- What is a Mortgage Offer?

- How Long Is a Mortgage Offer Valid For?

- Why Do Mortgage Offers Expire?

- Can I Extend My Mortgage Offer If It’s About to Expire?

- Can My Lender Withdraw an Expired Mortgage Offer?

- How to Avoid Your Mortgage Offer Expiring

- What If My Mortgage Offer Does Expire?

- Are New-Build Mortgage Offers Different?

- How Mortgage Offers and Agreements in Principle Differ

- The Bottom Line

What Happens If My Mortgage Offer Expires?

You’ve done it all – provided stacks of financial documents, passed the credit checks, and paid those pesky arrangement fees.

Finally, you receive that life-changing piece of paper – your mortgage offer.

Pop the champagne and celebrate because your journey to homeownership is nearing its sweet conclusion, right?

Not so fast! That mortgage offer isn’t set in stone forever. It comes with an expiration date that you need to watch closely.

Missing that date can disrupt your purchase and mean starting the application process all over again.

This guide explains everything about mortgage offer expiration dates in the UK. From how long they last and getting extensions to what to do if you miss the deadline.

With this knowledge, you can confidently manage your mortgage timeline and get those keys to your new home.

What is a Mortgage Offer?

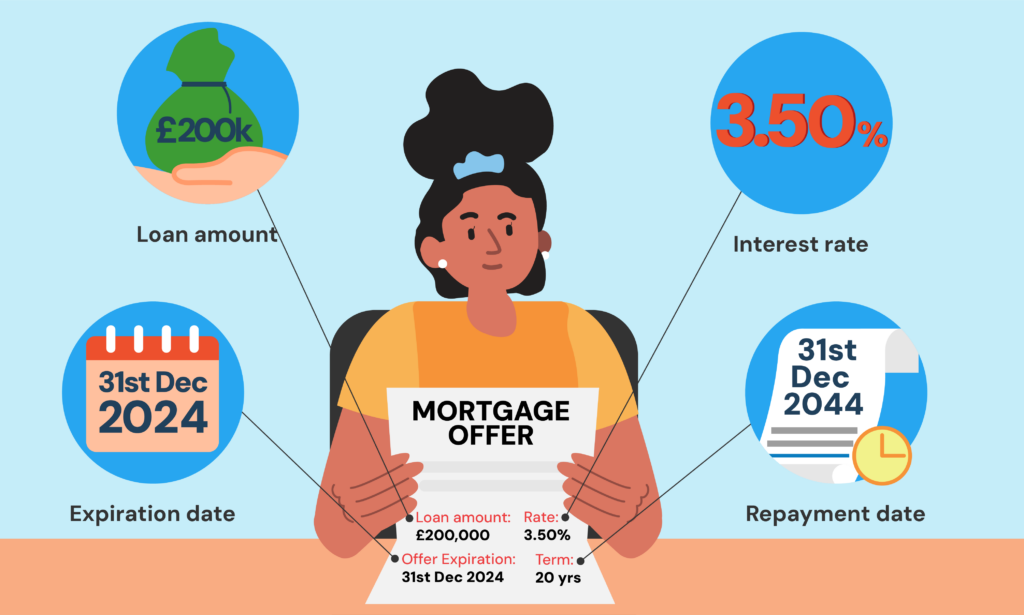

A mortgage offer is a lender’s formal approval to provide you with a home loan, assuming you meet all the stated terms and conditions. It confirms that your full application – your finances, credit, income, deposit, and property – has passed the lender’s criteria.

This checking process can take from 2-6 weeks, depending on your application’s complexity.

The offer letter details the loan amount, interest rate, repayment terms, and the expiration date by which you must complete your property purchase before the offer expires.

How Long Is a Mortgage Offer Valid For?

Most mortgage offers from UK lenders are valid for 3-6 months, though the precise expiration period can vary.

Some lenders start the clock ticking from the date you applied, while others use the date the offer was formally issued.

Either way, keeping close tabs on that expiry date is crucial because your home purchase needs to be completed before the offer runs out.

If not, you’ll likely need to renew your mortgage application, resubmit updated paperwork and potentially face another credit check that could impact your score.

Why Do Mortgage Offers Expire?

The main reason lenders attach an expiry date is to ensure your financial situation hasn’t significantly changed since your initial application.

A lot can happen in a few months – a new job, a shift in income, increased debts or expenses. The lender wants to verify this information is still accurate before releasing those mortgage funds.

Additionally, real estate deals often face delays from solicitors, surveyors, or sellers. A few months gives you that extra breathing room to get the legalities settled without stressing over the mortgage side.

Can I Extend My Mortgage Offer If It’s About to Expire?

Ideally, your mortgage and property purchase would align perfectly, with keys in hand well before the offer expires.

But, we all know how unpredictable the process can be.

Construction delays, solicitor backlogs, tough sellers – any number of things can put your completion date close to the offer’s expiration.

The good news? Most mortgage lenders understand this and are willing to grant extensions if you notify them before the offer lapses.

Exactly how much extra time they’ll allow can vary, but 3-6 additional months is typical.

It’s crucial to be proactive once you see that completion may be cutting it close. Don’t wait until the 11th hour.

Give your lender advance notice (30-60 days is advisable) about the situation and request that extension. They’ll likely need you to reconfirm some financial details before approving it.

Can My Lender Withdraw an Expired Mortgage Offer?

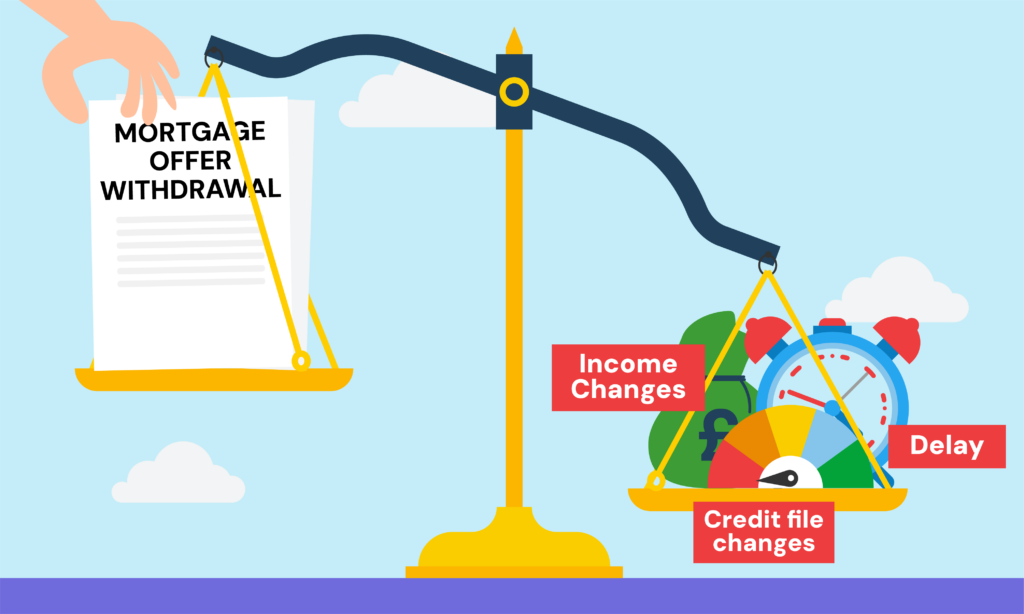

Yes, lenders can withdraw an expired mortgage offer, especially if too much time has passed.

Once that expiration date hits, whether or not they’ll still honour the initial offer comes down to a case-by-case review.

If only a few weeks have passed and your financial situation is stable, most lenders will likely grant a renewal or extension upon reapplication.

However, significant delays or major changes to your income or credit profile may cause them to reconsider.

At the end of the day, lenders need to protect themselves from excessive risk. An expired mortgage offer signals a potentially riskier investment or complications. They have to do their due diligence again.

How to Avoid Your Mortgage Offer Expiring

Clearly, it’s in your best interest to complete your mortgage well before that expiration date to avoid any issues or re-application hassles.

While delays can happen, you can keep your mortgage on track with these tactics:

- Find a mortgage offer with a long offer period, especially for new-builds.

- Use a good solicitor/conveyancer who is responsive and can move quickly

- Stay on top of providing information/documents to your lender promptly

- Have a chat with the seller about mutually agreeable completion timelines

- Consider getting a good mortgage broker involved to professionally co-ordinate all parties

Most importantly, be upfront with your mortgage lender from day one about any potential delays. The more they know, the smoother any extensions or reapplications can be handled down the line.

What If My Mortgage Offer Does Expire?

So despite your best efforts, the completion date came and went without those front door keys in hand. Your mortgage offer has officially expired – now what?

First, don’t panic!

As long as your overall financial picture and credit rating haven’t significantly worsened, you should still be able to get a new mortgage approval, even with the same lender.

However, you’ll need to restart the process.

You’ll likely need to resubmit documentation like bank statements, payslips, etc. and go through a new credit check and affordability assessment.

If the lender’s mortgage rates or your home’s valuation has changed, your new offer could end up looking quite different too.

Using an experienced mortgage broker can really help smooth out this renewal process. They’ll be able to review the current mortgage market, renew applications quickly with multiple lenders if needed, and ensure you get the best deal despite the delays.

Are New-Build Mortgage Offers Different?

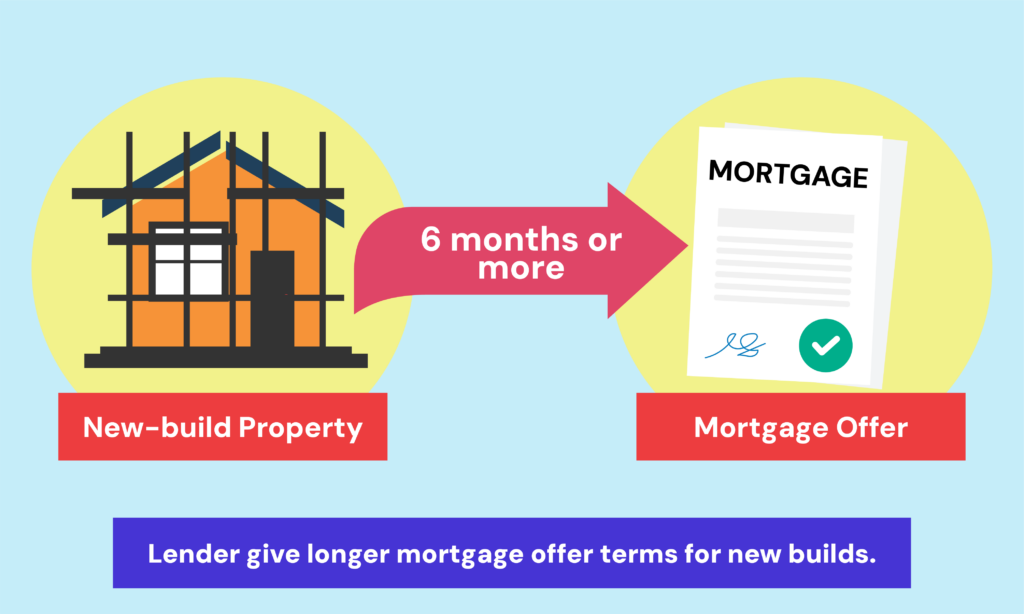

Yes, the process for new-build mortgage offers can be different.

When you purchase a new build, you might receive a fixed completion date from your developer, but some may work on a “completion on notice” basis. This means you won’t know the exact date until the property is structurally sound.

To account for these potential delays, lenders typically offer longer validity periods on new-build mortgages, sometimes lasting 6 months or more.

Another difference is phased payments. If you’re buying “off-plan” (before it’s built), you might need to make payments as construction progresses. This can affect your finances and how you structure your mortgage.

Finally, expect multiple valuations during construction to ensure the property value keeps pace with the loan amount.

Be prepared for possible delays due to construction hiccups. Clear communication with your solicitor and lender is key throughout the process.

How Mortgage Offers and Agreements in Principle Differ

It’s important not to confuse a full mortgage offer with a mortgage agreement in principle (AIP) or a decision in principle (DIP). These are two very different beasts in the home-buying journey.

An agreement in principle, typically valid for 60-90 days, is a lender’s initial indication that they’d likely lend you a certain amount based on a basic financial check. It’s not a firm offer but shows sellers you can probably secure financing.

A mortgage offer, however, comes after your full application is reviewed and approved for a specific property. It authorises the release of mortgage funds upon completion of the purchase.

In short, the AIP is an early nod of approval, while the mortgage offer is the final go-ahead. The latter is more decisive but comes with a strict time limit.

The Bottom Line

As a UK homebuyer, it’s crucial to stay aware of your mortgage offer’s expiration date. Keeping your completion on track avoids stressful re-applications and extra costs.

Communicate clearly with your lender about any anticipated delays. If the date is looming, be proactive in requesting an extension. And if it does expire, explore all your renewal options—your dream home may still be within reach!

If you’re not careful, you might face delays, added costs, and the hassle of reapplying for your mortgage. This is where a mortgage broker becomes invaluable. They can anticipate potential issues, provide expert advice, and take swift action to keep everything on track.

A good mortgage broker can make this journey smoother by handling the complexities, managing paperwork, and getting the best deal for you.

Need a broker? Get in touch with us. We’ll connect you with a qualified mortgage broker to ensure you stay on track and secure your home loan without a hitch.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can my mortgage offer be transferred to another property?

Most mortgage offers in the UK are conditionally approved for that specific property. If you change properties entirely, even with the same lender, you’ll typically need to re-apply and get full underwriting approval again based on the new home’s details and valuation.

Do mortgage lenders do final checks before completion in the UK?

Yes, mortgage lenders perform final checks before completion in the UK. They verify that your financial situation hasn’t changed since the initial approval.

This includes checking your employment status, credit score, and any significant financial changes. These checks ensure that the lender’s risk assessment remains accurate before releasing the funds for your property purchase.

How long does it take to complete the purchase after a mortgage offer?

Completing the purchase after receiving a mortgage offer typically takes one to two weeks, but it can extend to several weeks or even months.

This depends on factors like your solicitor’s efficiency, property issues, the seller’s readiness, and accessing funds for the deposit.

The key is to ensure all paperwork is promptly handled and any potential delays are communicated early to keep the process on track.

Related Articles

How Quickly Can You Sell a House in the UK?

If you’re thinking about putting your place on the market, you’re probably curious about how long it might take. Spoiler alert: there’s no exact timeline! It all depends on a few things, like the state of your property and how active the housing market is. On average, though, selling a house in the UK can […]

What Do I Need To Declare When Selling My Home?

Why You Need To Disclose Your Property’s Condition & History Disclosing your property’s condition and history in the UK is both legally required and builds trust with buyers. You must be upfront about any issues to avoid lawsuits under the Consumer Protection from Unfair Trading Regulations (CPR). Failure to do so could result in prosecution, […]

Mortgage Exit Fees Explained

What Is a Mortgage Exit Fee? A mortgage exit fee is an administration charge your lender hits you with when you pay off your mortgage in full before the end of the agreed term. So whether you’re remortgaging, moving house and porting your mortgage, or making lump sum overpayments to clear the balance early, there’s […]