- What is an Agreement in Principle?

- Do I Need To Get an Agreement in Principle?

- How To Get an Agreement in Principle?

- How Long is a Mortgage in Principle Valid?

- Does a Mortgage in Principle Affect Credit Score?

- How Many Times Can I Get an Agreement in Principle?

- How To Handle a Mortgage in Principle Rejection

- The Bottom Line

Mortgage Decision in Principle Explained

You’re ready to buy a home. You’ve saved, you’ve dreamed, and now you’re itching to start viewing properties.

But hold on – before you dive into the exciting world of house hunting, there’s a crucial step you might be overlooking.

It’s called an Agreement in Principle (AIP), and it could be the key to unlocking your homeownership dreams.

What is an Agreement in Principle?

An Agreement in Principle, also known as a Decision in Principle (DIP) or Mortgage in Principle, is basically an initial estimate of how much money a lender might be willing to lend you.

It’s not a guaranteed mortgage offer, but rather a thumbs-up that you’re likely to be approved for a certain amount.

Lenders will take a quick look at your income, expenses, and credit history.

If they like what they see, they’ll give you a certificate or statement stating how much you can borrow.

This statement can be helpful when house hunting, as it shows estate agents you’re a serious buyer.

Do I Need To Get an Agreement in Principle?

An Agreement in Principle (AIP) isn’t mandatory for getting a mortgage, but it has advantages that make it highly recommended.

Here’s why:

- It shows you’re serious. When you approach estate agents or sellers with an AIP in hand, you’re not just window shopping. You’re a potential buyer with some financial backing.

- It gives you a realistic budget. Instead of falling in love with properties you can’t afford, an AIP helps you focus on homes within your reach.

- It can speed up the process. When you find your dream home, having an AIP means you can move faster. In a competitive market, this could be the difference between securing the property and losing out.

- It can uncover potential issues early. If there are problems with your credit history or affordability, it’s better to know sooner rather than later.

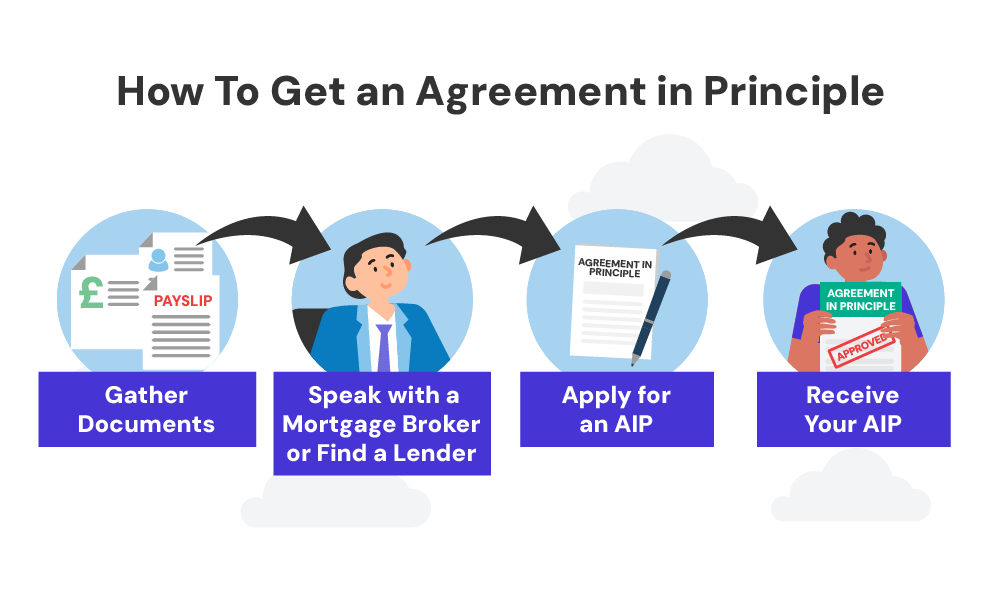

How To Get an Agreement in Principle?

Now that you’re convinced of the importance of an AIP, let’s walk through the process of getting one.

It’s simpler than you might think, and you can often do it in a matter of hours.

1. Gather Required Documents

Before you approach a lender, you’ll need to arm yourself with some key information. \

This typically includes:

- Proof of identity (passport or driving licence)

- Proof of address (recent utility bills or bank statements)

- Details of your income (payslips, tax returns for self-employed)

- Information about your outgoings (credit card statements, loan repayments)

- Bank statements (usually for the last three to six months)

Having these documents ready will make the process smoother and faster. It’s like preparing for a job interview – you want to put your BEST financial foot forward.

2. Speak with a Mortgage Broker or Find a Lender

You have two main options here: go directly to a lender or work with a mortgage broker.

A good broker can be particularly helpful if you’re new to the process. They can give you advice, compare different lenders, and potentially find deals you might miss on your own.

Plus, some brokers have access to exclusive products not available directly to consumers.

If you choose to go directly to a lender, research is key. Look at different banks and building societies, compare their rates and products.

3. Apply for an AIP

Whether you’re going through a broker or directly to a lender, the application process is similar. You’ll need to provide ALL the information you gathered earlier.

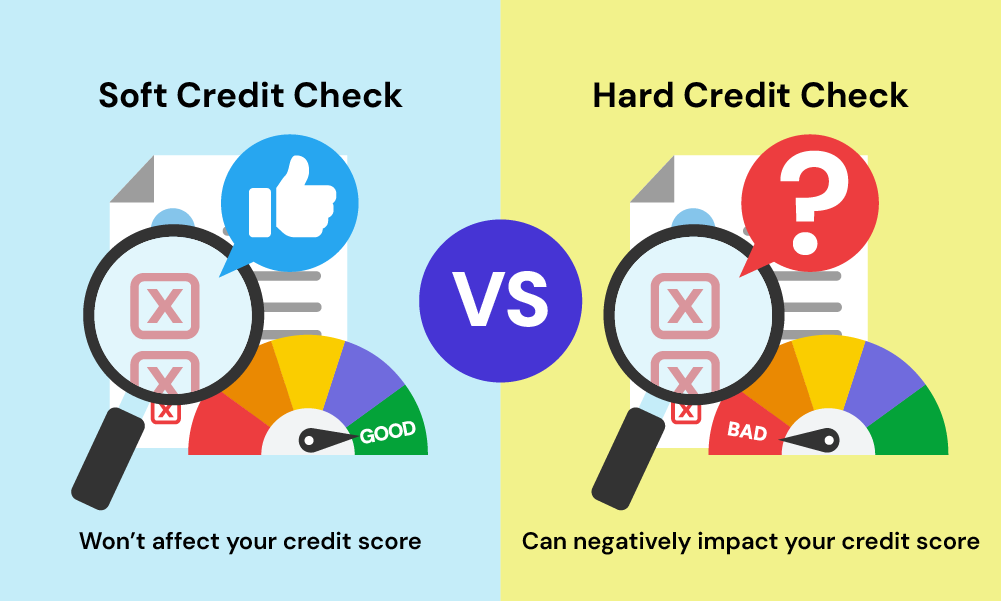

The lender will ask about your income, your outgoings, and your financial history. They’ll also perform a credit check.

This could be a ‘soft’ check, which doesn’t leave a mark on your credit file, or a ‘hard’ check, which does. Make sure you know which one the lender will perform.

Be honest in your application. It might be tempting to paint a rosier picture of your finances, but remember, any discrepancies will come out in the full mortgage application later. 😀

4. Receive Your AIP

If all goes well, you’ll receive your AIP. This usually happens quickly – often within hours, sometimes even minutes if you’re applying online.

Your AIP will tell you how much the lender is willing to let you borrow. Again, it’s not a binding offer, but it’s a good indication of what you might be able to secure when you make a full mortgage application.

Remember, just because a lender offers you a certain amount doesn’t mean you should borrow that much.

Consider your own budget and what you’re comfortable repaying each month.

How Long is a Mortgage in Principle Valid?

Typically, an AIP is valid for between 60 and 90 days.

This gives you a decent window to house hunt, but it’s not forever. If your search takes longer, you might need to get a new AIP.

This isn’t necessarily a bad thing – your financial situation might have improved, potentially increasing the amount you can borrow.

Keep in mind that the property market can change quickly. Interest rates might shift, lending criteria could tighten.

Your AIP is a snapshot of what you could borrow at a particular moment in time.

Does a Mortgage in Principle Affect Credit Score?

This is a common concern, and the answer is: it depends.

Some lenders perform a ‘soft’ credit check for an AIP. This doesn’t leave a footprint on your credit file and won’t affect your score.

Others might do a ‘hard’ check, which does show up on your credit report. Too many hard checks in a short period can negatively impact your credit score.

Always ask the lender which type of check they’ll perform. If you’re shopping around, try to stick with lenders who do soft checks for AIPs.

Remember, a single hard check isn’t likely to dramatically affect your score. It’s multiple checks in a short time that can raise red flags for lenders.

How Many Times Can I Get an Agreement in Principle?

Technically, you can get as many AIPs as you like. There’s no rule saying you can only have one at a time.

However, it’s generally not advisable to apply for multiple AIPs simultaneously. Here’s why:

- If lenders are performing hard credit checks, multiple applications could harm your credit score.

- Different lenders might offer different amounts, which could be confusing when you’re trying to set a budget.

- More isn’t necessarily better. One or two AIPs from reputable lenders should be sufficient.

If your circumstances change significantly or your AIP expires before you find a property, then it makes sense to get a new one.

Otherwise, stick with what you have.

How To Handle a Mortgage in Principle Rejection

First, don’t panic. A rejection doesn’t mean you’ll never get a mortgage. Think of it as an opportunity to reassess and improve your financial situation.

Here’s what you can do:

- Find out why. Lenders should give you a reason for the rejection. Understanding the ‘why’ is crucial for your next steps.

- Check your credit report. There might be errors or issues you weren’t aware of. Addressing these can improve your chances next time.

- Improve your financial health. Pay down debts, increase your savings, or look for ways to boost your income.

- Wait and try again. Sometimes, time is all you need. If you can wait a few months and improve your finances, you might have better luck.

- Consider alternative lenders. Some specialise in mortgages for people with less-than-perfect credit histories.

- Speak to a mortgage broker. They might be able to find a lender more suited to your circumstances.

Remember, a rejection isn’t a judgement on you as a person. It’s a financial decision based on the lender’s criteria at that moment.

The Bottom Line

A Mortgage Decision in Principle is your first real step on the property ladder.

It gives you clarity about your budget, boosts your credibility with sellers, and helps you move quickly when you find the right property.

Remember, getting a DIP doesn’t guarantee a mortgage, and a mortgage offer doesn’t oblige you to borrow. It’s a tool, not a commitment.

Use it wisely, and it could be the thing that helps you find and secure your dream home.

So, before you start viewing properties, take this important step. Get your finances in order, gather your documents, and apply for that Decision in Principle.

Unsure where to start? Get in touch. We can help you apply for a mortgage in principle by matching you with a qualified mortgage broker. They can simplify this process and help you get onto the property ladder with confidence.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How reliable is a mortgage in principle?

An AIP is a good indicator of what you might be able to borrow, but it’s not a guarantee. Lenders can still change their minds when you make a full mortgage application.

However, if your circumstances haven’t changed and you were honest in your AIP application, it’s usually a reliable guide.

Can I apply for an AIP online?

Absolutely! Many lenders offer online AIP applications. It’s often quicker than applying in person or over the phone.

Just make sure you have all your documents and information ready before you start.

Do I need to pay to get an Agreement in Principle?

Generally, no. Most lenders offer AIPs for free. They see it as part of their customer service and a way to attract potential borrowers.

However, if you’re using a mortgage broker, they might charge a fee for their services, which could include securing an AIP.

How long does it take to get a mortgage in principle?

The process can be surprisingly quick. If you’re applying online and have all your information ready, you could get an AIP in as little as 15 minutes.

Even if you’re applying in person or over the phone, it rarely takes more than a few hours.

However, in some cases, it might take a day or two if the lender needs to verify any information.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]