How To Get Mortgages with Rental Income?

Looking to get a mortgage with your rental income?

Being a landlord often means wrestling with financial decisions, especially when considering if rental income can count towards mortgage applications.

You probably want clear insights on how to use this income to buy a house or flat.

If that’s you, this guide is here to help.

We’ll explore how your rental income can work for you when applying for a mortgage. You’ll learn about what lenders are looking for, what papers you need, and how to make your rental income look good to them.

Ready?

Can Rental Income Secure You a Residential Mortgage?

Yes, you can.

If you’re managing properties as a professional landlord, you’ll find many UK lenders consider the income you earn from these rentals a solid foundation for your mortgage application.

They’re keen to know if you can handle the mortgage repayments.

To this end, they assess your rental income against potential risks, ensuring you can consistently meet payments without financial strain.

Lenders are aware that for some, rental income may be the main, if not the only, source of earnings.

They recognise the unique positions of landlords who might not have a steady salary but still possess the financial stability to repay a mortgage. This flexibility shows that lending isn’t a one-size-fits-all process.

How To Prove Rental Income for a Mortgage?

As discussed, your rental income can help you out with a mortgage, but there are a few things lenders will look at first.

Let’s break it down into simple bits:

Proof of Income Documentation

Be prepared to present detailed documentation of your rental income. Start gathering the following documents:

- SA302 form to show your tax calculations and declared income to HMRC.

- Rental agreement to prove expected income from tenants

- Bank statements showing rental income deposits (3-6 months)

- Additional income documentation for other investments (if applicable)

Stable Rental Income

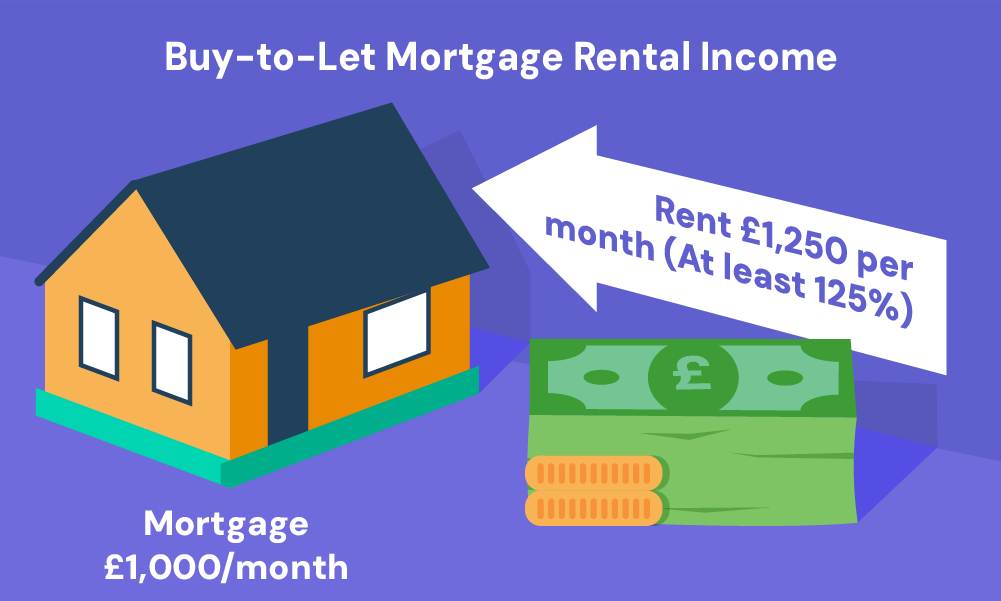

Your rental income should exceed your mortgage payments by 125% to 145%.

For both residential and buy-to-let mortgages, the general rule is that your rental income should be at least 125% to 145% of your mortgage repayments.

For example, on a £1,000 monthly mortgage, aim for rental earnings of £1,250 to £1,450.

This surplus acts as a safety net for any unforeseen costs or when the property isn’t rented.

The main difference between the two types of mortgages lies in the income assessment. For residential mortgages, lenders verify your income’s consistency through tax returns.

For buy-to-let mortgages, they focus on the property’s potential to generate future rent, requiring that it exceeds the mortgage payments by at least 125%, adjusting for tax rate differences.

Your Time as a Landlord

If you’ve been renting out properties for a while, say at least 2 years or more, that’s a big thumbs up. It shows lenders you’re not new to this game and you’ve got a steady flow of income coming in.

The Number of Rental Properties

More properties usually mean more income, which is music to lenders’ ears. They’ll be keen to know how many properties you own and what sort of income they’re bringing in.

Credit History

A good credit score can open doors. It tells lenders you’re good with money and a safe bet.

Your Deposit

The more you can put down as a deposit, the better. Around 20% of the property’s value is a good starting point, but more can improve your chances and possibly get you better mortgage terms.

Remember, not all lenders are the same. Some might have a soft spot for professional landlords, while others might have special rules for properties owned by your company.

Doing a bit of homework here, or teaming up with a mortgage broker, can really pay off.

How Much Can You Borrow?

When it comes to figuring out how much you can borrow, lenders put your rental income under the microscope.

How long you’ve been earning rental income, how many properties you’ve got, and the lender’s own rules play big roles.

For those of you with one or two properties, you might find that some lenders only take half of your rental income into account.

But, if you’re juggling three or more, they could be willing to consider your entire rental revenue.

And here’s the thing – not all lenders are the same.

While some stick to a fixed percentage of your income, others might be willing to look at the whole picture.

What they’re keen on is ensuring your rental income more than covers the mortgage repayments, usually aiming for it to be between 125% and 145% of the mortgage payment. This ensures you’re in a good position to manage a loan for a residential property.

To get a ballpark figure of what you might be able to borrow, try the mortgage affordability calculator below.

Simply enter your rental income details, and it’ll give you an estimate. But keep in mind, this is just a starting point.

The exact amount you can borrow will also hinge on things like your credit score and any other debts you might have.

How To Apply for a Mortgage Using Rental Income?

Securing a mortgage with rental income isn’t just about showing you’ve got money coming in; it’s about proving you’re a safe bet for lenders.

Here’s how to make your case:

1. Sort Out Your Finances

This is step one. Get a clear picture of your financial situation.

This means doing a thorough check of your credit score and getting any issues sorted. Check your score from credit agencies – Experian, Equifax, and TransUnion.

You’ll also want to gather all the necessary paperwork which proves your rental income. This includes:

- Proof of Identification (passport or driving licence)

- Proof of address (utility bills or council tax bills)

- Proof of deposit

- Evidence showing income and source of income such as bank statements, tax returns, and rental agreements.

- Evidence of outstanding debts such as credit card statements and loan statements

These documents help lenders see the full picture of your financial health.

Another thing you can work on during this is the amount of your deposit.

A bigger deposit can mean better mortgage terms.

Consider opening a high-interest savings account specifically for your deposit, cutting back on unnecessary spending, or even boosting your income with extra work.

A Lifetime ISA is also a smart move, thanks to the government adding 25% to your savings.

2. Get an Agreement in Principle (AIP)

An AIP shows how much you might borrow and signals to sellers that you’re a serious buyer. You can get one from banks, building societies, or a mortgage broker.

They last up to 90 days, giving you plenty of time to house hunt. Just watch out for hard credit checks that could affect your score. Making sure this step works for you without harming your credit is key.

3. Start Your House Hunt

With your AIP in hand, you know what you can afford.

Take your time to find the right place that fits within your budget. Check out different places, visit homes, and think about what you want.

If you’ve found the right spot, put in your offer through the estate agent.

4. Apply for a Mortgage

Once you’ve found a property and your offer is accepted, it’s time to make it official.

You might go straight to a lender or opt for a mortgage broker’s help to weigh your options. This phase includes checking the property’s value and state.

The whole process can take around 4-6 weeks, so review everything carefully before you commit.

5. Engage with a Solicitor

A solicitor will handle all the legal work, including property searches and transferring funds. They play a crucial role in making the deal official, so choose someone you trust.

After exchanging contracts with the seller, you’re all set – you can now enjoy your home while making sure you’re consistently paying your mortgage.

Remember, take a moment to seriously consider using your home as collateral for a loan. Not keeping up with repayments might result in you losing your home.

If you’re still unsure about your financial situation, consider speaking with a reliable mortgage broker. They know the ins and outs and can steer you towards the best deal for your situation.

Which Mortgage Lenders Accept Rental Income?

Many UK lenders are open to considering rental income when assessing your mortgage application.

This includes major banks like HSBC and Barclays, as well as smaller building societies like the Loughborough Building Society and Hinckley & Rugby Building Society.

However, their criteria can differ greatly.

For example, some may accept 100% of your rental income if you own multiple properties, while others may require a detailed history of stable rental income before considering it.

The documentation needed can also vary, with some lenders needing more than just your SA302 tax overview and bank statements showing rental income deposits.

The Bottom Line

The mortgage market can be tricky, especially when you’re using rental income to secure a loan. This is where having a mortgage broker helps. They know all about the market and can direct you to lenders that suit your needs.

Good brokers work hard to find the best deals, understand all the details, and track down lenders who accept rental income.

They can make the process easier, save you time, and improve your chances of finding a good mortgage deal.

Looking to find the right broker without the hassle? Get in touch with us. We’ll connect you with a trusted broker who can sort out your mortgage situation.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

Can I use rental income from overseas properties for a mortgage?

Yes, you can use rental income from abroad to help secure a mortgage here in the UK. But, it’s worth noting that UK lenders’ attitudes towards foreign income, including rental earnings, can differ a lot.

Some might not accept it at all. That’s why talking to a mortgage advisor or broker who knows the ins and outs of overseas income can be a smart move. They can help you find a lender that fits your circumstances.

Do I need a certain number of rental properties to qualify for a mortgage?

No, there’s no hard rule on how many rental properties you need to have.

Landlords are more interested in your experience as a landlord, the number of properties you own, and your ability to prove income through documents like tax returns.

These factors play a big part in whether your rental income can support your mortgage application.

Can I count rental income from a family member towards my mortgage?

Yes, rental income from a family member can count, but it’s up to the lender’s discretion. They’ll want to see that this income is steady and likely to continue.

Will mortgage lenders accept projected rental income?

Yes, some lenders might consider projected rental income, particularly if you’re buying a new property or one that’s yet to be built. They’ll usually ask for a rental assessment from a professional surveyor to make sure the figures stack up.

Remember, they’ll look at this alongside other factors like your financial health and the property’s market prospects.

For the best advice, speak directly with a lender or your mortgage advisor to see how projected income could work for your application.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

A Guide to Using Bonuses and Commissions for a Mortgage

Are you finding it tough to get lenders to look at your full income? We know that bonuses and commissions can change, and this can make some lenders a bit wary. But, don’t worry – having a variable income doesn’t mean you can’t get a good deal on a mortgage. There are lenders out there […]

Umbrella Company Mortgages Explained

Struggling to buy a house while working for an umbrella company? You’re probably worried that your job setup will make getting a mortgage a bit trickier. Here’s some good news – securing a mortgage is totally doable for umbrella company workers. This quick guide will show you how to successfully ace your mortgage application. Let’s get […]

How To Get A Student Mortgage in the UK: A Guide

Being a student can make securing a mortgage challenging. Lenders are often cautious due to your limited credit history and fluctuating income. But, here is the deal – it’s not impossible. With the right guidance, you can get on the property ladder while being a full-time student. Curious, how? This article will show you how […]