- What Is A Student Buy-To-Let Mortgage?

- Types Of Property For Student Lets

- The Pros And Cons

- Who Is Eligible?

- Can You Afford A Student Buy-To-Let Mortgage?

- Will Surveyors Value My Student Buy-to-Let Properly?

- Who Offers These Mortgages?

- What Are The Top Cities for Student-Let Properties in the UK?

- Can Students Themselves Get a Buy-to-Let Mortgage?

- Key Takeaways

- The Bottom Line: Apply For A Student Buy-to-Let Mortgage

A Guide to Student Buy-To-Let Mortgages

Student buy-to-let properties stand out in the UK. With universities brimming with students, there’s a constant need for places to live.

This high demand makes it an attractive option for investors considering buy-to-let mortgages. But before you dive in, it’s important to understand the specifics of this investment strategy.

This guide will walk you through everything you need to know about student buy-to-let mortgages.

Let’s get started.

What Is A Student Buy-To-Let Mortgage?

A student buy-to-let mortgage lets you buy a property to rent out to students, similar to a regular buy-to-let mortgage.

These mortgages are for homes suited to student living, like flats or houses. Some lenders have stricter rules than others, but it can be accessible to a range of investors.

The big draw is the steady stream of income from student renters, as there’s always a high demand for housing near universities.

Types Of Property For Student Lets

There are two main options for student renters: Purpose-Built Student Accommodation (PBSA) and Traditional Houses in Multiple Occupation (HMOs).

PBSA is built specifically for students, with modern features like Wi-Fi, lounges and gyms. It’s hassle-free for tenants as it includes bills and maintenance. PBSA is a cash investment for landlords, typically for experienced ones, as mortgages aren’t available.

HMOs are houses or flats with shared kitchens and bathrooms for student tenants. They feel more like a home and can be cheaper to buy for landlords. HMOs can bring in more rent, but they also involve more work managing them and following HMO rules.

HMOs with five or more tenants from different backgrounds, or those over three floors, are classed as large HMOs and need a licence. This licence costs money (price varies by area) and needs renewing every five years.

Some councils might also require planning permission for HMOs, which could be refused if there are too many HMOs in the area already.

Because of this added complexity, fewer lenders will give mortgages for large HMOs unless you have an expert advisor helping you.

The Pros And Cons

Investing in student buy-to-let properties can be rewarding, but it’s not without its challenges. Here’s a quick overview to see if it’s the right move for you.

Pros

- High demand in university towns and cities means you’re likely to find tenants easily.

- You could get higher rental yields compared to standard residential lets.

- If you have children, you could buy a property for them to live in when they go to university.

- Opportunity to diversify your investment portfolio.

- Some properties, especially PBSAs, come with management teams so you don’t have to deal with day-to-day tasks.

Cons

- Students might move out more often, which means more maintenance and managing new tenants.

- Student properties might need repairs and refurbishments more often due to wear and tear.

- Dealing with HMO regulations and licensing can be complicated.

- Some lenders may have stricter criteria for student lets.

- Market saturation in some areas may lead to competition for tenants.

Talking to a mortgage advisor can help you understand if this investment matches your financial goals and circumstances.

Who Is Eligible?

While student buy-to-let mortgages share similarities with standard buy-to-let mortgages, there are a few key differences to be aware of:

- Landlord experience. Some lenders prefer or require experience due to the complexities of managing student lets.

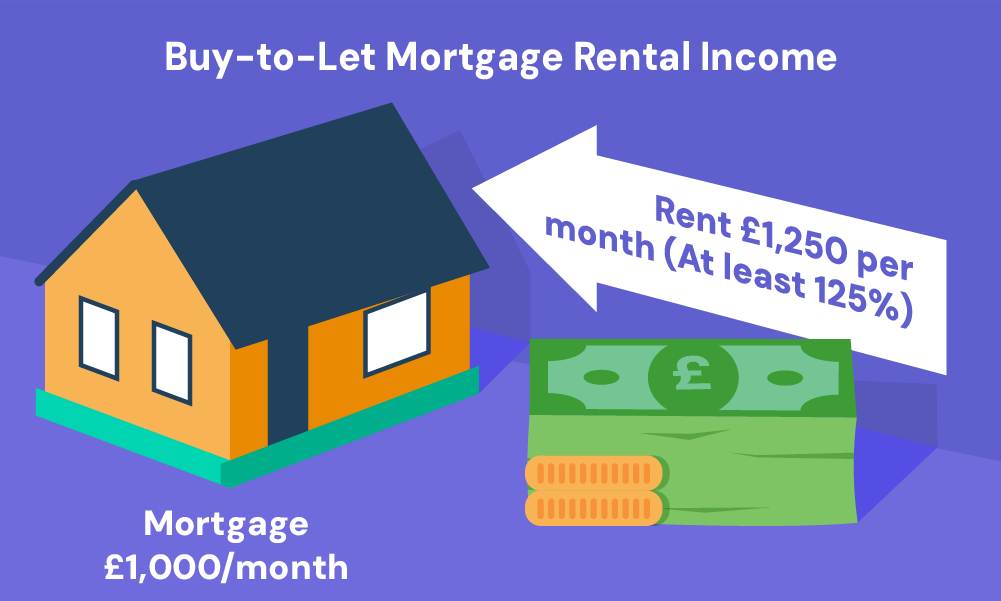

- Rental yield. The expected rental yield might need to be higher for student properties, with some lenders asking for 125% to 180% of the mortgage repayments.

- Property type. Lenders have specific preferences regarding the type of student property they’ll finance, with some being wary of larger HMOs.

- Deposit size. A larger deposit of at least 25% or more might be necessary, particularly for HMOs or in areas with high student property saturation.

- Landlord obligations. Managing student lets often involves additional responsibilities, such as ensuring the property meets safety standards and acquiring necessary HMO licences.

Meeting these criteria is essential for securing a student buy-to-let mortgage, so it’s worth reviewing your eligibility carefully.

Can You Afford A Student Buy-To-Let Mortgage?

Lenders usually offer up to 75% loan-to-value (LTV) for buy-to-let properties. LTV is the ratio of your loan to the value of the property. So, you’ll need at least a 25% deposit of the property’s price.

To see if you can afford a student buy-to-let mortgage, use our calculator. It shows your possible payments. But, remember, it’s just an estimate.

For precise advice, talk to a mortgage broker who knows about student lets.

Will Surveyors Value My Student Buy-to-Let Properly?

Yes, surveyors look at your student buy-to-let’s condition, location, and potential rental earnings to determine its value.

To get the best mortgage amount, choose a lender familiar with student HMOs. These lenders value the property based on how much rent it can bring in, not just its physical condition.

This helps you avoid needing a bigger deposit because of a low valuation. If you’re worried about the valuation, a mortgage broker can advise you and find solutions.

Who Offers These Mortgages?

Several lenders offer student buy-to-let mortgages, including Shawbrook Bank, Bank of Ireland, Aldermore, and Natwest.

For properties with higher occupancy, like larger Houses in Multiple Occupation (HMOs), specialist lenders might be your go-to as they’re more accustomed to dealing with the unique risks and requirements of student lets.

Additionally, student buy-to-let rates are typically higher than standard buy-to-let rates, but a bigger deposit gets you a better deal. A mortgage broker can help you find the right lender for your investment.

What Are The Top Cities for Student-Let Properties in the UK?

There isn’t a single perfect answer to this as the best city depends on what you prioritise.

But the best cities in the UK to invest in student lets often have a strong educational infrastructure, vibrant student life, and a high demand for rental accommodation.

Here are some top choices:

- Manchester

- London

- Birmingham

- Leeds

- Liverpool

- Nottingham

- Sheffield

- Newcastle

- Edinburgh

Can Students Themselves Get a Buy-to-Let Mortgage?

Students can get a buy-to-let mortgage, but usually with a strong guarantor like a parent. This helps them enter the property market despite not having a regular income.

There’s also a special “buy-for-uni” mortgage. This lets students buy a property, live in one room, and rent out the others. It’s a way to manage living costs and learn about property investment.

Getting a buy-for-uni mortgage can be tough. You’ll still need a guarantor and the property must be close to the university. But the benefits are good – it solves student housing issues and gets students started in property investment early.

Key Takeaways

- Student buy-to-let mortgages are similar to regular buy-to-let mortgages but for properties rented to students.

- There are two main property types: PBSAs, which are hassle-free for tenants and landlords, and traditional HMOs, which might bring in more rent but involve more work.

- The criteria for student buy-to-let is similar to standard ones, but with some exceptions like landlord experience, a higher expected rental yield, 25% deposit, and good property condition.

- Surveyors value properties based on condition, location, and rental potential. Choosing a lender familiar with student HMOs can ensure a fair valuation.

- If you’re a student you can get a buy-to-let mortgage with a guarantor’s help and a mortgage broker.

The Bottom Line: Apply For A Student Buy-to-Let Mortgage

If you’ve read this far, it means you’ve likely understood the basics about student buy-to-let mortgages.

First, figure out what you can afford to see which properties are in your reach. Then, collect all your important documents like your income proof, deposit proof, ID, and property details.

To find the best deals quickly and save time, consider using a professional mortgage broker. They’ll handle the heavy lifting, searching through options so you don’t have to. They’re well-versed in the market and can guide you to lenders likely to approve your mortgage.

Need a broker? Reach out to us. We’ll arrange a free, no-obligation consultation with a reliable broker who specialises in student buy-to-let mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I buy a student property for my child?

Yes, you can buy a student property for your child. It’s a way to invest your money and house them during their studies. They’ll save on rent and you could earn rental income. But remember, there’s an extra 5% tax on second homes.

Helping them buy with a gifted deposit might save on tax, but some lenders have rules, especially for HMOs (shared houses).

Is it possible to lease a property to my child?

Yes, you can certainly lease a property to your child.

However, if you’re buying a student HMO (house in multiple occupations) for both investment and your child’s accommodation, you’ll need a family buy-to-let mortgage.

These are less common as lenders worry about families being lenient on rent. Talk to an advisor to help you find a good deal as these mortgages are harder to come by.

Related Articles

Can You Buy A House Through Your Business?

Many British property investors are looking at a new strategy: buying houses through limited companies. While this approach offers potential tax advantages, it’s not for everyone. Let’s explore the pros and cons of using your business to buy a house in the UK. Can You Actually Live in a House Owned By Your Company? Living […]

Free Rental Yield Property Calculator

Becoming a landlord can be an exciting prospect. You get a steady stream of income, potential for property value growth, and you own a tangible asset. But, owning a property investment also comes with its challenges. You must consider factors such as rental rates, vacancy periods, and maintenance costs. Without a clear picture of your […]

Changing Your Buy To Let To Residential Mortgage

Life can take unexpected turns. Maybe you’re facing a breakup, a new job in another city, the kids needing their own space, or you’re simply looking to downsize. In any of these cases, moving into your buy-to-let might seem like a good move. But hold on! There are key rules: If you switch from renting […]