How To Get a Mortgage When You’re Paid in Cash: A Guide

Securing a mortgage in the UK can appear daunting if your income is paid in cash.

Tradespeople, freelancers, and workers in hospitality and retail often find themselves in this situation, receiving cash payments for their hard work.

Many believe that this payment method makes getting a mortgage impossible. However, this simply isn’t the case.

In this guide, we’re going to clear up some common myths about cash income and mortgages.

Let’s get started!

Can You Secure a Mortgage With Cash Income?

Absolutely! Earning your income in cash doesn’t stop you from getting a mortgage.

Lenders vary in how they view cash income.

While some may hesitate to lend because they prefer income that’s paid directly into a bank account, many are open to cash income and willing to consider your mortgage application if it all adds up.

Getting paid in cash means your money comes straight to you, not through a bank. But your employer must handle things properly, like paying your taxes and National Insurance contributions.

This system is known as PAYE, short for Pay As You Earn. As long as your employer sticks to these rules, lenders will view your cash income just like any other income.

So, dreaming of owning a home is still very much in reach, even if your wages are in cash. The key is to partner with a lender who understands your situation and is ready to support you on your journey to homeownership.

Is It Harder to Get a Mortgage with Cash Income?

Applying for a mortgage when your income comes in cash can be slightly more challenging. Banks and lenders will take a closer look at your application.

Their goal is to verify that your cash is legitimate and you have the means to repay the mortgage.

This scrutiny means you’ll need to provide more documents and undergo additional checks compared to someone whose income is directly deposited into their bank.

Another hurdle is finding a lender willing to approve mortgages for cash earners. With fewer lenders open to cash incomes, snagging a great deal might become a bit more challenging.

And if you’re navigating this path without expert guidance, like that from a mortgage broker familiar with cash incomes, you might face an even steeper uphill battle to get your application across the finish line.

How to Prepare for a Cash Mortgage Application

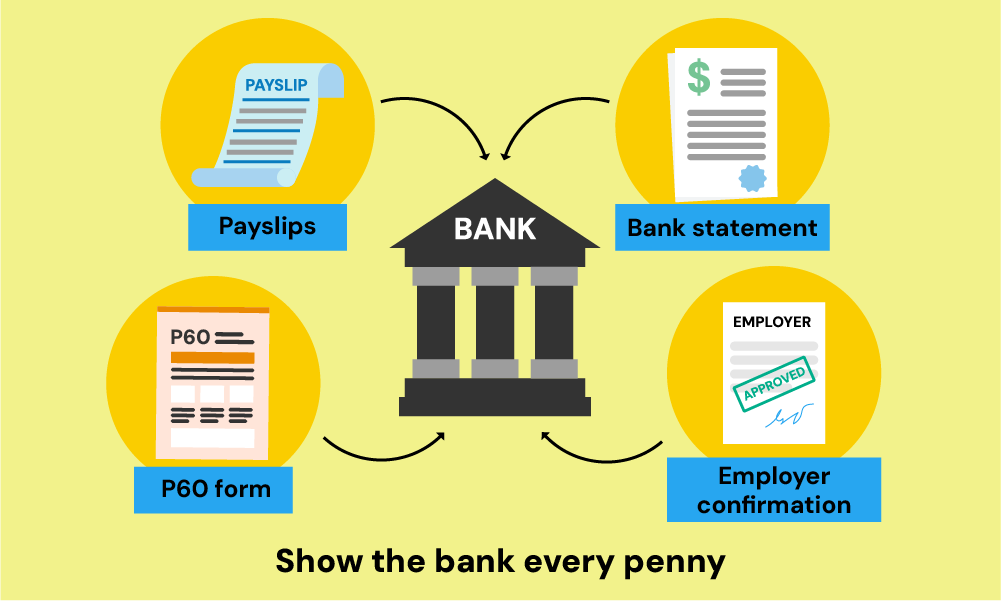

Preparing for your mortgage application is crucial, especially when you earn your income in cash. You’ll need to prove to the bank exactly how much you earn.

You can do this by gathering your payslips, a P60 form, bank statements, and possibly a letter from your employer confirming your cash income.

Keeping your bank statements up to date is vital. These statements should reflect the money you’ve saved or the cash deposits you’ve made.

This evidence allows the bank to verify that your declared income matches your actual earnings. Organising all your financial documents neatly is a smart move.

By doing so, you ensure that you’re ready to present a complete and accurate picture of your finances when you apply for a mortgage.

When Might Cash Income Not Be Acceptable?

Here are a few reasons why a bank might say no to your application:

- You have tax issues. If the bank isn’t sure your cash income has been reported properly for taxes, they might reject you. Make sure all your earnings are well-documented.

- You’re new to the UK. Banks are extra careful if you’ve recently moved to the UK, especially from another continent. They find it hard to check your income and financial history from another country. Showing a stable income and starting to build a financial history in the UK can help.

- You don’t have enough proof of income. Just showing your bank statements or a letter from your employer might not be enough. Sometimes, you must show more evidence, like extra payslips, your P60, or detailed bank statements.

- You don’t have a full-time and stable job. If your cash income is from a part-time job, it might be harder to get a mortgage. Showing a steady income over a longer period can help.

- Your lender prefers joint applications. Some lenders are hesitant to lend if the main earner’s income is all in cash unless you apply together with someone whose income isn’t in cash.

Steps to Start Your Mortgage Application with Cash Income

Starting your mortgage application when you have cash income might seem tricky, but here’s how you can do it step by step:

Gather Your Documents

First, collect all the paperwork that shows how much money you make. This includes payslips if you have them, any records of cash payments, your P60 form, and recent bank statements where you’ve deposited your cash income.

Check Your Credit Report

Next, take a look at your credit report. This is important because it shows if you’ve been good with money in the past.

You can get your credit report from credit agencies – Experian, Equifax, and TransUnion. Make sure everything is correct. If something is wrong, you can ask for it to be fixed.

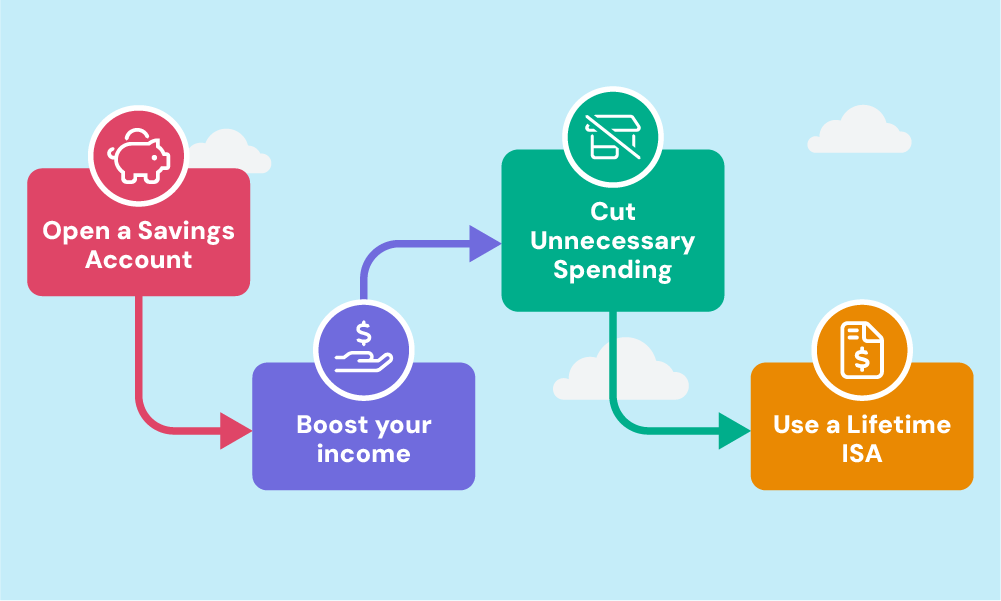

Save for a Bigger Deposit

Putting down a larger deposit means you need to borrow less money. Lenders prefer this as it lowers their risk.

To boost your deposit, try these steps:

- Open a Savings Account – Start a savings account just for your deposit. Choose one with a high interest rate to grow your savings faster.

- Boost your income – This can be a smart move if you have the time and flexibility to take on more work. Any extra money you make can go into your deposit savings

- Cut Unnecessary Spending – Stop buying things you don’t need and cut down on eating out. Cancel any subscriptions you’re not using. Then, move what you save into your deposit account.

- Use a Lifetime ISA – Consider getting a Lifetime ISA. This is a special savings account where the government adds 25% to your savings, up to a set limit. This is for buying your first home.

Find a Specialised Mortgage Broker

This is a key step. A mortgage broker who knows about cash income can help a lot. They can find the right bank for you and make sure your application is as strong as possible.

The Bottom Line

Buying a home with cash income means taking a few key steps.

Keep all your financial records, such as bank statements and income proofs, to show banks you have a reliable income. It’s also crucial to check your credit report for accuracy, as it reflects your financial responsibility.

A mortgage broker familiar with cash incomes can significantly simplify the process for you. They have the expertise to select the right bank and streamline your application, ensuring it meets the lender’s criteria.

To connect with a suitable broker, reach out to us. We’ll match you with a reliable mortgage broker for a free, no-obligation consultation, making your path to buying a home smoother.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Is it harder to get a mortgage with a cash deposit?

Yes, securing a mortgage with a cash deposit can be trickier, mainly because lenders must be sure the cash has a legal source. They check this to follow anti-money laundering laws. If you’re using a cash deposit, be ready to show where it came from, like a gift letter from your family.

Can self-employed individuals with cash income qualify for a mortgage?

Yes, you can. If you’re self-employed and earn cash, you can still get a mortgage. You’ll need to show you have a steady income and are financially stable.

This usually means sharing your tax returns, profit and loss statements, and bank statements from the last two or three years. Lenders will assess your income after you’ve taken out your business expenses to decide if you’re eligible.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

A Guide to Using Bonuses and Commissions for a Mortgage

Are you finding it tough to get lenders to look at your full income? We know that bonuses and commissions can change, and this can make some lenders a bit wary. But, don’t worry – having a variable income doesn’t mean you can’t get a good deal on a mortgage. There are lenders out there […]

Umbrella Company Mortgages Explained

Struggling to buy a house while working for an umbrella company? You’re probably worried that your job setup will make getting a mortgage a bit trickier. Here’s some good news – securing a mortgage is totally doable for umbrella company workers. This quick guide will show you how to successfully ace your mortgage application. Let’s get […]

How To Get A Student Mortgage in the UK: A Guide

Being a student can make securing a mortgage challenging. Lenders are often cautious due to your limited credit history and fluctuating income. But, here is the deal – it’s not impossible. With the right guidance, you can get on the property ladder while being a full-time student. Curious, how? This article will show you how […]