- What Is a Bridge to Let Mortgage?

- Who Should Consider a Bridge to Let Mortgage?

- How Much Can I Borrow?

- Benefits of Bridge-to-Let Mortgages

- Risks and Considerations of Bridge to Let Mortgages

- What Are Possible Exit Strategies For A Bridge To Let?

- What Interest Rates Can I Expect?

- How To Apply for a Bridge to Let Mortgage?

- How Much Do Bridge To Let Mortgages Cost?

- Can I Still Get Approval With Bad Credit?

- Can I Use a Bridge To Let For Home Improvements?

- Key Takeaways

- The Bottom Line

Bridge To Let Mortgages Explained: Is It For You?

Bridge-to-let mortgages are short-term finance options designed for property investors in the UK.

They’re quite the buzz in the property market, offering a bridge between buying a property and securing long-term finance.

In this piece, we’ll walk you through what bridge to let mortgages are, their benefits, and how they differ from traditional mortgages.

If you’re eyeing the property market, this read is for you.

What Is a Bridge to Let Mortgage?

A bridge-to-let mortgage is a short-term loan that bridges the gap until you get a buy-to-let mortgage on a property.

Bridge to let is ideal for acting fast in a competitive market, like buying at an auction or fixing up a property to rent.

Here are the standout features:

- Short-term, usually less than 2 years

- Interest is often rolled up, meaning you pay it all at the end

- Quick to arrange, making them perfect for auction purchases or refurb projects

- Usually has higher interest rates

- Works for residential or commercial properties

- Needs an exit strategy, either to refinance to a buy-to-let mortgage or rent the property

When securing bridge-to-let mortgages, lenders will factor in your expected rental income to make sure it covers the loan costs.

Who Should Consider a Bridge to Let Mortgage?

Bridge-to-let mortgages are ideal for investors who need to move fast or can’t get a standard buy-to-let mortgage. Here are some situations where they shine:

- Property developers looking to quickly buy, develop, and rent or sell a property.

- Landlords who want to refurbish a property either sell or rent it out.

- Investors who need fast financing to secure a property at auction.

- Buyers who encounter limitations with standard buy-to-let mortgages, like for properties needing renovation.

- Investors who prefer a short-term loan or have capital tied up elsewhere.

- Anyone planning to convert their buy-to-let property to an HMO.

- Commercial buy-to-let investors.

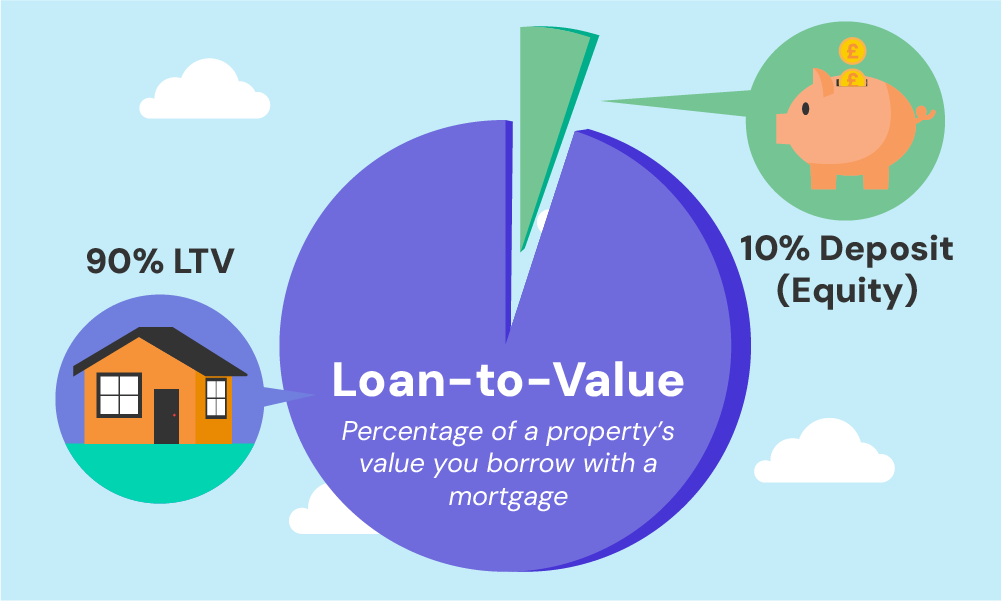

How Much Can I Borrow?

You can borrow at least 70% of your property’s value with most lenders. This is called the loan-to-value (LTV) ratio. The exact amount depends on your property value, property investment experience, and your exit strategy.

For interest, you can either pay monthly or roll it into the loan. Rolling it up might avoid immediate affordability checks if you have a good exit plan, but monthly payments require proving you can afford them.

Benefits of Bridge-to-Let Mortgages

Opting for a bridge to let mortgage comes with several advantages:

- Get pre-approved exit finance. Prove your ability to repay with a future buy-to-let mortgage.

- Become a more attractive buyer. Complete faster with bridge-to-let’s quicker turnaround times.

- Bridge the sales gap. Buy a new property before selling your existing one, avoiding chain delays (subject to affordability checks).

- Fast access to funds. Perfect for quick property purchases or refurbishments.

- Potential for property value increase. Renovations during the bridge-to-let period could boost your profits.

- Secure auction properties. Act fast and win at auctions with bridge-to-let financing.

Risks and Considerations of Bridge to Let Mortgages

Using a bridge to let mortgage has its disadvantages too. Be mindful of:

- Higher Costs. Expect higher interest rates and fees than traditional mortgages due to the short-term, flexible nature of the loan.

- Risk of negative equity. Property values can fluctuate. If the property value falls during your bridge-to-let term, you might owe more than the property is worth.

- Risky if the Exit Strategy Fails. If your plan to refinance or sell the property falls through, you might face financial difficulties.

- Potential for vacant property. If you struggle to find tenants quickly, you’ll be responsible for the mortgage repayments and any property costs without rental income to offset them.

- Short Repayment Term. These loans are short-term, which means you’ll have a shorter window to repay the loan compared to a standard buy-to-let mortgage.

- Not Suitable for Long-Term Financing. These are not long-term solutions and are best used as a temporary fix for specific situations.

Before considering a bridge to let mortgage, consulting with a specialist accountant is advisable to fully understand the tax benefits and implications for your situation.

What Are Possible Exit Strategies For A Bridge To Let?

As we’ve discussed, bridge-to-let loans are short-term and cost more than regular mortgages. You need a good exit strategy to repay them on time.

These loans must be repaid in full, usually by selling the property.

If you can’t repay, your credit score will suffer. Here’s what to do if your plan goes wrong:

- Extend the loan. Talk to your lender about extending the loan term, but only if they agree and you haven’t borrowed the maximum amount against your property value (LTV ratio).

- Refinance. You can switch to a different lender, but this means new fees and another exit plan. Make sure it’s a long-term solution to avoid future problems.

- Sell the property. If you can’t repay, the lender might repossess the property. This will hurt your credit score and make it harder to borrow money in the future.

To manage a bridge to let loan responsibly, have a backup plan and understand all the possible outcomes.

What Interest Rates Can I Expect?

Bridge to let interest rates can be anywhere from 0.4% to 1.5% each month, much higher than regular mortgages.

Unlike traditional mortgages with annual rates, bridge-to-let mortgages typically use monthly rates due to their short-term nature.

Several factors affect these rates, including the loan-to-value (LTV) ratio, property condition, your credit history, and the lender’s perceived risk.

A lower LTV ratio, meaning you borrow a smaller portion of the property value, can result in more favourable rates.

This translates to lower risk for lenders because there’s more equity in the property. The property’s condition also plays a significant role.

Properties requiring extensive refurbishment might incur higher rates due to the added risk of renovation projects.

Your credit history is another crucial factor.

While bridge-to-let mortgages are available to those with bad redit, a stronger credit score can help you secure lower interest rates.

A good credit history signifies reliability to lenders, reducing their risk.

To obtain the best rates, you’ll need to present a strong application.

This includes a solid exit strategy, demonstrating how you plan to repay the loan, either through refinancing to a long-term mortgage or selling the property.

Comparing offers from various lenders can also help you find more competitive rates.

How To Apply for a Bridge to Let Mortgage?

Applying for a bridge to let mortgage involves a few key steps and requires meeting certain criteria.

Here’s what you need to know to get started:

Eligibility Criteria

To be eligible for a bridge-to-let mortgage, you’ll generally need to meet the following requirements:

- A good credit score (depending on the lender)

- A clear and solid exit strategy (e.g., refinancing to a buy-to-let mortgage or renting the property)

- A minimum property value (set by the lender)

- Enough experience as a landlord (lenders may have requirements)

- A viable financial plan demonstrating your ability to repay the loan

- The projected rental income from the property should cover the mortgage repayments (at least 125% in some cases)

- Sufficient equity in the property or a substantial deposit at least 30% of the property price.

- Some lenders may require income proof to cover interest payments and any unforeseen costs.

Each lender has their own criteria for these mortgages. Typically, you can get approval within 24-48 hours as long as you meet their criteria.

Required Documentation

When applying, you’ll need to provide:

- Your passport and a recent utility bill for proof of identity and address.

- Details of your income, expenses, and any current mortgages or loans for financial information.

- Property details its value and your plans for it under property details.

- Your personal details such as your age, job, and where you live.

- Proof of experience as a landlord (if required by the lender).

- Proof of your plan to repay the loan, such as refinancing to a buy-to-let mortgage or selling the property.

- Details about any other assets you own that could be used for security (if applicable).

- Proof you can afford the monthly repayments, if applicable.

- Some lenders might check if the property can be sold easily, especially if you don’t finish planned fixes, known as resale potential.

Application Process

Once you’ve prepared the necessary documents, it’s highly recommended to consult an experienced mortgage broker to help you with your application.

You can discuss with them any concerns you have regarding your finances and mortgage choices. They can offer you personalised advice about the best exit strategy for your situation.

They can also recommend lenders and help with the application process, from submitting your application to completion.

For a quick, free, and no-obligation consultation with a reputable mortgage broker, get in touch with us.

How Much Do Bridge To Let Mortgages Cost?

Let’s not forget the cost…

As an investor, you want to make sure this is a profitable venture. So it’s important to account for all the costs.

Here’s what to expect:

- Arrangement Fees. Also known as facility fees, these are set by the lender for arranging the loan, often up to 2% of the loan value.

- Interest Rates. Typically higher than those for traditional mortgages, reflecting the loan’s short-term nature. These can be fixed or variable.

- Valuation Fees. For assessing the property’s value to determine the loan amount.

- Exit Fees. Some lenders might charge around 1% of the loan value when you repay the loan.

- Broker Fees. If you use a broker to find your loan, they may charge a fee for their services.

- Legal Costs. Includes conveyancing for the property purchase and any refinance process, covering legal aspects and paperwork.

All these fees should be clearly outlined by the lender beforehand, allowing you to assess the loan’s affordability and how it fits into your investment strategy.

Can I Still Get Approval With Bad Credit?

You might be able to get a mortgage with bad credit, but it’s not a sure thing.

While having good credit is always better, some lenders are willing to look past a low credit score. They’ll focus more on the property, your plan for repaying the loan, and the details of your credit issues—like how serious they were and how long ago they happened.

If your credit isn’t great, you might have to pay higher interest rates, and some lenders might ask for a bigger deposit to reduce their risk.

A specialist mortgage broker can help you find lenders who are more open to working with people in your situation.

Just keep in mind that getting approved will depend on your financial situation, how well you meet the lender’s requirements, and what mortgages are available at the time.

Can I Use a Bridge To Let For Home Improvements?

Yes, you can use a bridge to let mortgage for home improvements.

This type of mortgage is ideal for properties that need work before being rented out. Traditional lenders may avoid these properties, but bridge loans are designed for such situations.

Specialist lenders will assess the viability of the project, considering the potential increase in value after renovations.

Once the property is up to standard, you can switch to a buy-to-let mortgage and start renting it out.

Key Takeaways

- A bridge-to-let mortgage is a short-term loan to help you quickly buy a property, fix it up, and then rent it out or sell it. It’s great for property investors, landlords, or anyone buying at auction or renovating homes.

- When applying for bridge-to-let, you must have a clear plan to repay the loan, like remortgaging to buy-to-let mortgage or selling the property. Without a good plan, you could face extra costs or financial trouble.

- These loans have higher interest rates than residential mortgages. The better your credit score and property value, the lower your rates might be.

- Bad credit doesn’t rule you out, but expect stricter terms, higher rates, or larger deposits. While not guaranteed, a good broker can guide you to lenders willing to work with your situation.

The Bottom Line

While bridge-to-let mortgages can be a valuable tool for property investment, they do come with risks. Having a clear exit strategy and considering the costs is important.

If you’re considering a bridge to let mortgage, talking to a mortgage advisor is a good next step. They can provide personalised advice and help tailor a solution to your needs.

Want to find out more about bridge-to-let mortgages? Contact us and we’ll connect you with a reputable mortgage broker who specialises in this area. They can give you expert advice tailored to your investment goals.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is there a minimum loan amount for bridge to let mortgages?

This varies by lender, but some might set a minimum, often around £25,000.

What's the difference between bridge to let and buy to let bridging loan?

A bridge-to-let mortgage is for investors who want to refurbish a property then turn it into a long-term rental. It quickly becomes a regular buy-to-let mortgage.

In contrast, a buy-to-let bridging loan is a short-term loan for various buy-to-let purposes, like quick auction purchases. It doesn’t automatically convert into a long-term mortgage.

Related Articles

Can You Buy A House Through Your Business?

Many British property investors are looking at a new strategy: buying houses through limited companies. While this approach offers potential tax advantages, it’s not for everyone. Let’s explore the pros and cons of using your business to buy a house in the UK. Can You Actually Live in a House Owned By Your Company? Living […]

Free Rental Yield Property Calculator

Becoming a landlord can be an exciting prospect. You get a steady stream of income, potential for property value growth, and you own a tangible asset. But, owning a property investment also comes with its challenges. You must consider factors such as rental rates, vacancy periods, and maintenance costs. Without a clear picture of your […]

Changing Your Buy To Let To Residential Mortgage

Life can take unexpected turns. Maybe you’re facing a breakup, a new job in another city, the kids needing their own space, or you’re simply looking to downsize. In any of these cases, moving into your buy-to-let might seem like a good move. But hold on! There are key rules: If you switch from renting […]