- What Is A Special Purpose Vehicle?

- What Are SPV Mortgages?

- Why Do Investors Choose SPVs?

- How Do I Set Up An SPV?

- How Soon Can I Apply For A Buy-To-Let After SPV Application?

- What Are The Eligibility Criteria?

- What Is A SIC Code and Why Is It Important For SPV Mortgages?

- What Are Documents Required To Get SPV Mortgages?

- How To Get SPV Mortgages?

- Who Offers SPV Mortgages?

- How Much Can I Borrow?

- Things To Consider

- Key Takeaways

- The Bottom Line

SPV Buy-To-Let Mortgages: What Investors Need to Know

Everyone loves saving on taxes. If you invest in property, reducing tax on your buy-to-let means more profit for you. You could save, reinvest, or upgrade your properties.

However recent tax lawA changes have made these savings tough to achieve. Many investors now form limited companies, using mortgage costs as deductible expenses to cut their tax bills.

But, what does this mean for your mortgages, and how can you set it up?

This guide will explain how SPV mortgages work for buy-to-let investments.

What Is A Special Purpose Vehicle?

A Special Purpose Vehicle, or SPV, is essentially a company set up for a specific project. In the property market, SPVs are mainly used for buying and holding properties.

These can be any type of business structure, such as private limited companies, limited liability partnerships, or public limited companies.

Lately, more investors are turning to SPVs for property deals because these structures can offer tax benefits and protect personal assets.

This shift has led to a growing demand for mortgages tailored for these SPVs.

What Are SPV Mortgages?

An SPV mortgage is a loan where the borrower is an SPV, not an individual.

With this type of mortgage, you can buy various properties, including residential buy-to-let houses, flats, and sometimes commercial properties.

The idea is simple: the SPV owns the property, and the mortgage is in the company’s name.

While this often means financial risk is limited to the company, it’s not always so simple. Some lenders might ask for a personal guarantee from the investors, which could affect this protection (we’ll cover this later).

Why Do Investors Choose SPVs?

Most property investors lean towards Special Purpose Vehicles (SPVs) to get financing and enjoy limited liability protection.

Limited liability ensures your personal assets are generally shielded from business debts if things go awry.

However, be aware that some lenders may still require a personal guarantee, holding you personally liable if the SPV defaults on the loan.

Here are some other reasons:

Tax Advantages

Compared to individual landlords, SPVs offer clear tax benefits, particularly regarding mortgage interest. Here’s how they benefit you:

- Lower Corporation Tax Rates. SPVs pay a flat Corporation Tax rate, currently at 19%. This is often lower than personal Income Tax rates, which can climb as high as 45% for top earners.

- Full Mortgage Interest Relief. Unlike individual landlords with a capped 20% deduction, SPVs can deduct the full cost of mortgage interest as a business expense, lowering their taxable profits.

- Tax-Efficient Profit Withdrawals. Owners can take profits out as dividends, which may be taxed at a lower rate than personal income. Plus, they benefit from the £2,000 tax-free dividend allowance.

- Wider Range of Deductible Expenses. SPVs can claim a broader range of expenses against their tax bill, including service charges and repairs, further reducing their tax burden.

Other Benefits

With an SPV, growing your property portfolio is straightforward. You can own as many properties as you like, making it easier to expand.

Plus, sharing ownership is a breeze. You can bring in partners or family members as shareholders, which could also save you some tax.

And if you’re thinking of passing on a property, doing it through an SPV can be more tax-efficient. This way, managing and growing your investments is simpler and potentially more rewarding.

How Do I Set Up An SPV?

To set up an SPV as a limited company, follow these steps:

- Check if a limited company suits your business needs. Consider alternatives like sole trading or partnerships.

- Choose a unique name for your company, making sure it complies with naming rules and isn’t trademarked.

- Appoint your directors and decide if you need a company secretary. Remember, a single person can be both director and shareholder.

- Identify your shareholders or guarantors and anyone with significant control, like those with more than 25% of shares or voting rights.

- Prepare your company’s foundational documents: the memorandum of association and articles of association, which dictate how your company operates.

- Be aware of the records and accounts you must maintain to comply with legal and financial regulations.

- Register your company with Companies House, providing an official address and selecting a SIC code that describes your business activities. This step often includes registering for Corporation Tax.

Read more from the UK government’s site here.

It’s wise to set up your SPV before diving into buy-to-let investments.

If you transfer properties into an SPV later, you might face stamp duty, capital gains tax, and other charges. Starting with an SPV can save you these extra costs and hassle.

How Soon Can I Apply For A Buy-To-Let After SPV Application?

You don’t have to wait after applying for your SPV to start looking into buy-to-let mortgages.

In fact, you can kick off your mortgage application process at the same time as your SPV setup. This approach not only saves you time but also gets your investment plans moving faster.

A mortgage broker who knows the ins and outs of SPV mortgages can guide you on the smartest moves for your specific situation.

What Are The Eligibility Criteria?

Here’s what lenders usually look for SPV mortgage applications:

- SPVs must have appropriate SIC Codes related to property rental or management.

- Newly formed SPVs are eligible, but directors should have a personal income of £20,000-25,000 per annum

- Experience in property investment or management can be beneficial but not always necessary.

- Minimum 25% deposit for the property value. (Some lenders offering 80% LTV, may accept 20% deposit)

- Lenders will check the backgrounds of all shareholders and directors.

- Personal guarantees might be required from directors.

- Good credit history for both the SPV and its directors is crucial.

- Lenders may have specific requirements for the property type and location.

- Some lenders might have age restrictions for directors at the time of the mortgage application and its maturity.

- Some lenders will look at the number of properties you already own, assessing your entire portfolio.

- The number of shareholders in your SPV can also be a factor.

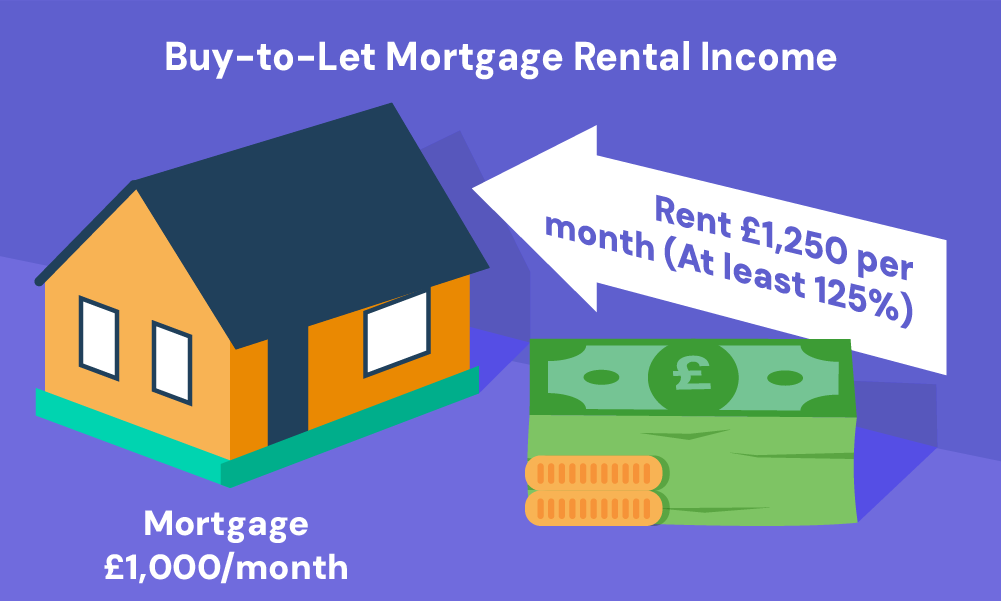

- Rental income should ideally cover 125% -145% of the mortgage payments.

What Is A SIC Code and Why Is It Important For SPV Mortgages?

A SIC code stands for Standard Industrial Classification. It’s a code that categorises the business activity of a company.

When you register your SPV (Special Purpose Vehicle) for property investment, you’ll need to choose a SIC code.

This code informs mortgage lenders about your business type. It helps them understand if the company aligns with their buy-to-let mortgage criteria.

There are different SIC codes for various property investment activities.

Choosing the appropriate code ensures your SPV is classified for the type of buy-to-let mortgage you’re seeking (e.g., rental property vs. property flipping).

For instance, a common SIC code for an SPV holding a buy-to-let property is 68209 (other letting and operating of own or leased real estate).

Remember, it’s always best to consult a mortgage broker specialising in SPV mortgages.

They can advise you on the most suitable SIC code for your specific investment goals and ensure a smooth application process.

What Are Documents Required To Get SPV Mortgages?

To help you get started with your application, here’s a general list of the documents you’ll need:

- Certificate of Incorporation for your SPV.

- Memorandum and Articles of Association.

- Identification documents for all directors and shareholders, usually a passport or driving licence.

- Proof of address for all directors and shareholders, like a recent utility bill or bank statement.

- Business bank statements, typically for the last 3 to 6 months.

- Details of the property or properties the SPV intends to purchase.

- Proof of rental income or rental projections for the property.

- Latest set of SPV’s accounts if applicable.

- Details of existing mortgages or loans held by the SPV.

- Personal income evidence for directors, such as payslips or tax returns.

This isn’t an exhaustive list, and requirements can vary widely. For precise documentation needs, it’s best to check directly with the lender or consult a mortgage broker.

How To Get SPV Mortgages?

Getting an SPV mortgage starts much like a standard buy-to-let application.

Your first move? Team up with a mortgage broker who knows SPV mortgages inside out. They’re clued up on what lenders look for and can steer you through from start to finish.

Your broker is your ace in the hole. They’ll sift through lenders to find the ones most likely to welcome your application. This means you can skip the endless online searches and stay focused on growing your venture.

Looking for a broker? Reach out to us. We’ll arrange a free chat with a top-notch broker who’s all about SPVs, no strings attached.

Who Offers SPV Mortgages?

Several lenders cater to SPV mortgages, understanding the unique needs of property investors. Some of the notable names include:

- The Mortgage Works

- Natwest

- Molo Finance

- LendInvest Mortgages

- Aldermore

- Landbay

- Leeds Building Society

- Mansfield Building Society

- Saffron Building Society

- Leek Building Society

- Vernon Building Society

Do keep in mind that rates for SPV mortgages might be higher than those for standard residential mortgages, reflecting the buy-to-let investment’s nature.

How Much Can I Borrow?

Most buy-to-let mortgage lenders offer at least 75% LTV. But some may offer as higher as 80% depending on your financial situation and factors such as potential rental income, property type, condition, and location.

For an estimate of your repayments, use a buy-to-let mortgage calculator below.

[Embedded buy-to-let mortgage calculator]

Each lender has its criteria, so the amount you can borrow may vary. Checking with a broker can give you a clearer picture tailored to your situation.

Things To Consider

Before jumping into an SPV for your buy-to-let investment, here are some potential challenges and drawbacks to be aware of:

- Increased Administrative Tasks. Running an SPV means you’ll deal with more paperwork and admin, from filing annual accounts to managing company records.

- Complex Taxation. Tax matters can get more complicated with an SPV. You’ll need to navigate Corporation Tax, Dividend Tax, and possibly others, which can be quite a maze.

- Potential for Personal Guarantees. Some lenders might ask you to sign a personal guarantee, meaning you could be personally liable if the SPV fails to pay the mortgage.

- Mortgage Rate Differences. Often, mortgage rates for SPVs can be higher than personal mortgages, affecting your investment’s profitability.

- Regulatory Hurdles. SPVs face strict regulatory requirements, which can be daunting and time-consuming to comply with.

- Property Transfer Costs. If you’re transferring personal properties into an SPV, be prepared for potential stamp duty and capital gains tax implications.

While SPVs offer significant advantages, weighing these considerations is crucial to making an informed decision.

Key Takeaways

- A Special Purpose Vehicle (SPV) is a company set up just to buy and manage properties, making it easier to expand your portfolio and enjoy tax perks.

- SPV mortgages are taken out in the company’s name, but lenders might still ask you for personal guarantees and check your financial background.

- Using an SPV can save on taxes by allowing full mortgage interest deductions, paying lower corporation tax, and taking profits through dividends.

- Setting up an SPV involves registering it as a limited company, picking the right SIC code for property work, and having the right paperwork ready.

- To get an SPV mortgage, you’ll usually need a 25% deposit, a good credit score, rental income that covers mortgage payments, and a steady personal income for directors.

The Bottom Line

SPV mortgages are a specialised field, meaning the number of deals and lenders can be limited. Often, the best offers come from specialist lenders who might not advertise widely.

To uncover the best deals, teaming up with a skilled mortgage broker who understands SPVs and buy-to-let mortgages is key.

If you’re looking for guidance, we’re here to help. Reach out to us, and we’ll arrange a free chat with a trusted mortgage broker who specialises in SPVs.

They can give you insights and options you need to make the right decision for your investment.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What happens if my SPV can't pay the mortgage?

If your SPV cannot meet its mortgage obligations, the lender may take possession of the property. If a personal guarantee was provided, the lender could also pursue the guarantor’s personal assets to recover the debt.

Are there any restrictions on who can set up an SPV?

There are no specific restrictions on who can set up an SPV. However, lenders typically prefer directors with a stable personal income and, ideally, some experience in property investment or management.

How do I find the best SPV mortgage deals?

The best SPV mortgage deals are often available through specialist lenders who understand the unique needs of property investors. Working with a knowledgeable mortgage broker can help you identify and secure the most competitive offers tailored to your investment goals.

Related Articles

Can You Buy A House Through Your Business?

Many British property investors are looking at a new strategy: buying houses through limited companies. While this approach offers potential tax advantages, it’s not for everyone. Let’s explore the pros and cons of using your business to buy a house in the UK. Can You Actually Live in a House Owned By Your Company? Living […]

Free Rental Yield Property Calculator

Becoming a landlord can be an exciting prospect. You get a steady stream of income, potential for property value growth, and you own a tangible asset. But, owning a property investment also comes with its challenges. You must consider factors such as rental rates, vacancy periods, and maintenance costs. Without a clear picture of your […]

Changing Your Buy To Let To Residential Mortgage

Life can take unexpected turns. Maybe you’re facing a breakup, a new job in another city, the kids needing their own space, or you’re simply looking to downsize. In any of these cases, moving into your buy-to-let might seem like a good move. But hold on! There are key rules: If you switch from renting […]