- What’s My End Goal?

- Before You Overpay or Investâ¦

- Should You Be Debt-Free?

- How Much Earlier Could I Be Mortgage-Free?

- Will You Need That Money For Other Goals?

- Should You Invest Instead?

- How Do Tax Implications Affect The Decision?

- The Pros and Cons of Overpaying Your Mortgage

- The Pros and Cons of Investing

- Am I Accounting For My Full Financial Situation?

- The Bottom Line: Mortgage Pay Off vs Investing

Should I Pay Off My Mortgage Early Or Invest?

The age-old dilemma for homeowners with extra money – what’s the smarter move? Pay down the mortgage quicker or invest those spare funds?

It’s a tricky decision with no one-size-fits-all answer. Paying off your mortgage eliminates debt sooner while investing gives your money the potential to grow.

Both have merits, it just depends on your individual situation.

Let’s look at the key factors to consider when deciding whether to pay off your mortgage early or invest that extra cash.

What’s My End Goal?

Your overarching financial objectives play a major role here. Are you prioritising:

- Being mortgage-free and debt-free sooner? Overpaying your mortgage is the way to go.

- Building an investment portfolio for retirement or other goals? Investing spare money is probably better.

There’s no right or wrong end goal, it’s personal preference. But being clear on your primary aim makes the decision easier.

Before You Overpay or Invest…

Before rushing to overpay your mortgage or jump into investments, take a step back and assess your financial health. Here’s a quick checklist:

1. Can You Earn More Than You Owe?

See if you can find investments that offer a higher return than your mortgage interest rate.

If your mortgage rate is low and investments promise bigger gains, investing might be smarter.

2. Do You Have an Emergency Fund?

Make sure you have a solid emergency fund – ideally 3 to 6 months of living expenses – in an easily accessible savings account.

This safety net is crucial before putting extra money towards investments.

3. Are You Free of High-Interest Debt?

Focus on paying off any high-interest debts like credit cards or personal loans. These typically cost you more in the long run compared to your mortgage.

4. Are You Saving for Retirement?

Check your contributions to retirement accounts. Starting early and taking advantage of compound interest can significantly benefit your future nest egg.

5. Have You Checked Your Mortgage Terms?

Review your mortgage terms. Some lenders charge penalties for early repayment. Factor these fees into your calculations to see if overpaying still makes sense.

6. Have You Considered Tax Implications?

Understand the tax implications of both overpaying your mortgage and investing. In the UK, for example, ISAs offer tax-free growth on investments, which can be a major advantage.

All sorted? Great!

Once you’ve considered these factors, you’ll be well on your way to making an informed decision about whether to overpay your mortgage or invest.

Should You Be Debt-Free?

Some people find immense peace of mind in eliminating debt, like their mortgage. The security and freedom of owning your home outright is a powerful motivator.

However, others are happy to hold onto a low-interest mortgage if it allows them to invest and potentially build greater wealth in the long run.

The decision between investing and paying off debt comes down to weighing both the financial advantages and the emotional rewards of being debt-free.

To get a clearer picture of the potential benefits of overpaying your mortgage, check how soon you can be mortgage-free.

How Much Earlier Could I Be Mortgage-Free?

Overpaying even small amounts on your mortgage can shave years off the term.

For example, say you’re 5 years into a 25-year £200,000 mortgage at 4% interest. If you overpay £200 per month, you’ll be mortgage-free a huge 4 years early!

Use an overpayment calculator to see how much sooner you could pay off your mortgage by making overpayments.

[Embedded Calculator]

Will You Need That Money For Other Goals?

While overpaying your mortgage can be tempting, don’t go overboard and deplete your savings for other goals or emergencies.

Large lump sums are great for accelerating payments, but they lock your money away. Consider if you might need that cash suddenly.

If your mortgage offers an offset account or borrow-back option, these allow overpayments while keeping your money accessible (check for penalties first). This flexibility is ideal if unexpected costs arise.

The key is finding a balance that tackles your mortgage while keeping enough in savings for emergencies and future plans.

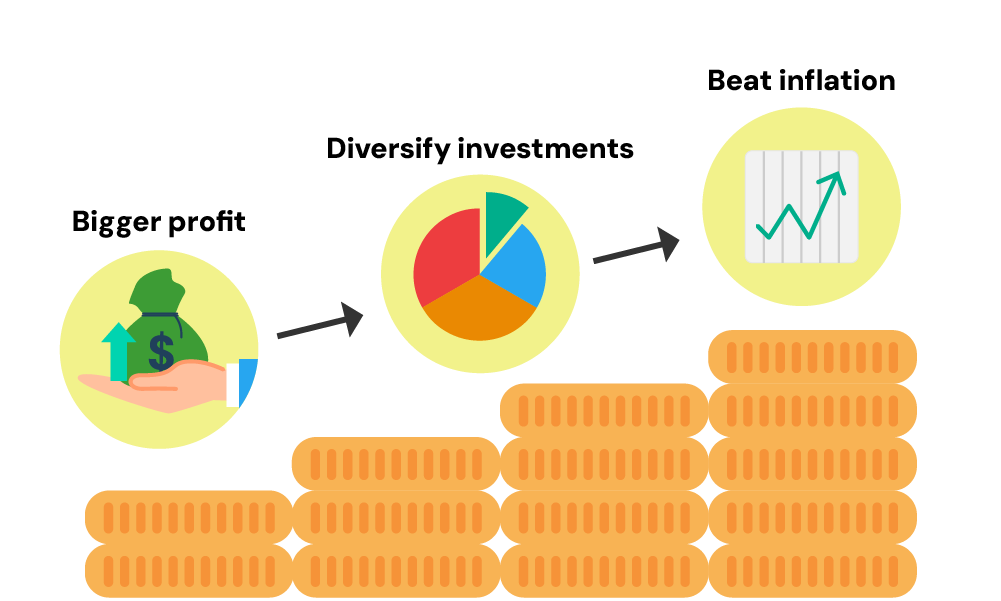

Should You Invest Instead?

Throwing your money into investments can also be a clever financial move. Here’s why you might choose this over early mortgage repayment:

- Potentially Bigger Profits. Stocks and other investments have historically offered higher returns than mortgage interest rates. Invest wisely, and your wealth could grow much faster than just paying off your mortgage.

- Spread the Risk. Investing lets you diversify your assets. Splitting your money across different investments reduces risk and potentially boosts returns.

- Beat Inflation. Investments, especially stocks and property, tend to outpace inflation over time. This keeps your buying power strong and grows your wealth.

How Do Tax Implications Affect The Decision?

In the UK, the Personal Savings Allowance (PSA) lets basic rate taxpayers earn up to £1,000 interest a year on savings tax-free. Higher-rate taxpayers get £500, and additional-rate taxpayers get nothing.

Overpaying your mortgage can save you more interest than you’d earn tax-free from savings or investments.

However, money in an ISA (Individual Savings Account) grows completely tax-free. So, for larger sums, an ISA might be more tax-efficient than paying off your mortgage.

Remember, your personal tax situation will affect the best strategy.

The Pros and Cons of Overpaying Your Mortgage

Let’s talk about the good and bad sides of overpaying that mortgage of yours.

Pros

- You’ll save a bunch of interest by reducing what you owe faster.

- Becoming mortgage-free sooner gives you peace of mind and more financial freedom (doesn’t that sound nice?)

- Once it’s paid off, you’ll have extra cash flow each month to use however you like.

- You get a guaranteed return equal to your mortgage interest rate. (not too shabby!)

- Lowering your mortgage balance can improve your loan-to-value ratio, possibly scoring you better rates later on.

Cons

- Overpaying ties up your cash, making it harder to get your hands on money in an emergency.

- You might miss out on potentially higher returns from investing that extra cash instead.

- Some mortgages charge early repayment fees, which can put a dent in your savings.

- You lose the perk of tax deductions on that mortgage interest.

- Once that money goes to overpayments, it’s not easy to access it for other financial needs.

The Pros and Cons of Investing

Now, let’s look at investing that spare cash instead of overpaying. Here’s an overview of its own pros and cons

Pros

- You could potentially earn higher returns compared to your mortgage interest rate.

- Diversifying your investments reduces risk and boosts your potential gains.

- Investments like stocks and property usually outpace inflation, so your money keeps its spending power.

- Compound growth is a beautiful thing that can make your money grow significantly over time.

- ISAs offer tax-free growth, adding even more to your returns.

- You can sell stocks and bonds quickly if you need to get your hands on some cash.

Cons

- Investments can go up and down in value, so you might lose money, especially in the short term.

- The market’s performance is unpredictable, which can affect your returns.

- Investing involves fees and costs like management fees and taxes on profits.

- It takes time, knowledge, and effort to manage investments successfully.

- Market ups and downs can be stressful and lead to hasty decisions that hurt your long-term returns.

- Money tied up in investments isn’t easy to access for other financial needs or emergencies.

There you have it–the good, the bad, and the not-so-pretty about overpaying your mortgage or investing that extra cash.

Am I Accounting For My Full Financial Situation?

There’s no universal right or wrong answer for whether to prioritise mortgage overpayments or investing. It depends on your:

- Income and job security

- Other assets and debts

- Long-term goals and risk tolerance

- Tax position

- Age and where you are in the mortgage term

Get a full financial plan in place looking at all these factors. Consider speaking to a financial advisor to determine the optimal strategy for you.

Sometimes a blended approach of some overpaying and some investing is the right balanced solution.

The Bottom Line: Mortgage Pay Off vs Investing

Most people benefit from a mix of mortgage overpayment and investing for the long term.

Paying off your mortgage completely offers security and satisfaction. However, investing can grow your money much faster for retirement or other goals.

You don’t have to choose just one. Even a small overpayment of £50-£100 a month can significantly shorten your mortgage term. Meanwhile, investing any extra captures market growth.

To find the right balance, consider your mortgage rate, risk tolerance for investments, tax situation, timelines, and personal goals.

Consulting a financial advisor can help you create the best mortgage and investment plan for your life stage and goals.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What if my mortgage has a high early repayment penalty?

If your mortgage has a high early repayment penalty, carefully consider whether overpaying is worth the cost.

Many lenders allow up to 10% of your mortgage balance to be overpaid each year without penalties. Exceeding this limit could result in fees ranging from 1% to 5% of the overpaid amount.

To avoid these penalties, you might split your funds between smaller overpayments and other investments.

Always check your mortgage terms and consult your lender for precise details about potential penalties.

At what age should you pay off your mortgage?

There is no specific age to pay off your mortgage, as it depends on individual financial situations and goals.

Many aim to be mortgage-free by retirement (around 65+) to reduce living expenses. Paying off your mortgage before retiring can provide financial security and peace of mind.

Evaluate your retirement plans, income sources, and other debts to determine the best timeline for you.

What happens after you pay off your mortgage?

After paying off your mortgage, you own your home outright and no longer have monthly mortgage payments. Your lender will send a mortgage release or deed of reconveyance, confirming the loan is paid in full.

Update your homeowner’s insurance to reflect this change and continue budgeting for property taxes and maintenance.

Review your financial plans and redirect funds from mortgage payments towards savings or other goals.

What do I do after I pay off my mortgage?

After paying off your mortgage, take these steps:

- Get a mortgage release document from your lender confirming the loan is paid off.

- Update and inform your insurance company and remove the lender from your policy.

- Adjust your budget from mortgage payments to savings, investments, or maintenance.

- Keep your record safe.

- Celebrate! Enjoy the security and peace of mind of being mortgage-free.

Related Articles

How Quickly Can You Sell a House in the UK?

If you’re thinking about putting your place on the market, you’re probably curious about how long it might take. Spoiler alert: there’s no exact timeline! It all depends on a few things, like the state of your property and how active the housing market is. On average, though, selling a house in the UK can […]

What Do I Need To Declare When Selling My Home?

Why You Need To Disclose Your Property’s Condition & History Disclosing your property’s condition and history in the UK is both legally required and builds trust with buyers. You must be upfront about any issues to avoid lawsuits under the Consumer Protection from Unfair Trading Regulations (CPR). Failure to do so could result in prosecution, […]

What Happens If My Mortgage Offer Expires?

What is a Mortgage Offer? A mortgage offer is a lender’s formal approval to provide you with a home loan, assuming you meet all the stated terms and conditions. It confirms that your full application – your finances, credit, income, deposit, and property – has passed the lender’s criteria. This checking process can take from […]