- What is the Deposit Unlock Scheme?

- How Does the Deposit Unlock Scheme Work?

- Deposit Unlock Scheme Builders

- Who Offers Deposit Unlock Mortgages?

- What are the Benefits of the Deposit Unlock Scheme?

- Are There Any Limitations to the Deposit Unlock Scheme?

- How to Apply for a Deposit Unlock Mortgage?

- Alternatives To Deposit Unlock Mortgages

- Key Takeaways

- The Bottom Line

A Complete Guide To Deposit Unlock Scheme

The high cost of housing and strict mortgage requirements in the UK can make buying a home, especially a new build, a challenge.

Deposit Unlock Mortgages offer a solution. These mortgages are designed specifically for new-build properties and allow buyers to put down a smaller deposit upfront.

This article will explain how the scheme works, who it benefits, and why it might be a better option compared to traditional mortgages.

Whether you’re a first-time buyer or looking to move, Deposit Unlock Mortgages could be your key to unlocking your new home.

What is the Deposit Unlock Scheme?

The Deposit Unlock Scheme is a mortgage initiative that lets you buy a new build home with just a 5% deposit. This is a lifeline for first-time buyers and home movers in the UK.

To qualify for the scheme, you need to:

- Choose a new build home from a participating builder.

- Secure a mortgage from a participating lender.

- Have at least 5% of the home’s price for your deposit.

Launched in June 2021 by a collaboration of 17 property developers from the Home Builders Federation (HBF), the scheme was initially rolled out with Newcastle Building Society.

It saw a wider release with Nationwide Building Society and was later joined by Accord Mortgages in August 2022.

With the Help to Buy scheme ending in October 2022, Deposit Unlock has become an essential option for purchasing a home with a smaller upfront payment.

How Does the Deposit Unlock Scheme Work?

First, you choose a property from a participating builder. These builders have partnered with lenders to make buying easier for you.

In other words, builders insure the mortgages to reduce the risk for lenders. They use some of the money from house sales to pay for this insurance.

Normally, mortgage lenders require a 15% to 25% deposit because new builds can lose value quickly.

But, with the builder’s support, lenders are happy to offer mortgages with just a 5% deposit from you. This means more people can buy a home in the UK.

In addition, the maximum loan you can get is £750,000, but this depends on the lender and your situation.

Deposit Unlock Scheme Builders

The Deposit Unlock Scheme is supported by a wide range of home builders across the UK. Here’s a list of the participating builders:

- 3West Group

- A R Cartwright

- AJ Property Group

- Allison Homes

- Anderson Design & Build

- Anderson O&U

- Ashberry Homes

- Ashwood Homes

- Baker Estates Limited

- Barratt Homes

- Barratt London

- Beal Homes Limited

- Bellway Homes

- Bellway London

- Bewley

- Blackstone Developments Limited

- Bloor Homes

- Bovis Homes

- Braidwater Limited

- CALA Homes Limited

- Campion Homes Limited

- Chase New Homes

- City & Country Homes

- Countryside Properties

- Crest Nicholson

- Croudace Homes

- David Wilson Homes

- Davidson Group

- Deanfield Homes

- Denbury Homes

- Devine Homes

- Devonshire Homes

- Durkan Estates

- Edenstone Holdings

- Edwards Homes

- Fairgrove

- Fairview

- Fenwood Estates

- Fortitudo Limited

- Genesis Homes

- Gleeson Build & Develop Limited

- H&H Properties

- Hagan Homes

- Hayfield Homes

- Hill

- Hopkins Homes Limited

- Ilke Homes

- Kebbell Country Homes

- Kebbell Development

- Keepmoat Homes

- Kitewood Estates Limited

- Lagan Homes

- Life Less Ordinary

- Linden Homes

- Macar Developments

- Mandale Homes

- MCI

- Metis Homes

- Miller Homes

- MJ Gleeson PLC

- Morris Homes

- Morrish Homes

- Nicholas King Homes

- Norfolk Homes

- Orbit Homes

- Pat Munro Homes

- Pearce Fine Homes

- Pentland Homes Limited

- Persimmon

- Peter Ward Homes

- Prospect Homes

- Redrow

- Sigma Homes

- St Modwen Homes

- Stonebond Group

- Stonebridge Homes

- Taylor Wimpey

- Thakeham

- Thomas Homes

- Tilia Homes

- Vistry Group

- Waters Homes

- Weston Homes PLC

- Wheeldon Brothers

- Woodstock Homes

If you’re interested in a new-build home and want to take advantage of the Deposit Unlock Scheme, checking if your preferred builder is on this list is a great first step.

Who Offers Deposit Unlock Mortgages?

Currently, a select group of mortgage lenders offer Deposit Unlock Mortgages. This includes:

- Nationwide Building Society

- Newcastle Building Society

- Accord Mortgages

- Perenna

- Bluestone Mortgages

Each lender has different terms, but they all aim to make it easier for you to buy a new home.

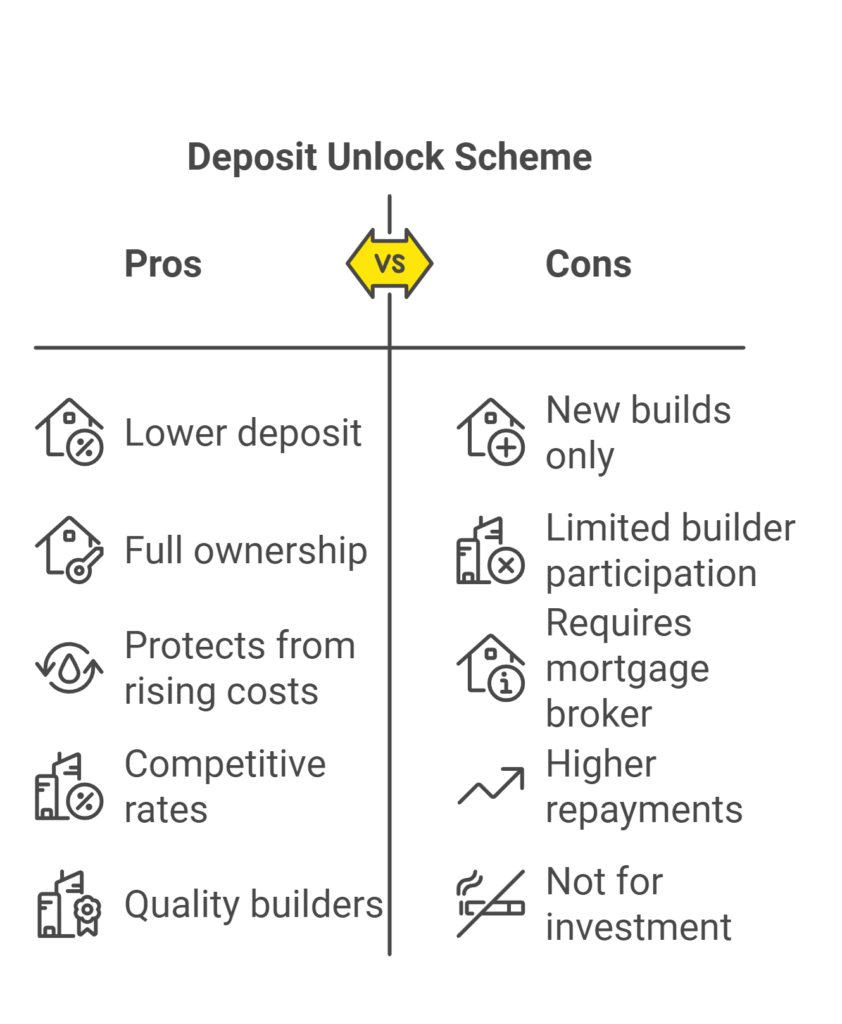

What are the Benefits of the Deposit Unlock Scheme?

Owning your dream home with just a 5% deposit is the main benefit of the Deposit Unlock scheme. Beyond this, here are the pros of securing this mortgage:

- Gain easier access to new builds, often out of reach due to high initial deposit requirements.

- Own 100% of your home right from the start, unlike with shared ownership schemes where you initially own apart.

- Protect yourself from rising rent and property prices by buying your home sooner.

- Enjoy competitive mortgage rates thanks to the insurance-backed guarantee that gives lenders confidence.

- Choose from properties offered by the UK’s leading house builders, ensuring quality and reliability.

- Take advantage of the scheme’s availability to help you move quickly into your new home.

- Buy new-build properties up to the price of £833,250 with no regional price cap restrictions, offering you more choices in your home search.

These benefits make the Deposit Unlock scheme a standout option if you’re aiming to purchase a new build without the heavy financial burden usually involved.

Are There Any Limitations to the Deposit Unlock Scheme?

The Deposit Unlock scheme has perks, but there are downsides to consider before you jump in. Here’s what you need to know:

- You can only buy new-build homes, not older properties which might be cheaper or in your preferred area.

- Not all builders participate, so your options might be limited to specific developments or areas.

- Most lenders require a mortgage broker to apply, adding an extra step to the buying process.

- Lower deposits typically mean higher monthly repayments and more interest paid overall.

- This scheme is only for buying a home to live in, not for investment or buy-to-let purposes.

- Depending on the economy and lender criteria, these mortgages might not always be available.

Before opting for a Deposit Unlock mortgage, consider these points carefully:

- Make sure the homes available are where you want to live.

- Check if you can afford the higher monthly payments.

- Talk to a mortgage broker who can help you see all your choices and find the best deal.

How to Apply for a Deposit Unlock Mortgage?

If you’re interested in applying for a Deposit Unlock mortgage, here’s a straightforward guide to get you started.

First, you’ll want to find a mortgage broker who specialises in these types of mortgages. They’re the experts and can guide you through the whole process.

You’ll need a few things to apply:

- Proof of your income to show you can afford the mortgage.

- Details of your savings to cover the 5% deposit.

- Identification documents like your passport or driver’s licence.

- Proof of your current address.

The broker will help you fill out the application and send it to the right lender. They’ll also explain all the details, so you understand everything before you sign.

Think about what you can manage monthly and long-term. These choices will affect your finances for years, so picking the right path for you is crucial. Always talk to a professional to get the best advice tailored to your needs.

Alternatives To Deposit Unlock Mortgages

Besides the Deposit Unlock scheme, there are several other ways to make buying a home more achievable:

- Shared Ownership. Buy part of your home and pay rent on the rest. You can buy more shares over time. This helps if full ownership is out of reach at first.

- First Homes Scheme. Specifically for first-time buyers, homes are sold at a minimum of 30% below market value. You’ll still need a mortgage and deposit, but the reduced price makes it easier.

- Mortgage Guarantee Scheme. Available until June 2025. This scheme encourages lenders to offer mortgages with just a 5% deposit by providing a government guarantee on these loans.

- Lifetime ISAs. Save for your first home with a Lifetime ISA. The government adds a 25% bonus to your savings, up to £1,000 per year, which can go towards your deposit.

- Own New Rate Reducer. When you buy a new build with this scheme, the developer contributes 3% or 5% of the purchase price towards lowering your mortgage rate. This lowers your monthly payments for the first 2 to 5 years, making it easier to manage costs as you settle in.

- Family Deposit Mortgages. Your family can help you buy a home by contributing towards your deposit or using their home as security. This can boost your buying potential.

- Guarantor Mortgages. A family member or friend guarantees your mortgage by pledging their savings or their own home as security. This can make lenders more willing to offer you a mortgage.

- Saving Up. Simply saving for a larger deposit opens up more mortgage options and potentially better rates.

Key Takeaways

- The Deposit Unlock Scheme helps you buy a new-build home with just a 5% deposit, making it easier for first-time buyers and home movers.

- Only new-build homes from participating builders are eligible, so you need to check if the builder of your chosen property is part of the scheme.

- Other options like shared ownership, government schemes, or saving for a larger deposit can also help if this scheme doesn’t suit your needs.

The Bottom Line

Let’s wrap up what we’ve talked about.

The Deposit Unlock scheme lets you buy a new-build home with just a 5% deposit. It’s a great help if you’re a first-time buyer or moving home and struggling to save for a larger deposit.

This scheme, along with others, is shaping the future of buying new builds in the UK. It makes homeownership more accessible at a time when saving enough for a traditional deposit is tough for many.

To access these mortgages, working with a mortgage broker is essential. They are the only way you can apply for a Deposit Unlock mortgage. Brokers can clarify all the details and help you navigate the best deals to suit your needs.

Need a broker? Get in touch with us. We’ll connect you with a reliable mortgage broker who specialises in Deposit Unlock mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do I need a high income to qualify?

Not necessarily. Your income should support mortgage payments, but the scheme aims to lower the upfront cost.

Can I combine this with other schemes?

Typically, no. Deposit Unlock is not usually compatible with other ownership schemes like shared ownership.

Is it only for first-time buyers?

No, if you’re moving homes you can also use it. It’s not for second homes or investment properties, though.

Can I buy any home with it?

No, the scheme is specific to new-build homes that participate in the scheme, and not all builders are involved.

Related Articles

How To Save For A Mortgage Deposit?

Saving for a deposit on your first home can be tough, but a clear plan will help you reach your goal. Your first step? Figure out how much you need to save. 💷 In the UK, a typical mortgage deposit is at least 5% of the house price. With average UK house prices sitting at […]

What Is Proof Of Deposit For A Mortgage?

When you’re buying a house, one of the first things you need is a deposit. This is a chunk of money you pay upfront. 💷 Most mortgage lenders ask for at least 5% to 20% of the property’s value. However, it’s not enough to simply have the deposit amount ready. You must also show where […]

Can I Really Get a Mortgage With No Deposit in the UK?

While saving a deposit is the traditional path to home ownership, the dream of buying a house with no money down is very tempting. With soaring property prices, can you really get a 100% mortgage and avoid years of gruelling savings? 🤔 What Is a No Deposit or 100% Mortgage? A no deposit or 100% […]