- What Is Buy to Let?

- How Does Buy to Let Work?

- What Is a Buy to Let Mortgage?

- Are Buy To Let Properties Worth It in 2024?

- Am I Eligible?

- What Makes A Good Rental Yield?

- How Much Deposit Do I Need To Put Down?

- How Much Can I Borrow?

- What Rates Should I Expect For Buy To Let Mortgages?

- Buy to Let Mortgages Fees and Costs

- Get The Paperwork Right: Hereâs Your Checklist

- How To Get a Buy to Let Mortgage?

- Buy To Let Taxes Explained

- How To Choose the Right Buy to Let Property

- Can First-Time Buyers Get a Buy To Let Mortgage?

- Can You Remortgage a Buy To Let?

- What If You Need To Rent Out Your Home Temporarily?

- Landlord Responsibilities Checklist

- Should You Get Buy To Let Mortgages?

- Key Takeaways

- The Bottom Line

Everything About Buy To Let Mortgages: A 2025 Guide

They say you can’t buy happiness, but you can buy property (and that’s pretty close).

For those aiming for regular income, building long-term wealth, or diversifying investments, buy to let is a popular choice.

The idea is simple: buy a property, find tenants, earn from rent and possibly the property’s value growth.

And one way to fund this purchase is through a buy to let mortgage. What’s this, who can apply, and how to get one – we’ve covered it all in this guide.

What Is Buy to Let?

Buy to let (BTL) is when you buy a property intending to rent it out. This is different from buying a house to live in yourself.

Over the years, buy to let has grown in the UK, showing its strength in the property market.

The concept is all about investing your money in a physical asset – a house or flat – and using it to generate rental income and, hopefully, capital appreciation over time.

How Does Buy to Let Work?

Buy to let means you buy a property to rent it out. Your goal as a landlord is to earn money from the rent.

This rent should help pay for any costs such as your mortgage, any expenses like maintenance costs, insurance, and fees for letting agents if you use one.

Over time, you might also make money if the property’s value goes up. So, when you sell the property, it could be worth more than you paid.

For buy to let to be a good choice for you, picking the right property is key. You need to find a place that’s priced well and can get good rent.

Look around the housing market to find where demand for rentals is high and think about what type of home would attract the people you want to rent to.

Running your property well, on your own or with a management agency, means happy tenants and steady rent.

What Is a Buy to Let Mortgage?

A buy to let mortgage lets you purchase a property intended for renting out. This type of mortgage is different from your standard mortgage because it depends on the possible rent you could earn from the property.

Here’s what else you need to know:

| Feature | Residential Mortgage | Buy to Let Mortgage |

|---|---|---|

| Purpose | For buying a property you intend to live in. | For purchasing a property to rent out to tenants. |

| Income Consideration | Based on your salary and creditworthiness. | Mainly based on the potential rental income from the property. Expected rental income typically needs to be at least 125% of the monthly mortgage payments. |

| Interest Rates | Generally lower, reflecting the perceived lower risk. | Higher, due to the higher risk associated with rental properties. |

| Deposit | Can be as low as 5-10% of the property’s value. | Usually requires a larger deposit, often 20-25%, with the best rates at 40% or more. |

| Fees | Standard arrangement and valuation fees. | Higher arrangement fees, sometimes calculated as a percentage of the loan amount. |

| Repayment Type | Mostly capital and interest repayments, meaning you pay off part of the loan and the interest each month. | Often interest-only, where monthly payments cover only the interest, and the original loan amount is repaid at the end of the term. |

| Minimum Income Requirements | Income must be sufficient to cover mortgage repayments and other expenses. | Often requires a minimum personal income of £20,000-£25,000, besides the expected rental income. |

Are Buy To Let Properties Worth It in 2024?

Opinions on buy to let investments in 2024 are mixed. Here’s why.

Some argue it’s not the best move this year.

With rising mortgage rates, your monthly costs go up, which could cut into what you make from rent.

Many are also worried that house prices might fall. If your property’s value drops soon after buying, you might not make a quick profit.

Changes in rental laws are another headache. New rules, like the 5% extra stamp duty and changes to mortgage interest relief, complicate things. The Renters’ Reform Bill might also shake up the scene, potentially squeezing landlords’ earnings.

The effort and cost to keep a property up to scratch and legal can also turn people off. However, there’s still a strong case for buy to let.

Rental demand is high in many places, promising steady income. If you’re in it for the long haul, short-term value dips might not bother you. You’re looking at the potential for rent income and value growth over the years.

Also, today’s market might let you buy at a lower price, raising your profit chances later.

So, is buy to let worth it in 2024? It depends on your financial stance, investment strategy, and how you see the market trends.

Am I Eligible?

To qualify for a buy to let mortgage, you need to:

- Meet the minimum age criteria. Some lenders might want you to be at least 21 years old

- Have at least 20-25% of the property’s price as a deposit.

- Prove your rental income is 125-145% of your mortgage payments – This is known as rental yield.

- Earn a certain amount usually at £25,000 each year aside from the rent. (Not all lenders ask for this)

- Show you’ve got a good credit history, proving you’re good at paying back what you owe.

- Be a UK resident. This helps lenders check your financial situation more easily. Some lenders might consider non-residents but under stricter conditions.

- Own a residential property to show your experience in handling properties. (Depends on lender’s criteria)

What Makes A Good Rental Yield?

Let’s say you buy a property for £200,000 and it brings in £10,000 a year from rent, your rental yield is 5%(£10,000 divided by £200,000).

Rental yield is a simple way to see how much money a rental property makes each year compared to its purchase price.

A good rental yield varies. However, in the UK a figure between 5-8% means your investments give you a decent return.

Anything above this is often seen as excellent, showing your property earns a lot relative to its price.

Buying properties in popular areas or investing in HMOs or student flats might give you higher returns. But, they also come with more work and extra costs.

To get an idea of what rent to charge, talk to letting agents or use a rent calculator.

Check below to see how much you could charge for rent. This calculator considers the type of property you have, its location, and how high demand is in that spot.

How Much Deposit Do I Need To Put Down?

You need at least 20-25% of the purchase price as a deposit. So, if you’re buying a property that costs £100,000, you’ll need to put down at least £20,000 to £25,000.

For the best deals on the market, you’ll need a deposit of at least 40% of the property price.

The size of the deposit you need can also change based on how much rent you expect to get from the property.

How Much Can I Borrow?

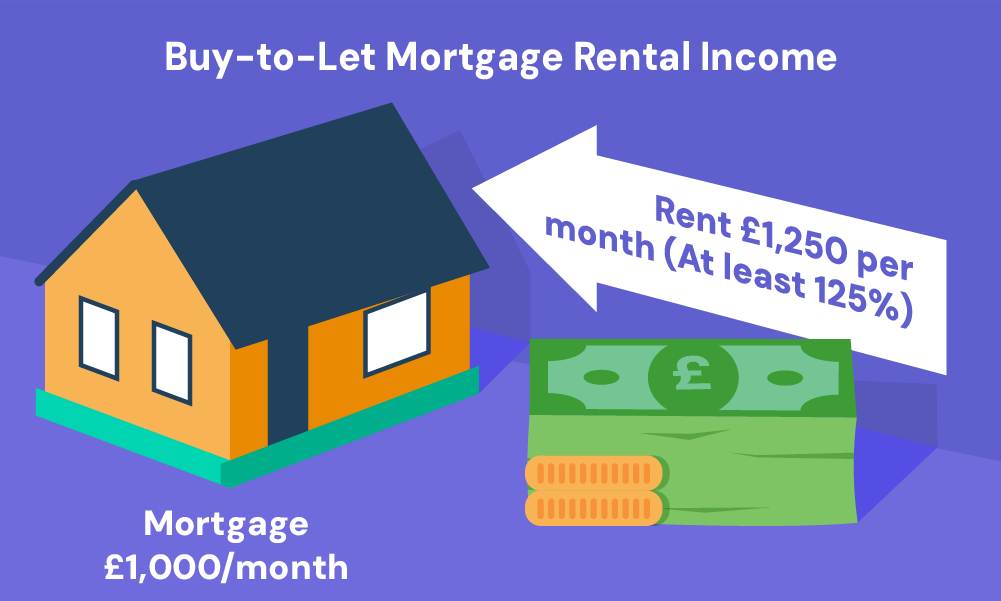

For Buy to Let mortgages, the amount you can borrow depends on the property’s rental income.

Lenders want the rent to be at least 125-130% of the mortgage payments.

So, if your mortgage is £1,000 a month, you need a rent of £1,250 to £1,300. This extra amount helps you cope with changing mortgage rates or unexpected costs.

The greater your rent, the higher the amount you can borrow.

Lenders use a rental stress test to ensure the rent you charge can comfortably cover the mortgage payments under these terms.

Say, you’re looking at a property with an expected rent of £15,000 a year. Your lender wants at least a 125% coverage ratio.

Here’s how the maths would go: £15,000 (annual rent) / 1.25 (coverage ratio) = £12,000 (maximum annual mortgage payment)

Break that down to monthly, and you’ve got a mortgage payment of £1,000 that the rent needs to cover.

With Buy to Let mortgage rates going up, hitting this rental figure might be tough. Lenders are getting stricter with how they calculate rent compared to mortgage payments. If your rent doesn’t hit the mark, you may need to put down a bigger deposit.

However, some lenders might look at your personal income if your rent doesn’t cover the mortgage. This means your own money can make up for any shortfall in rent.

It’s important to look around because lenders have different rules. You might find one that offers the loan amount you need, fitting your specific situation.

What Rates Should I Expect For Buy To Let Mortgages?

Right now, BTL mortgage rates are higher than they’ve been in a long time. You may find these rates ranging from 3% or more from online comparison websites.

Moreover, these rates are usually higher compared to standard residential mortgages.

To find the best rate, shop around. Or, to speed up the research process, consult with a good buy to let mortgage broker.

Buy to Let Mortgages Fees and Costs

Buy to let mortgages come with a cost. Besides paying off the mortgage itself, there are some initial fees you need to know about. Here are some of the popular ones:

- Arrangement Fee. This big fee, often around £1,500, is for the paperwork and admin to get your mortgage sorted. You can pay it upfront or add it to your mortgage, but paying straight away usually means you pay less interest over time.

- Mortgage Broker Fee. Paying for a mortgage broker’s help to snag the best deal might cost you about £500 or a part of your mortgage amount. Some brokers get paid by the mortgage lender instead of charging you directly.

- Booking Fee. Some lenders ask for this fee, a couple of hundred pounds when you apply for your mortgage. It shows you’re serious about taking the offer.

- Valuation Fee. Lenders check if the property’s price matches the loan you’re asking for. This fee can be between £100 and £1,500, changing with the property’s price.

- Conveyancing Costs. The legal bit of making the property yours costs around £850 to £1,500. This fee goes to your solicitor, and there might be extra charges on top.

- Bank Transfer Fee. Moving the mortgage money to your solicitor costs about £8 to £50. It’s for making sure the big-money move goes smoothly.

There are ongoing costs too:

- Letting Agent Fees. If you’re not managing the property yourself, letting agent fees can range from 5% to 15% of your rental income, depending on the level of service—basic tenant finding to full management.

- Landlord Insurance. This is a must to cover various risks, including damage to the property, unpaid rent, and liability claims. The cost varies based on property size, location, tenant type, and the specific insurance policies you choose, such as buildings, contents, and liability coverage.

- Maintenance and Association Membership. Keeping your property in top shape not only satisfies legal requirements but also appeals to tenants, preserving your investment’s value. Joining associations like The National Landlords Association or The Residential Landlords Association. You can get support and access to resources for managing your property effectively.

- Void Periods. Costs vary as they depend on the rental income you would have received. It’s essential to budget for periods when the property may be unoccupied between tenancies.

Get The Paperwork Right: Here’s Your Checklist

Applying for a BTL mortgage? You need these:

- A valid photo ID (like a passport or driving licence).

- Proof of where you live (like utility bills or bank statements).

- For employed folks: Your P60 and the last 3 months’ payslips.

- For the self-employed: SA302 (tax returns) and 2-3 years’ business accounts.

- The last 3 months’ personal bank statements, showing your income.

- Your solicitor’s details, who will handle the transaction.

- The estate agent’s details, if you’re buying through one.

- A mortgage statement if you already own property.

- Proof of any rental income, typically from an ARLA-regulated agent.

- Business bank statements if you own one or more rental properties.

- Any proof of where your deposits come from (like savings, a loan, or a gift).

This list isn’t everything. Lenders might ask for more based on what they need. These documents prove you’ve got the right advice and help fill out forms correctly. They usually satisfy most lender requests.

Talk directly with lenders or a mortgage broker. They’ll tell you exactly what you need for your BTL mortgage application and give you advice that fits your situation.

How To Get a Buy to Let Mortgage?

At this point, you’re likely familiar with buy to let mortgage, and the right documents.

To understand the process easier, let’s break it into an example. Imagine you’re buying a property for £200,000 with the goal to rent it out.

Here’s what you need to do:

1. Work with a Buy To Let Mortgage Broker

Find a good mortgage broker who knows the buy-to-let market well. They can help you:

- Understand mortgage rates and what they mean for you.

- Find the best mortgage deals that fit your budget.

- Guide you through applying, making sure you’ve got all the right papers.

- Give you advice tailored to your money situation and the housing market.

- Explain all the small print in your mortgage offer.

In short, they make the whole mortgage process easier for you to get through. Want an easier way to meet the right broker? Get in touch with us. We’ll set up a free, quick, no-obligation consultation with a buy to let mortgage broker.

2. Apply for the Mortgage

Submit your mortgage application through your broker.

You’ll need to provide detailed financial information, including proof of income and your expected rental income.

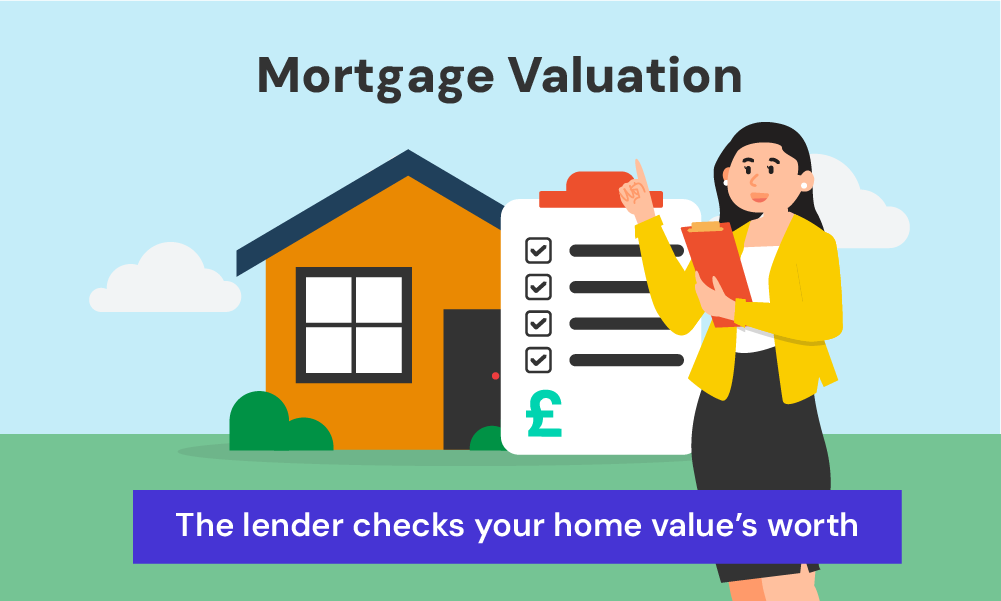

3. Undergo Mortgage Valuation

Before approval, your lender will assess the property’s worth to ensure it matches the price – the process is known as mortgage valuation. This is performed by an independent surveyor.

During this, you might be asked to pay valuation fees ranging from £150 to £500. But, some lenders may offer this for free as part of their mortgage deals.

4. Get Mortgage Approval

Once the lender has looked at the property’s valuation, your finances, and its rental potential, they might offer you a mortgage.

Let’s say they offer you a mortgage with a 75% loan-to-value (LTV) ratio, a 6.3% fixed interest rate for 5 years (payable for 25 years; arrangement fee of £1,499 ).

This means you’re borrowing £150,000 and will need at least a £50,000 deposit to buy the property.

Go over these terms and conditions with your mortgage broker to check if they match your financial plans. Not keeping up with repayments could mean you lose your buy to let property.

5. Complete the Purchase

If you’re happy with the offer, it’s key to engage with a solicitor to complete the purchase. They will handle the legal documents, transfer of funds, and property registration. This might cost you between £500 to £1,500.

Your solicitor will also check there are no issues with renting out the property. They’ll look into any rental restrictions, advice on environmental issues, planning laws, and tax.

Make sure to talk over any big plans you have for your property with your solicitor. They can give you the lowdown on what you need to think about to make your investment work best for you.

The journey from applying for your buy to let mortgage to getting the keys can take between 4 to 6 weeks. If things are straightforward, you might even secure your loan in just 4 weeks.

6. Prepare the Property for Tenants

Ensure the property meets safety standards and looks appealing.

This might involve repairs or furnishings, with costs varying widely based on the property’s condition, location, and the standard of furnishing you aim to provide.

7. Craft the Tenancy Agreement

Before you find tenants, it’s crucial to prepare a tenancy agreement or contract. This document outlines the rights and responsibilities of both you and your tenants.

It covers rent amounts, payment dates, deposit details, property maintenance, and notice periods.

You can create this agreement yourself using templates available online or seek legal advice to ensure it complies with current housing laws. Some landlords choose to have their letting agent handle this if they’re using one, ensuring all legal bases are covered.

Remember, a clear and fair contract protects both you and your tenants throughout the tenancy.

8. Find Tenants!

Once you’ve got everything set – the property all clean, bright, and spotless, it’s time to find the tenants!

Advertising online through platforms like Rightmove, Zoopla, Prime Location, and On The Market is a good start. Using high-quality photos that show off your property’s best features can make it stand out.

You can also use letting agents. They can manage adverts, conduct viewings, and vet potential tenants. They typically charge 5-15% of your rental income for their services but can save you time and effort in finding the right tenants.

Here’s a quick overview of the scenario:

| Cost Type | Amount/Rate | Details |

|---|---|---|

| Purchase Price | £200,000 | The total cost of the property you’re buying. |

| Deposit | £50,000 (25%) | The upfront amount you need to secure the mortgage. |

| Mortgage Amount | £150,000 | The amount you’re borrowing from the lender. |

| Interest Rate | 6.3% | Fixed for 5 years, on a 25-year term. |

| Monthly Repayment | £787.50* (interest-only) | Estimated interest payment based on a £150,000 mortgage at 6.3% over 25 years. |

| Arrangement Fee | £1,499 | Can be added to the mortgage or paid upfront. |

| Valuation Fee | £150 – £500 | Some lenders might offer this for free. |

| Conveyancing Fee | £500 – £1,500 | Legal fees for transferring the property. |

| Rental Income Required | £984.38+ | Must cover at least 125% of the mortgage payment for interest-only calculation. |

These numbers are just to give you an idea of how getting a BTL mortgage works. Real-life terms and your situation might be different. For advice that fits you, chat with a good mortgage broker.

Buy To Let Taxes Explained

There are only two certainties in life: death and taxes.

As a landlord, from buying your property, through renting it out, to eventually selling or passing it on, taxes are a key part of your investment.

Let’s break down the taxes you’ll encounter:

Stamp Duty

If you’re buying a second property or a buy-to-let in England or Northern Ireland, there’s an extra cost to consider: a 5% Stamp Duty Land Tax (SDLT) surcharge.

This is added on top of the regular SDLT rates and can make a noticeable difference to your budget.

Here’s a quick breakdown of the current SDLT rates (valid until 31 March 2025):

| Property Value Band | Standard Rate | Additional Property Surcharge | Total Rate for Additional Properties |

|---|---|---|---|

| Up to £250,000 | 0% | 5% | 5% |

| £250,001 to £925,000 | 5% | 5% | 10% |

| £925,001 to £1.5 million | 10% | 5% | 15% |

| Over £1.5 million | 12% | 5% | 17% |

Let’s use an example to help you understand these rates.

Say you bought a second property in 2024 for £200,000. With the 5% surcharge, your SDLT bill would be £10,000 (5% of £200,000).

From 1 April 2025, the nil-rate band for standard residential purchases will return to £125,000 (£300,000 for first-time buyers).

This will adjust the SDLT rates as follows:

| Property Value Band | Standard Rate | Additional Property Surcharge | Total Rate for Buy to Let |

|---|---|---|---|

| Up to £125,000 | 0% | 5% | 5% |

| £125,001 to £250,000 | 2% | 5% | 7% |

| £250,001 to £925,000 | 5% | 5% | 10% |

| £925,001 to £1.5 million | 10% | 5% | 15% |

| Over £1.5 million | 12% | 5% | 17% |

Using the same £200,000 example, here’s how SDLT would work from April 2025:

First £125,000:

- Standard SDLT: 0% = £0

- Surcharge: 5% of £125,000 = £6,250

Next £75,000 (up to £200,000):

- Standard SDLT: 2% of £75,000 = £1,500

- Surcharge: 5% of £75,000 = £3,750

Total SDLT:

- Standard SDLT = £1,500

- Additional surcharge = £10,000

Grand Total = £11,500

That extra 5% might not sound like much at first, but it can push up the total cost significantly, especially since most properties are priced above £125,000.

As property values climb into higher bands, the SDLT bill grows alongside them.

The good news? SDLT is deductible from any capital gains tax when you eventually sell the property, so you’re not taxed twice.

That said, reduced tax relief on mortgage interest might eat into your returns, so it’s worth factoring this into your calculations.

If you’re buying in Scotland or Wales, there are similar surcharges under their own systems—Land and Buildings Transaction Tax (LBTT) in Scotland and Land Transaction Tax (LTT) in Wales. But, the rates and thresholds differ, so check the specific rules for those regions.

Stamp duty can feel like a sting, but understanding how it works helps you prepare and make smarter investment decisions. After all, knowledge is power—and it might just save you a few grey hairs.

Capital Gains Tax

Selling your buy to let property for more than its purchase price means you’ve made a profit, which is taxable under Capital Gains Tax (CGT).

For those in the basic tax band, CGT on property is 18%. If you’re in a higher tax band, you face a 28% rate on these gains. From April 2024, this rate drops to 24%.

You also have a £3,000 tax-free allowance (£6,000 for couples), which reduces the amount of profit you need to pay tax on.

You can lower your CGT bill by deducting certain costs related to buying, selling, or improving your property, like stamp duty and solicitor fees. But only significant improvements count (normal maintenance costs are not included).

Planning and knowing these tax duties helps in managing your property investment wisely. If you’re unsure about anything, consider seeking advice from a tax advisor to guide you right.

Income Tax

The rent you collect from your tenants is taxable income.

The amount of tax you pay depends on your total income, including this rent, and which tax band you fall into. The lowest tax rate is 20%, but if you earn more, you could be taxed at 40% or even 45%.

To work out your taxable income from the property, you can deduct certain allowable expenses. These expenses might include letting agent fees, property maintenance costs, and mortgage interest.

Mortgage Interest Tax Relief

Previously, landlords could offset mortgage interest and arrangement fees against their income tax, by up to 45%

But from 2017 to 2020, this changed. Now, you get a credit for 20% of your mortgage interest instead.

This shift significantly impacts higher-rate taxpayers, possibly making them up to £2,000 a year worse off. Conversely, cash buyers and those in the 20% tax band are least affected.

Inheritance Tax (IHT)

For buy-to-let owners, your property counts towards your estate’s total value when assessing for IHT.

Should your estate’s worth go over the threshold (£325,000 for single individuals or £650,000 for those married or in civil partnerships), any amount above this limit could face a 40% tax rate.

Landlords planning ahead can find ways to lessen the IHT hit. Setting up a company for your property or using trusts are two ways to do this, but you need proper advice from experts to make these work.

How To Choose the Right Buy to Let Property

When selecting a property to rent out, remember:

- Location is key. Aim for areas with excellent transport links. A property within a 15-minute walk to train or tube stations is ideal, as it significantly boosts its rental appeal.

- Match the property to local demand. Research which types of properties are in high demand in your area. A modern flat may appeal to commuting professionals, whereas a spacious house could be more suitable for families. Getting this wrong might make it hard to find tenants.

- Consider the pros and cons of new builds. While new builds are appealing, they often come at a premium. Older properties might offer more space for your investment and could be easier to rent out if they’re not surrounded by a lot of competition from other landlords.

- Prepare for empty periods (voids). There will be times when your property is empty. Make sure you have a financial buffer to cover mortgage payments during these voids to avoid financial strain.

- Have a mortgage repayment strategy. If you opt for an interest-only mortgage, don’t rely solely on selling the property to repay it. Market fluctuations might mean the property sells for less than anticipated, so plan for how you will cover any shortfall.

Can First-Time Buyers Get a Buy To Let Mortgage?

Yes, you may be able to get a buy to let mortgage. This can be an option if you find it tricky to buy a home in your area.

You can invest in a property elsewhere, rent it out, and potentially benefit from future value growth.

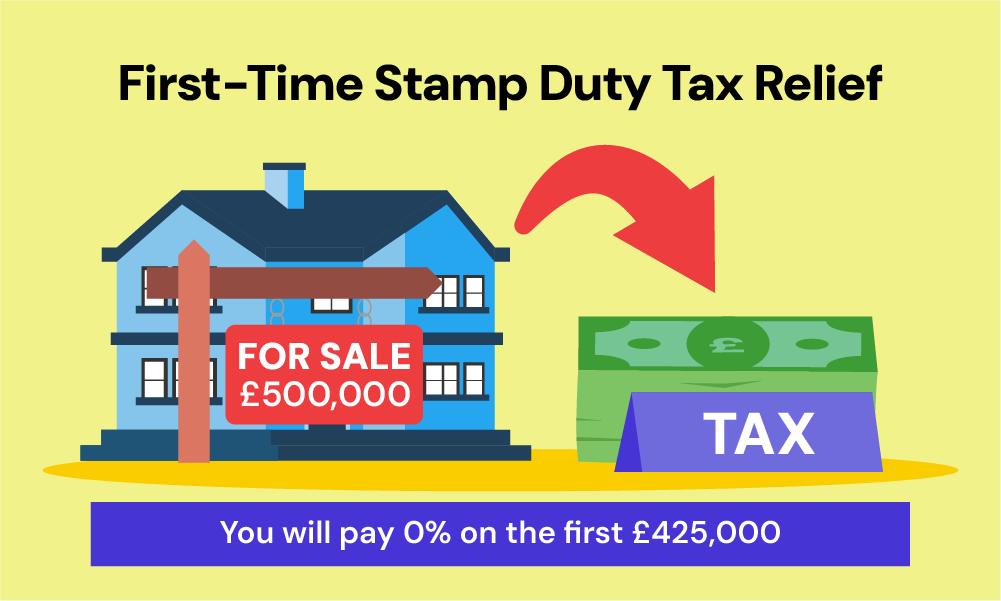

But, there’s a catch—you won’t qualify for first-time buyer stamp duty relief.

This relief can save you thousands when buying properties priced up to £425,000 in England and Northern Ireland.

Starting from 1 April 2025, though, this threshold will drop to £300,000, which means you’ll face higher stamp duty costs on your purchase.

Another challenge is that not all lenders offer buy-to-let mortgages to first-time buyers, so getting approved could be trickier than for seasoned homeowners.

For more guidance, consult a buy-to-let mortgage broker. They may help you find lenders who might accept your application.

Can You Remortgage a Buy To Let?

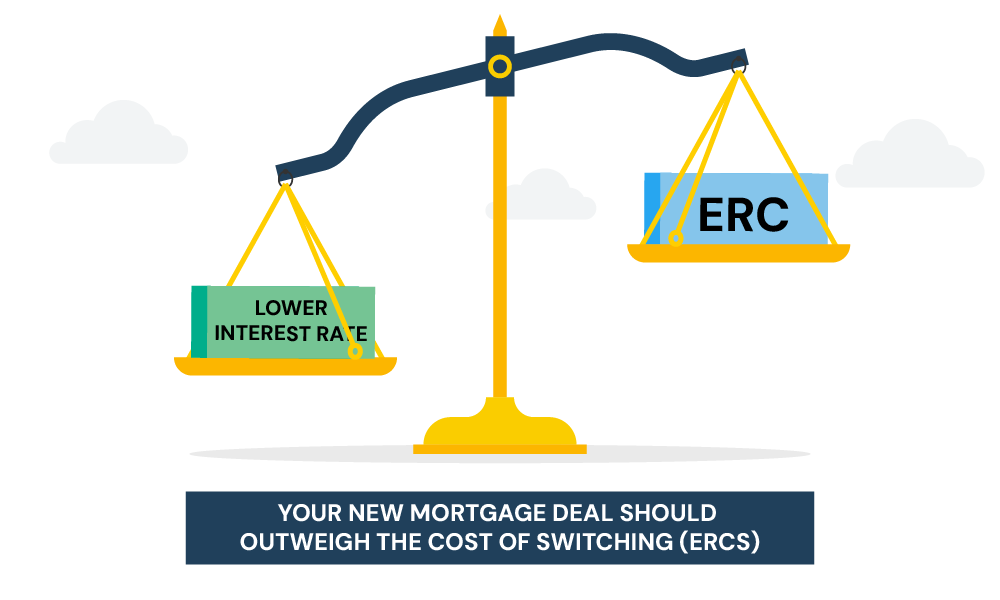

Yes, remortgaging your buy-to-let is an option. While deals might not be as cheap as before, they can still benefit you.

You might get a better interest rate, adjust your mortgage, or get money out of your property for new investments or updates.

But, before you jump in, watch out for any early repayment fees with your current mortgage, as they could be high. Also, look closely at the new mortgage’s terms. Consider the mortgage terms, rates, and other details to see if it fits you better.

Applying for a new mortgage means lenders will review your finances and your property’s rental income to make sure you can afford it and that it’s still a good investment.

Lenders often have stricter requirements for buy-to-let remortgages, like needing more equity in the property and proof that rent covers the mortgage payments well. If remortgaging proves difficult, you might consider selling your buy-to-let property.

What If You Need To Rent Out Your Home Temporarily?

Life can be unpredictable, leading you to move temporarily for various reasons. If selling your home isn’t the right move, renting it out could be your answer.

Consent to Let allows you to rent your property for up to 12 months under your current mortgage. It’s ideal if you’re not typically a landlord but need a temporary solution.

To start, talk to your mortgage lender about your situation. They’ll review your request, but approval isn’t guaranteed. If approved, they may adjust your mortgage terms or interest rate for the short term.

Not all lenders offer Consent to Let, and some may suggest switching to a buy-to-let mortgage for longer rental periods.

As a temporary landlord, you’re responsible for ensuring the property is safe and meets rental legal standards. Also, consider how you’ll manage the property if you’re far away.

Landlord Responsibilities Checklist

As a landlord, you need to make sure your property is ready to rent.

Here’s a checklist of the legal responsibilities you must follow:

- Offer a Safe Environment – Ensure the property is safe and free from health hazards.

- Gas Safety – Have all gas appliances checked yearly by a Gas Safe registered engineer and provide tenants with a safety certificate.

- Electrical Safety – Ensure electrical systems and appliances are safe to use. Electrical safety checks must be done every five years. Your tenants should have a copy of the certificate.

- Fire Safety – Check that all provided furniture is fire-safe and that smoke alarms are installed on every floor. In certain properties, carbon monoxide detectors are also required.

- Provide an Energy Performance Certificate (EPC) – Your property needs a valid EPC before you can rent it out. The current minimum rating is E, but upcoming legislation aims to raise this to C by 2025 for new tenancies, extending to all tenancies by 2028. Failing to meet these standards could lead to significant fines. EPCs are valid for 10 years.

- Protect the Tenant’s Deposit – Place any deposit in a government-approved scheme within 30 days of receiving it. For properties under an assured shorthold tenancy in England and Wales, options include DPS (Deposit Protection Service), TDS (Tenancy Deposit Scheme), or MyDeposits. This safeguards the deposit and outlines how it’s to be handled.

- Right to Rent Checks – Confirm that your tenants have the legal right to rent in the UK.

- Maintenance and Repairs – Keep the structure and exterior of the property in good repair, along with heating, plumbing, and electrical systems.

- Tenancy Agreement – It’s essential to provide a clear, written tenancy agreement. In England and Wales, the Assured Shorthold Tenancy (AST) is most common, defining the legal rights and duties of both you and your tenant. ASTs typically specify whether the tenancy is for a set term or on a rolling basis, granting tenants the legal right to occupy their property for the agreed period.

- Respect Tenant Privacy – Follow the legal process for property access and respect the tenant’s right to quiet enjoyment of the property.

- Handle Evictions Properly – If you need to evict tenants, you must follow the correct legal procedure.

- Provide a ‘How to Rent’ Guide – Give tenants the latest version of the government’s ‘How to Rent’ checklist.

>> More about Landlords’ Responsibilities

Should You Get Buy To Let Mortgages?

Deciding on a buy-to-let mortgage depends on your financial goals and circumstances. Here’s a quick look at the pros and cons:

Pros:

- Potential for long-term capital growth as property values increase.

- Steady income stream from rental payments.

- Rent can cover mortgage repayments and potentially provide profit.

- Property can be a tangible asset compared to stocks or bonds.

Cons

- Requires a significant initial investment for down payment and fees.

- Property value and rental income can fluctuate with the market.

- Being a landlord comes with responsibilities and legal obligations.

- Potential for vacant periods without rental income.

- Additional costs like maintenance, repairs, and property management.

Key Takeaways

- A buy-to-let mortgage is a loan to help you buy a property to rent out. Lenders check the rent you expect to earn, not just your income. You’ll need a larger deposit (20–25%) and pay higher interest rates than regular mortgages.

- To qualify, you must be at least 21 years old, have good credit, and sometimes a personal income of £20,000–£25,000. You’ll also need savings for the deposit and proof the rent will cover 125–145% of the mortgage payments.

- To get a buy-to-let mortgage, find a broker to help you, collect documents like ID and income proof, and let the lender value the property. Once approved, hire a solicitor to handle legal steps and get the property ready for tenants.

- Taxes include a 5% Stamp Duty charge on second homes, Income Tax on rent, Capital Gains Tax if you sell for a profit, and Inheritance Tax if the property’s value exceeds certain limits.

- Pick the right property by looking at location and rental demand. Properties near transport or in popular areas rent out faster. Choose a property that suits your target tenants, and save money for times it might be empty.

- Landlords must keep properties safe, with regular gas and electrical checks and working smoke and carbon monoxide alarms. Protect tenant deposits in approved schemes, provide an Energy Performance Certificate (C rating by 2025 for new rentals), and give tenants a clear agreement of their rights and duties.

The Bottom Line

We’ve covered key points about buy-to-let mortgages, from how to apply and what to watch out for.

Before diving into property investment, always do your homework. Markets change, and what works today might not work tomorrow.

Seek advice from seasoned mortgage brokers. Their insight can save you time and money, and help you avoid common pitfalls.

To get started, reach out to us. We’ll arrange a free, no-obligation consultation with a buy to let mortgage broker to help in your journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I live in my buy to let property?

No, buy-to-let mortgages are for properties you intend to rent out, not live in yourself. If this is your goal, you’ll need to get a residential mortgage designed for that purpose.

Read our first time buyers guide to know more about residential mortgages.

Can I rent out a room in your house with a mortgage in the UK?

It depends on your current mortgage agreement. Some lenders allow lodgers but with restrictions. It’s best to check with your lender first to avoid any complications.

Are buy-to-let mortgages regulated?

Most buy-to-let mortgages are not regulated by the Financial Conduct Authority (FCA) in the UK. This is because they’re considered business loans, where you’re aiming to profit from renting the property.

However, there’s an exception: consumer buy-to-let mortgages. These are mortgages for properties you intend to rent out to close family members (parents, children, siblings, etc.). Because it’s similar to a regular residential mortgage, the FCA regulates consumer buy-to-let mortgages for your protection.

When did buy to let mortgages start in England?

Buy-to-let mortgages have been around since 1996. They were created to make life easier for landlords, giving them a specific way to borrow money for buying properties to rent out.

How old do you have to be to get a buy-to-let mortgage in the UK?

The minimum age to apply for a buy-to-let mortgage is usually 18, but most lenders prefer you to be at least 21 or even 25.

They also have an upper age limit, often around 70 or 75, by the time the mortgage ends.

What percentage of UK mortgages are buy-to-let?

Buy-to-let mortgages make up about 12-15% of all mortgages in the UK. This number can change depending on things like the economy, property trends, and government rules for landlords.

What is the meaning of let to buy?

Let-to-buy is a clever move where you rent out your current home to tenants and use that rental income to help pay for a new home. It’s a handy option if you’re moving but don’t want to sell your old place – you get to keep it and become a landlord at the same time.

Related Articles

Can You Buy A House Through Your Business?

Many British property investors are looking at a new strategy: buying houses through limited companies. While this approach offers potential tax advantages, it’s not for everyone. Let’s explore the pros and cons of using your business to buy a house in the UK. Can You Actually Live in a House Owned By Your Company? Living […]

Free Rental Yield Property Calculator

Becoming a landlord can be an exciting prospect. You get a steady stream of income, potential for property value growth, and you own a tangible asset. But, owning a property investment also comes with its challenges. You must consider factors such as rental rates, vacancy periods, and maintenance costs. Without a clear picture of your […]

Changing Your Buy To Let To Residential Mortgage

Life can take unexpected turns. Maybe you’re facing a breakup, a new job in another city, the kids needing their own space, or you’re simply looking to downsize. In any of these cases, moving into your buy-to-let might seem like a good move. But hold on! There are key rules: If you switch from renting […]