjoy a quiet pint after a long day. For anyone dreaming of swapping their office view for the behind-the-bar camaraderie, the idea of running a pub might sound like the […]