- What Counts as Proof of Income for a Mortgage?

- Proof of Income For Employed

- Proof of Income for Self-Employed

- Proof of Income for Unemployed

- Proof of Rental Income

- Proof of Foreign Income

- How Supplementary Income Influences Your Mortgage

- Can You Get a Mortgage Without 3 Months of Payslips?

- What If You Lack Sufficient Proof of Income?

- Do You Still Need Proof of Income for Buy-to-Let Mortgages?

- Can You Still Get a Mortgage Even Without Proof of Income?

- Key Takeaways

- The Bottom Line

Proof of Income for Mortgages Explained

Showing your income is crucial for mortgage applications in the UK, whether you have a regular job or run your own business.

This helps lenders decide how much they can lend you.

Understanding what they accept as proof of income can make your application smoother and increase your chances of approval.

This guide explains everything you need to know.

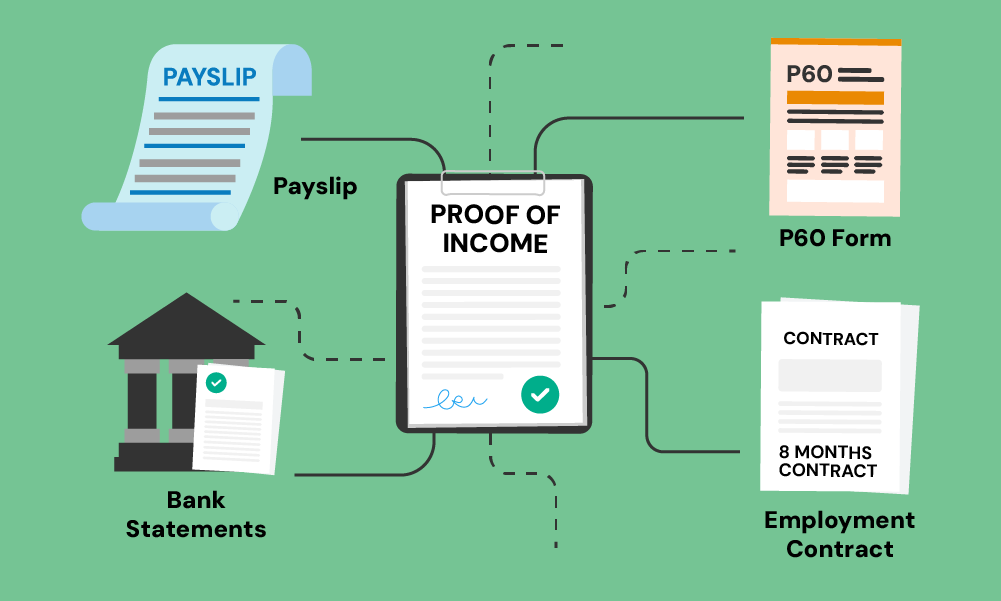

What Counts as Proof of Income for a Mortgage?

Proof of income for a mortgage is the documentation you provide to show how much money you earn. It helps lenders decide if you can afford the mortgage payments.

This usually includes your payslips, bank statements, P60 forms, and possibly your employment contract, depending on your job situation.

Essentially, it’s about proving you have a steady income to support your mortgage application.

Proof of Income For Employed

Here is the list of proof of income needed when employed:

- 3-6 months of your most recent payslips (including your salary and any additional income like overtime.

- P60 forms from the last two years. This document shows your total earnings and the tax you’ve paid on these earnings each year.

If you lack three months’ payslips, perhaps you’re new to the job, or a contractor, your lender might require:

- Employment Contract to show details of your salary.

- Bank Statements to show consistent income deposits from your employer.

Proof of Income for Self-Employed

As a self-employed, your income might vary more. It’s key to have the correct paperwork ready when you approach a lender. Here’s what they typically ask for:

- SA302 form or a tax year overview from HMRC for the past two to three years. This shows how much you’ve earned each year.

- Business accounts or profit/loss statements for the last two to three years, verified by an accountant. This proves how well your business is doing.

- Bank statements or dividend vouchers if your business pays you dividends.

- For contractors, your latest or upcoming work contracts.

Proof of Income for Unemployed

If you’re unemployed and applying for a mortgage, lenders will need to see any other income you might have:

- Official documents or letters from the government confirming you’re receiving benefits.

- Most recent pension statements, showing the amount you get.

- Details of any investment income, like dividend statements or interest from savings accounts.

Proof of Rental Income

For those with rental properties looking to apply for a mortgage or remortgage, you’ll need:

- Current tenancy agreements that detail the rental income you earn.

- Recent bank statements that show rental payments deposited into your account.

- The SA302 form from your tax returns, if you’ve declared rental income, shows the income you’ve made from your properties.

Proof of Foreign Income

If you earn income from abroad, you’ll have to provide:

- Foreign tax returns from the country where you earn income, showing what you’ve declared.

- International bank statements that record your income deposits, with translations into English where needed.

- Employment contracts from any foreign company you work for, that show your salary and job terms.

- Proof of currency exchange to show how your foreign income converts to GB

How Supplementary Income Influences Your Mortgage

Lenders evaluate all income sources to determine your ability to afford mortgage payments.

This includes not just your salary but also any supplementary income such as bonuses, commissions, and rental income.

The impact of this additional income on your application depends on the type of income, its regularity, and how lenders perceive its stability.

To provide a clearer understanding, here’s a unique table detailing types of supplementary income, how much of this income lenders typically consider, and what evidence you need to present:

| Type of Supplementary Income | Percentage Considered | Evidence Required |

|---|---|---|

| Basic Salary from employment | Usually 100% | Payslips, P60s, bank statements, employment contract. |

| Bonuses/Overtime/Commissions/ Allowances | 0-100% | Payslips, P60s, bank statements, employment contract. |

| Pension or Retirement income | Usually 100% | Pension statements, P60s |

| Rental Income | Usually 100% | SA302 forms, tenancy agreements, bank statements |

| State Benefits | 0-100% | Bank statements, payment schedule or reward letter |

| University Bursary or Grant | 0-100% | Letter from institution with payment breakdown |

| Overseas Income | 0-100% | Translated payslips, self-employment accounts, employer details |

| Child Maintenance | 0-100% | Court order, bank payments |

Can You Get a Mortgage Without 3 Months of Payslips?

You can get a mortgage in the UK even without three months of payslips. This is helpful for new hires, self-employed people, or those with irregular work.

For new starters, your employment contract is often enough to apply before your first payslip arrives.

Some lenders may even consider you if you have a confirmed job offer with a start date within the next few months (3-6 months).

Self-employed individuals can use:

- business accounts (1-3 years’ worth)

- tax returns (including SA302s and HMRC tax summaries), and

- recent bank statements (personal and business, last 3 months) instead of payslips.

Contractors or those with variable employment might need to show work contracts or recent invoices, detailing their earnings and financial stability.

What If You Lack Sufficient Proof of Income?

If you’re finding it hard to show enough proof of your income, there are ways around it. Perhaps you don’t have the usual number of payslips or your income varies month by month.

In these cases, lenders might still work with you if you can show other evidence of earnings, like bank statements or contracts if you’re a contractor.

This is where a mortgage broker can really help. They know the ins and outs of what different lenders need and can guide you on how to show your income in the best light, even if it’s not straightforward.

Brokers can be especially helpful if your situation is a bit unusual, helping you find a lender who understands and can accommodate your specific needs.

Do You Still Need Proof of Income for Buy-to-Let Mortgages?

Yes, most buy-to-let mortgages require proof of income. Lenders typically want to see:

- A minimum personal income of £25,000 per year.

- A projected rental income that covers 125% to 145% of the mortgage repayments.

- Possible other income sources like investments, pensions, benefits, or savings.

For investors looking to earn from property rentals, some mortgage options don’t require you to show a minimum income level.

However, you’ll likely need to provide a business plan or evidence of projected rental income to demonstrate you can afford the mortgage.

When you apply for a buy-to-let mortgage, lenders usually ask for:

- An estimate of the potential rental income, as valued by an estate agent.

- Any current rental agreements, if the property is already rented, to verify your income from rent.

- Proof of your experience as a landlord, which may include statements from properties you’ve managed.

- Evidence of your personal income, like payslips or SA302 tax return forms, particularly important for first-time landlords.

Not all lenders ask for the same documents or even criteria, so it’s a good idea to check with your lender or a mortgage broker to ensure you have the necessary paperwork for a smooth application process.

Can You Still Get a Mortgage Even Without Proof of Income?

Getting a mortgage without traditional income proof is trickier than before. In 2011, self-certification mortgages, where you declared your income without proof, were phased out to reduce risk.

Now, showing your income is essential to prevent fraud and ensure you can repay. However, there are exceptions. Buy-to-let mortgages focus on rental income, and bridging loans for short-term needs might not require income proof.

If you lack standard income proof, you might still qualify by showing financial stability through bank statements, savings, or investments.

Mortgage brokers can help you find lenders open to alternative documentation. A strong credit history, a large deposit, or additional security can also improve your chances.

While self-certifying your income is gone, alternative routes still exist. Talking to mortgage brokers can help you explore these options.

Key Takeaways

- Showing how much you earn is key when applying for a mortgage. This proof helps lenders decide if you can handle the payments.

- What you need to show can change based on your job. Employed people might need recent payslips, P60 forms, an employment contract, or bank statements. If you’re self-employed, you’ll likely need your tax returns and business accounts.

- Not all your income might count towards a mortgage. For example, lenders might only consider part of your overtime pay, bonuses, or allowances.

- For buy-to-let mortgages, you need to show your personal income, potential rental earnings, and sometimes other income too.

- Each lender has different rules on what income they accept and how they check if you can afford a mortgage.

The Bottom Line

Applying for a mortgage is no easy feat. It’s a mix of research, paperwork, and negotiations that can really test your patience.

And the last thing you want? Landing a mortgage deal that doesn’t suit you, as it could cost you dearly down the line.

Finding yourself stuck with the wrong lender or broker can easily turn into a costly mistake.

That’s why it’s key to get it right from the start. The right advice can really make a difference.

If you’re gearing up for a mortgage and drowning in paperwork, a mortgage broker can be your lifeline. They’ll sort out the paperwork, sift through lenders to find your fit, and clear up any mortgage jargon. In short, they do the hard work so you can focus on what matters.

Unsure how to start? Get in touch with us. We’ll hook you up with a great mortgage advisor who’ll make sure you’re prepped and ready for a smooth mortgage journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can you remortgage without traditional proof of income?

Yes, it’s possible to remortgage without traditional proof of income, but options may be limited.

Lenders will still need evidence of your ability to make repayments, such as bank statements or alternative documentation that shows your financial stability.

How do recent changes or uncertainties (like COVID-19) affect income verification?

The COVID-19 pandemic has made lenders more cautious. You might need to provide additional documentation to prove the stability of your income during such uncertain times. Lenders may also review your employment situation and any impact on your earnings more closely.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

A Guide to Using Bonuses and Commissions for a Mortgage

Are you finding it tough to get lenders to look at your full income? We know that bonuses and commissions can change, and this can make some lenders a bit wary. But, don’t worry – having a variable income doesn’t mean you can’t get a good deal on a mortgage. There are lenders out there […]

Umbrella Company Mortgages Explained

Struggling to buy a house while working for an umbrella company? You’re probably worried that your job setup will make getting a mortgage a bit trickier. Here’s some good news – securing a mortgage is totally doable for umbrella company workers. This quick guide will show you how to successfully ace your mortgage application. Let’s get […]

How To Get A Student Mortgage in the UK: A Guide

Being a student can make securing a mortgage challenging. Lenders are often cautious due to your limited credit history and fluctuating income. But, here is the deal – it’s not impossible. With the right guidance, you can get on the property ladder while being a full-time student. Curious, how? This article will show you how […]