- What is the Bank of England’s Base Rate?

- How The Base Rate Affects Your Money

- How The MPC Sets The Base Rate

- How Does the Base Rate Affect Your Mortgage?

- Should You Remortgage To A Fixed Term Deal Now?

- Will Base Rate Changes Affect My Mortgage Application?

- The History of UK Base Rates Over The Years

- How Often Does the Base Rate Change?

- Key Takeaways

- The Bottom Line

A Definitive Guide To Bank Of England’s Base Rates In 2025

Interest rates are fees for borrowing or rewards for saving.

They affect your money, from how fast your savings grow to how much you pay on your mortgage. They even impact the whole economy.

The Bank of England plays a central role in setting interest rates, and this guide will explore how this impacts your finances and the UK economy through its base rate.

What is the Bank of England’s Base Rate?

The Bank of England base rate is the UK’s key interest rate, set by the Monetary Policy Committee (MPC). It’s a powerful tool to control inflation and promote economic stability.

Right now, the base rate is 4.5%. If this changes, it can affect many other interest rates in the UK.

Commercial banks and lenders often adjust their rates for lending and saving based on this rate. As a result, changes in the base rate can impact financial products like mortgages and loans available to you.

How The Base Rate Affects Your Money

The base rate change has a direct impact on your finances. This rate influences the interest rates on mortgages, loans, and savings accounts. Here’s how:

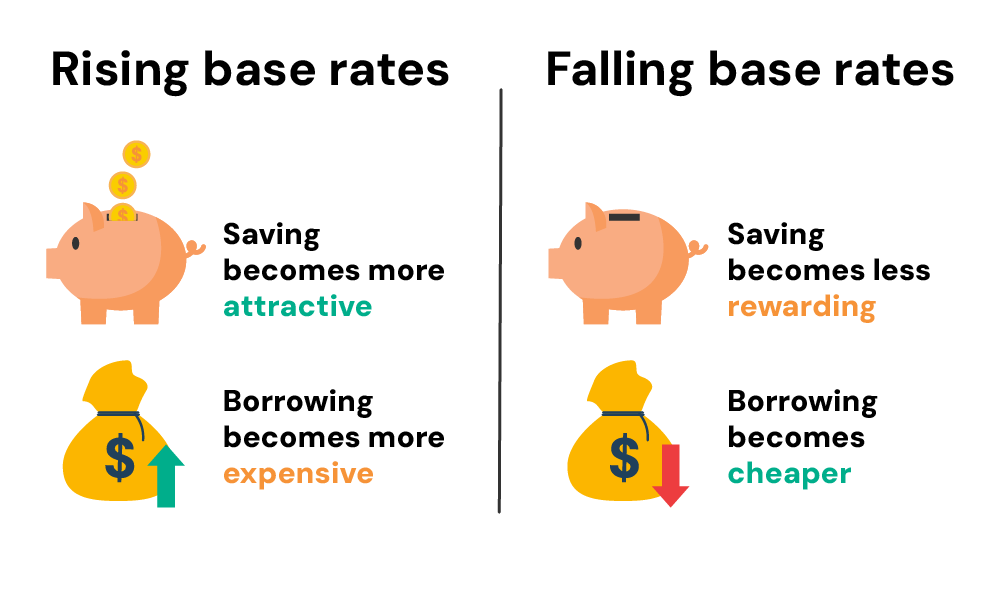

Rising base rates 📈

- Saving becomes more attractive. Banks offer you better interest rates on your savings accounts.

- Borrowing becomes more expensive. Mortgages and loans come with higher interest rates, potentially leading to less spending.

Falling base rates 📉

- Borrowing becomes cheaper. Loans and mortgages have lower interest rates, making it easier to borrow money.

- Saving becomes less rewarding. You earn less interest on your savings, potentially leading to more spending.

Note though that, base rates aren’t the only player.

Banks can consider their own costs and need to balance savings and loan rates. Other economic factors also influence interest rates beyond the base rate.

How The MPC Sets The Base Rate

The MPC meets every 6 weeks to set the base rates.

They have one BIG goal: to keep inflation low and stable and hit the, aiming for a government-set target of around 2%.

Here’s how they decide:

- Inflation – If prices rise too quickly (above the 2% target), the MPC raises the base rate to slow down spending and cool things down. Conversely, if inflation is low, they might cut the base rate to encourage borrowing and boost the economy.

- Economic Growth – A booming economy might prompt the MPC to raise the base rate to prevent overheating. Conversely, sluggish growth could lead to a rate cut to stimulate activity.

- Jobs – A strong job market, with more people earning and spending, can influence the MPC to raise rates. On the other hand, high unemployment might lead to a rate cut to encourage hiring.

- People’s Finances – The MPC considers how much people earn, spend, and feel about their finances, as it affects overall economic activity.

- Global Economy – Since international events can impact the UK’s economy, the MPC takes those into account as well.

The MPC considers all these factors and then decides to raise, lower, or hold the base rate. This decision helps keep the UK’s economy stable.

So, the next time you hear about a base rate change, you’ll know the MPC is just trying to keep things running smoothly for the UK. 👍

Clearing the Jargon: Inflation and Recession

- Inflation means prices go up over time, so your money buys less. Imagine a loaf of bread costs £1 today, but £1.10 next year. That’s inflation.

- Recession is when the economy slows down a lot. During this, businesses produce less, people spend less and unemployment often rises.

To fight a recession, the BoE might cut the base rate to encourage borrowing and spending, which can get the economy going again.

How Does the Base Rate Affect Your Mortgage?

As we’ve talked about, base rates can affect your mortgage repayments in a couple of ways. It can influence how much you pay each month and the total cost of your mortgage overall.

Let’s break down how this works for you.

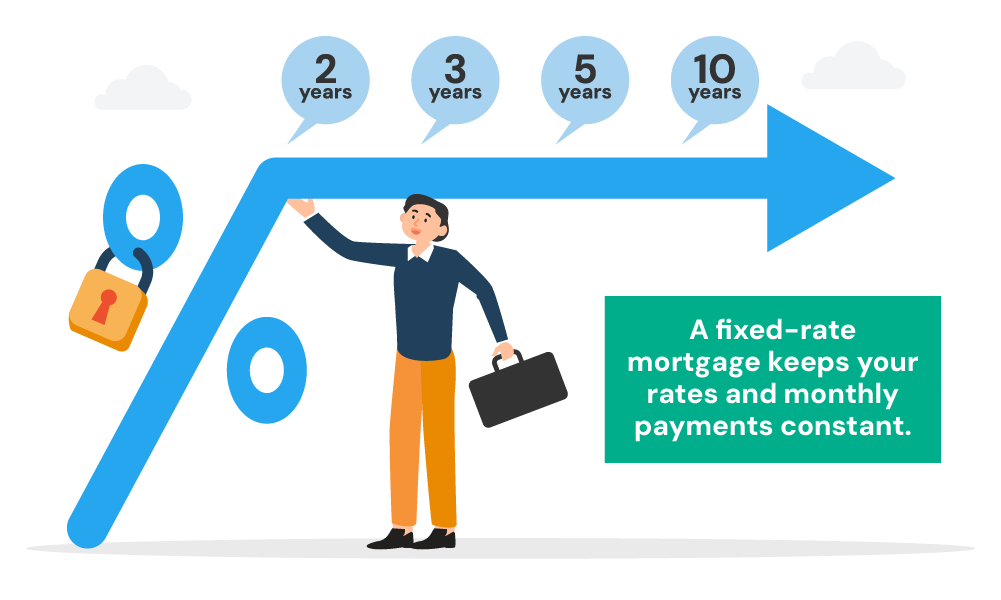

Fixed Rate Mortgages

Your monthly payments are locked in for a set term, typically 2, 5, or 10 years.

This means no matter what happens to interest rates in general, your payment stays the same.

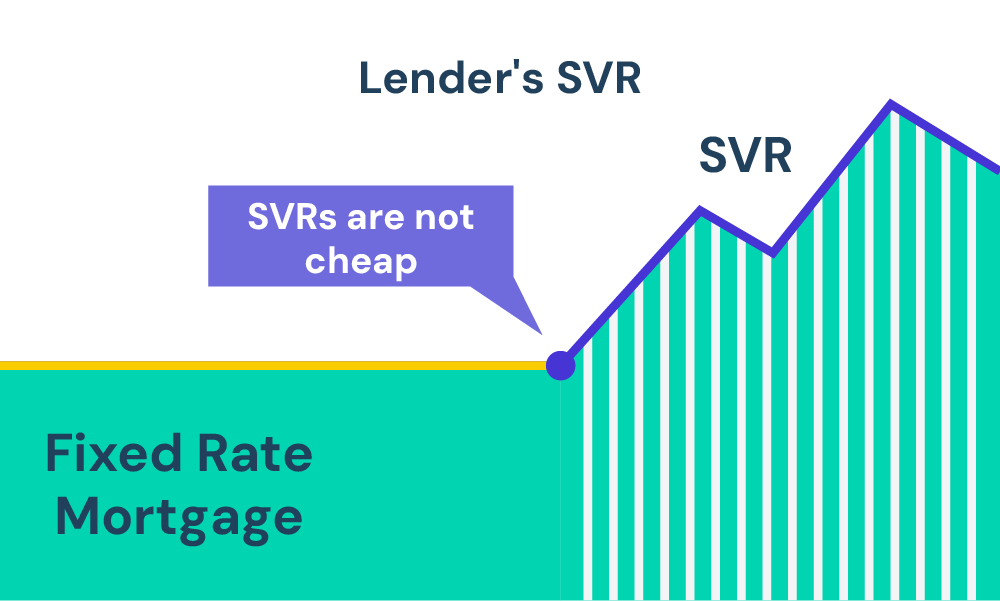

Once your fix ends, your lender will switch you to a different rate–called Standard Variable Rate (SVR). These are often more expensive deals advertised for new mortgages.

So before your fixed-rate deal ends, it’s best to look for new deals to remortgage and get a LOWER rate.

This keeps you away from overpaying your mortgage.

Remember, fixed rates are great when base rates are low. You lock in that good rate and avoid any nasty surprises later.

However, don’t forget: if base rates fall while you’re fixed, you won’t see those savings in your monthly payments.

Tracker Rate Mortgages

As the name suggests, these mortgages follow the BoE’s base rate. This means your mortgage interest rate goes up or down along with the base rate.

For example, your mortgage rate could be set at 1% above the base rate. So, if the base rate is 4.50%, your mortgage rate would be 5.50%.

Tracker mortgages are transparent and keep you aligned with what’s happening in the market. However, it’s important to factor in potential rate rises when you’re budgeting for your monthly payments.

This way, you’ll be prepared if your payments increase.

Standard Variable Rate Mortgages (SVRs)

Unlike tracker mortgages, SVRs aren’t directly tied to the Bank of England’s base rate. Instead, your lender sets the rate, but it often moves in the same direction as the base rate.

Let’s say your fixed-rate deal ends, and you land on the lender’s SVR. If the base rate goes up, your lender might raise their SVR by a smaller amount, say 0.25%. This could push your mortgage rate from 8% to 8.25%.

On a £200,000 mortgage, this increase could bump your monthly payment from £1,330 to £1,360.

While SVR hikes might not perfectly match base rate rises, you’re still likely to see your payments go up.

Remember: This is just an example to show how SVR changes can affect your payments. Your specific situation might be different.

Discount Rate Mortgages

Discount mortgages give you a temporary reduction on your lender’s standard variable rate (SVR).

For instance, if the SVR is 4.50% and you get a 1% discount, you’ll initially pay a lower rate of 3.50%.

The drawback is that these mortgages aren’t fixed. Their rates can change along with the SVR, so your monthly payments could go up or down.

Therefore, it’s important to consider how stable the SVR is and the size of the discount you’re offered before choosing this type of mortgage.

Capped Rates Mortgages

This mortgage type offers the best of both worlds: some flexibility and some protection.

They track your lender’s standard variable rate (SVR), but unlike a regular SVR, they have a ceiling.

This means your rate can go down if the SVR falls, but it can’t rise above the cap you agreed on upfront, even if the SVR skyrockets.

While capped mortgages shield you from sharp rate increases, they do come at a cost. They’re usually MORE expensive than regular SVRs.

There’s also another catch sometimes called a “collar.” This sets a minimum rate for your mortgage, so even if the SVR plunges, your rate won’t go any lower.

Should You Remortgage To A Fixed Term Deal Now?

It depends.

If your current mortgage term is ending soon, or you’re on a variable rate, remortgaging to fixed could be a smart move.

With interest rates and living costs on the rise, a fixed-rate mortgage offers stability. Your monthly payments stay the same for the entire term, making it easier to budget during these economic ups and downs.

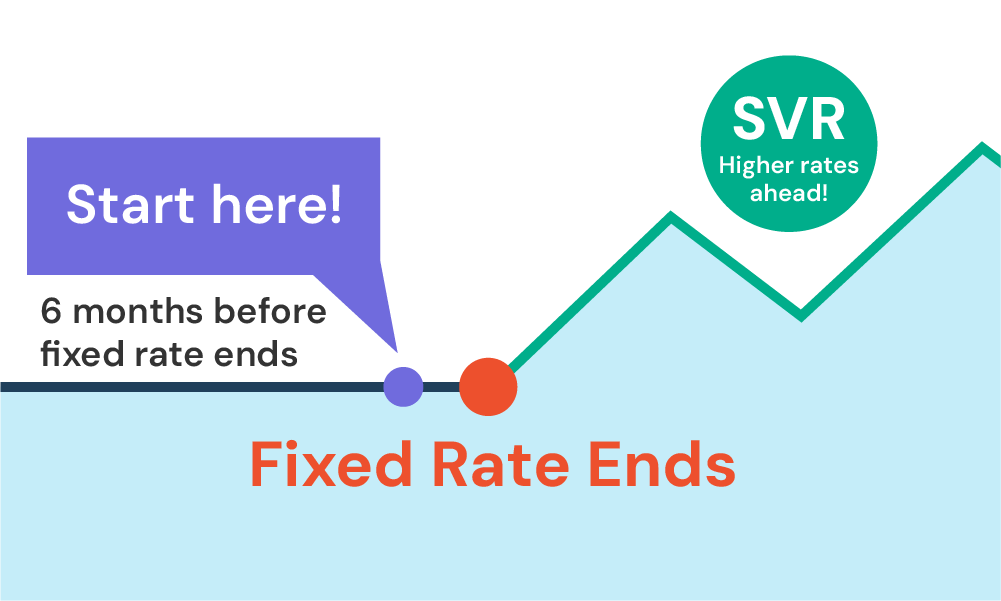

To lock in a good rate before potential future increases, start exploring remortgaging options 3-6 months before your current deal ends.

The initial fees might be worth it for the long-term savings you could see on your mortgage.

Will Base Rate Changes Affect My Mortgage Application?

Base rate changes can definitely impact your mortgage application. Here’s why:

- The base rate influences the interest rates lenders offer on mortgages.

- Most lenders can adjust their rates anytime before final approval.

So, if the base rate fluctuates while you’re applying, the interest rate on your application could change as well.

The good news is there’s a point where your rate gets locked in. This timing varies by lender – for some it’s the agreement in principle, for others it’s the full application.

Feeling unsure about how base rate changes might affect your ability to afford the mortgage? Chat with a mortgage broker. They can explain how stable your offered rate is and recommend lenders known for consistent rates.

Remember, being informed is key when making mortgage decisions.

The History of UK Base Rates Over The Years

The UK’s base rate has a long and interesting history, reflecting the country’s economic ups and downs.

Here’s a look at some key changes in the base rate since 1996:

| Date Changed | Base Rate(%) |

|---|---|

| 8/3/2023 | 5.25 |

| 6/22/2023 | 5 |

| 5/11/2023 | 4.5 |

| 3/23/2023 | 4.25 |

| 2/2/2023 | 4 |

| 12/15/2022 | 3.5 |

| 11/3/2022 | 3 |

| 9/22/2022 | 2.25 |

| 8/4/2022 | 1.75 |

| 6/16/2022 | 1.25 |

| 5/5/2022 | 1 |

| 3/17/2022 | 0.75 |

| 2/3/2022 | 0.5 |

| 12/16/2021 | 0.25 |

| 3/19/2020 | 0.1 |

| 3/11/2020 | 0.25 |

| 8/2/2018 | 0.75 |

| 11/2/2017 | 0.5 |

| 8/4/2016 | 0.25 |

| 3/5/2009 | 0.5 |

| 2/5/2009 | 1 |

| 1/8/2009 | 1.5 |

| 12/4/2008 | 2 |

| 11/6/2008 | 3 |

| 10/8/2008 | 4.5 |

| 4/10/2008 | 5 |

| 2/7/2008 | 5.25 |

| 12/6/2007 | 5.5 |

| 7/5/2007 | 5.75 |

| 5/10/2007 | 5.5 |

| 1/11/2007 | 5.25 |

| 11/9/2006 | 5 |

| 8/3/2006 | 4.75 |

| 8/4/2005 | 4.5 |

| 8/5/2004 | 4.75 |

| 6/10/2004 | 4.5 |

| 5/6/2004 | 4.25 |

| 2/5/2004 | 4 |

| 11/6/2003 | 3.75 |

| 7/10/2003 | 3.5 |

| 2/6/2003 | 3.75 |

| 11/8/2001 | 4 |

| 10/4/2001 | 4.5 |

| 9/18/2001 | 4.75 |

| 8/2/2001 | 5 |

| 5/10/2001 | 5.25 |

| 4/5/2001 | 5.5 |

| 2/8/2001 | 5.75 |

| 2/10/2000 | 6 |

| 1/13/2000 | 5.75 |

| 11/4/1999 | 5.5 |

| 9/8/1999 | 5.25 |

| 6/10/1999 | 5 |

| 4/8/1999 | 5.25 |

| 2/4/1999 | 5.5 |

| 1/7/1999 | 6 |

| 12/10/1998 | 6.25 |

| 11/5/1998 | 6.75 |

| 10/8/1998 | 7.25 |

| 6/4/1998 | 7.5 |

| 11/6/1997 | 7.25 |

| 8/7/1997 | 7 |

| 7/10/1997 | 6.75 |

| 6/6/1997 | 6.5 |

| 5/6/1997 | 6.25 |

| 10/30/1996 | 5.94 |

| 6/6/1996 | 5.69 |

| 3/8/1996 | 5.94 |

| 1/18/1996 | 6.13 |

These figures reveal the base rate’s rollercoaster ride. The Bank of England adjusts it depending on what’s happening in the world.

These changes impact borrowing costs and savings rates, affecting the whole economy.

How Often Does the Base Rate Change?

The BoE keeps a close eye on the economy and adjusts the base rate around 8 times a year through their MPC.

While predicting these changes can be a guessing game, the Bank tries to give us a heads-up on what to expect, which can be helpful for your financial plans.

In emergencies like the 2008 financial crisis, they can even hold emergency meetings to adjust the base rate quickly.

To be prepared, keep an eye on the upcoming meetings here.

Key Takeaways

- The Bank of England’s base rate, now 4.5%, affects how much interest you pay on loans and mortgages and how much you earn on savings.

- Higher base rates mean saving is more rewarding, but borrowing costs more; lower rates do the opposite.

- The Monetary Policy Committee (MPC) sets the base rate every 6 weeks to keep prices stable and the economy steady.

- Base rate changes have a knock-on effect on mortgages. Tracker mortgages follow the base rate closely, while fixed-rate and SVR mortgages aren’t as directly tied.

The Bottom Line

To sum it up, the base rate matters! 🙂 It can affect your mortgage payments and savings rates.

So, stay informed–check the news and BoE updates to understand what’s happening in the market. In this way, you make smarter financial decisions.

Building financial resilience is also key. Plan your budget carefully and save where possible.

If you’re looking at mortgages, consider your needs.

A fixed-rate mortgage offers stability if rates rise, while a variable rate might be better if they fall. Choose what suits you best.

And for BIG decisions like mortgages, professional advice is recommended. A good mortgage advisor can explain your options and give personalised tips.

To save time finding an advisor, contact us. We’ll connect you with a qualified FCA mortgage broker to solve your specific mortgage situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can the base rate go negative?

The Bank of England hasn’t ruled out negative base rates, though it’s never happened in the UK.

This would mean lenders wouldn’t charge interest to borrow money. However, things wouldn’t be quite as simple as free loans or mortgages.

Even with a negative base rate, banks likely wouldn’t offer loans or mortgages without any interest.

Borrowing might get cheaper, but don’t expect zero or negative rates just yet. Similarly, your savings accounts might not be charged, but the interest earned could be very low.

The main purpose of a negative base rate is to boost the economy by encouraging people to borrow and spend more. But the actual impact on everyday things like loans, mortgages, and savings might be smaller and more complex than you might think.

How does the base rate affect my savings?

For your savings, a higher base rate means you earn more interest on your savings accounts.

Imagine you have £10,000 saved with a bank offering 2% interest above the base rate. At the current rate, you’d earn £725 a year.

If the base rate drops to 0.75% and your bank adjusts its savings rate accordingly, your annual earnings would fall to £675.

It’s like getting a bigger reward for keeping your money saved, but with low base rates, that reward shrinks.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Tracker Mortgages Rates: Everything You Need to Know

Is your mortgage holding you back from saving money? Maybe you’re a first time buyer, planning to move soon, or a homeowner expecting interest rates to dip. A tracker mortgage might be perfect for you. This mortgage offers you more flexibility than a fixed-rate mortgage. But, like with any financial product, you want to make […]

What You Need to Know About Specialist Mortgage Lenders

When it comes to finding the right mortgage lender, not everyone fits into the standard high street lending rules. If you’re self-employed, have bad credit, or need a more customised mortgage, it can feel frustrating when your bank says “no.” But don’t worry – specialist mortgage lenders can help. These lenders focus on people who […]

Mortgage Valuation Types & Fees: What Should You Expect?

Wondering how much the property you want to buy is really worth? A mortgage valuation helps both you and your lender figure that out. But not all valuations are the same, and costs can vary. Knowing which type of valuation fits your situation can save you time and money during the mortgage process. In this […]