Commercial Mortgages: How To Secure Care Home Finance?

Did you know the demand for care homes is soaring?

The latest UK Census of 2021 shows more than 11 million people are over 65. This spike from 9.2 million since 2011 highlights the need for more care homes.

On top of this, around 410,000 people live in these homes, creating £15.9 billion in revenue annually.

But you might be wondering, how exactly do we fund these care homes?

That’s what this guide aims to explain. We’ll cover everything you need to know about care home financing to help you make a smart decision for your new or existing project.

What is a Commercial Mortgage for Care Homes?

A commercial mortgage for care homes is a special type of business mortgage designed to buy, improve, or run a care home.

With this loan, you can borrow up to 90% of the care home’s value, which acts as the loan’s security. You can choose to pay it back over 1 to 25 years.

Because it’s for a business, getting this type of mortgage is tougher and riskier than getting a residential mortgage. This usually means higher interest rates and stricter rules from lenders.

It’s smart to talk to a broker who knows about care homes. They can help you find a mortgage that fits your budget and matches what you know about running a care home. They’ll make sure you get a deal that’s right for your care home’s needs.

Steps to Secure Your Care Home Financing

Just like with any mortgage loan, preparation is key! To get care home financing you need to:

1. Craft a Detailed Business Plan

Your business plan is your roadmap to success. It should clearly outline:

- How your care home will operate profitably, with financial projections and marketing strategies.

- Details about occupancy rates.

- The quality of care you’ll provide showcases your commitment to excellence.

- Your long-term growth or exit strategy, ensures you have a vision for the future.

Demonstrating a profitable business model is key to convincing lenders of your ability to repay the loan.

2. Gather All Your Documents

Lenders want to see your business’s financial health. You’ll need:

- Your business’s financial records for the last 2-3 years.

- Bank statements for you and your business from the last 3 months.

- Proof of where you live and who you are.

- Any agreements you have for your business location.

- Your business plan, of course.

- Details about your care home’s ratings and how full it is.

- Check your credit score to avoid surprises.

3. Ensure Your Credentials Are Solid

Show you’ve got what it takes to run a care home.

This means sharing your experience, Care Quality Commission (CQC) ratings, and meeting all health and safety rules.

Make sure to show every award or commendation that highlights your commitment to care quality.

4. Explore the Best Mortgage Deals

Every care home is different, which means every loan needs to be tailored. Your care home’s location, size, financials, and potential for growth all play a part in finding the right loan.

Also, consider the overall terms of the deal.

A broker who knows about care home loans can help here. They can find deals you might not see on your own.

Eligibility Criteria

Since care homes are considered as businesses, lenders look at them through a commercial mortgage lens. Here’s what you need to qualify:

Industry Experience

You should have 2-3 years of experience in managing a care home to improve your chances. Lenders check this to see if you can run the business well.

They also look at the qualifications of your management team. At least, someone should have a Level 4 NVQ in Health and Social Care or something similar.

Business Performance

If you’re planning to take over an existing care home, showing it’s been doing well financially will help your case.

Your business plan needs to cover how stable the finances are, how full the care home usually is, and how you expect it to grow.

Regulatory Compliance

Meeting the standards set by regulators is crucial. In the UK, this means the Care Quality Commission (CQC).

A good rating from them shows you meet health and safety standards, which lenders like to see.

What is the Care Quality Commission (CQC)?

The Care Quality Commission (CQC) is the body that checks all health and social care services in England.

It makes sure these services provide people with safe, effective, compassionate, and high-quality care, and they encourage services to improve.

A CQC certification is proof that a care home meets these standards, making it very important for getting a mortgage.

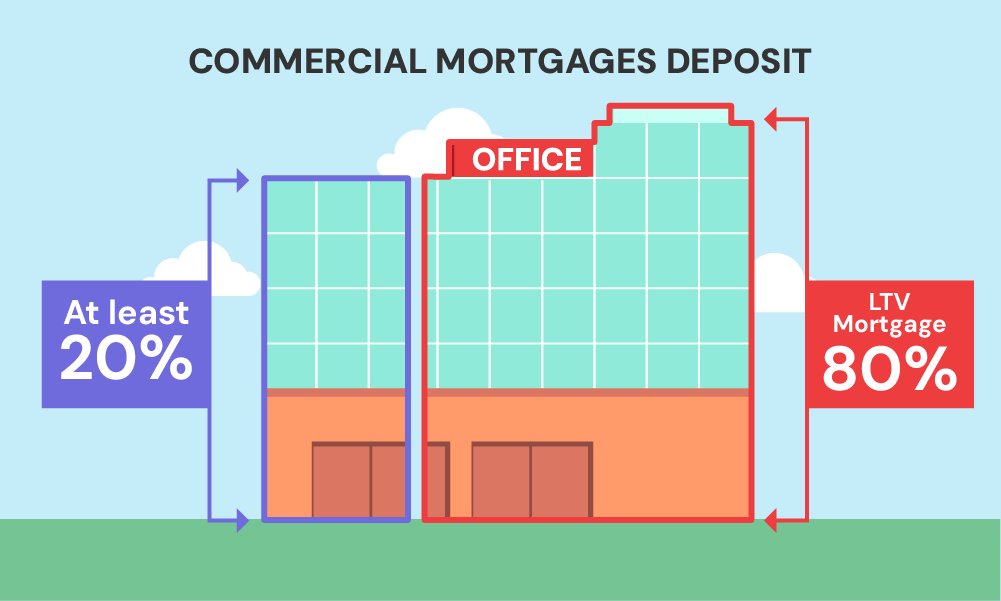

How Much Deposit Do You Need?

Usually, you’ll need to put down 20-40% of the care home’s buying price as a deposit.

When you put down a big deposit, it does a few things.

First, it lowers the risk for the lender. They see that you’ve got a lot invested in this, which means you’re likely to work hard to make it a success.

Also, a bigger deposit shrinks the loan amount compared to the care home’s value. This is safer for lenders because if things don’t work out, they have a better chance of getting their money back.

Having the cash for a large deposit also proves to lenders that you’re in a solid financial position. It’s not easy to save up that kind of money, after all.

Lastly, it shows you’re serious. Buying a care home is a big commitment, and a hefty deposit tells lenders you’re ready to take on the challenge.

Can You Get Financing Without Direct Experience?

Yes, you can get financing even if you haven’t run a care home before, but you’ll need to put in some work.

Experience in areas related to healthcare or management can help. Lenders want to see that you understand the business and can handle it successfully.

Here’s what you need to show:

- Talk About Your Experience – If you’ve worked in roles that involve caring for others or managing a team, even if it’s in a different industry, that’s valuable. Describe how these experiences have prepared you to manage a care home.

- Get CQC Certification – The Care Quality Commission (CQC) makes sure care homes meet certain standards. Having this certification shows lenders you’re serious about providing quality care and that you understand the rules.

- Show You’re Ready for the Challenge – Running a care home takes dedication and a lot of hard work. You’ll need to be in good health, show you have strong morals, and get any qualifications you might need for the job.

You need to prove that your background and plans line up with what it takes to run a successful care home.

Alternative Financing Options

Care home mortgages are not your only options to finance a care home. Let’s break down some other alternatives:

- Bridging Loans. These are quick loans that help you use the value of what you already own to buy something new, like a care home. You use them for a short time until you arrange long-term finance or sell something else.

- Development Finance. This is perfect if you’re starting a care home from scratch or making big changes to one. You get money bit by bit as you build, which means you only pay interest on what you spend. It’s great for keeping costs in check.

- Releasing Equity through Remortgages. If you have properties already, why not use them to help buy another? By remortgaging, you can get the money you need for a new care home without dipping into your savings.

Each choice has its own benefits.

Bridging loans are fast, development finance matches your project’s pace, and releasing equity makes your existing properties work for you. Think about what you need and pick the option that fits best.

Key Takeaways

- A commercial mortgage helps you buy, improve, or run a care home, letting you borrow up to 90% of its value. You can pay this back over 1 to 25 years.

- Making a clear business plan that shows how your care home will make money, how many people will stay there, and the quality of care you’ll provide is key to getting a loan.

- If you’ve run a care home for 2-3 years and meet the Care Quality Commission (CQC) standards, you’re more likely to get the mortgage you want.

- Other ways to finance your care home, like bridging loans, development finance, or using the value of your other properties, can also help, depending on what you need.

The Bottom Line

Getting a loan for a care home can be tricky, so it’s really helpful to have a broker by your side.

A broker who knows all about care home loans will make things easier for you and help you get the best deal.

Want to make things easier for yourself? Get in touch with us. We’ll connect you with a trusted broker who understands exactly what you need, saving you time and worry.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

How much does it cost to open a care home?

Generally, you might need to borrow anywhere from £500,000 to £2 million to start.

Factors such as location, size, and whether you’re starting anew or buying an existing facility can impact this amount. Also, you must consider the cost of buying the property, hiring staff, the right equipment, and other operational costs.

Related Articles

Can You Change From Commercial Mortgage To Residential?

Since 2015, it’s been easier to switch your mortgage from commercial to residential, all thanks to the UK government’s major changes to the General Permitted Development Order (GPDO). These rules have simplified changing a building’s use from commercial to residential, offering developers more opportunities to turn unique business spaces into homes. You might be considering […]

Should You Get A Semi-Commercial Mortgage? A Guide

If you want to own a building with a shop on the ground floor and flats above, you’re the perfect candidate for a semi-commercial mortgage. This option is also great for investors looking to buy such mixed-use properties and for developers aiming to create spaces that blend living and commercial areas. Curious? This article explores […]

How To Buy A Pub With Commercial Mortgages? A UK Guide

Pubs are more than just places to drink. They’re the soul of British culture – a haven where locals gather to unwind, celebrate, or simply enjoy a quiet pint after a long day. For anyone dreaming of swapping their office view for the behind-the-bar camaraderie, the idea of running a pub might sound like the […]