How To Get Mortgages on Probationary Period?

Many think getting a mortgage while on probation is impossible, making homeownership seem unrealistic for job starters.

But it’s not all bad news!

This guide clears up myths and offers a simple way to navigate the mortgage process on probation.

Can You Get a Mortgage While on Probation?

Yes, it’s possible to get a mortgage during your probation period, but there are extra steps to consider.

Lenders often view probation as a sign of less stable employment because your role might not be permanent yet.

They worry if you’re still in the early stages of your job, it might be easier for you to be let go, especially if the company needs to make cuts.

This doesn’t mean you can’t get a mortgage; it means you need to show lenders you’re a reliable borrower in other ways.

They’ll take a closer look at your income, how you spend your money, and your credit score to decide if you can keep up with mortgage payments.

Eligibility Criteria for Mortgages on a Probationary Period

To qualify for a mortgage, you need to provide proof of your financial health. Lenders will look for these crucial factors:

- Job Type – Jobs in the public sector, like teaching or nursing, are often seen as more secure. This can make your mortgage application look stronger.

- Probation Length – Lenders prefer shorter probation periods, usually around 3 months, because they suggest you’ll soon move into a more stable employment phase.

- Time in Your Current Role – The longer you’ve been in your job, the better. Being new might raise concerns, but if you’ve been there for a few months, it shows stability.

- Credit History – Good credit is crucial. It shows lenders you’re responsible with money. If you’ve had issues, getting advice on improving your credit can help.

- Deposit Size – A bigger deposit, ideally 20-25%, can make your application more attractive. It reduces the lender’s risk and shows you’re serious about the purchase.

- Managing Debt – Keeping debt under control proves you can handle your finances well. Lenders want to see that you’re not overstretching yourself.

- Type of Property – Choosing a standard property can ease your mortgage process. Unusual properties might be harder to get approved for because of their unique risks.

- Experience in Your Field – Showing that you’ve worked in the same industry or similar roles before can reassure lenders about your job security and income stability.

Remember, this is a general rule. Not all lenders will require these criteria. It’s best to directly check on your lender or with your mortgage broker before you apply.

How To Get a Mortgage During Probation?

Once you know whether you qualify or not, it’s time to learn the practical steps to turn your understanding into action.

Here’s how you start:

1. Sort Out Your Finances

Before diving into the property market, especially if you’re on probation, it’s crucial to have your finances sorted.

Check your credit score with agencies like Experian, Equifax, and TransUnion to understand your financial health. Fix any issues you find.

To show you’re financially stable, gather essential documents such as:

- Proof of ID (passport or driving licence)

- Proof of address (utility bills or council tax bills)

- Recent payslips (3-6 months)

- Bank statements (3-6 months)

- Employment contract showing probation details

- Proof of deposit

- Additional income documentation (if applicable)

Also, start saving for a deposit. The bigger your deposit, usually 10-20% of the house price, the better your mortgage terms could be.

To boost your deposit, try these steps:

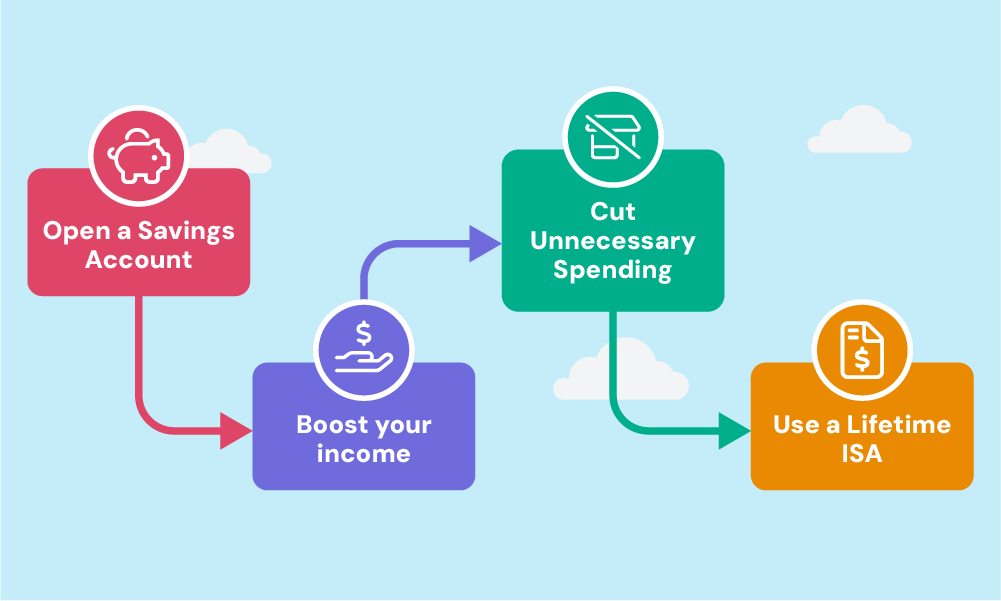

- Open a Savings Account – Start a savings account just for your deposit. Choose one with a high interest rate to grow your savings faster.

- Boost your income – This can be a smart move if you have the time and flexibility to take on more work. Any extra money you make can go into your deposit savings

- Cut Unnecessary Spending – Stop buying things you don’t need and cut down on eating out. Cancel any subscriptions you’re not using. Then, move what you save into your deposit account.

- Use a Lifetime ISA – Consider getting a Lifetime ISA. This is a special savings account where the government adds 25% to your savings, up to a set limit. This is for buying your first home.

2. Get an Agreement in Principle (AIP)

An Agreement in Principle gives you an idea of how much you can borrow. While it’s not mandatory to have one, getting an AIP is a smart move.

An AIP clarifies how much you can afford, making house hunting easier and showing sellers you’re serious about buying.

Remember, this is not a guaranteed offer from a lender. You can obtain one from banks, building societies, or through a mortgage broker. An AIP typically lasts between 30 to 90 days, which is plenty of time to search for the right property.

Be mindful, though. Some AIPs require a hard credit check, which might affect your credit score.

It’s not always the case, but it’s important to check with your lender or broker.

This way, you can enjoy the benefits of having an AIP without unwelcome surprises on your credit report, setting the stage for a successful home search.

3. Start Your House-Hunt

With your AIP, you can now look for your ideal home. Explore areas, visit homes, and think about what you want from a place.

Stick to your budget and don’t rush. When you’ve landed on the right spot, it’s time to make an offer through the estate agent.

4. Apply for a Mortgage

Once your offer is accepted, it’s time to apply for the mortgage.

You can apply directly to a lender or use a mortgage broker who can guide you and help compare offers.

Lenders will need a property survey to check its value and condition.

The whole process, from application to receiving your mortgage offer, usually takes 4-6 weeks. Review your mortgage offer carefully before accepting.

5. Engage with a Solicitor for Completion

A solicitor or conveyancer will manage the legal bits of buying your home, like land registry and contract exchange. They make the deal official.

Follow their lead, and soon you’ll be on to the final step – getting the keys.

Once you exchanged contracts with the seller, you’re now committed to buying the property and paying the mortgage.

If you’re on probation and struggling with the mortgage process, talking to a mortgage broker can help. They’ll guide you, choose the best lenders, and improve your chances of getting a mortgage while you focus on time with your loved ones.

They handle the tough parts for you.

However, picking the right broker is key, and with so many choices, it can feel daunting. We’re here to make it easier.

Just reach out to us, and we’ll quickly connect you with a trusted mortgage broker for a free, no-obligation chat to assist with your mortgage needs.

Before you dive in, think twice about using your home as collateral. Failing to meet repayments can result in losing your property.

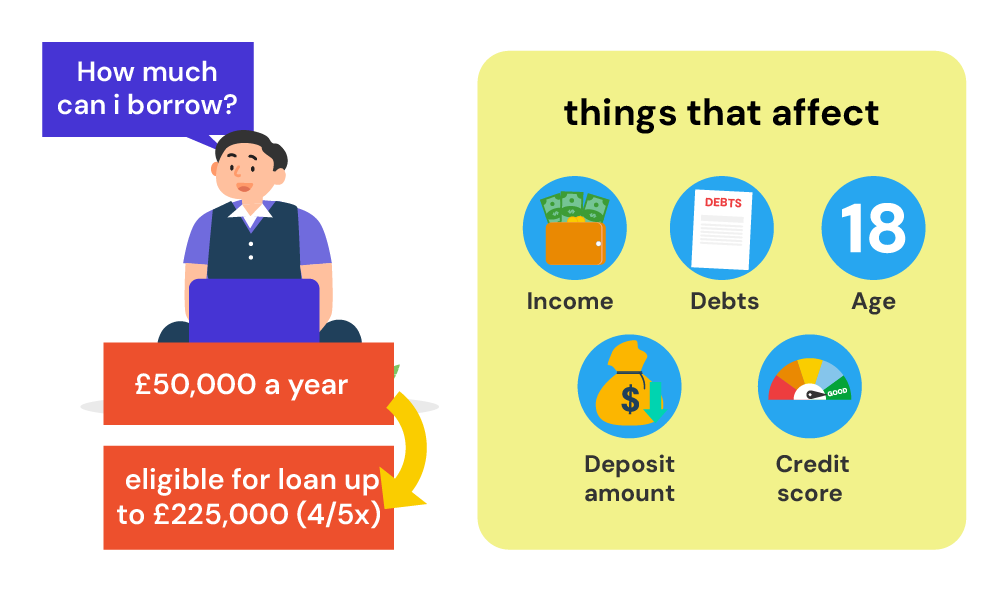

How Much Can I Borrow?

Most lenders offer loans 4.5-5 times your annual salary. This means if you’re earning £30,000 a year, you could potentially borrow between £135,000 and £150,000.

However, if you’re on probation, lenders might be more cautious. They might only consider your basic salary, and not count any extra earnings like bonuses, commissions, or overtime pay in their calculations.

This affects the total amount you’re able to borrow. That’s why sometimes it’s best to wait until you’ve become a regular before applying for a mortgage.

To get a clearer idea of what you might afford, try using a mortgage affordability calculator.

Just pop in your details – don’t worry, it won’t take any personal information from you. This tool gives you an initial estimate, helping you understand your borrowing potential without any commitment.

[Embedded Mortgage Affordability Calculator]

Can I Remortgage During My Probation Period?

Yes, you can remortgage while on probation, but it might be a bit tricky.

Not as many lenders are keen to offer deals if you’re still new at your job and on probation. But, it’s not impossible to find a good deal.

First, have a chat with your current mortgage provider. They’ll tell you if you can remortgage with them while you’re on probation and how it might change your mortgage.

If you’re looking for a better deal, talking to a mortgage broker is a smart move. They know the ins and outs of remortgaging during probation and can point you to lenders who might consider your application.

They can also help you understand if moving to a new lender might change how much you can borrow or if there are any special rules you need to follow because you’re on probation.

Key Takeaways

- Getting a mortgage or remortgaging while on probation is doable, but you’ll need strong financial documents and a clean credit history to convince lenders you’re stable.

- Lenders care about your job type, how long your probation is, and your past finances. They prefer people in stable fields with shorter probation periods.

- A bigger deposit and experience in the same field help your application. This shows commitment and lowers the risk for lenders.

- During probation, they might only consider your base salary, not bonuses or overtime, when deciding how much you can borrow.

The Bottom Line

Getting a mortgage while on probation can be tricky, but with a mortgage broker’s help, it becomes much simpler. They can guide you through the process, making sure you find a lender who understands your situation.

If you want to save time and avoid stress, let us help. Contact us, and we’ll put you in touch with a trusted broker who’s ready to assist with your unique mortgage needs.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Can being a first-time buyer affect my chances if I'm on probation?

Being a first-time buyer on probation doesn’t necessarily impact your mortgage application negatively. But, lender policies vary—some may not see your probation as an issue, while others might be more cautious.

Working with a mortgage broker can help identify lenders who are more receptive to your situation.

What's the required number of payslips for my mortgage application?

Lenders typically ask for your three most recent payslips to verify your income.

If you’ve recently started a new job and don’t have enough payslips, providing your employment contract showing your salary details may be acceptable as proof of income.

Is it advisable to apply for a mortgage after probation?

Applying for a mortgage after completing your probation could expand your lender options and potentially secure you better interest rates.

This approach also allows you to include any additional earnings like bonuses or overtime pay in your application, possibly increasing the amount you can borrow.

But, if you find the right property during your probation, and your financial standing is strong, applying before your probation ends is still feasible.

Will the length of my probation impact my mortgage application?

The specific length of your probation period—typically three to six months—isn’t usually a significant concern for lenders.

What matters more is showing job stability and nearing the end of your probation, which can reassure lenders of your employment continuity.

Some lenders might delay funding until your probation is complete, so it’s important to verify the terms of your mortgage offer to ensure it aligns with your needs.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

A Guide to Using Bonuses and Commissions for a Mortgage

Are you finding it tough to get lenders to look at your full income? We know that bonuses and commissions can change, and this can make some lenders a bit wary. But, don’t worry – having a variable income doesn’t mean you can’t get a good deal on a mortgage. There are lenders out there […]

Umbrella Company Mortgages Explained

Struggling to buy a house while working for an umbrella company? You’re probably worried that your job setup will make getting a mortgage a bit trickier. Here’s some good news – securing a mortgage is totally doable for umbrella company workers. This quick guide will show you how to successfully ace your mortgage application. Let’s get […]

How To Get A Student Mortgage in the UK: A Guide

Being a student can make securing a mortgage challenging. Lenders are often cautious due to your limited credit history and fluctuating income. But, here is the deal – it’s not impossible. With the right guidance, you can get on the property ladder while being a full-time student. Curious, how? This article will show you how […]