What Is Classed As A First Time Buyer In The UK?

Buying a home is both exciting and daunting, especially if it’s not your first rodeo. The rules around who qualifies as a true “first-time buyer” can be confusing.

Getting this wrong could cost you valuable money through missed tax reliefs and prime mortgage deals.

Whether you’re just stepping onto the property ladder or boomeranging back after a break, it’s crucial to understand your status.

This guide will clarify if you still retain your first-time buyer privileges or if you’re officially a well-seasoned homeowner.

We’ll break down the official definitions, explore loopholes that could work in your favor, and provide tips on making the most of your circumstances.

By the end, you’ll be an expert on first-time buyer classifications and ready to approach lenders with clarity and confidence.

Who Classifies as a First-Time Buyer?

A first-time buyer is someone who has never owned or held a major interest in a residential property or land, anywhere in the world. This includes any form of ownership, whether outright, shared, or inherited.

Essentially, if you’ve never had your name on the title deeds of a residential property, you’re classed as a first-time buyer.

To be classed as a first-time buyer, you must meet specific criteria:

- You have never owned a residential property, either in the UK or abroad.

- You have never had a major interest in a residential property.

- You have never inherited a residential property.

- You are not buying with someone who has previously owned a residential property.

What Are the Benefits for First Time Buyers?

First-time buyers in the UK can enjoy several benefits:

- Stamp Duty Land Tax (SDLT) relief on properties up to £425,000.

- Access to government schemes like First Homes and Lifetime ISAs.

- Special mortgage deals, including lower interest rates and lower deposit requirements.

Can You Be a First Time Buyer Twice?

Unfortunately, you cannot technically be a first-time buyer twice. Once you’ve owned a property, you lose the first-time buyer status permanently.

This applies even if you sold the property years ago. Lenders and the government will still classify you as a homemover or previous homeowner.

However, some lenders may offer similar benefits to first-time buyers under specific conditions.

What Are The Exceptions?

While you can’t technically be a first-time buyer again, some lenders may treat you as one if you haven’t owned a home for at least 3 years or you are no longer a homeowner due to divorce or separation.

This could make you eligible for their first-time buyer mortgage deals, which often come with incentives like cashback or free legal services.

However, you still won’t qualify for the first-time buyer Stamp Duty exemption, as you’ve previously owned property.

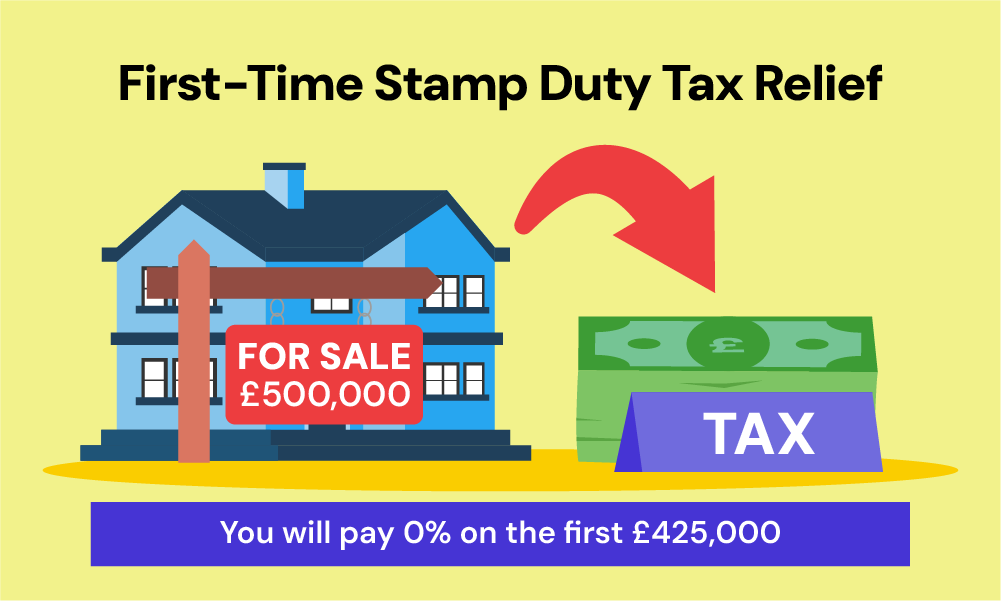

To provide further clarity, here is a breakdown of the first time buyers SDLT rates for different property purchase prices:

| Property Purchase Price | SDLT rate |

|---|---|

| £0 to £425,000 | Zero |

| £425,001 to £625,000 | 5% |

For instance, say you buy a property for £500,000, you will pay 0% on the first £425,000 and 5% on the remaining £75,000, resulting in £3,750 SDLT.

And you can only claim this tax benefit if you’re classed as a first time buyer in the UK. 🤓

The only exception to this would be if you purchase a property under £250,000, where all buyers are exempt from SDLT.

Does It Matter If You Had a Mortgage Before?

Yes, having held a mortgage in the past usually means you were on the property’s title deeds, and lenders will consider you a previous homeowner.

It doesn’t matter if you’ve since been removed from that mortgage and the deeds – you’ll still be classed as a homemover – you don’t qualify for SDLT relief, but you can still access other mortgage deals and government schemes.

Can First-Timers and Second-Timers Buy Together?

Yes, you can. A first-time buyer can take out a joint mortgage with someone who has owned a home before. However, as a couple, you won’t be eligible for the first-time buyer Stamp Duty exemption.

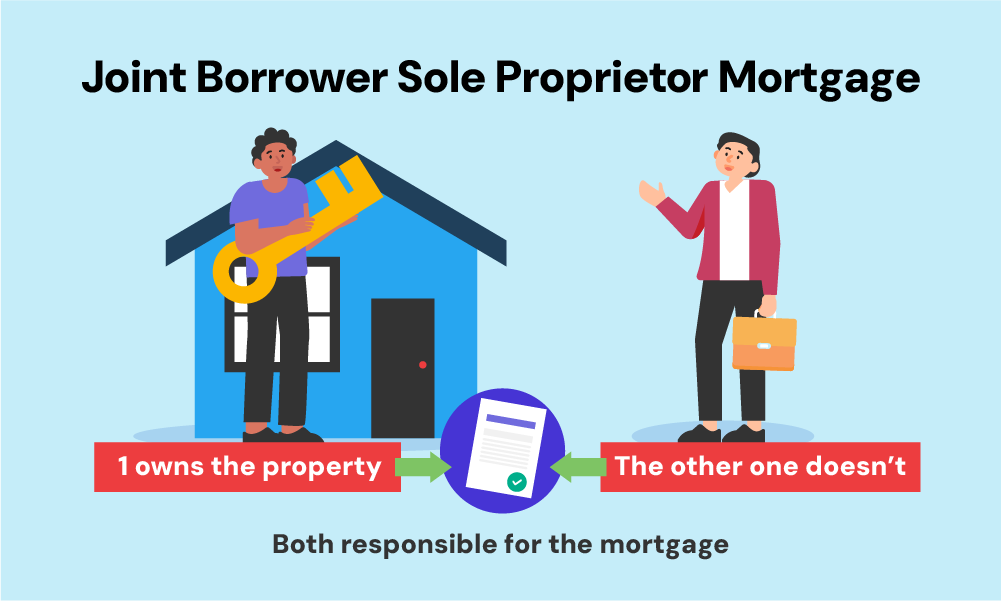

There’s a clever solution though: a joint borrower sole proprietor (JBSP) mortgage.

This lets up to four people chip in for the mortgage, but only one person gets their name on the deeds. Everyone shares responsibility for repayments, but only the first-time buyer is listed as the owner.

This way, the first-time buyer can still benefit from the stamp duty exemption.

Many UK lenders offer these mortgages, making them a handy option for couples where one partner hasn’t owned a property before.

Things to Consider When Buying Again

Buying a home again requires considering your changed circumstances. Perhaps your income has shifted, or maybe you’re going solo this time around. These changes affect how much you can borrow and what mortgage options are available.

If you’re buying later in life, some lenders offer flexible age limits. Make sure your chosen mortgage fits your retirement plans – you want repayments to align with your expected income after retirement.

Your credit score is vital. Check it regularly for errors and, if needed, improve it by paying down debt and making timely payments.

Stay informed about current market conditions. Monitor interest rates and property prices. Locking in a lower rate can save you significantly in the long run. Understanding whether local property prices are rising, stable, or falling will help you make a better choice.

Explore different mortgage products. Decide between a fixed or variable rate based on your finances and risk tolerance. If your situation is unique, like being self-employed, look into specialist mortgage products.

Government schemes can offer substantial support. See if you qualify for schemes like First Homes or Shared Ownership, which can provide financial aid and make buying a home more affordable.

The Bottom Line

Even though you can only be a true first-time buyer once, some lenders might consider you one if you haven’t owned a home in a long time. But you’ll probably miss out on the government’s stamp duty break for first-time buyers.

Feeling lost? Not sure if you qualify or need help navigating mortgages as a previous homeowner?

A good mortgage broker can be your knight in shining armour.🌟

Here’s why a whole-of-market broker is your best bet: they search ALL lenders and deals, not just a select few. This means they find the perfect mortgage for you, whether you’re buying alone, with a partner, or even in a group.

They can even handle tricky situations like joint borrower sole proprietor mortgages, making sure you get the best possible terms.

Plus, they save you time and stress by dealing with all the paperwork and negotiations, making the whole process smoother and easier.

So, if you’re re-entering the property market and feeling daunted, a whole-of-market broker is your secret weapon. They have the knowledge, connections, and drive to find the ideal mortgage for you.

That way, you can focus on the important stuff, like planning your housewarming party (or, let’s be honest, Netflix and chill).

Need a broker? Get in touch with us. We’ll connect you with a good mortgage broker for a free, no-obligation consultation to help you solve your mortgage situation.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

What is a second time buyer?

A second-time buyer is someone who’s owned a home before and is now buying another. This could be someone moving house, buying a second home, or even someone who sold their first place and is now jumping back into the market.

While they won’t get perks like reduced Stamp Duty Land Tax (meant for first-time buyers), second-time buyers can still access other mortgages and government schemes available to homeowners.

What age are most first-time buyers?

In the UK, the average age of first-time buyers is typically around 32 years old. This age can vary depending on factors such as location, income levels, and housing market conditions.

In more expensive areas, like London, the average age may be higher due to the higher cost of properties and the need for larger deposits.

Who qualifies as a first-time buyer in Ireland?

A first-time buyer in Ireland, similar to the UK, is someone who has not previously purchased or built a residential property, either as a sole or joint owner, anywhere in the world.

Do couples lose first-time buyer status if one partner bought in the past in the UK?

Yes, couples lose first-time buyer status if one partner has ever owned a home before. This disqualifies them from perks like reduced Stamp Duty Land Tax.

There’s a possible loophole though: a joint borrower sole proprietor mortgage. Here, both partners can be on the mortgage but only the first-time buyer goes on the title deeds. This way, the qualifying partner might still get some first-time buyer benefits.

Related Articles

Cracking the Mortgage Code: A Definitive Guide for First Time Buyers in 2025

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.