- What is a Woodland?

- Can You Get a Mortgage to Buy Woodland in the UK?

- Why Buy a Woodland?

- How Do Woodland Mortgages Work?

- What Are Your Options for Buying a Woodland?

- What Are the Costs Involved in Buying a Woodland?

- Can You Live in Your Woodland?

- How to Get Started with a Woodland Mortgage

- Refinancing a Woodland Mortgage

- Key Takeaways

- The Bottom Line: Are Woodland Mortgages Worth It?

Mortgages For Woodland: A Full Guide To Buying a Woodland

Picture this: you wake up to birds chirping softly and sunlight filtering through leafy branches.

You feel calm, breathing in the fresh woodland air.

Your kids are off exploring, finding sticks and spotting squirrels, while you sit back with a warm cup of tea, soaking in the peace and quiet.

If this sounds like your idea of a perfect escape from the city, you might be dreaming about owning your own woodland in the UK.

But here’s the catch: getting a mortgage for woodland isn’t quite the same as for a regular house. It can be a bit tricky, with different rules and a few extra hoops to jump through.

No need to worry, though. In this guide, we’ll break it all down simply, covering what you need to know to make that woodland retreat a reality.

What is a Woodland?

In the UK, woodland simply means a piece of land mostly covered in trees.

Picture it as nature’s little oasis—filled with a mix of broadleaf and conifer trees, offering a perfect setting for wildlife, camping, or a quiet walk.

Woodlands are all over the UK, with some famous spots in Scotland (Caledonian Forest), Wales (Snowdonia!), and England (the New Forest or Sherwood Forest).

Can You Get a Mortgage to Buy Woodland in the UK?

Yes, you can, but it’s a bit different from getting a standard mortgage. If you walk into your usual bank and ask about a woodland mortgage, you might get a puzzled look.

Woodland mortgages are more specialised—meaning you’ll need a lender who understands woodland purchases because they don’t carry the same “resale value” as a typical house.

People buying woodland tend to be nature enthusiasts, conservationists, or those with plans for a forestry or tourism business.

Depending on your goals, you might need a particular type of mortgage: a woodland mortgage, commercial mortgage, or even an agricultural mortgage if you’re planning to sell timber.

Each one has its own rules, interest rates, and conditions. We’ll explain these in more detail shortly.

Why Buy a Woodland?

Woodlands are often romanticised. Think of camping under the stars, nature walks, and beautiful wildlife.

But owning a woodland can also be practical and even profitable. Some people buy woodland as an investment, hoping the value of the land will grow.

Others might look at starting a business, such as selling timber, setting up a glamping site, or even offering educational nature retreats.

And let’s not forget the environmental benefits. Buying woodland to conserve it means you’re doing your bit for biodiversity, which is quite the legacy to leave behind.

How Do Woodland Mortgages Work?

Woodland mortgages aren’t quite the same as your usual home loan. Unlike a house, a woodland doesn’t have walls or a roof you can easily sell, so lenders see it a bit differently.

They look at things like where it is, how easy it is to access, and whether you might make some income from it. Perhaps by selling timber or running a small business.

Since woodlands come with extra risks, interest rates for these mortgages can be a bit higher than for regular home loans.

Plus, you’ll usually need a 30% deposit, as most lenders cap woodland loans at 70% of the land’s value.

They’ll also ask about your plans for the land. Are you thinking of enjoying it for yourself, conserving the area, or perhaps earning some extra cash?

If you’ve got bigger plans—like timber production or even ecotourism—a commercial or agricultural woodland mortgage might be a better fit.

These are designed for woodlands that can bring in income, and you’ll likely need a solid business plan to show the lender you’re prepared.

What Are Your Options for Buying a Woodland?

Depending on your plans, you’ve got a few different ways to go about buying woodland:

Woodland Mortgage

If you’re looking to own a small bit of woodland for relaxation or conservation, a woodland mortgage is often the easiest route.

It’s a great option if you just want a peaceful spot to escape to on weekends or to enjoy some nature without big business plans.

Commercial or Agricultural Mortgage

Got a business idea for your woodland, like selling timber or setting up a glamping site?

Then a commercial or agricultural mortgage might be your best match.

Lenders will want to see how you plan to make money from the land, so get ready to wow them with your woodland dreams.

Equity Release or Remortgage

Already own a home? One option is to remortgage or release some of the equity in your property to fund the woodland.

Residential mortgages tend to have lower interest rates, so this can sometimes be a cheaper route. Just make sure you have enough equity to cover a good part of the woodland’s price.

SIPP (Self-Invested Personal Pension)

Some people use their pensions to buy woodland, though it’s a bit more complex.

If your pension allows for this, a SIPP can be a tax-efficient way to own land, but you’ll need advice, as the rules are strict.

Cash Purchase

If you have the funds, buying with cash is also an option.

It skips the hassle of dealing with lenders and can speed things up, though it does require a solid upfront amount.

What Are the Costs Involved in Buying a Woodland?

Woodlands aren’t cheap.

The price depends on several factors, including location, size, and the quality of the trees.

You’re looking at around £10,000 per acre, but this can vary greatly. Remember that additional costs also include legal fees, survey fees, and any work you might want to do on the land.

On top of the purchase price, interest rates for woodland mortgages can be higher than what you might be used to, often around 1.5%-2% above the Bank of England base rate.

The interest is high partly because selling woodland is more challenging, meaning it’s riskier for lenders.

Also, if you’re planning on remortgaging an existing property to buy a woodland, watch out for early repayment fees on your current mortgage—this could eat into your budget.

Income Multiples and Loan Calculations

How much you can borrow will also depend on your income. Lenders often use income multiples to determine the borrowing limit.

For example:

- 3x Salary: If you earn £40,000, you may be able to borrow up to £120,000.

- 4x Salary: For an income of £50,000, you could potentially borrow £200,000.

- 5x Salary: With an income of £60,000, your borrowing potential might be up to £300,000.

These figures are just examples, and the actual amount you can borrow will depend on various factors, including your overall financial health and the specifics of the woodland you wish to purchase.

Can You Live in Your Woodland?

No, not really. You can’t just pop up a cabin and call it home.

Most woodland mortgages come with restrictions that prevent you from building a permanent dwelling.

However, you may be able to set up a temporary structure—think along the lines of a cosy cabin used occasionally for maintaining the land or camping.

If you’re serious about building a home, you’ll need to apply for planning permission, and that’s easier said than done.

Local councils are often reluctant to approve permanent dwellings in woodlands, given the impact on the environment.

But don’t let that dampen your dreams too much—there’s always a way if you’re determined enough (and have a good lawyer).

How to Get Started with a Woodland Mortgage

Here are the key steps to help you get the mortgage you need for your woodland purchase:

- Get Clear on Your Plans. Before you even start looking at woodlands, get clear on what you want to do with the land. Are you buying it for conservation? Planning to build a nature retreat? Knowing what you want will help you choose the right type of mortgage.

- Speak to a Specialist Broker. Woodland mortgages aren’t something your average high-street bank deals with, so you’re best off speaking to a specialist broker. They have the contacts and know-how to connect you with lenders that understand this kind of purchase. We offer a free broker-matching service to help you find the right expert for your needs.

- Gather Your Documents. As with any mortgage, you’ll need to provide proof of identity, address, income, and details about your financial situation. If you’re going for a commercial mortgage, you’ll also need a solid business plan.

- Start Your Application. Once you have all your documents sorted and your broker has helped you find the right lender, it’s time to apply. Be prepared for a bit of back and forth—these kinds of mortgages can take longer to get approved compared to a regular house mortgage.

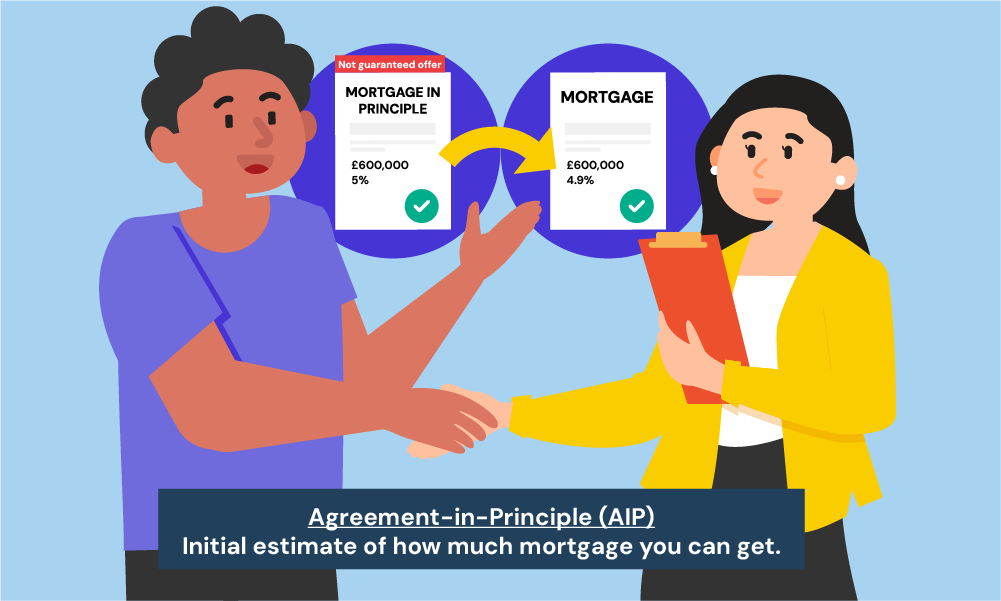

Do You Need an AIP for a Woodland Mortgage?

An Agreement in Principle (AIP) is a document from a lender that estimates how much they’re willing to lend you. It’s based on your financial information.

While it’s not a formal mortgage offer, an AIP is a valuable tool for woodland buyers. Here are the reasons why it’s best to get one:

- It helps you understand your budget.

- It signals to sellers that you’re a serious buyer.

- You can focus on woodlands within your budget.

- It gives you an edge in negotiations.

- It can make the full mortgage process quicker, as lenders have already reviewed your information.

In short, an AIP can save you time, improve your buying position, and streamline the entire mortgage process.

Refinancing a Woodland Mortgage

If you already own woodland and are looking for better mortgage terms, refinancing is an option.

Remortgaging onto a better deal with your existing lender can be beneficial, especially if they are already familiar with the property. But, watch out for early repayment fees that might apply.

In some cases, there might be new lending options available that weren’t around when you first took out your loan.

A specialist broker can provide insights into the current market and help you decide whether it’s worth switching lenders.

Key Takeaways

- Buying woodland in the UK can be a dream come true, but woodland mortgages are niche products requiring specialist lenders.

- There are different financing options depending on your intentions—whether for conservation, personal use, or business.

- LTV for woodland mortgages is typically 70%, meaning you’ll need at least a 30% deposit.

- Interest rates are often higher for woodland mortgages compared to standard residential ones.

- You generally can’t live on woodland without planning permission, which is difficult to obtain.

- Typical borrowing limits are based on income multiples, with loans often capped at 3-5 times your salary.

The Bottom Line: Are Woodland Mortgages Worth It?

That really depends on your goals.

If you’re a nature enthusiast who dreams of spending weekends surrounded by trees, it could be a rewarding purchase.

For those planning to make money—whether through timber sales, a business venture, or simply holding the land as an investment—it could also pay off in the long run.

Just make sure you go in with your eyes open: woodland mortgages aren’t as simple as residential ones, and there’s a bit of red tape involved.

If you’re still not sure, a specialist broker can give you a clearer idea of whether a woodland mortgage fits your financial goals and lifestyle.

Need a broker? Get in touch with us. We’ll help you get match with a qualified mortgage broker specialising in woodland mortgages in the UK.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

How much deposit do I need for a woodland mortgage?

Typically, you’ll need at least a 30% deposit, as lenders often cap the Loan-to-Value (LTV) ratio at 70%.

Can I build a cabin on woodland?

Usually, you can only build temporary structures for occasional use, such as a small cabin for camping. Permanent dwellings require planning permission, which is often hard to get.

Are there tax advantages to owning woodland?

Yes, commercially managed woodland is exempt from inheritance tax after two years. Income from timber sales is also exempt from income tax and capital gains tax.

Can I get a mortgage for large acreages in the UK?

Yes, but it’s more challenging. Large acreages, typically over 10 acres, require specialist lenders, as mainstream lenders usually stick to properties up to three acres.

Lenders like Atom Mortgages or Bluestone Mortgages may consider larger plots, but they’ll want to know how you plan to use the land.

For commercial use, such as timber, glamping, or farming, you’ll likely need a commercial or agricultural mortgage, which requires a clear business plan.

A specialist mortgage broker can be a big help, as they know lenders who deal with large land purchases and can match you with the best options.

Related Articles

What To Do If Mortgage Survey Is Lower Than Expected

Buying, selling, or remortgaging a home already has plenty of steps. Then, just when things seem on track, the surveyor steps in to assess the property’s worth. Sometimes, though, they give a lower number than you hoped, and that can cause problems. Especially if you’ve planned your budget and are expecting a good mortgage offer. […]

Should You Buy a Timber Framed House in the UK?

Buying a timber-framed home? Timber-framed homes are more than just a trend. They bring eco-friendliness, great insulation, and a charm that’s hard to find in conventional builds. Plus, they’re faster, easier, and often cheaper to construct. For a first-time buyer, that’s a lot of pros. And if you’re wondering whether these properties are mortgageable in […]

How To Buy a Studio Flat: A Complete Mortgage Guide

Are you looking for a home that’s cosy, low-maintenance, and close to everything? For many, a studio flat ticks all these boxes—compact, cosy, and close to the action. But getting a mortgage for one can be trickier than you might think. Lenders often get picky with smaller spaces, and that’s where a little know-how can […]