- What Are Second and Third Charge Bridging Loans?

- How Do They Compare to First Charge Loans?

- How Can You Use a Second Charge Bridge Loan?

- Eligibility Criteria

- How to Successfully Apply for a Second or Third Charge Bridge Loan

- Is a Second Charge Bridging Loan Regulated in the UK?

- Which Lenders Offer These Loans?

- How Much Can You Borrow with a Second Charge Bridging Loan?

- The Bottom Line

Second and Third Charge Bridging Finance Explained

When cash flow gets tight and traditional loans aren’t cutting it, you don’t have to hit the panic button. Second or third charge bridging loans can be your financial lifeline.

Now, you might be thinking, “That sounds great, but what’s the catch?”

Well, there are a few nuances you should be aware of, like varying interest rates and eligibility criteria that can make or break your loan application.

But fear not, we’re here to clear the fog.

In this guide, you’ll discover what these loans are, why they could be the right fit for you, and how they differ from your typical first charge loans.

What Are Second and Third Charge Bridging Loans?

Picture this: you already have a mortgage on your home, and now you need extra funds for a renovation or investment.

A second charge bridging loan lets you access more money using the same property as collateral. However, the lender of this loan stands second in line with your original mortgage lender when it comes to repayment.

Similarly, a third charge bridging loan comes into play when you’ve already got two loans against an asset like a home.

This new lender will be third in the repayment hierarchy. The risks are higher, the terms stricter, and your chances of getting approved are slimmer, but it’s not impossible.

Both types of loans offer a lot of versatility, generally have short terms (often around a year), and might not even require monthly payments.

How Do They Compare to First Charge Loans?

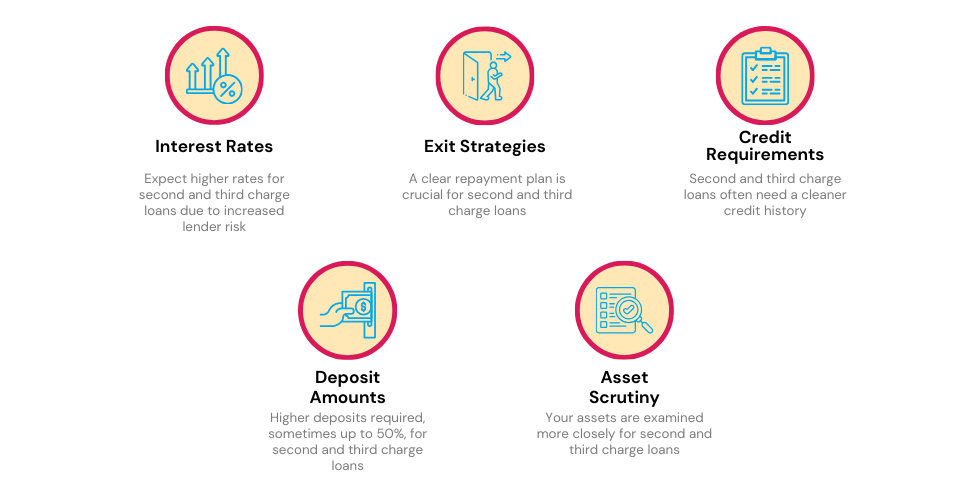

Interest Rates

First off, you’ll notice that the interest rates are higher for second and third charge loans. This is because the lender is taking on more risk, standing behind one or two other loans in case of default.

Exit Strategies

When applying for a first charge loan, often a mortgage, you generally don’t need an elaborate exit strategy.

But for a second or third charge loan, you’ll need a clear plan to repay the loan when its term ends, be it through remortgaging, inheritance, or investments.

Credit Requirements

First charge loans might be more forgiving on your credit score, but second and third charge loans usually require a cleaner credit history. Any credit hiccups could jeopardise your repayment plan, making you a higher-risk candidate.

Deposit Amounts

You might secure a first charge loan with a 25% deposit, but for second and third charge loans, you’re looking at a steeper requirement, sometimes as high as 40-50%.

Asset Scrutiny

The quality of your assets will be more closely examined in second and third charge loans. The more liquid or valuable the asset, the more favourable terms you could negotiate.

How Can You Use a Second Charge Bridge Loan?

Just like other bridge loans, a second charge bridge loan offers you a ton of flexibility. Whether you’re in a rush to buy property or need funds for your business, this type of loan can be a lifesaver.

Here’s a quick rundown of what you can do with it:

Buying Property

You can use a second charge bridge loan to snag a new property. The loan will be paid off through the sale of your current property.

You can use this loan for buying different types of properties like houses to rent out, HMOs, or even commercial buildings.

Upgrading Property

If you have an old property that needs a makeover, a second charge bridge loan can fund small or big renovations. You get the money you need based on the value of your property.

Business Boost

If you own a business, a second charge bridge loan can be a life-saver. Use it to settle your tax bill, expand your workspace, or even fund a deposit for a new purchase. It’s a quick way to get your hands on cash for business needs.

Eligibility Criteria

To take advantage of the above uses, you need to meet certain criteria. Here’s what you should know:

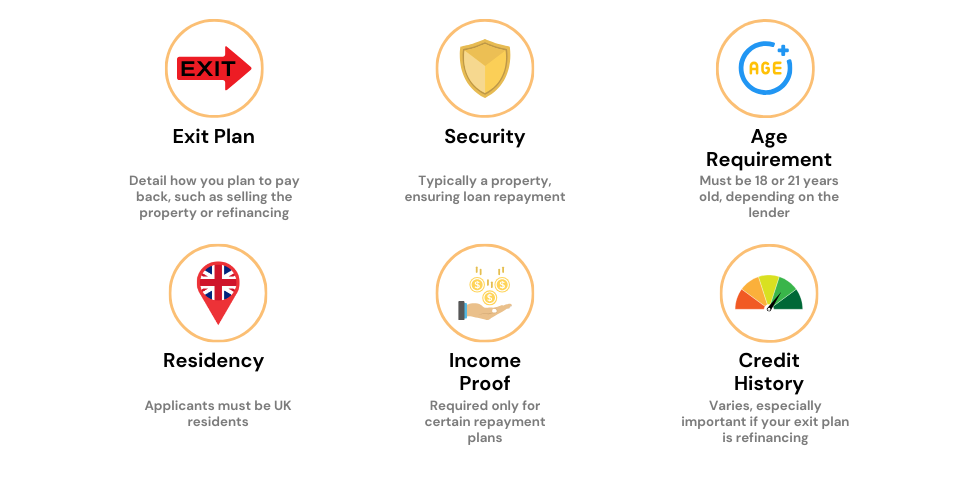

- Owning a property is non-negotiable as the loan is secured against it.

- You need to be at least 18 or 21, depending on the lender’s policy.

- Sufficient equity in your property is essential, as it serves as collateral.

- A consistent income source ensures you can keep up with repayments.

- Your credit score plays a role in the terms and rates you’ll get.

- An exit strategy is a must, indicating how you intend to pay off the loan.

Note: Lenders may have additional requirements, so treat these as general guidelines rather than hard rules.

How to Successfully Apply for a Second or Third Charge Bridge Loan

Applying for a second or third charge bridge loan can be a bit tricky, but don’t worry. Here’s a handy guide to help you navigate the application process.

Speak to a Broker Early On

You might consider speaking to a broker as a last resort, but consulting one at the outset is actually a smart move.

Brokers are experts in the lending industry. They understand the nuances of various lenders’ requirements and can give you a game plan for your loan application. Talking to a broker early can save you both time and money.

Here’s how a broker can assist you:

- Organise Your Finances – Get a grasp on your financial situation by reviewing your assets, debts, and how much you can afford to borrow.

- Gather Your Paperwork – Be ready with important documents like your ID, proof of address, and bank statements, as you’ll need these for any lender.

- Craft Your Exit Strategy – An exit strategy outlines how you intend to repay the loan, be it through the sale of property or another avenue.

- Identify Suitable Lenders – Brokers can match you with lenders that align with your financial status and needs.

- Understand Interest Rates and Fees – Get the low-down on the costs associated with your loan to avoid any surprises.

- Clarify Eligibility Criteria – Know exactly what lenders are looking for to improve your chances of approval.

- Suggest Loan Amounts – Based on your financial assessment, a broker can guide you on how much you should aim to borrow.

Pro Tip: Watch for Red Flags

As you gather your information, keep an eye out for potential issues, like a low credit score or insufficient deposit. Your broker can help you identify and address these red flags to improve your application.

Before you proceed with your loan application, it’s essential to fully understand all the legal and financial details. This is a good time to consult with your broker, and even legal advisors if needed, to make sure you’re well-informed.

Once you feel confident about the details, schedule a final consultation with your broker. In this meeting, they can review all your prepared materials and guide you towards lenders who are likely to approve your application.

If you’re looking for expert guidance, don’t hesitate to get in touch. We can connect you with experienced bridging finance advisors who can help you every step of the way.

Is a Second Charge Bridging Loan Regulated in the UK?

If you’re getting a second charge bridging loan for a residential property where you or a family member will live, know that the Financial Conduct Authority (FCA) regulates it. The FCA ensures that lenders follow strict guidelines and assess whether the loan is suitable and affordable for you.

But what if you’re investing in property for business? In that case, the loan is unregulated by the FCA. Don’t fret; unregulated doesn’t mean risky. These loans follow different rules tailored for non-residential properties.

Which Lenders Offer These Loans?

If you’re in the market for a second or third charge bridging loan, there are several lenders to consider, such as Clifton PF, Market Financial Solutions (MFS), MT Finance, Precise Mortgages, and West One Loans. Keep in mind that this list isn’t exhaustive.

Since the bridging loan market is smaller than that for mortgages, you’ll find other providers as well. Consult a broker for tailored advice on which lenders best suit your needs based on rates and eligibility criteria.

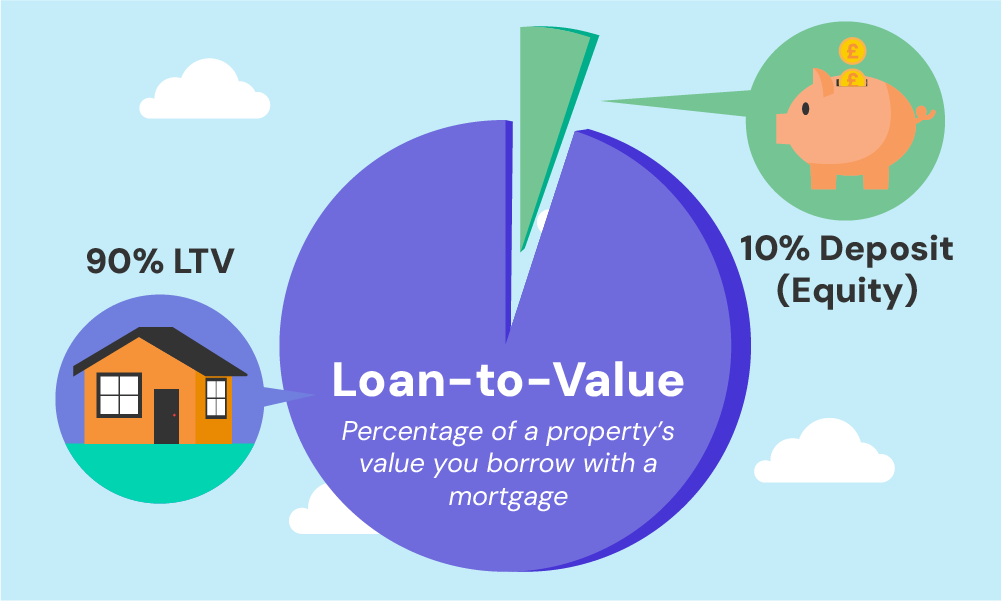

How Much Can You Borrow with a Second Charge Bridging Loan?

These loans usually start at £50,000, but there’s no fixed upper limit. However, it’s not a one-size-fits-all scenario. The amount you can borrow hinges on the equity in your property and the lender’s specific criteria.

In terms of Loan-to-Value (LTV), you could secure up to 80% of your property’s value. Even better, if you’ve got other assets, you might borrow more.

But let’s not forget that bridging loans can be costly. They come with higher interest rates and additional fees compared to regular loans like mortgages.

Plus, you’ll be juggling mortgage payments alongside the bridging loan repayments. Your credit history and ability to repay will also play into how much you can borrow.

Curious about the potential costs? Check out our bridge loan calculator to get an idea of the overall expense.

The Bottom Line

Getting second and third-charge bridging loans can be challenging. Different lenders have their own sets of rules and rates, making it tough to know where to start.

Here’s your takeaway: these loans are complex but they offer a financial solution when you need quick, additional funding. Knowing the ins and outs can save you money and stress.

Bridging loan advisors are experts who can simplify this for you. They’re adept at matching you with lenders that meet your financial criteria, and can even help you find more favourable terms. In essence, they’re your shortcut to making an informed decision that saves you both time and money.

Want to learn more? Just fill out this quick form. We’ll arrange for a specialised advisor to contact you for a free, no-obligation chat.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I use remortgaging to settle a second charge bridge loan?

Yes, you can opt for remortgaging to pay off a second charge bridge loan. You might switch to a new lender or choose a better mortgage option from your current one. However, lenders will assess your ability to repay over the loan term. For these intricate scenarios, consulting an advisor is a smart move.

Can a second charge loan be denied by a lender?

A lender can turn down your application for reasons like unaffordability or your inability to repay. If your property’s value doesn’t meet the lender’s loan criteria, that can also lead to a refusal.

Is it possible to have more than one second charge bridge loan?

Although possible, having multiple loans against your property is risky. It could harm your credit score and borrowing potential in the future. Consult an expert for personalised advice on this matter.

What's the interest rate for a second charge bridge loan?

Interest rates for bridge loans are usually higher than regular mortgages due to their short-term nature. Rates differ among lenders, and having a first charge loan doesn’t necessarily impact the interest rate for a second charge.

Do I need approval from my first charge lender for a second charge?

Yes, you need consent from your original lender to be eligible for a second charge loan on the same property.

How long does it take to finalise a second charge bridging loan?

Typically, it takes between 5 to 14 days to finish the second charge bridging loan process, provided the first charge lender gives consent. Delays from the first charge lender are common and can extend the process. So, it’s wise to seek their consent early on.

Can I get second charge loans even with poor credit?

While bridging finance lenders are generally more lenient, not all are open to offering second charge loans to those with bad credit. The market options can be limited, especially if your exit strategy involves refinancing. Despite these challenges, in many situations, loans can still be extended to those with a poor credit history.

Related Articles

An In-Depth Guide To Secured and Unsecured Bridging Loans

If you’re in the UK and planning a big move—maybe you’ve found your dream home or you’re eyeing a property investment—you’ve got some financial decisions to make. One of them is choosing between a secured and an unsecured loan. Why does this choice matter? The loan you choose impacts your interest rate, borrowing limit, required […]

Fast Bridging Loans: How to Apply and What You Need?

Imagine you’ve spotted the perfect property investment—fantastic location, huge potential, and it’s a steal. There’s just one hitch: your assets are tied up, and the clock is TICKING. You’ve been down this road before—missing out because the cash wasn’t there when you needed it. But what if there was a way to make your assets […]

Large Bridging Loans: Quick Cash for High-Value Properties

If you’re considering a big financial step and need quick access to a substantial amount of money. Large bridging loans might be your answer. However, let’s be clear: This is big money we’re talking about. Taking out such a loan is a serious commitment. In this guide, we’ll break down what large bridging loans are, […]