Government Schemes Available to First-Time Buyers in 2025

Buying your first home is exciting, but it can also be really hard. You might feel unsure about how to start and what help is out there for you.

The good news is the government has schemes to help first-time buyers like you.

However, each scheme is different and it can be tough to choose the right one.

So we’ve put together this guide to help you decide which scheme works the best for you.

First Homes Scheme

Best for: First-time buyers & key workers finding it difficult to afford a home in their local area.

Under the First Homes Scheme, you can get a substantial discount of 30% to 50% on new-build homes in England.

This is great news if you’re looking to buy your first home but find the prices a bit steep.

What’s even better is that this discount isn’t just for you – it sticks with the house. So, if in the future you decide to sell it, the next eligible buyer gets the same discount.

To give an example, let’s take a look at the numbers.

Let’s say you’ve found a home valued at £350,000. Under the scheme, you’re eligible for a 30% discount. This reduces the price to £245,000, a saving of £105,000.

For this discounted price, your required deposit would be £12,250 (which is 5% of £245,000), and the mortgage you would need to take out is £232,750.

Do You Qualify?

To be eligible, you must tick all the boxes below:

- You need to be buying your first home.

- Your yearly income should be below £80,000 (£90,000 in London).

- You must get a mortgage for at least half of the property’s discounted price.

- The discounted price of the home should not be more than £420,000 in London or £250,000 elsewhere in England.

- Local councils might give priority to key workers, local residents, or those with lower incomes.

- If you’re in the Armed Forces, or recently left, there are special rules to help you.

Pros

- Buy your first home at a large discount, between 30%-50%.

- A smaller deposit might be enough, possibly just 5%.

- Priority access for key workers and local residents, helping them stay local.

- No stamp duty on homes under £425,000, as tax is calculated on the discounted price.

Cons

- Only for first-time buyers with limited income.

- Price limits on properties, up to £250,000 outside London and £420,000 in London, after discount.

- Limited number of homes are available, which may reduce your options.

- When selling, you must offer the same discount to the next qualified buyer, which could lower your selling price and market.

- You need a mortgage for at least 50% of the home’s price, which requires financial stability and savings.

Lifetime ISAs

Best for: Young adults (18-40) saving for a first home or retirement.

The Lifetime ISA (Individual Savings Account) allows you to save up to £4,000 each year until you’re 50. The government adds a 25% bonus to your savings, up to a maximum of £1,000 per year.

This means you can potentially receive up to £32,000 in free cash from the government if you maximise your contributions. You can hold cash or stocks and shares in your Lifetime ISA, or a combination of both.

Do You Qualify?

- You must be aged 18 to 40 to open a Lifetime ISA.

- You need to be a UK tax resident.

- You can only open a Lifetime ISA for yourself.

- You must make your first payment into your ISA before you’re 40.

Pros

- Tax-free withdrawals after you turn 60.

- A 25% boost on your savings from the government.

- Flexibility to access your money early if needed (though this incurs a 25% penalty unless used for a first home or due to terminal illness).

Cons

- Annual contribution limit of £4,000.

- No new contributions are allowed after you turn 50.

- Pensions might offer more tax relief for higher-rate taxpayers.

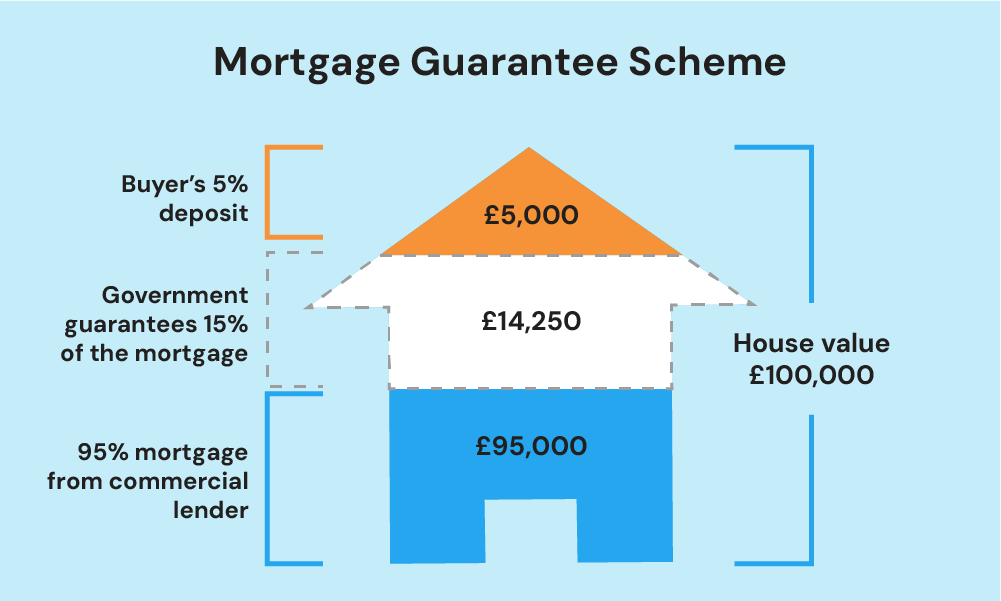

Mortgage Guarantee Scheme

Best for: Individuals struggling to save a large deposit for a home.

The Mortgage Guarantee Scheme is similar to a 95% mortgage but with extra support from the government.

You start with a deposit between 5% and 9% of the home’s price. Then, the lender gives you a mortgage for up to 95% of the home’s value.

For example, if you want to buy a flat worth £100,000, you would pay a deposit of 5%, which is £5,000. You then get a mortgage for the remaining £95,000.

The government promises to cover 15% of your mortgage loan, which is £14,250. This makes lenders more willing to give you a mortgage, as they have less risk.

You don’t need to do anything special to apply for this; your mortgage lender will handle it.

They might charge a fee to the government for this guarantee, which could slightly increase the cost of your loan. This might mean higher interest rates or fees for you.

Do You Qualify?

- You’re buying a home in the UK to live in, not to rent out or as a second home.

- You have a deposit of between 5% and 9%, so your mortgage would be 91% to 95% of the home’s value.

- The home you want to buy costs £600,000 or less.

- You’re getting a repayment mortgage, not just paying interest.

- You pass the lender’s checks to see if you can afford the mortgage.

- You’re an individual buyer, not a company.

Pros

- You can get a mortgage with a smaller deposit, as low as 5%.

- This makes it easier for more people to buy a home.

Cons

- You can only buy homes up to £600,000.

- You might pay more in interest compared to mortgages with bigger deposits.

- There’s a risk of negative equity. This is when your home’s value drops below the amount you owe on the mortgage. It can make it hard to sell your home or change your mortgage later.

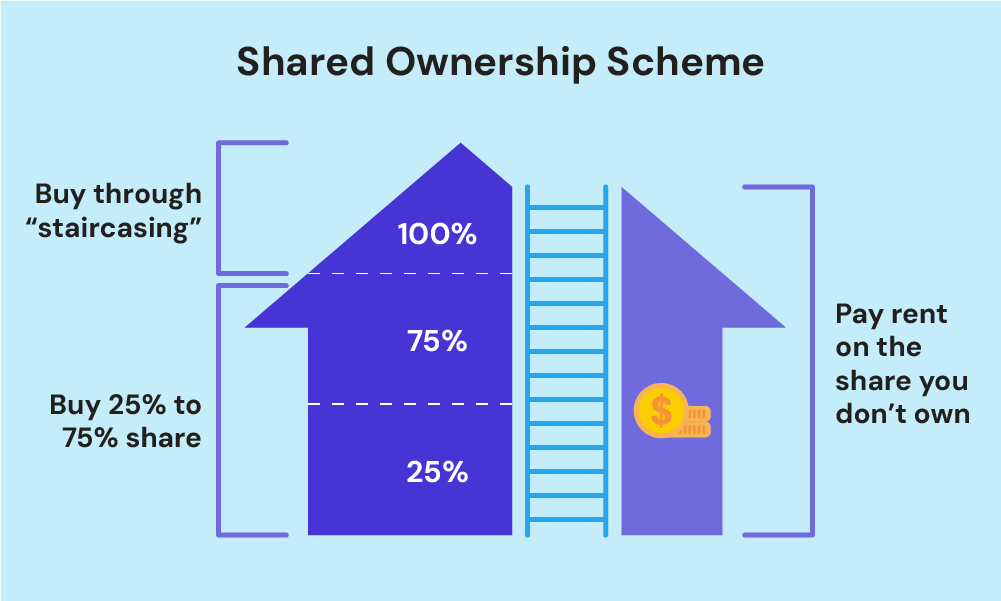

Shared Ownership Scheme

Best for: Those who can’t afford to buy a whole house.

In the Shared Ownership Scheme, you buy a portion of a property, typically between 25% and 75%. You’ll pay rent on the part you don’t own.

This scheme allows you to use a mortgage or savings to finance the share you’re buying. You’ll also need a deposit, usually 5% to 10% of the share’s value.

For example, let’s say you find a property that’s valued at £300,000. If you buy a 40% share, that’s £120,000. Your deposit would be 5% of this share, which is £6,000. You would then need a mortgage for the remaining £114,000.

For the 60% of the property you don’t own, you’ll pay rent, usually around 3% per year of the value of that share.

Here’s a breakdown:

- Home Value: £300,000

- Your Share Price: £120,000

- Deposit: £6,000

- Mortgage: £114,000

Your rental payments will be on the remaining £180,000 (which is 60% of the home’s value). At 3% rent per year, this is £5,400 annually, or £450 per month.

You have the option to buy more of the property over time, known as staircasing. As you buy more shares, your rent decreases.

Do You Qualify?

- Your household income must be £80,000 a year or less (£90,000 in London).

- You can’t afford the full deposit and mortgage for a home that meets your needs.

- One of these must be true: You must be a first-time buyer, a previous homeowner who can’t afford a new home, forming a new household, or an existing shared owner looking to move.

Pros

- Gradually increase your home ownership through staircasing.

- Buy a home sooner than if you were saving for a full purchase.

- Priority access for military personnel.

Cons

- Mortgages under this scheme often have higher rates.

- Selling your share can be tricky, especially if you don’t own the whole property.

- You pay both rent and a mortgage until you own 100% of the property.

- As you buy more shares, the cost can increase if the property value goes up.

Rent to Buy

Best for: Tenants who aspire to save for a home deposit while renting.

Rent to Buy is a scheme that allows you to rent a property at a discounted rate (typically around 20% below market rent), with the intention of buying the home after a set period. This scheme is designed to help you save for a deposit while you’re renting.

For example, if the market rent is £1,000 a month, you might pay £800 a month under Rent to Buy, allowing you to save the difference.

In some cases, a portion of the rent paid during the rental period may contribute towards a deposit if you decide to buy the home.

Do You Qualify?

- Your household earns £60,000 a year or less.

- You are either a first-time buyer or you previously owned a home but can’t afford to buy one now.

- You have a good credit history.

- Eligibility criteria may vary depending on the housing association offering the property.

Pros

- Reduced rent helps in saving for a deposit.

- Opportunity to live in the property before deciding to buy, allowing you to get a feel for the home and community.

- Potential to buy the home through Shared Ownership.

- First chance to buy the home, with no external buyer competition.

Cons

- Limited choice of properties.

- Potential for house prices to increase beyond affordability during the rental period.

- The property might not be available for purchase at the end of the rental term.

- Need to join a waiting list for the scheme in some cases.

Right to Buy

Best for: Council tenants who want to buy their home at a discount.

Right to Buy allows you to buy your rented council home at a lower price than the market value. The discount you get depends on where you live, how long you’ve been a tenant, what type of property it is, and the value of the home.

If you’re buying with someone else, the discount is based on whoever has been a public sector tenant the longest.

Do You Qualify?

To apply for Right to Buy, you should:

- Plan to make the property your main home.

- Be the main tenant of the property.

- Have a secure tenancy agreement.

- Have rented from a public sector landlord (like a council) for at least 3 years.

Pros

- Get a discount on the home’s price

- More financial stability compared to renting.

- You don’t have to move—you can buy the home you’re already living in.

Cons

- If you sell within five years, you might have to pay back some or all of the discount.

- Fewer homes are available under this scheme, especially in high-demand areas.

Key Takeaways

- First Homes Scheme offers first-time buyers like you and key workers up to 50% off on new-build homes.

- Lifetime ISAs add a 25% government bonus to savings for a first home or retirement.

- Mortgage Guarantee Scheme lets you buy your first home with a small deposit, as low as 5%.

- Shared Ownership Scheme allows you to buy part of a home and rent the remainder, suited for lower incomes.

- Rent to Buy allows you to rent a home at a lower rate while saving to buy it, giving you a head start in owning your home.

- Right to Buy enables council tenants to buy their homes at a discounted price.

The Bottom Line

Choosing the right-first-time buyer scheme can be tough. You have many options to consider, and even after reading through this guide, it’s normal to feel unsure about which scheme is right for you.

Speaking with a trusted mortgage advisor can clear up the confusion and help you find the path that suits you best.

However, finding the right advisor could be stressful and time-consuming. To make things easier for you, get in touch with us.

We’ll connect you to a reliable advisor to guide you through your options and secure the best deal for your needs.

Get Matched With Your Dream Mortgage Advisor...

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Can Couples Open a Joint Help to Buy ISA? Find Out Here

You and your partner are serious about buying your first home, and you’re probably looking for every possible way to make it affordable. Maybe you’ve looked into joint savings accounts before, only to find the Help to Buy ISA doesn’t allow joint applications. So, where does that leave you? This article unpacks how individual Help […]

How Help To Buy ISA Works For Your House Deposit

You opened a Help to Buy ISA just before the deadline in 2019. Now you’re ready to make the most of it. You’ve been steadily saving, but with house prices still high, every extra pound counts. In this article, you’ll learn how to get the best out of your ISA. We’ll show you when and […]

Help to Buy ISA End Date Explained: Are There Alternatives?

If you’ve been saving up with the dream of owning your first home, chances are you’ve come across the Help to Buy ISA. But you might be wondering if it’s still around or if you’ve completely missed the boat. The scheme closed to new applicants back in 2019, which was a bit of a letdown […]