- Can I Change My Interest Only Mortgage To Repayment?

- Whatâs the Difference Between Interest-Only and Repayment Mortgages?

- Why Switch to a Repayment Mortgage?

- How To Switch From an Interest-Only Mortgage to Repayment

- How To Pay Off an Interest-Only Mortgage Early

- Can I Change My Mortgage to Interest-Only?

- Key Takeaways

- The Bottom Line: Whatâs the Best Move for You?

Changing from Interest-Only to Repayment Mortgage Explained

Are you starting to feel like your interest-only mortgage isn’t working for you anymore?

Maybe the thought of that looming lump sum at the end is weighing on your mind.

If you’re looking for a way to get more out of your monthly payments and feel more in control of your finances, it might be time to switch things up.

In this guide, we’ll cover everything you need to know about switching to a repayment mortgage, the pros and cons, how to get started, and what options might suit your situation best.

Can I Change My Interest Only Mortgage To Repayment?

Absolutely, you can switch from interest-only to repayment.

Many people in the UK are doing it because it’s a better fit for their financial situation.

Maybe you’re tired of worrying about that big lump sum at the end of your mortgage. Or maybe you want to start owning your home.

The good news is, most lenders are happy to help you switch—as long as you can show them you can afford the higher payments.

And the best part is, once you switch, you’re reducing your debt month by month, instead of just paying interest.

That’s something to look forward to!

What’s the Difference Between Interest-Only and Repayment Mortgages?

First, let’s clear up the basics. 🙂

An interest-only mortgage means that your monthly payments only cover the interest on your loan. So, by the time your mortgage term ends, you still owe the full loan amount.

This might sound appealing at first because your monthly payments are lower, but it can cause a bit of a panic when you realise you need to cough up the full amount at the end.

On the other hand, with a repayment mortgage, your monthly payments are higher because they cover both the interest and a portion of the loan itself.

Over time, this reduces the amount you owe until, at the end of the term, you own your home outright.

No more debt hanging over your head—sounds great, right?

Image comparing interest only vs repayment mortgage

Why Switch to a Repayment Mortgage?

So, why would you want to switch from an interest-only mortgage to a repayment one? 🤔

The most obvious reason is peace of mind. With a repayment mortgage, you won’t have to scramble for a huge lump sum at the end of your term.

Instead, you’re slowly chipping away at your debt month by month.

This means that by the time your mortgage is up, you’ve paid off the full amount and your home is completely yours. 🏠

Another reason to switch is that repayment mortgages often come with lower interest rates.

Lenders love knowing they’ll get their money back bit by bit rather than waiting for one big payout at the end. So they’re usually happy to offer you a better deal.

However, it’s worth remembering that monthly payments will go up. That’s because you’re now paying off both the interest and the loan.

But the trade-off is that you’re reducing your debt and building equity in your home.

Here’s a quick look at the pros and cons:

Pros:

- You own your home at the end and you build equity.

- No big lump sum to worry about at the end of the mortgage term.

- A clear repayment plan helps you manage your finances.

- You’ll pay less interest overall.

Cons:

- Higher monthly payments.

- Less flexibility with your money.

- Early repayment charges might apply if you switch lenders.

- Your new interest rate could go up if you remortgage.

How To Switch From an Interest-Only Mortgage to Repayment

Okay, so you’ve decided switching is the right move for you—great choice! But how do you actually go about it?

1. Talk to your lender

Your first step should be chatting with your current lender.

Most lenders are more than happy to help you switch to a repayment mortgage, especially if you can prove that you can afford the higher payments.

Some lenders even make this process super easy—just a quick phone call or email and they’ll sort it out.

Sounds simple, right?

Keep in mind, though, that your lender will want to check your affordability. This means they’ll look at your income, expenses, and any other debts to make sure you can handle the new payments without any trouble.

If you pass the checks, brilliant—you’re on your way to a repayment mortgage!

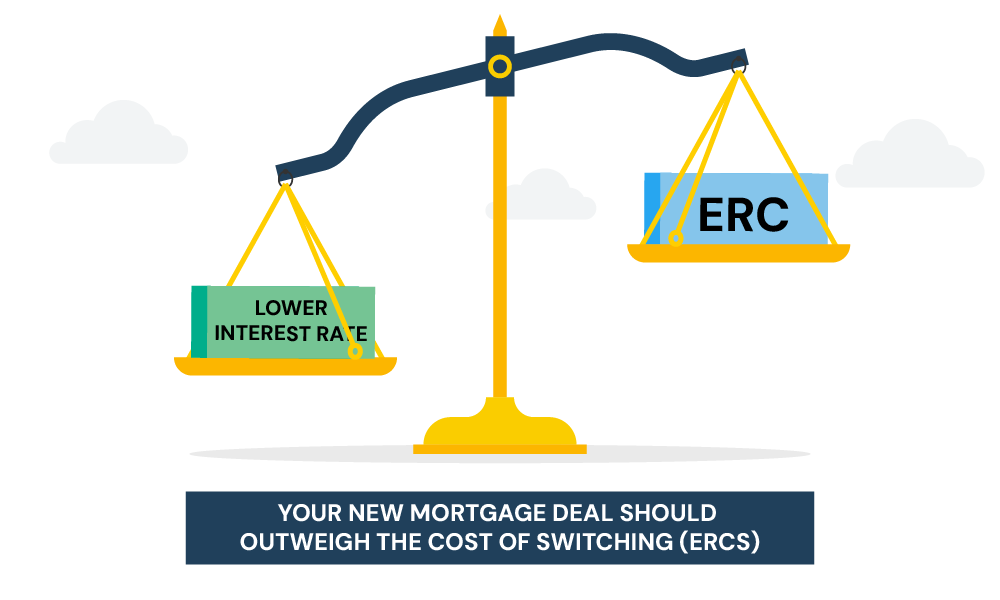

2. Remortgage to a new lender

If your current lender isn’t able to offer the best deal, or maybe they don’t allow the switch, you can always look at remortgaging with a new lender.

This might be a bit more of a hassle, as you’ll need to go through a new mortgage application. But it could save you money in the long run, especially if you find a better interest rate.

Keep an eye out for early repayment charges (ERCs).

If you’re in a fixed-term deal and want to leave early, your lender might charge you a fee. These fees can be a bit steep, so make sure you factor them in when comparing deals.

3. Consider a part-and-part mortgage

Not sure if you can handle full repayment just yet? No worries! Many lenders offer a part-and-part mortgage option.

This is where you pay off part of the loan on a repayment basis and part of it on an interest-only basis.

It’s a good middle ground—your monthly payments will be lower than full repayment, but you’ll still be reducing your overall debt.

It’s a bit like dipping your toes in the water before jumping all the way in.

Image

4. Use a Mortgage Broker

If you’re not quite sure where to start or just want to make sure you’re getting the absolute best deal, a broker can do the heavy lifting for you.

They’ll scour the market and compare thousands of mortgage products, finding the ones that suit your financial situation perfectly.

A whole-of-market broker isn’t tied to any specific lenders, meaning they’ve got access to way more deals than you’d find on your own.

Whether you’re remortgaging or switching with your current lender, a broker can help you navigate the process and save you time, stress, and potentially a lot of money.

And, let’s face it, who doesn’t love the idea of someone else handling the paperwork? 📝

A broker can also help you dodge pitfalls like early repayment charges or surprise fees, making sure you’re not stung by any hidden costs.

They’ll also take your personal circumstances into account—whether you’ve got a patchy credit history or unusual income sources—and find lenders that are a good fit for you. 👌

If you’re on the fence about switching, or simply want to explore your options, having a broker in your corner can make the whole process smooth sailing.

So, whether you’re diving in with full repayment or dipping your toes in with part-and-part, using a broker ensures you’ll be making the most informed decision with confidence.

How To Pay Off an Interest-Only Mortgage Early

If you’re already thinking ahead and wondering how to pay off your interest-only mortgage early, there are a few strategies you can try:

- Overpayments. Some lenders allow you to make overpayments on your mortgage, which can help reduce the overall balance and the amount of interest you pay. Even small extra payments can make a big difference over time.

- Savings or investments. If you’ve built up savings or have investments, you could use these to pay off part or all of your mortgage early. Just make sure you won’t need that money for anything else.

- Downsizing. Selling your home and moving to a smaller, cheaper property is another way to clear your mortgage debt early. This option isn’t for everyone, but if you’re open to moving, it could be a way to become mortgage-free faster.

Can I Change My Mortgage to Interest-Only?

While this article focuses on s witching from interest-only to repayment, it’s worth mentioning that you can also go the other way—switching to an interest-only mortgage.

This might appeal to you if you want to reduce your monthly payments. But keep in mind, it’s a riskier option because you’ll still owe the full loan at the end.

Lenders are usually a bit more cautious about approving interest-only mortgages, as they want to see a clear plan for how you’ll repay the loan.

This could be through selling a property, using investments, or another repayment vehicle.

If you think switching to interest-only might suit you better, be prepared for some extra checks and questions from your lender.

Image

Key Takeaways

- You can switch from an interest-only mortgage to a repayment mortgage if you can afford the higher payments.

- Switching helps you pay off your loan gradually and removes the need for a large lump sum at the end.

- Talk to your current lender or explore remortgaging options if needed.

- Consider a part-and-part mortgage if full repayment isn’t affordable right now.

- Using a mortgage broker can help you find the best deal and avoid early repayment charges.

- You can pay off an interest-only mortgage early with overpayments, savings, or downsizing.

The Bottom Line: What’s the Best Move for You?

Switching can give you more control and peace of mind. By paying off your loan gradually, you avoid the stress of a huge lump sum at the end. Plus, you build equity in your home and might get a better interest rate.

But it’s not for everyone. The higher payments can be a challenge, so make sure it fits your financial plan.

If you’re unsure, talk to a mortgage broker. They can help you weigh your options and find the best deal for you.

Looking for the right broker? Get in touch with us. We’ll connect you with a reliable broker who can help you solve your specific mortgage situation.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What happens if I can’t pay off my interest-only mortgage?

If you can’t pay off the loan at the end of the term, you may need to sell your home, remortgage, or find another way to clear the debt.

Is switching to a repayment mortgage expensive?

Your monthly payments will go up, and you might face early repayment charges if you switch lenders. But in the long run, you’ll pay less interest and build equity in your home.

What is a part-and-part mortgage?

It’s a hybrid option where you pay part of your loan on an interest-only basis and part on a repayment basis. It’s a good option if you want to reduce your debt but can’t afford full repayment right now.

Do I need a solicitor to switch my mortgage type?

If you’re staying with your current lender, probably not. If you’re remortgaging, you might need one to handle the legal bits.

Will switching affect my credit score?

If you’re staying with your current lender, probably not. If you’re remortgaging, there might be a small, temporary dip due to the credit check.

How long does it take to switch from interest-only to repayment?

Switching from interest-only to repayment typically takes 4 to 8 weeks, depending on your lender and whether you need to remortgage.

Related Articles

Retirement Interest Only Mortgages Explained

Tired of stressing about money in your retirement? Maybe you’d like to help your kids get their first home, finally tackle those overdue home improvements, or simply have more financial freedom to travel and enjoy life. These are all great reasons, and you might find the answer here. We’ll explain what a Retirement Interest-Only (RIO) […]

Part and Part Mortgages Explained: Is It Right For You?

In 2022, the number of part and part mortgages in the UK fell by 11.9% from the previous year, reaching 222,000. While this shows a decline, part and part mortgages still offer lower monthly payments and more flexibility. If you want to own a home but need more affordable monthly payments, this type of mortgage […]

Interest-Only vs Repayment Mortgage: Which Suits You Best?

Mortgages are the biggest financial commitment you’ll ever make. You might be wondering: Can I afford the monthly payments? What are my long-term plans for this property? And, most importantly, which mortgage type suits me best? In the UK, there are two main repayment methods to choose from—interest-only mortgages and repayment mortgages. Picking between the […]