- Who Qualifies as a Foreign National for UK Mortgages?

- Mortgage Eligibility for Foreign Nationals

- Getting a UK Mortgage With a Visa

- How Much Can I Borrow?

- How Do I Get a Mortgage With Less Than 3 Years Living in the UK?

- How Much Deposit Do I Need as a Foreign National?

- Does Having No Credit History in the UK Stop Me Getting a Mortgage?

- Can I Get a Buy-to-Let Mortgage as a Foreigner?

- Tips for Getting Approved as a Foreign National

- The Bottom Line: The UK Welcomes Foreign Homebuyers

Can Foreigners Get a Mortgage in the UK? A Complete Guide

Foreign nationals can get a mortgage and buy property in the UK. However, the mortgage process and requirements can be more complex compared to British citizens.

This guide covers everything you need to know about getting a mortgage as a foreigner living in or moving to the UK.

Who Qualifies as a Foreign National for UK Mortgages?

The term “foreign national” encompasses anyone who doesn’t hold a UK passport or permanent UK residency. This includes:

- Non-UK Citizen with Leave to Remain or Permanent Residency – You weren’t born in the UK, but you’re allowed to live here as long as you want.

- Non-UK Resident or No Permanent Residency – You don’t live in the UK or don’t have permission to live here indefinitely.

- EU Citizen – As an EU citizen, some of the above might apply to you (requirements may differ post-Brexit).

It doesn’t matter where you’re originally from – the key factor is your current immigration status in the UK.

Mortgage Eligibility for Foreign Nationals

Your path to mortgage approval depends mainly on your residency status and income situation in the UK.

Here are the key categories lenders assess:

Permanent Residents

If you have indefinite leave to remain (ILR) or permanent residency, getting a mortgage approval works very similarly to a UK citizen.

You’ll need to meet the standard requirements like:

- Minimum 2 years of residency in the UK

- Stable job/employment income

- Good UK credit history and score

- Minimum 5-10% deposit (or more with less than 2 years residency)

Building a strong credit footprint from the day you arrive is crucial. Opening a UK bank account, getting on the electoral roll, and paying all bills punctually from local accounts boosts your mortgage chances.

EU/EEA Nationals

Before Brexit EU citizens could more easily get UK mortgages by just showing 2+ years of residency. Now the rules align closer to requirements for non-EU nationals.

As an EU/EEA national, you’ll generally need to provide:

- Proof of permanent UK residency

- Stable job and income source within the UK

- Established UK credit report and score

- Minimum 10-15% deposit

Having an EU credit history can be an advantage, as it may transfer more readily to UK lenders versus starting fresh.

Non-Residents

Not currently residing in the UK makes you a higher mortgage risk in lenders’ eyes. You’ll face much tougher financial scrutiny and need to check more boxes like:

- Larger deposit of at least 25%, sometimes 30%+

- Proof of substantial income/assets to repay the loan

- Significant evidence of ties or footprint in the UK (previous residency, job, family etc.)

- Having an accepted visa type like ancestry, spouse, investor etc.

Without residency, satisfying stringent identity, source of income, and anti-money laundering checks from lenders is required.

Getting a UK Mortgage With a Visa

Many different visa types can allow foreigners to get a mortgage, though some are viewed more favourably than others:

Work Visas

Skilled work visas like the Skilled Worker, Intra-Company, and Representative of an Overseas Business visa are acceptable to many lenders. These show you have permission to legally work and remain in the UK.

Ideally, the work visa should have at least 2-3 years’ validity remaining when applying for a mortgage. That provides lenders confidence you’ll be able to keep your job and repay long-term.

Family Visas

The UK spouse/partner and unmarried partner visas are another viable path to getting a mortgage.

Having a permanent British citizen or resident as a co-applicant helps reassure the lender.

Investor and Entrepreneur Visas

High net-worth individuals can potentially qualify for UK mortgages with visas like the Investor and Innovator/Start-Up visas.

These require significant investment in the UK, which shows commitment and wealth to back a mortgage.

Student Visas

It’s challenging but not impossible to get a UK mortgage on a student visa like the Student Route.

You’ll need a very large deposit, confirmed income, and a near-guaranteed path to post-study work/residency.

Ancestry Visa

The UK Ancestry visa for Commonwealth citizens can work for getting a mortgage if you have strong, provable ties to the UK like a job lined up. Having previously lived in the UK also boosts chances.

Again, speaking to a knowledgeable mortgage broker is highly recommended with any of these visa types. They’ll know which lenders are most amenable based on your specific situation.

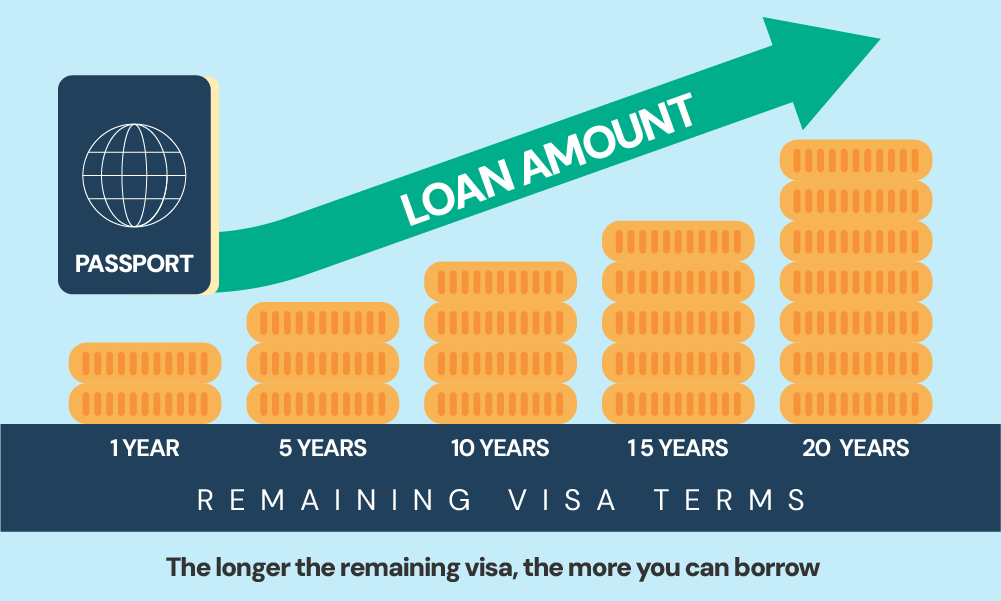

How Much Can I Borrow?

Several factors influence how much you can borrow for a mortgage as a foreign national in the UK. Lenders typically use an income multiplier of 4 to 4.5 times your annual salary.

If you’re applying with a partner, your combined income increases your borrowing power. Be prepared to show employment contracts and payslips as proof of income.

Foreign nationals often require a larger deposit, ranging from 25% to 40% of the property value, to mitigate the lender’s risk.

While a strong UK credit history is helpful, it’s not necessarily essential. What truly matters is stable employment in the UK or documented proof of income for self-employed applicants.

The length and type of your visa also play a role. A longer visa with more years remaining allows you to borrow a larger sum.

Finally, lenders will assess your existing debts and financial commitments to ensure you can comfortably manage the mortgage payments.

How Do I Get a Mortgage With Less Than 3 Years Living in the UK?

Getting a mortgage with less than 3 years’ residency in the UK isn’t impossible, but it’s more difficult. Most lenders want to see at least 2-3 years of UK credit history.

However, some key tips are:

- Get a permanent job and open a UK bank account as soon as possible

- Save the biggest deposit you can afford – around 25% is ideal

- Use a broker to access lenders more flexible on residency requirements

- Provide thorough documentation like job contracts, visa details etc.

So it comes down to building that residency paper trail and demonstrating long-term stability. The longer you’ve been in the UK, the better.

How Much Deposit Do I Need as a Foreign National?

For foreign nationals, bigger deposits are preferred – think 20% or higher. The more you can put down upfront, the lower the lender’s risk.

A deposit of around 25% (75% loan-to-value) is ideal and gives you the best chance, especially with less than 2 years of UK residency.

Of course, every lender is different. But increasing your deposit shows commitment and boosts your chances.

Does Having No Credit History in the UK Stop Me Getting a Mortgage?

No, it doesn’t necessarily stop you from getting a mortgage as a new arrival. Many foreign nationals get UK mortgages with little to no local credit history.

The key things lenders assess are:

- Ability to earn a stable income in the UK

- Intention to remain long-term (visa validity)

- Ability to repay the mortgage amount

So providing documentation like employment contracts, six months’ payslips, etc proves you’re low risk – even without a local credit file.

However, as discussed, building some credit history helps smooth approval.

Can I Get a Buy-to-Let Mortgage as a Foreigner?

In addition to residential mortgages, foreign nationals can qualify for buy-to-let mortgages to invest in UK rental properties. The requirements closely mirror those for a standard mortgage:

For UK Residents

- Minimum 2 years residency

- Proof of stable employment/income

- Good UK credit score

- Minimum 20-25% deposit

For Non-Residents

- Larger deposit of 25%+ (some lenders want 35%+)

- Must pass strict background, anti-money laundering checks

- Proof of substantial income/assets/UK ties

- Accepted visa type

The mortgage underwriting process for non-resident buy-to-let is extremely rigorous. Using an experienced broker is highly recommended to navigate the complexities.

Tips for Getting Approved as a Foreign National

While getting a UK mortgage is achievable as a foreigner, it does require diligent preparation to present yourself as a low-risk borrower:

- Maximise Your Deposit. Whether a resident or not, a larger deposit of 25% or more shows financial commitment. This minimises risk for lenders and improves mortgage eligibility.

- Build Your Credit Profile. Establish a robust, traceable UK credit footprint as soon as you arrive. Getting credit accounts like a mobile phone plan, opening a UK bank account, and religiously paying all bills boost your credit score.

- Organise Documents Upfront. Have at least 6 months’ worth of payslips, job contract details, bank statements, residency documentation, and identification ready. Being organised and transparent smooths the underwriting process.

- Explain Your UK Connections. If a non-resident, highlight ties to the UK such as previous residencies, family connections, property ownership, education history etc. This evidence shows commitment to staying long-term.

- Enlist a Mortgage Broker. An independent mortgage broker experienced with foreign nationals is invaluable. They can match your profile to amenable lenders, prepare your application comprehensively, and negotiate the best rates.

The Bottom Line: The UK Welcomes Foreign Homebuyers

Despite more regulatory hurdles, getting a mortgage as a foreign national is readily achievable in the UK housing market. The key is illustrating you have the financial means and longer-term stability to reliably repay the loan.

While permanent UK residents face requirements akin to British citizens, admittedly the process is more arduous for recent arrivals and non-residents.

With perseverance, adequate documentation, and guidance from a broker, that dream of UK home ownership can become a reality no matter where you hail from.

Need a broker? Get in touch with us. We’ll connect you with a good mortgage broker for a free, no-obligation consultation to help you get a foreign national mortgage.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a mortgage as a foreign national even with bad credit?

Yes, it’s possible to get a mortgage as a foreign national even with bad credit, but it will be more challenging.

Lenders see borrowers with bad credit as riskier, so expect higher interest rates and stricter terms. Here’s what can help:

- Offer a bigger deposit

- Prove steady income

- Talk to a specialist broker

- Improve your credit score

While bad credit makes securing a mortgage trickier, it’s not out of reach. Consulting a mortgage broker can help you navigate your options and find a lender that suits your situation.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]