- How Much Interest Will You Pay for Development Finance?

- What Affects Your Development Finance Rates?

- How Do Current Rates Compare?

- What Extra Costs Come with Development Finance in the UK?

- What Paperwork Do You Need for a Development Loan?

- How Can You Get a Better Rate on Your Development Finance?

- The Bottom Line

How To Get Better Development Finance Rates In The UK?

Did you know that even a small change in interest rates can cost you a lot of money?

For example, if you borrow £1 million for a property project and the interest rate goes up by just 1%, you’ll pay an extra £10,000 each year. Over a three-year project, that adds up to £30,000 more!

Understanding how these rates work is really important to keep your project on track and within budget.

In this guide, we’ll explain how lenders decide your rates, what affects them, and how you can secure the best deal.

Whether you’re new to property development or have done it before, this guide will help you make smart financial choices and avoid surprises.

How Much Interest Will You Pay for Development Finance?

If you’re planning a property project in the UK, one of the first things you’ll want to know is how much interest you’ll need to pay.

The answer depends on a few key things, like how much you’re borrowing, your experience, where your project is, and how your loan compares to the total value of the finished project (called the gross development value or GDV).

For smaller loans under £500,000, experienced developers might see yearly rates as low as 6.5%, while newer developers often face rates closer to 9% a year.

Larger loans over £500,000 tend to have annual rates between 4.5% and 7.5%, especially if the loan is less than 70% of the project’s GDV and the developer has some experience.

Higher-risk or smaller loans may come with monthly rates between 0.85% and 1.35%, which means you could be paying 10.2% to 16.2% per year.

On the other hand, for large projects exceeding £1 million, skilled developers can usually expect yearly rates around 6.5% to 7.5%.

These figures are only estimates, and extra costs like setup fees or exit charges might not be included. Always review the full details before moving forward with a loan.

What Affects Your Development Finance Rates?

The rate you get for a loan depends on several things. Here’s a simple breakdown:

- Your Experience. If you’ve successfully done similar projects before, lenders might trust you more and give you a lower rate.

- Loan Amount. Borrowing more money can sometimes mean a higher interest rate, even though it seems like it should be the opposite.

- Location of Your Project. If your site is in a faraway or tricky-to-reach area, costs go up, which can make your rate higher.

- Loan Size vs. Project Value. Lenders look at how much you’re borrowing compared to how much your finished project will be worth. If the project seems risky, the rate may be higher.

- Loan Length. Development loans are usually short-term, up to three years. Shorter timelines can sometimes make rates higher because they seem riskier to lenders.

- The Economy. If interest rates in the economy are high or lots of people are borrowing, your rate might go up too.

- Type of Project. Big or complicated projects like new buildings often come with higher rates than simpler ones, like fixing up an existing property.

- Lender Rules. Every lender has different offers, so it’s worth checking what they include and watching for extra fees.

These are the main things that decide your loan rate. Make sure you ask questions, compare options, and read all the details before choosing.

How Do Current Rates Compare?

It’s hard to say exactly what loan rate you’d get because it depends on your project, loan size, and experience. But here’s a simple idea of what different lenders usually offer:

Big Banks

- Best for large loans starting at £1 million.

- They might cover up to 70% of your costs.

- Interest rates start at around 4.5%.

- Great for experienced developers working on easy, low-risk projects.

Special Finance Companies

- Work with loans from £1 million and up.

- Can cover up to 90% of your costs.

- Interest rates start at 6.5%.

- Suitable for tricky or high-risk projects handled by experienced developers.

Small Lenders for New Developers

- Good for smaller loans starting at £300,000.

- They can cover up to 85% of costs.

- Interest rates start higher, around 9%.

- Perfect for new developers or medium-risk projects.

To get the best deal, it’s smart to ask a specialist broker for help. They’ll compare rates, find the right lender, and make the process easier. Without help, you might end up paying more.

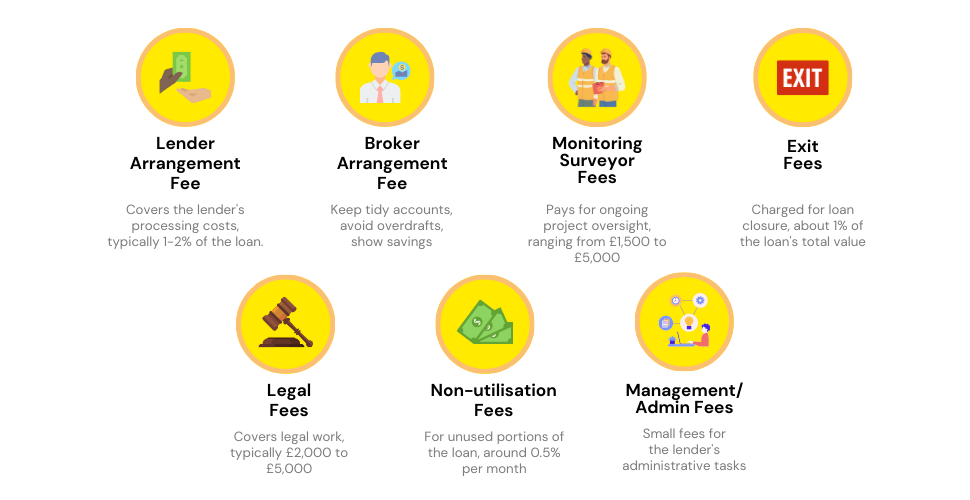

What Extra Costs Come with Development Finance in the UK?

When getting a development finance loan, the interest rate isn’t the only thing to think about. There are other fees that can quickly add up, and these depend on the lender.

Here’s what you might need to budget for:

- Lender’s Setup Fee. This is a fee for arranging the loan, usually 1-2% of the total amount you borrow. For example, if you borrow £1 million, you’ll pay £10,000 to £20,000. This fee is often taken out of your loan before you get the money, so you’ll receive less than you applied for.

- Broker’s Fee. If you go through a broker, they might also charge around 1% of the loan amount, similar to the lender’s setup fee.

- Surveyor Charges. Known also as Quantity Surveyor Fees, these can range anywhere between £1,500 to £5,000 based on how complex your project is.

- Exit Costs. This fee is charged when you finish paying back the loan. It’s usually 1% of the loan amount or the value of the completed project (called the gross development value or GDV). For example, if your loan is £500,000, you might pay £5,000 to exit. If based on GDV, it could be more.

- Legal Costs. You should budget between £2,000 and £5,000 for legal expenses, including the fees for a solicitor.

- Non-Usage Fees. While this is less common, this fee is charged when you don’t use all the money you borrowed. Some lenders charge a fee of about 0.5% of the unused amount each month.

- Admin Charges. These smaller fees, usually a few hundred pounds, cover the lender’s admin work like processing your application and managing paperwork during your project.

When choosing a loan, don’t just focus on the interest rate—these extra costs add up quickly. Always ask the lender for a full list of charges so you can plan your budget.

What Paperwork Do You Need for a Development Loan?

Getting a development loan means showing your lender you’ve planned everything well. The more information you provide, the better your chances of getting a good deal.

Here’s what you’ll usually need:

- Planning Permissions and Architectural Plans

- Planning Constraints

- Detailed Cost Breakdown

- Past Development Records

- Operational Timetable

- Architects and Contractors Contact Information

- Assets and Liabilities Overview

- Exit Plan

- Projected Final Value of the Project

Different lenders might ask for extra documents, like property valuations or post-development estimates.

Having all the paperwork ready makes the loan process much smoother. Always check with your lender to make sure you meet their specific requirements.

How Can You Get a Better Rate on Your Development Finance?

If you want a lower interest rate on your development loan, here are some simple tips that can help:

- Pay a Bigger Deposit. The more money you put down upfront, the lower your interest rate might be. Just make sure you’re okay with tying up more cash at the start.

- Understand How Interest Works. Interest is usually charged on the money you’ve used (the amount you’ve borrowed and not yet paid back), not the full loan amount. This means you only pay interest on what you actually spend.

- Build a Good Track Record. If you’ve done property development before and have a history of successful projects, lenders are more likely to give you a better rate.

- Shop Around. Different lenders offer different rates, so take time to compare your options. A good broker can guide you and help find the best deal.

- Start Small and Gain Experience. If this is your first project, you might pay higher rates at first. But as you complete more projects and prove yourself, getting lower rates will become easier.

The Bottom Line

A good broker can be a big help when you’re working on a property project.

While they can’t promise you the lowest rates, they can make it easier to find good options and guide you through the process. This is especially useful if you’re new to development or don’t have a lot of money to put down upfront.

Brokers can also save you time by comparing deals from different lenders and helping with your application. This might improve your chances of getting approved.

Even if the rates aren’t the lowest, they can connect you with lenders who understand your project and fit your needs.

Not all brokers are the same, so it’s smart to ask about their experience and past successes before choosing one. Being clear about your goals and any challenges can help them find the best options for you.

If you’d like help, reach out to us and we’ll connect you with a broker who knows all about development finance. With the right support, you can focus on what really matters—getting your project done.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What's the usual LTV for property development loans?

Typically, the LTV (Loan to Value) for development finance varies between lenders and depends on a few factors. Generally, you can expect an LTV ranging from 50% to 70% of the project’s Gross Development Value (GDV). Keep in mind that higher LTVs might offer more funds, but they also increase your financial risk.

How can I secure a development loan with better rates?

To boost your chances of getting a development loan with better rates, consider consulting a finance broker who specialises in this area. Your odds improve with factors like past experience, a thorough project plan, realistic financial forecasts, and a solid exit strategy. Comparing various lenders can also help you pinpoint the most favourable rates for your project.

How do lenders charge interest on development finance?

Interest on development loans is usually charged monthly. The rate can be expressed on either a monthly or yearly basis. Generally, the interest accrues based on the remaining loan balance, not the total loan amount.

Is a development loan interest tax-deductible?

Yes, the interest and fees you pay on your development finance can be deducted from your taxable income. This also applies when you switch to development exit financing; all the associated costs can be deducted against your profit.

How are monthly interest payments managed?

Most commonly, interest is rolled into the loan amount, so you usually won’t have any monthly payments. However, some lenders do offer the option to pay the interest monthly, although this is rare and might require further documentation regarding your income and ability to make payments.

Related Articles

Residential Development Finance: A Complete Guide

If you’re eyeing a property development opportunity, chances are you’re also wondering how to finance it. It’s rare for anyone to have enough upfront cash to cover all the costs, and that’s precisely why residential development finance is invaluable. This specialised loan could be the linchpin that holds your project together, setting the scope and […]

Development Finance Calculator: Get A Quick Quote

In development finance, the borrowing range is expansive, stretching from £200,000 to as much as £50 million, depending on your chosen lender. However, unlike more straightforward loan types, what you can borrow is influenced by unique factors such as the projected profitability of your development, the loan-to-cost (LTC) ratio, and even planning permissions. That’s where […]

Why You Need a Development Finance Broker on Your Side

In property development, sorting your finances can often be the deciding factor in your project’s success. Whether you’re eyeing a line of townhouses or a towering apartment block, you need money solutions that fit your plans like a glove. To make this happen, you will need a development finance broker. These experts not only connect […]