- How Much Can I Borrow with £2,000 a Month?

- Does the Mortgage Term Affect My Affordability?

- What Other Factors Influence My Mortgage Affordability?

- How Your Job Affects Your Mortgage

- Can I Get a Mortgage for £2,000 a Month if I Have a Low Income?

- What Proof of Income Do Lenders Require?

- What Loan-to-Value Ratio Can I Get with £2,000 a Month?

- What Youâll Really Pay Beyond Mortgage

- How Can a Mortgage Broker Help Me?

- Key Takeaways

- The Bottom Line

How Much Mortgage Can I Get For £2,000 a Month?

Thinking about buying a home?

One of the biggest questions is how much you can afford to pay each month. 🤔

If you’ve set aside £2,000, you’re probably wondering what kind of property you can buy, how much you can borrow, and what affects how much you can afford.

This article will explain everything you need to know about a £2,000 monthly mortgage.

We’ll break down the details in simple terms so you can easily understand your options and make informed decisions about your financial future.

How Much Can I Borrow with £2,000 a Month?

How much you can borrow with a £2,000 monthly mortgage payment depends on several factors.

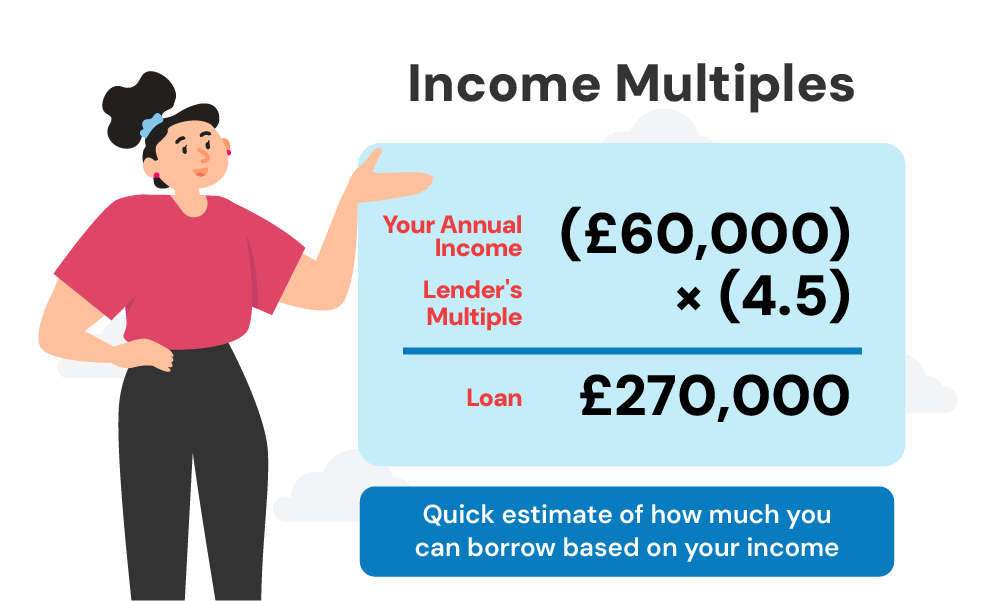

Your income is a key factor.

Lenders often use a simple calculation: they multiply your yearly income by a number between 4.5 and 6 to estimate how much you can borrow.

For example, if you earn £60,000 a year, you might be able to borrow between £270,000 and £360,000.

But, this is just one part of the puzzle. The interest rate and the length of your mortgage also play a big role.

For instance, with a 25-year mortgage at 4% interest, a £2,000 monthly payment could get you a mortgage of around £378,900.

But if the interest rate rises to 5%, that amount drops to about £342,100.

As you can see, even a small change in the interest rate can significantly affect how much you can borrow.

To get a more accurate picture, use a mortgage calculator or speak to a mortgage advisor.

Does the Mortgage Term Affect My Affordability?

Yes, it does.

The length of your mortgage can seriously affect how much you can borrow.

A longer mortgage (like 30 years) means lower monthly payments. This sounds good, right?

But it also means you’ll pay much more in interest over the whole loan.

For example:

- With a 30-year mortgage, you might be able to borrow around £419,000 if you can afford monthly payments of £2,000 at an interest rate of 4%.

- But if you shorten it to 20 years, with the same payments and interest rate, you’d only be able to borrow about £330,000.

So, it’s a trade-off.

Do you want to borrow more now and pay more later, or borrow less now and pay less overall?

Choosing the right mortgage term is important. It’s about balancing what you can afford now with your long-term financial goals.

What Other Factors Influence My Mortgage Affordability?

Your income and how long you want your mortgage to last aren’t the only things that matter.

Lenders look at your whole financial picture to decide how much you can borrow.

Outgoings and Debts

Lenders will check your income and outgoings. This includes things like other loans, credit card bills, and your everyday spending.

If you have a lot of debt or spending, you might be able to borrow less.

Credit History

Your credit score is really important.

A good score can help you get a better interest rate, which means you could borrow more.

A poor credit score could mean higher interest rates and borrowing less.

Deposit Size

A bigger deposit means you need to borrow less. This can help you get a better mortgage deal.

Most lenders want a deposit of 5-10% of the property’s value, but more is always better.

Profession

What you do for a living can make a difference. Some jobs, like doctor, lawyer, or accountant, are seen as more stable with higher earnings.

Lenders might offer better deals to people in these jobs.

If your income isn’t steady, for example if you’re self-employed, you might need to provide more financial information.

Age

Your age also matters. Younger people can often get longer mortgages with lower monthly payments.

Older people might have limits on how long their mortgage can be.

Lenders will check if you’ll still be working when the mortgage ends and might ask for proof of your pension or savings.

People closer to retirement might need a bigger deposit.

How Your Job Affects Your Mortgage

Your job plays a big part in whether you can get a mortgage.

Lenders like to see people with steady, long-term jobs.

If you’re employed on a PAYE basis with a regular salary, you’ll likely find it easier to get a mortgage.

But if you’re self-employed, things can be a bit trickier.

Lenders will want to see at least two years of your business accounts or tax returns (SA302) to check your income.

Even if you earn a good amount, if your income isn’t regular or easy to prove, you might find it harder to borrow as much as you’d like.

Can I Get a Mortgage for £2,000 a Month if I Have a Low Income?

If you don’t earn a lot but want a mortgage with monthly payments of £2,000, you might need to think about some other options.

One thing you could do is spread your mortgage over a longer period. This means your monthly payments will be lower, so you might be able to borrow more.

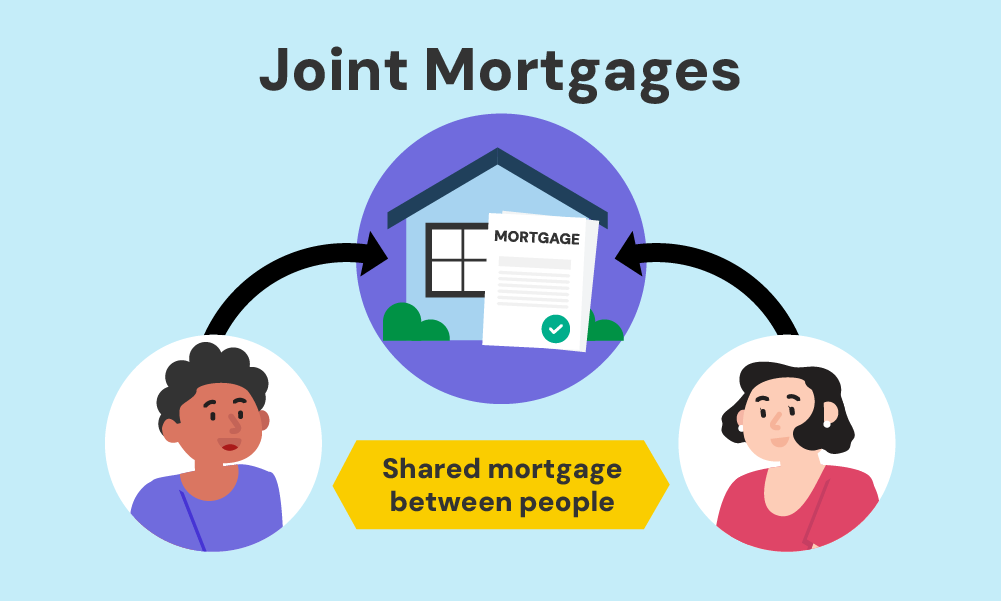

Another option is to get a joint mortgage. This means you combine your incomes, which could help you borrow more. But remember, you’re both responsible for paying it back.

What Proof of Income Do Lenders Require?

To assess your affordability, lenders will ask for proof of your income. You’ll typically need to provide:

- P60 or Employment Contract to show your annual income and employment status.

- Payslips at least three months’ worth of payslips to confirm your monthly income.

- Bank Statements at least three to six months to show financial stability and spending habits.

- A passport or driving licence is needed to verify your identity.

If you’re self-employed, you’ll need to supply additional documents, like tax returns and business accounts.

What Loan-to-Value Ratio Can I Get with £2,000 a Month?

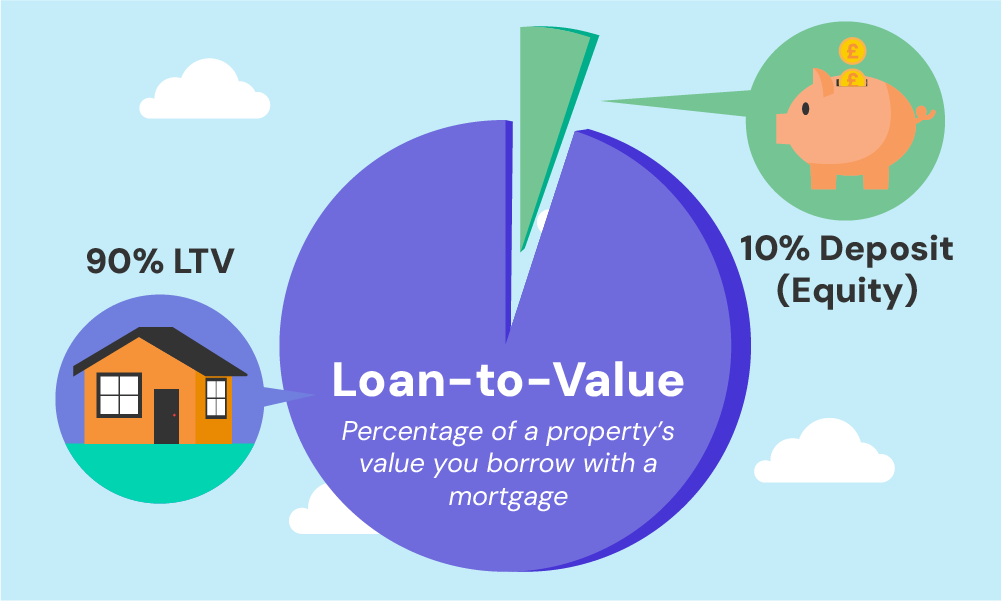

Loan-to-Value (LTV) ratio shows how much you borrow compared to the house price.

For example, if the house is worth £300,000 and you have a £30,000 deposit, you’re borrowing £270,000 – that’s a 90% LTV.

As we’ve discussed, most lenders want you to put down at least 5-10% of the house price.

The more you put down, the better deal you might get on your mortgage and the lower your interest rate could be.

But things like your age or credit score can also affect how much you need to put down.

If you’re seen as a bigger risk, you might need a bigger deposit.

What You’ll Really Pay Beyond Mortgage

Your £2,000 mortgage payment isn’t the only cost you’ll have. There are lots of other things you need to pay for when buying a home.

Here are some of the main ones:

Arrangement fees

This is a charge from the lender to set up your mortgage. It can be anything from £0 to £1,499.

Sometimes, you can add this to your mortgage, but this means you’ll pay more interest in the long run.

Valuation Fees

Before approving a mortgage, the lender will want to check if the house is worth what you’re borrowing.

This usually costs between £150 and £1,500. Some lenders might do this for free, so it’s worth asking.

Legal fees

You’ll need a solicitor to handle all the legal stuff when buying a house.

This can cost between £800 and £1,500, but it depends on how complicated things are. It’s a good idea to get a clear breakdown of costs before you agree.

Stamp Duty

Stamp Duty is a tax you pay when you buy a house. How much you pay depends on the price of the house and if it’s your first home.

If you’re a first-time buyer, you might not need to pay any Stamp Duty up to a certain price.

You can use a stamp duty calculator to see how much you’ll need to pay.

Survey Fees

A survey can help you check the house for any problems. It’s not always needed, but it’s a good idea.

There are different types of surveys.

A basic one costs around £250, while a more detailed one can be up to £1,500. The price depends on how much information you want.

Mortgage Broker Fees

Mortgage brokers can help you find the best mortgage deal. They might charge you a fee, either a fixed amount (usually around £300 to £500) or a percentage of your mortgage.

Sometimes, they get paid by the lender instead. It’s important to check exactly how they make their money.

Home Insurance

Your lender will make you get it as soon as you buy the house. This covers the building itself, in case of things like fire or flooding.

It usually costs around £150 to £300 a year, but the price depends on the size and type of your house.

You might also want insurance for your stuff inside the house, called contents insurance.

Removal Costs

Moving your stuff?

You’ll probably need to hire a removal company, especially if you’ve got lots of furniture or you’re moving a long way.

This could cost you anywhere from £300 to £1,500.

It’s a good idea to get quotes from a few different companies and book in advance, especially if you’re moving at a busy time of year.

Land Registry Fee

You’ll need to pay a fee to officially own the house.

It depends on how much the house costs and is usually between £20 and £910. Your solicitor will take care of this for you.

Ongoing Maintenance and Repairs

Once you own a property, you’re responsible for keeping it in good condition. This means doing repairs and general upkeep.

It’s a good idea to save some money each year for unexpected things that might break or need fixing, especially if your home is old.

You could aim to save about 1% of the house’s value each year.

How Can a Mortgage Broker Help Me?

Sorting out a mortgage can be a headache, especially if you’re trying to stick to a budget.

That’s where a good mortgage broker comes in.

They can:

- Give you personalised advice: They’ll look at your money situation and suggest the best mortgage for you.

- Find you the best deal: Good brokers have access to loads of different mortgages, so they can find you the best one.

- Do the paperwork: Applying for a mortgage is a lot of hassle. A broker can handle most of it for you.

Key Takeaways

- With a £2,000 monthly mortgage, you could borrow between £310,000 and £379,000, depending on your income, term, and interest rate.

- Longer mortgage terms mean lower monthly payments but more interest paid over time.

- Lenders consider your income, debts, credit score, deposit size, profession, and age when deciding how much you can borrow.

- A stable job, good credit, and a larger deposit can improve your mortgage options.

- Budget for extra costs like fees, stamp duty, and home insurance.

The Bottom Line

Getting a mortgage for £2,000 a month isn’t just about your monthly payment.

You need to think about your money situation, understand what affects how much you can borrow, and get advice from an expert to find the best deal.

Want to save time and money? Contact us. We can put you in touch with a mortgage expert for a free, no-obligation consultation to get started.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a buy-to-let mortgage for £2,000 a month?

Yes, you can, but buy-to-let mortgages are usually interest-only and based on rental income rather than your personal income.

Lenders typically require rental income to be 125%-145% of the monthly mortgage payment.

What happens if interest rates rise?

If you’re on a fixed-rate mortgage, your payments won’t change until the fixed period ends. If you’re on a variable-rate mortgage, your payments could increase if interest rates rise.

Related Articles

Getting a Mortgage with Student Loans: What to Know

As someone looking to get on the property ladder, you already know how important it is to have your finances in order. For many, student loans are a big part of that picture, especially when the average student debt for recent graduates in the UK is £45,600. While it may sound like a lot, student […]

Does Overdrafts Affect Your Mortgage Application?

When you’re on the path to homeownership, every financial detail matters. From saving for a deposit to ensuring your credit score is in top shape, the journey is full of hurdles. But what about that overdraft you’ve been dipping into? Can it really affect your mortgage application? Let’s break it down. Can an Overdraft Impact […]

Does Renting Affect Your Mortgage Application?

In today’s housing market, many people find themselves renting for longer periods before making the leap to homeownership. But what happens when your renting history includes missed payments? Can these rent arrears affect your ability to get a mortgage? This article delves into how rent arrears could influence your mortgage application and what you can […]