- Can You Get a Mortgage if You Have a Disability?

- Which Disability Benefits Do Lenders Consider?

- How to Get a Mortgage on Disability Benefits?

- How Much Can You Borrow on Disability Benefits?

- Are There Any Grants or Schemes to Help?

- Mortgage Lenders That Accept Disability Benefits

- Can You Get a Mortgage with Bad Credit and Disability Benefits?

- The Bottom Line

Getting Mortgages For Disabled On Benefits In The UK

Over 16 million people in the UK have disabilities, and many wonder if they can get a mortgage while receiving benefits.

The good news? It’s entirely possible. However the process can be more complex.

In this guide, we’ll explore every aspect of obtaining a mortgage when you’re ill or disabled, giving you the knowledge to make an informed decision.

Can You Get a Mortgage if You Have a Disability?

Yes, you can get a mortgage even if you have a disability and are on benefits.

Anti-discrimination laws in the UK are clear: lenders can’t reject your mortgage application just because of a disability or illness.

The Equality Act 2010 backs you up, defining disability as any physical or mental condition that significantly impacts your daily life in the long term.

This legislation ensures that lenders assess your application based on affordability and financial circumstances, just like anyone else’s.

They can’t charge you higher interest rates, ask for larger deposits, or demand higher monthly repayments because of your disability.

Fair treatment and equal opportunities to get a mortgage are your rights.

But remember, securing a mortgage may involve some additional steps and considerations. Here’s what you need to keep in mind:

- You must be able to repay the mortgage

- You have a good credit score

- You have money saved up for a deposit

- Your income includes employment earnings, benefits, or other sources

- Your monthly outgoings and existing debts are manageable

- The property’s value meets the lender’s requirements

- The loan-to-value (LTV) ratio is within acceptable limits

Which Disability Benefits Do Lenders Consider?

In the UK, many lenders will look at your disability benefits as part of your income when deciding if you can afford a mortgage. This applies to both high-street banks and specialist lenders.

The benefits they consider include:

- Disability Living Allowance (DLA)

- Personal Independence Payment (PIP)

- Employment and Support Allowance (ESA)

- Attendance Allowance

- Carer’s Allowance

- Child Benefit

- Child Tax Credit

- Maternity Pay

- Jobseekers Allowance

- Pension Credits

- Universal Credit

- Widow’s Pension

- Working Tax Credit

Lenders are more likely to approve your application if you receive long-term disability benefits, as they provide a stable and predictable income stream.

Benefits awarded for short-term disabilities or illnesses may be viewed less favourably, as lenders cannot guarantee the longevity of these payments.

>> More about Mortgages on Benefits

How to Get a Mortgage on Disability Benefits?

The first step in obtaining a mortgage while on disability benefits is to consult with a mortgage broker who specialises in this area.

An experienced broker can guide you through the entire process, from preparing the necessary documentation to finding the right lenders and negotiating the best rates.

Here’s a general overview of the process:

- Gather ALL relevant paperwork, including proof of income (benefit statements), bank statements, and evidence of any other sources of income.

- Get copies of your credit reports and work on improving your credit score if necessary.

- Your broker will assess your financial situation and identify lenders that accept disability benefits as income.

- Apply for pre-approval with the selected lenders, providing all required documentation.

- Once pre-approved, your broker will assist you in finding suitable properties within your budget.

- Complete the formal mortgage application process, and your broker will negotiate the best terms on your behalf.

How Much Can You Borrow on Disability Benefits?

The amount you’ll be approved for largely depends on your specific income and outgoings situation.

Lenders will carefully check your finances to make sure you can afford the mortgage repayments, even if interest rates go up. They’ll be more cautious if your only income is disability benefits.

As a general rule, most high-street lenders cap the maximum mortgage loan at around 4.5 times your annual income for those on benefits. So, with a £25,000 income, you might get a mortgage of up to £112,500 (4.5 times £25,000).

But each situation is different. Lenders consider:

- All your income (benefits, pensions, part-time wages)

- The type and reliability of your disability benefits

- Your age and employment status (retired, unable to work)

- Any existing debts and loans

- Your household expenses

The MORE stable your disability benefits are, the MORE you might be able to borrow.

To increase your borrowing power, you’ll need:

- A good credit score

- Long-term benefits (lasting the mortgage term)

- A larger deposit to reduce the mortgage amount

- Proof of low expenses and few debts

Don’t just take the first lender’s offer either. Using an independent broker, you can seek out the most borrowing-friendly mortgages for disability situations.

To get a quick estimate of what you may be able to borrow based on your current income and expenses, try this handy mortgage borrowing calculator:

[embedded mortgage calculator]

The calculator provides a rough guide, but each lender has their own criteria. With the right preparation and expert mortgage advice, you can put your best foot forward and secure an affordable mortgage that meets your homeownership needs.

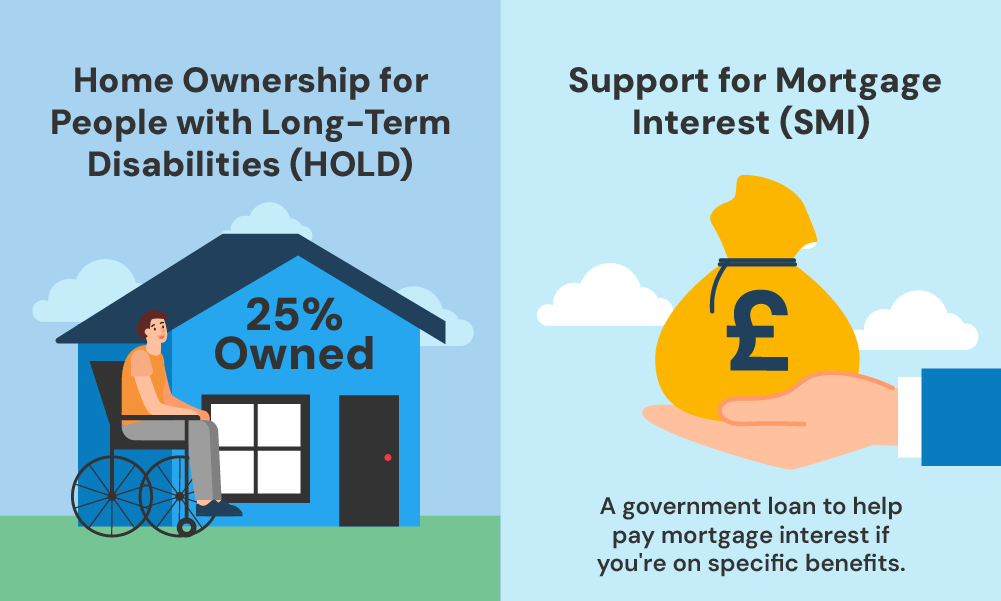

Are There Any Grants or Schemes to Help?

If you’re struggling to afford a mortgage solely on disability benefits, the UK government offers several schemes and grants to assist you in becoming a homeowner.

One such scheme is the Home Ownership for People with Long-Term Disabilities (HOLD), which is a shared ownership program available in England.

Under the HOLD scheme, you can purchase a share of a property (typically 25%) and rent the remaining share from a council or housing association.

As your financial situation improves, you can gradually increase your ownership stake through a process known as “staircasing.”

Additionally, the Support for Mortgage Interest (SMI) program provides a loan to help cover your mortgage interest payments if you’re receiving certain benefits, such as Income Support, Jobseeker’s Allowance, Universal Credit, or Employment and Support Allowance

It’s crucial to explore all available options and seek guidance from housing organisations and mortgage advisors to determine your eligibility for these schemes.

Mortgage Lenders That Accept Disability Benefits

Many mainstream and specialist lenders in the UK are open to considering disability benefits as a legitimate source of income for mortgage applications. Some of the notable lenders that accept disability benefits include:

- Barclays

- NatWest

- Halifax

- Together Money

- Foundation Home Loans

- Pepper Money UK

- Tandem Bank

- Virgin Money

It’s essential to work with a knowledgeable mortgage broker who can match you with the most suitable lender based on your specific circumstances.

Can You Get a Mortgage with Bad Credit and Disability Benefits?

While having bad credit can make securing a mortgage more challenging, it’s not an insurmountable obstacle.

Specialist lenders and brokers can assist you in finding mortgage solutions, even if you have adverse credit and rely on disability benefits for your income.

It’s essential to be transparent about your credit history and work on improving your credit score before applying for a mortgage.

Additionally, providing a larger deposit can improve your chances of approval and result in more favourable interest rates.

The Bottom Line

Getting a mortgage on disability benefits can be tricky, but it’s definitely possible with the right help. A good mortgage broker specialising in disabilities can make a big difference.

These brokers are experts in the mortgage market, lender requirements, and government schemes for people with disabilities.

They’ll give you personalised advice and support throughout the process, making sure you understand everything. They can even fight for you to get the best deal possible based on your situation.

Looking for the right broker? Get in touch. We’ll connect you with a qualified mortgage broker with experience in mortgages for disabled on benefits.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do I still need insurance to get a mortgage on disability?

Yes, certain types of insurance are typically required to get a mortgage, whether you have a disability or not. However, not all insurance types are mandatory. Here are the details:

- Buildings Insurance: This is usually mandatory. Lenders require it to protect the structure of the property against risks like fire, flood, and other damages. You need to have this insurance in place by the time you exchange contracts.

- Contents Insurance: This covers your personal belongings inside the home. While highly recommended, it is not usually a requirement from lenders.

- Life Insurance: This is not mandatory for getting a mortgage, but it is often recommended. Some lenders might suggest it to ensure that the mortgage can be paid off in the event of your death, providing financial security for your dependents.

- Mortgage Payment Protection Insurance (MPPI): This insurance is optional but can be very beneficial. It covers your mortgage payments if you’re unable to work due to illness, accident, or unemployment, offering extra security.

- Critical Illness Cover: Also optional, this insurance pays out a lump sum if you’re diagnosed with a serious illness. It can help cover your mortgage or other expenses, providing additional peace of mind.

While not all insurances are mandatory, having appropriate insurance can provide significant financial protection and peace of mind for both you and the lender.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]