- What Are Early Repayment Charges?

- Why Do Lenders Charge ERCs?

- Can You Get a Mortgage Without ERCs?

- What Types of No ERC Mortgages Are Available?

- What About Buy-to-Let Mortgages with No ERCs?

- What Are the Benefits of No ERC Mortgages?

- Are There Any Drawbacks to No ERC Mortgages?

- How Can You Avoid ERCs on Standard Mortgages?

- Which UK Lenders Offer No ERC Mortgages?

- Is a No ERC Mortgage Right for You?

- How Can You Find the Best No ERC Mortgage?

- Are There Alternatives to No ERC Mortgages?

- The Bottom Line

Mortgages with No Early Repayment Charges Explained

Many UK homeowners dread those pesky early repayment charges (ERCs) that can cost thousands if you want to clear your mortgage sooner than planned.

If you’re one of them, you might be looking for ways to avoid these fees or find more flexible mortgage options.

Here’s the thing: some mortgages don’t have ERCs. But there’s a trade-off – these products often carry slightly higher interest rates.

It’s a classic case of weighing up flexibility versus cost.

Let’s dig deeper, understand how these options work, and see if they’re the right fit for your situation.

What Are Early Repayment Charges?

An early repayment charge is a fee your lender may impose if you pay off your mortgage earlier than the agreed term.

This can happen if you:

- overpay by more than your lender allows

- switch to a new lender during your current deal, or

- need to sell your home and terminate the mortgage early.

ERCs are typically calculated as a percentage of your remaining loan balance, usually ranging from 1% to 5%.

For instance, if you have £100,000 left on your mortgage and face a 5% ERC, you could be looking at a hefty £5,000 charge. That’s why it’s crucial to understand ERCs before you commit to a mortgage deal.

Why Do Lenders Charge ERCs?

Lenders want to protect their interest.

When you take out a mortgage, the lender expects to earn a certain amount of interest over the agreed term. If you repay early, they miss out on that interest income.

ERCs act as a deterrent, discouraging borrowers from switching lenders every time they spot a slightly better deal.

However, most lenders do offer some flexibility, typically allowing you to overpay up to 10% of your outstanding balance each year without incurring an ERC.

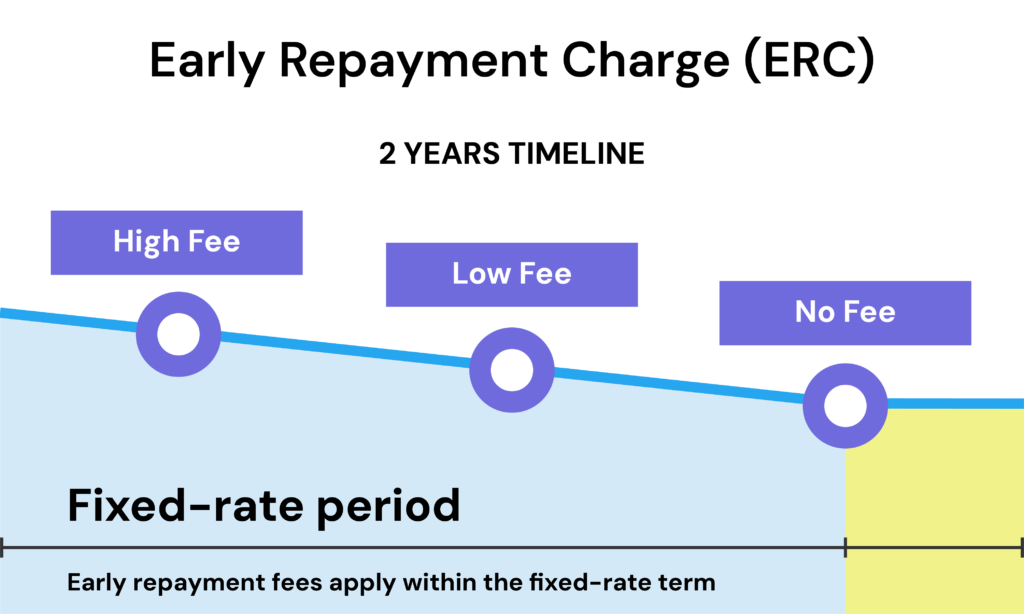

It’s worth noting that some lenders reduce their ERCs over time.

For example, you might start with a 5% charge that drops to 1% after a few years, eventually being waived altogether.

As a general rule, the longer you have left on your introductory deal, the higher the ERC is likely to be.

Can You Get a Mortgage Without ERCs?

The good news is that yes, you can find mortgages without early repayment charges.

These are often referred to as “no ERC mortgages” or “flexible mortgages”.

While they’re not as common as standard mortgages with ERCs, several UK lenders offer these products.

No ERC mortgages can be particularly appealing if you think you might want to pay off your mortgage early or if you’re uncertain about your future plans.

However, it’s important to weigh up the pros and cons before deciding if this type of mortgage is right for you.

What Types of No ERC Mortgages Are Available?

When it comes to no ERC mortgages, you have several options to choose from. Let’s explore some of the most common types:

- No ERC Fixed-Rate Mortgages. While less common, some lenders do offer fixed-rate deals without ERCs. Be prepared for potentially higher arrangement fees to offset the lack of ERCs.

- No ERC Tracker Mortgages. These are quite common, especially once you’ve moved onto the lender’s standard variable rate (SVR). This is often a good time to remortgage without facing an ERC.

- No ERC Equity Release Mortgages. These are less common due to the nature of equity release products, but some lenders may offer them or waive ERCs after a certain period.

What About Buy-to-Let Mortgages with No ERCs?

If you’re a landlord or considering investing in property, you might be interested in buy-to-let mortgages with no early repayment charges.

These products do exist, although they’re less common than residential no ERC mortgages.

Buy-to-let mortgages without ERCs can be particularly beneficial for landlords who:

- Plan to sell properties within their portfolio

- Want the flexibility to remortgage frequently to take advantage of the best rates

- Expect to receive lump sums that could be used to pay down mortgage debt

However, as with residential mortgages, buy-to-let mortgages without ERCs often come with higher interest rates.

You’ll need to carefully calculate whether the flexibility justifies the potential extra cost.

What Are the Benefits of No ERC Mortgages?

Opting for a mortgage without early repayment charges can offer several advantages:

– Flexibility. You have the freedom to make overpayments or pay off your mortgage entirely without penalty. This can be especially beneficial if you receive a bonus, inheritance, or other lump sum.

– Potential interest savings. By making overpayments, you can reduce the overall interest you’ll pay over the life of your mortgage.

– Easier to remortgage. Without ERCs, you can switch to a better deal as soon as one becomes available, rather than waiting for your initial deal period to end.

– Sell your property without penalty. If you need to move house unexpectedly, you won’t face additional charges for paying off your mortgage early.

– Peace of mind. Knowing you’re not locked into your mortgage can provide a sense of financial security and control.

Are There Any Drawbacks to No ERC Mortgages?

While no ERC mortgages offer great flexibility, they’re not without their downsides:

– Higher interest rates. To compensate for the lack of ERCs, lenders often charge slightly higher interest rates on these mortgages.

– Limited fixed-rate options. Most no ERC mortgages are variable rate products. If you’re looking for the security of a fixed rate, your options may be more limited.

– Shorter deal periods. Some lenders only offer no ERC deals for shorter periods, such as two years, after which you might need to remortgage.

– Stricter lending criteria. Because these mortgages are riskier for lenders, you might face stricter eligibility requirements.

– Potential for higher overall costs. If you don’t make use of the flexibility, you could end up paying more in interest over the life of the mortgage compared to a product with ERCs.

Before choosing a no ERC mortgage, carefully consider whether the flexibility justifies any potential extra costs.

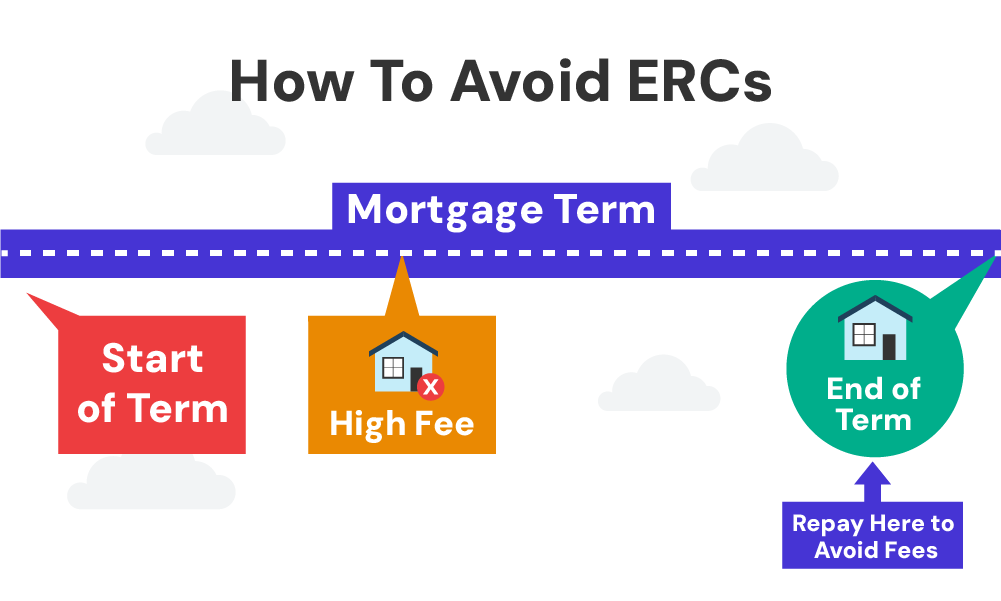

How Can You Avoid ERCs on Standard Mortgages?

If you already have a mortgage with ERCs, there are still ways to minimise or avoid these charges:

- Time Your Repayments. Plan your overpayments or full repayment towards the end of the mortgage term or at the end of a fixed-rate period. ERCs often decrease or are eliminated after the initial fixed period or as the mortgage term progresses.

- Use Your Overpayment Allowance. Most lenders allow you to overpay by up to 10% each year without incurring ERCs. Take advantage of this if you can.

- Port Your Mortgage. If you’re moving house, you might be able to take your current mortgage with you, avoiding ERCs.

- Switch to a More Flexible Mortgage. When your current mortgage deal ends, consider remortgaging to a new product that offers more flexibility with early repayments. Some lenders offer flexible mortgages with lower or no ERCs after an initial period.

- Wait it Out. If you’re close to the end of your ERC period, it might be worth waiting until it expires before making any changes.

Which UK Lenders Offer No ERC Mortgages?

Several UK banks and building societies offer mortgages without early repayment charges.

This includes:

- Leeds Building Society

- Newcastle Building Society

- Axis Specialist Finance

- Clydesdale

- Coventry for Intermediaries

These lenders typically offer no ERC mortgages as Bank of England tracker rates or discounted variable deals.

It’s worth noting that while standard variable rate (SVR) mortgages usually don’t have ERCs, their interest rates tend to be much higher than other products.

Is a No ERC Mortgage Right for You?

Deciding whether a no ERC mortgage is right for you depends on your circumstances. You might consider a no ERC mortgage if:

- You’re unsure about your future plans and want maximum flexibility.

- You think you might come into a lump sum of money that you’d like to use to pay off your mortgage.

- You’re self-employed or have a variable income and want the option to make large overpayments without penalty.

- You’re a buy-to-let investor looking to regularly refinance your properties.

However, if you’re confident you won’t need to repay your mortgage early and you’re looking for the lowest possible interest rate, a standard mortgage with ERCs might be more suitable.

How Can You Find the Best No ERC Mortgage?

Finding the best no ERC mortgage requires some research and potentially professional advice. Here are some steps you can take:

- Compare Offers. Look at products from different lenders, comparing not just the interest rates but also any fees and the overall cost of the mortgage.

- Check the Small Print. Make sure you understand all the terms and conditions, not just the lack of ERCs.

- Think Long-Term. Consider how your circumstances might change and whether the flexibility of a no ERC mortgage is worth potentially higher costs.

- Consider a Broker. A mortgage broker can help you navigate the market and find deals that might not be directly available to consumers.

Are There Alternatives to No ERC Mortgages?

If you’re attracted to the flexibility of no ERC mortgages but put off by the potentially higher interest rates, there are alternatives to consider:

- Mortgages with limited overpayment allowances – As discussed, many mortgages let you overpay up to 10% each year, helping you clear your debt faster and become mortgage-free sooner. This avoids Early Repayment Charges (ERCs).

- Offset mortgages – These allow you to use your savings to reduce the interest you pay on your mortgage, potentially allowing you to pay it off early without ERCs.

- Shorter fixed-rate periods – By choosing a shorter fixed-rate period, you’ll have the opportunity to remortgage sooner without facing ERCs.

- Split mortgages – Some lenders allow you to split your mortgage, with part on a fixed rate with ERCs and part on a variable rate without ERCs.

These options might provide a middle ground, offering some flexibility without the potentially higher rates associated with full no ERC mortgages.

The Bottom Line

No Early Repayment Charge (ERC) mortgages offer flexibility, allowing you to overpay without penalty.

However, these mortgages might not be the cheapest option due to potentially higher interest rates or fees.

While valuable for some borrowers who prioritise flexibility, no ERC mortgages aren’t a one-size-fits-all solution.

To make an informed decision, consult a qualified mortgage broker. They can assess your situation, compare mortgage options, and help you find lenders offering no ERC mortgages if it aligns with your goals.

Ready to explore your options? Simply contact us, and we’ll connect you with a reputable mortgage broker to guide you through the application process.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do all mortgages have early repayment charges?

Not all mortgages penalise you for early repayment. Early repayment charges (ERCs) are common with fixed-rate and some tracker mortgages, but there are also products designed specifically to avoid these fees.

To be certain, always check your mortgage agreement or talk directly to your lender to confirm if ERCs apply to your specific mortgage.

Are there fees for paying a mortgage early?

Many fixed-rate and some variable-rate mortgages charge fees for early repayment, known as early repayment charges (ERCs). These fees vary by lender and mortgage terms. Check your mortgage agreement or ask your lender for details.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]