- What Is A CIS Mortgage And How Does It Apply To You?

- How Can You Make CIS Mortgages Work For You?

- Why Choose A CIS Mortgage?

- Are You Eligible for a CIS Mortgage?

- How Much Can You Borrow with a CIS Mortgage?

- How Much Deposit Will You Need for a CIS Mortgage?

- What Are The Requirements For A CIS Mortgage?

- Can I Get A CIS Mortgage With Bad Credit?

- The Bottom Line: How Can a Mortgage Broker Help You

How CIS Mortgages Can Benefit You: A Complete Guide

If you work in the construction industry, understanding Construction Industry Scheme mortgages (CIS mortgages) could open new doors for you.

Though the term ‘CIS mortgage’ isn’t an official classification, it refers to the application process for a mortgage using the CIS scheme, tailored specifically to the needs of construction workers like you.

CIS mortgages are a fitting solution for those who might not have three years’ accounts or who have declared a low net profit.

Unlike traditional mortgage applications that hinge on filed accounts, CIS mortgages take into consideration your gross income from payslips.

This unique approach makes it an attractive option for many construction industry professionals.

Whether you’re a seasoned builder or a budding contractor, this guide is crafted for you. It’s time to explore how you can unlock the opportunities of a mortgage tailored to the construction profession

What Is A CIS Mortgage And How Does It Apply To You?

The Construction Industry Scheme (CIS) is more than just a financial term—it’s a gateway to homeownership for many in the construction field.

Initiated by HMRC, CIS aims to simplify tax matters for contractors and subcontractors alike.

Under this scheme, contractors can deduct certain amounts from the payments to subcontractors, forwarding them to HMRC as advance payments for taxes and National Insurance.

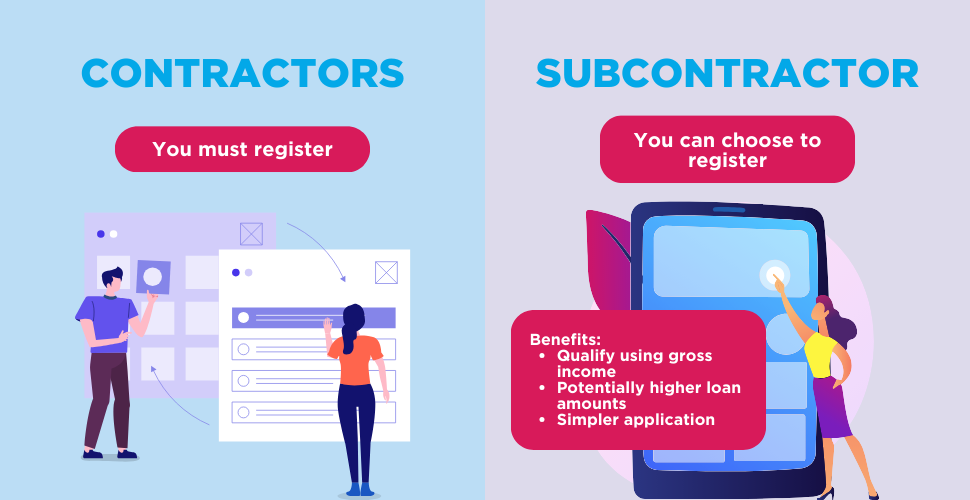

If you’re a subcontractor, you may be wondering if this scheme is mandatory. The good news is, it’s not.

While contractors must register, as a subcontractor, you have a choice. And this choice can influence the deductions made from your earnings.

By using the CIS method for your income, you pave a smoother path to applying for a mortgage. What’s more, you stand a chance to borrow more, putting you closer to your dream home.

Here are some of the benefits of a CIS mortgage:

- You can use your gross income, rather than your net income, to apply for the mortgage.

- You may be eligible for higher borrowing limits.

- The application process may be simpler, as you will not need to provide business accounts.

How Can You Make CIS Mortgages Work For You?

If you’re self-employed in construction and write off many expenses to reduce your tax, this may make getting a mortgage tricky.

This practice can make your net profit appear lower, and traditional lenders, who focus on this net figure, might offer you less than you were hoping for.

As discussed earlier, CIS mortgages change this by focusing on your gross income instead of the net. This can boost the mortgage amount you can borrow.

Here are some tips on how to make CIS mortgages work for you:

- Get registered with HMRC. This is a government scheme that requires contractors to deduct tax and National Insurance from payments made to subcontractors. Once you’re registered, you’ll have a CIS number that you can provide to your lender.

- Provide your lender with your payslips. This will show your gross income, which is the amount of money you earn before expenses are deducted.

- Look for lenders who specialise in CIS mortgages. These lenders are more familiar with the scheme and will be more likely to approve your mortgage application.

- Be prepared to provide additional documentation. This may include your business accounts, tax returns, and P60s.

If you’re working hard in construction, this mortgage type recognises that effort and offers a realistic borrowing amount in line with your actual earnings.

It’s wise to consult with a good mortgage broker to ensure that you fully understand and take advantage of the opportunities available through CIS Mortgages tailored to your profession.

Why Choose A CIS Mortgage?

If you’re a construction worker operating under the CIS scheme, a CIS mortgage can provide you with some valuable benefits.

Benefits

- Borrow More – Your gross income, rather than net, is taken into account, meaning you could borrow more.

- More Suitable Lenders – Many lenders offer mortgages to CIS workers, so you can take advantage of offers designed specifically for your profession.

- Streamlined Application – While most lenders require at least three years of accounts, the CIS scheme could get you approved with just one year’s accounts.

- Better Rates and Deals – The ability to borrow more may translate into better rates and deals tailored for you.

While it can be a fantastic option for many in the construction industry, it’s wise to understand the potential drawbacks that might affect you.

Drawbacks

- Not Everyone Offers It – You might find that not all lenders offer CIS mortgages, and those that do might have specific requirements. It could limit your options.

- Interest Rates Could Be Higher – Depending on your financial situation, you might end up with a higher interest rate compared to standard mortgages.

- Watch Out for Tax – The deductions are meant to be payments toward your tax and National Insurance. Mishandle these, and you could face unexpected tax bills.

- Additional Information Requirements – Applying for a CIS mortgage may require you to provide additional information. This extra step could make the process a bit more complex for you.

A CIS mortgage offers unique benefits but comes with its drawbacks. If you’re thinking of going down this path, a clear understanding of both can lead you to make an informed decision tailored to your situation.

If in doubt, consulting an expert could be the next best step.

Are You Eligible for a CIS Mortgage?

When it comes to CIS mortgages, not every lender is on board, and criteria can vary widely among those who do offer them. You will be assessed individually, but here’s what most lenders typically look for:

- 3 to 6 months of CIS payslips, with 6 months being quite common

- 3 to 6 months of bank statements, again leaning towards 6 months

- Tax on the scheme must be deducted at 20%

- Minimum of 5% deposit or more.

- Good credit history

These requirements are there to ensure that you fit the profile for a CIS mortgage, making the process transparent and straightforward for you.

How Much Can You Borrow with a CIS Mortgage?

If you’re considering a CIS mortgage, lenders will determine your borrowing power based on your average annual income, using either twelve months’ payslips or the latest 3-6 months of payslips.

They will focus on your gross income to calculate this average.

Once they’ve assessed your average annual income, lenders typically offer to lend an amount up to four times that income.

But keep in mind, your outgoings and other financial commitments, such as loans, additional mortgages, or credit cards, will also be considered.

These factors combined will provide lenders with a clear indication of how much you can comfortably borrow.

Use the self-employed mortgage calculator to see how much you might be able to borrow.

How Much Deposit Will You Need for a CIS Mortgage?

When applying for a CIS mortgage, the deposit plays a crucial role. While it’s possible to find a mortgage with only a 5% deposit, aiming for at least 10% is generally recommended.

The size of your deposit directly impacts the mortgage rates you’ll be eligible for. A larger deposit often leads to better mortgage rates, making a 15% deposit an ideal target, though anything above this is certainly advantageous.

Remember, understanding both the borrowing capacity and the importance of your deposit size in the CIS mortgage process is key.

These insights will guide you in making informed decisions as you pursue your goal of homeownership.

What Are The Requirements For A CIS Mortgage?

If you are a construction worker and registered for the Construction Industry Scheme (CIS), you’ll find that the process is quite straightforward.

Lenders will typically ask for your payslips to verify your income. Being registered means you might not need to provide complete accounts; payslips alone could suffice.

However, if you’re unregistered, the process might be a bit different. You may be asked to provide accounts for at least one year and possibly an SA302.

Some lenders may even require three years of employment history. Being unregistered often leads to your mortgage amount being assessed on declared net income figures, which could be lower than if you were registered.

That’s why a CIS mortgage could be particularly beneficial if you’re a self-employed construction worker.

Can I Get A CIS Mortgage With Bad Credit?

Having bad credit doesn’t necessarily shut the door to obtaining a CIS mortgage. There might still be lenders willing to work with you, especially since the CIS mortgage framework acknowledges the unique financial dynamics of construction workers.

Of course, having bad credit can make the process more complex, but it doesn’t make it impossible.

By seeking expert advice and taking a proactive approach to understanding your options, you might find suitable lenders who specialize in cases with adverse credit.

Enquiring a mortgage broker could be a great first step. They can explain the nuances and guide you through the process, helping you find a mortgage that aligns with your circumstances.

The Bottom Line: How Can a Mortgage Broker Help You

For construction workers looking for homeownership, exploring CIS Mortgages is worth the effort.

With benefits such as better rates and borrowing capacity tailored to your unique income structure, it’s an option that aligns well with your profession.

While the process might seem complex at first glance, it doesn’t have to be overwhelming.

Seeking professional advice from a mortgage broker who understands the unique nature of CIS Mortgages can guide you without pushing you into something that doesn’t suit your needs.

If you want to get started, feel free to reach out to us. We will link you with a good mortgage advisor specialising in CIS mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can a subcontractor like me get a CIS mortgage easily?

Yes, as a subcontractor, you can get a CIS mortgage more easily if you are registered under the Construction Industry Scheme (CIS).

Unlike traditional self-employed individuals, who often need 2-3 years’ worth of accounts, being part of the CIS allows you to leverage your gross income, potentially smoothing the mortgage application process.

It can make obtaining a mortgage more straightforward and might even provide access to better terms and rates. Make sure to consult with a mortgage expert who is familiar with the CIS to guide you through the specifics of the application.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache. Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself. But there’s good news: With the right support, YOU can switch your mortgage without a hitch. In this article, we’re going to […]

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]