- Do Bonuses and Commissions Count Towards a Mortgage?

- Do Lenders Accept Overtime for a Mortgage?

- What Do Lenders Look for a Mortgage?

- How Much Can You Borrow

- How To Get a Mortgage Using Bonus and Commissions?

- How Lenders View Part-Time Jobs and Bonus Income

- Can I Get a Mortgage Using a Bonus Even with Bad Credit?

- Lenders Who Accept Bonus and Commissions Income for Mortgages

- The Bottom Line

A Guide to Using Bonuses and Commissions for a Mortgage

Are you finding it tough to get lenders to look at your full income?

We know that bonuses and commissions can change, and this can make some lenders a bit wary.

But, don’t worry – having a variable income doesn’t mean you can’t get a good deal on a mortgage. There are lenders out there who’ll take these into account.

This guide will show you how to make the most of your bonus and commission income for a mortgage.

Do Bonuses and Commissions Count Towards a Mortgage?

Yes, bonuses and commissions can help with your UK mortgage application, but how much they help depends on the lender.

They may be cautious as these earnings fluctuate, unlike a fixed salary.

Most of the time, lenders will only count part of your bonus or commission towards your mortgage. How much they’ll consider can vary.

Some might count half of it, while others might be okay with counting more, like 75% or even all of it. This depends on things like how regularly you earn this extra money and your credit history.

If you get your extra income every month, lenders are more likely to count it because it shows you have a steady flow of money coming in.

But if you only get bonuses or commissions once or twice a year, lenders might not be as keen to include it.

They find it harder to see this as regular income, so you might need to look around more to find a lender who will consider 100% of it.

To make your mortgage application smoother with this kind of variable income, getting help from a mortgage broker who knows the ins and outs of these situations is a good idea. They can guide you to the right lender for your specific situation.

Do Lenders Accept Overtime for a Mortgage?

Yes, many lenders are open about counting overtime towards your mortgage. But again, it’s not all cut and dried.

Factors such as the amount of overtime income, how often you get it, and whether it’s a regular part of your job matter. Lenders will perform thorough assessments to ensure you can manage your mortgage repayments, even if there’s a drop in your additional income.

The key point here is consistency.

If you’ve got a solid track record of earning overtime, and it looks like it’ll keep coming, lenders are more likely to count it towards your mortgage.

What Do Lenders Look for a Mortgage?

When you’re after a mortgage and your income includes commissions and bonuses, lenders have a checklist to tick off.

First off, they want to see consistency. That means they’re keen to know that your bonus or commission isn’t a one-off but something you regularly get. They typically look at your last two or three years’ earnings to get a good picture.

Then there’s the amount. They’ll usually take a percentage of your average bonus or commission income over those years — often around 50% to 60% — when calculating how much you can borrow. This is because they’re a bit cautious about income that can go up and down.

Stability in your job plays a big part too. Lenders feel more comfortable if you’ve been in your job for a while, showing that your income is likely to continue.

They’ll also check out your credit history, your outgoings, and other debts to make sure you can comfortably afford the mortgage repayments.

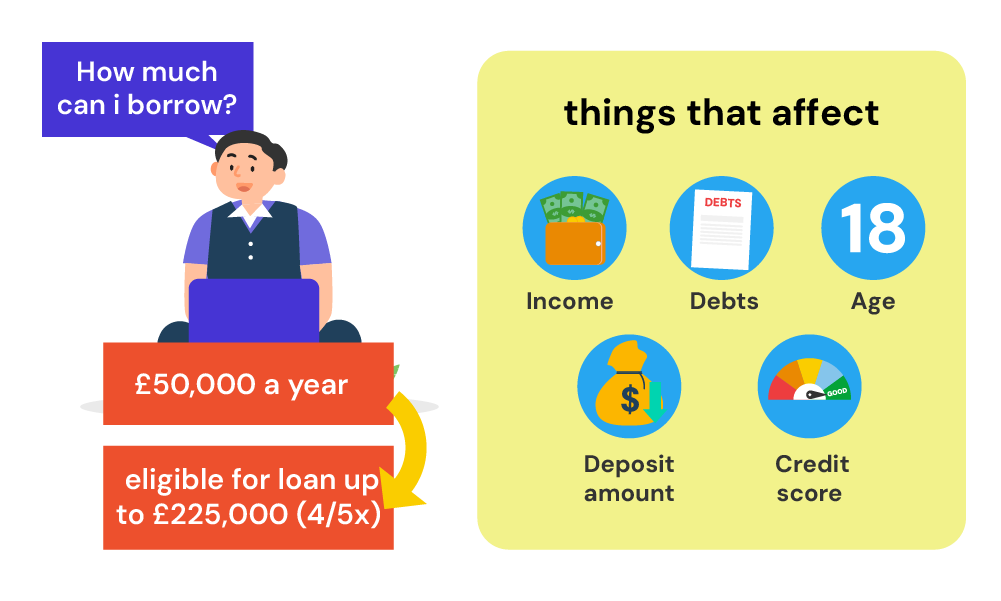

How Much Can You Borrow

In the UK, lenders usually decide how much you can borrow by multiplying your yearly earnings. This can range from four to five times your annual salary.

But, it’s not just about how much you make. Lenders also consider other factors, such as your debts compared to your income, how stable your job is, and where your money comes from – that includes your bonuses and commissions.

To get a good starting point about how much you can borrow, including what you earn from bonuses and commissions, use the calculator.

Note though that this is just an estimate. The exact amount you can borrow can vary depending on your financial health and lender’s criteria.

It’s important to speak with a mortgage broker to see your options. These experts can take a close look at your finances and find lenders who are happy to consider your full income. In short, they can make sure that you get a deal that fits your financial needs.

How To Get a Mortgage Using Bonus and Commissions?

Here’s how you can kick-start your mortgage application using bonuses and commissions:

1. Organise Your Finances

Getting a mortgage starts with understanding your financial situation. If you’re earning through bonuses or commissions, it’s crucial to present a strong financial profile. Begin with:

Check your credit score with agencies like Experian, Equifax, and TransUnion. A good credit score can make a big difference.

Gathering necessary documents to prove your income stability, including:

- Proof of ID (passport or driving licence)

- Proof of address (utility bills or council tax bills)

- Recent payslips and bonus/commission statements (3-6 months)

- Bank statements (3-6 months)

- Employment contract detailing your income structure

- Proof of deposit and any additional income documentation

Boosting your deposit is also key. A larger deposit, often 10-20% of the home’s price, can lead to better mortgage terms.

Consider opening a high-interest savings account, cutting unnecessary expenses, and exploring a Lifetime ISA to maximise your savings.

2. Get an Agreement in Principle (AIP)

An AIP gives you a ballpark figure of how much you might borrow based on your income, including bonuses and commissions.

While not mandatory, it’s a wise move that shows sellers you’re a serious buyer.

Just be mindful of the potential for a hard credit check, which could impact your credit score. Choose lenders or brokers who can offer an AIP with minimal impact on your credit.

3. Start Your House-Hunt

With your AIP in hand, start looking for your ideal home within your budget.

Take your time to find a place that meets your needs and preferences. Once you find the right home, make your offer through the estate agent.

4. Apply for a Mortgage

After your offer is accepted, proceed with the mortgage application. You have the option to apply directly to a lender or work with a mortgage broker who can compare different offers and guide you through the process.

Expect to undergo a property survey to assess the home’s value and condition. Typically, securing a mortgage takes about 4-6 weeks from application to offer acceptance.

5. Complete the Purchase with a Solicitor

A solicitor or conveyancer will handle the legal aspects of your home purchase, including land registry and contract exchange.

They play a crucial role in finalising the deal. Once contracts are exchanged, you’re legally committed to buying the property and fulfilling your mortgage payments.

If you earn through bonuses and commissions, getting a mortgage might seem tricky. A mortgage broker can make it easier by finding lenders okay with varied incomes, boosting your shot at approval.

Not sure where to begin? We can link you with a reliable mortgage advisor for a free chat about your options.

Just remember, failing to keep up with mortgage repayments can risk losing your home, so think carefully about your payment plan.

How Lenders View Part-Time Jobs and Bonus Income

Part-time jobs with bonus income get a careful look from lenders too. They’re checking if your part-time income plus any bonuses is steady and reliable.

Just like with full-time roles, they usually want to see a history of what you’ve been earning.

If your part-time job pays bonuses, lenders will likely average these out over the last few years, similar to commission-based income.

But here’s the thing: they want to be sure that your income pattern isn’t all over the place. Stability is key.

For part-timers, lenders might be a bit more cautious, so having a solid track record of your earnings, including any bonuses, can help your case.

It shows them that your income is predictable enough to keep up with mortgage payments.

Can I Get a Mortgage Using a Bonus Even with Bad Credit?

If you have a bad credit history but earn a good chunk of your income from bonuses or commissions, don’t lose hope.

There are mortgage specialists out there who get it. They’re used to dealing with folks who don’t fit the regular mould.

These specialists know which lenders are more open-minded about bad credit and irregular income types.

They can help negotiate your case, showing lenders that your bonus or commission income is reliable and that you’re on top of managing your finances now, even if you’ve had hiccups in the past.

The key is to be upfront about your situation. A good broker can help you find a lender who understands that people’s financial situations can change and improve.

They’ll look at your current income and how you manage your money today, not just your past mistakes.

So, yes, even with a poor credit history, getting a mortgage isn’t out of the question if you’ve got a bonus or commission income — with the right help and the right lender, it’s possible.

Lenders Who Accept Bonus and Commissions Income for Mortgages

Different lenders have different ways of dealing with bonus income, so let’s look at a few examples:

- Metro Bank goes a bit easier, accepting 50% of your average bonus over the last three years.

- Halifax might let you use up to 60% of your bonus income, but there’s a catch. If your basic salary is lower, they’ll only consider bonuses up to that amount. They also want to see a history of you getting these payments.

- HSBC wants to see up to three years of bonus history before they make a decision. And then, they might only count half of your average bonus towards your income.

- Coventry Building Society takes a stricter stance. They’re not keen on annual bonuses but might be more flexible with regular, smaller bonuses or commissions.

- Kensington Private Bank stands out by potentially accepting up to 100% of your bonus income, provided you’ve got a solid track record of bonus payments.

Each lender has its own rules and what they’re willing to consider as income. That’s why talking to a mortgage advisor can help. They know the ins and outs of each lender’s criteria and can guide you towards the best deal for your situation.

The Bottom Line

Applying for a mortgage with commission and bonus income has its challenges, but it’s possible with the right help.

The key is to present your variable income in the best light, ensuring lenders see you as a reliable borrower.

If the thought of navigating this process feels overwhelming, don’t worry.

Teaming up with a skilled broker who can provide the best-tailored advice for your unique situation can save you time and stress.

Reach out to us, and we’ll match you with a top mortgage broker who can help you kickstart your homeownership using bonus income and commission for mortgages.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a buy-to-let mortgage using bonuses and commissions in the UK?

Yes, you can. Lenders in the UK do consider bonus and commission income for buy-to-let mortgages. But, they’ll look closely at how consistent this income is over time.

They could ask for evidence of previous experience as a landlord, a spotless credit history, and possibly set age restrictions.

Is it possible to obtain a mortgage if my earnings are solely from commission?

Yes, getting a mortgage when your income is purely from commission isn’t out of the question.

But, you might need to look beyond traditional lenders to those who specialise in handling variable incomes.

The key here is demonstrating that your commission income is both regular and dependable over time.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Umbrella Company Mortgages Explained

Struggling to buy a house while working for an umbrella company? You’re probably worried that your job setup will make getting a mortgage a bit trickier. Here’s some good news – securing a mortgage is totally doable for umbrella company workers. This quick guide will show you how to successfully ace your mortgage application. Let’s get […]

How To Get A Student Mortgage in the UK: A Guide

Being a student can make securing a mortgage challenging. Lenders are often cautious due to your limited credit history and fluctuating income. But, here is the deal – it’s not impossible. With the right guidance, you can get on the property ladder while being a full-time student. Curious, how? This article will show you how […]

Stipend Mortgage: Can You Buy a Home as a PhD Student?

Getting a mortgage while you’re doing a PhD can seem as tricky as cracking a tough equation. The main hurdle? Most lenders aren’t familiar with stipend income and might worry about its reliability since it doesn’t grow like a regular salary. They might also question how long you’ll receive it. The good news: with some […]