How Much Do You Need for a Mortgage? Find Out Now

When you’re planning to buy a house, one of the biggest questions you’ll likely have is: How much do you need to earn to get the mortgage you need?

Knowing how much you need to make is really important. It affects how much you can borrow and what kind of home you can get.

In this article, we’ll help you figure out what salary you need and how to make the most of your money.

How Much Income Do You Need for a Mortgage?

The income you need for a mortgage largely depends on how much you want to borrow.

Most UK lenders use a standard income multiple to calculate how much they’ll lend.

Typically, this is around 4 to 4.5 times your annual salary, although some lenders may offer up to 6 times your income under specific circumstances.

Example: If you earn £30,000 per year, a typical lender might offer you a mortgage of up to £135,000 based on a 4.5 times income multiple.

If you’re earning £50,000, this could rise to £225,000.

Here’s a breakdown of how income multiples translate to potential mortgage amounts:

| Annual Salary | 4x Income | 4.5x Income | 5x Income | 6x Income |

|---|---|---|---|---|

| £30,000 | £120,000 | £135,000 | £150,000 | £180,000 |

| £40,000 | £160,000 | £180,000 | £200,000 | £240,000 |

| £50,000 | £200,000 | £225,000 | £250,000 | £300,000 |

| £60,000 | £240,000 | £270,000 | £300,000 | £360,000 |

| £70,000 | £280,000 | £315,000 | £350,000 | £420,000 |

What Salary Do You Need for a £700k or £800k House in the UK?

Higher property prices mean you’ll need a higher salary to secure the mortgage.

For example, to afford a £700,000 house, your income would need to be enough, especially if you’re aiming for a lower deposit.

Let’s break it down:

For a £700k House:

- 4x Income: You’d need an income of £175,000.

- 4.5x Income: You’d need an income of £155,556.

- 5x Income: You’d need an income of £140,000.

- 6x Income: You’d need an income of £116,667.

For an £800k House:

- 4x Income: You’d need an income of £200,000.

- 4.5x Income: You’d need an income of £177,778.

- 5x Income: You’d need an income of £160,000.

- 6x Income: You’d need an income of £133,333.

Here’s a table summarising these figures:

| House Price | 4x Salary | 4.5x Salary | 5x Salary | 6x Salary |

|---|---|---|---|---|

| £700,000 | £175,000 | £155,556 | £140,000 | £116,667 |

| £800,000 | £200,000 | £177,778 | £160,000 | £133,333 |

What About a £600k or £450k Mortgage?

If your target is a £600,000 or £450,000 mortgage, the required salary is slightly more attainable, but still demands a significant income.

For a £600k Mortgage:

- 4x Income: You’d need an income of £150,000.

- 4.5x Income: You’d need an income of £133,333.

- 5x Income: You’d need an income of £120,000.

- 6x Income: You’d need an income of £100,000.

For a £450k Mortgage:

- 4x Income: You’d need an income of £112,500.

- 4.5x Income: You’d need an income of £100,000.

- 5x Income: You’d need an income of £90,000.

- 6x Income: You’d need an income of £75,000.

Here’s how the numbers look:

| Mortgage Amount | 4x Salary | 4.5x Salary | 5x Salary | 6x Salary |

|---|---|---|---|---|

| £600,000 | £150,000 | £133,333 | £120,000 | £100,000 |

| £450,000 | £112,500 | £100,000 | £90,000 | £75,000 |

How Does Affordability Work in Practice?

While your income gives you a general idea, lenders also look at your spending habits to see if you can afford a mortgage.

They compare your income to your expenses to see how much money you have left over each month.

Here’s how it works:

Lenders calculate your monthly income, including your salary and other sources like bonuses or rental income. Then, they subtract your regular expenses, such as:

- Rent or mortgage: If you already have a home, this will be deducted.

- Bills: Gas, electricity, water, and council tax can cost between £100 and £300 per month.

- Insurance: Home, car, and life insurance might cost £50 to £150.

- Loans: Any personal loans, car finance, or credit card debt.

- Childcare: If you have children, this can be expensive.

- Living costs: Food, transport, and other daily expenses.

After subtracting these expenses, you have your disposable income. The more you have left over, the more you can borrow.

How This Affects Your Mortgage

- High disposable income – If you have a lot of money left over each month, lenders are more likely to offer you a larger mortgage.

- Low disposable income – If you have little money left over, lenders might offer you a smaller mortgage.

Example:

If you earn £50,000 per year and want to borrow £225,000, but your expenses are high, the lender might only offer you £180,000. However, if your expenses are low, you might qualify for the full amount.

To improve your affordability, you can:

- Reduce expenses or find cheaper deals.

- Pay off debts to increase your disposable income.

- Save a bigger deposit to appear more attractive to lenders.makes you less risky for lenders.

How Much Deposit Do You Need?

Your deposit size is key to getting a mortgage.

Most lenders usually require at least a 10% deposit, but a 20% deposit can give you better mortgage options, including lower interest rates and a higher borrowing limit.

For example:

- 10% Deposit: For a £200,000 house, you’d need £20,000.

- 20% Deposit: For a £200,000 house, you’d need £40,000.

Can You Increase Your Mortgage Eligibility?

Yes, you can often increase your mortgage eligibility. Here are a few ways to do this:

Increase Your Deposit

A larger deposit reduces the lender’s risk, making you eligible for a bigger mortgage or better interest rates.

Aim for at least a 20% deposit, as this often unlocks more competitive deals.

If saving is tough, consider a Lifetime ISA, where the government adds a 25% bonus to your savings, up to £1,000 per year.

Improve Your Credit Score

Your credit score is crucial for mortgage approvals.

Check your credit report regularly to ensure it’s accurate. Pay off debts, avoid late payments, and lower your credit card balances.

Simple steps like registering to vote and limiting credit applications can also boost your score.

Consider Joint Applications

Combining incomes with a partner or family member can significantly increase your borrowing power.

Some UK lenders even consider joint applications with more than two applicants, which can be useful if you’re pooling resources to buy a home.

Reduce Debt

Paying off debts before applying for a mortgage can improve your affordability score.

Clear credit cards, personal loans, and car finance.

The less you owe, the more disposable income you have, making you a more attractive borrower.

Show Stable Employment

Lenders prefer applicants with stable jobs. If possible, avoid changing jobs or industries shortly before applying.

Being in the same job for at least two years can reassure lenders of your financial stability.

Minimise Financial Commitments

Lenders consider your overall financial obligations when assessing your mortgage application.

Reducing commitments like personal loans, car finance, and even unnecessary subscriptions can improve your affordability.

Avoid taking on new financial commitments before applying for a mortgage.

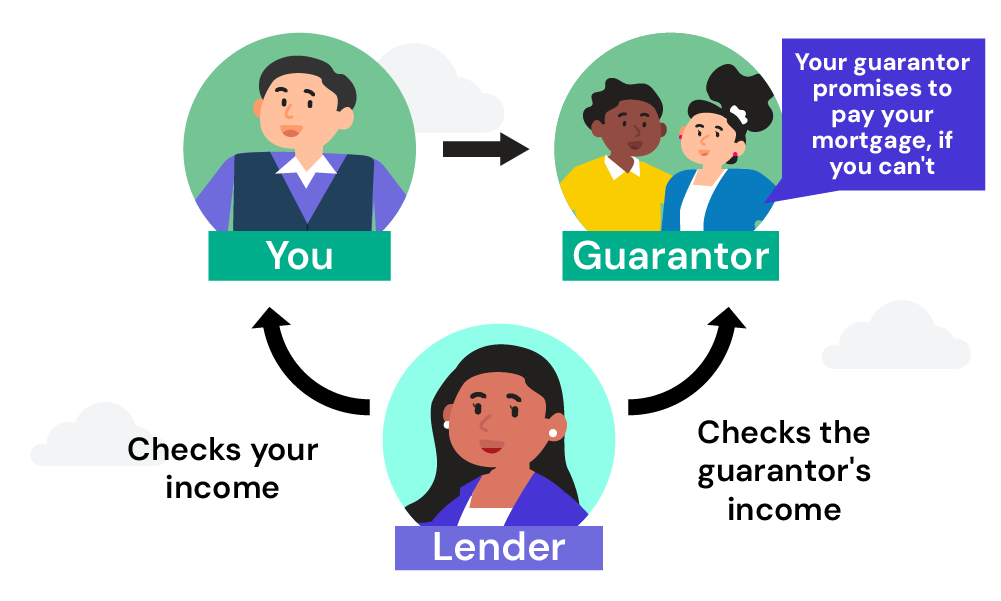

Consider a Guarantor Mortgage

If you’re struggling to meet eligibility criteria, a guarantor mortgage might be an option.

A family member, usually a parent, agrees to cover the mortgage payments if you’re unable to.

This can help you secure a mortgage when you don’t meet the standard criteria on your own.

Opt for a Longer Mortgage Term

Extending your mortgage term can lower your monthly payments, making it easier to pass affordability checks.

While this means you’ll pay more interest over time, it can be a practical way to increase your borrowing potential.

Seek Professional Advice

A good mortgage broker can be invaluable.

They have access to deals that aren’t available directly to consumers and can guide you to lenders who offer higher income multiples or more flexible terms based on your situation.

They can also advise on government schemes like First Homes or Shared Ownership.

Key Takeaways

- Lenders typically offer mortgages up to 4 to 4.5 times your salary; some go up to 6 times.

- To buy a £700k-£800k house, you’ll need an income of £116,667 to £200,000.

- High disposable income improves your chances of getting a larger mortgage.

- A 10-20% deposit can get you better mortgage deals.

- Increase your eligibility by saving more, improving your credit score, reducing debt, and getting advice from a mortgage broker.

The Bottom Line

After reading this article, you might be wondering if your dream home is really achievable.

While the information here can give you a general idea, your specific financial situation is key.

To get the most accurate and tailored advice, it’s best to speak to a qualified mortgage broker. They can assess your situation, explore your options, and help you find the best deal.

If you want to save time and avoid the hassle, get in touch with us. We’ll connect you with a trusted broker who can help with your specific mortgage needs.

Get Matched With Your Dream Mortgage Advisor...

Frequently asked questions

How does joint income affect my mortgage eligibility?

Joint income can significantly increase your borrowing potential, allowing you to afford a more expensive property.

Can I get a mortgage with a low credit score?

Yes, but it may limit your options. Improving your credit score before applying can help you secure better terms.

How much do you need to earn to buy a house?

The amount you need to earn to buy a house depends on the property price and what the lender will allow you to borrow. In the UK, lenders usually offer mortgages of up to 4 to 4.5 times your yearly salary.

For example, to buy a £200,000 house, you’d need a yearly income of about £44,444 to £50,000. But some lenders might offer up to 6 times your income, so you could borrow more if you earn more.

What salary do you need for an £800k house in the UK?

To afford an £800,000 house in the UK, you’d need a salary of between £133,333 and £200,000, depending on what the lender will allow you to borrow.

Most lenders offer up to 4 to 4.5 times your salary, but some might offer up to 6 times, especially for wealthy people or those with a big deposit.

A bigger deposit and a good credit score can also help you get a mortgage for this amount.

Related Articles

Getting a Mortgage with Student Loans: What to Know

As someone looking to get on the property ladder, you already know how important it is to have your finances in order. For many, student loans are a big part of that picture, especially when the average student debt for recent graduates in the UK is £45,600. While it may sound like a lot, student […]

Does Overdrafts Affect Your Mortgage Application?

When you’re on the path to homeownership, every financial detail matters. From saving for a deposit to ensuring your credit score is in top shape, the journey is full of hurdles. But what about that overdraft you’ve been dipping into? Can it really affect your mortgage application? Let’s break it down. Can an Overdraft Impact […]

Does Renting Affect Your Mortgage Application?

In today’s housing market, many people find themselves renting for longer periods before making the leap to homeownership. But what happens when your renting history includes missed payments? Can these rent arrears affect your ability to get a mortgage? This article delves into how rent arrears could influence your mortgage application and what you can […]