- What Changes Affect Your Mortgage Application?

- Can a Change in Circumstances End Your Mortgage Offer?

- How To Tell Your Lender About Changes?

- Mortgage Rules When Things Change

- What Happens If You Change the Property You Want to Buy?

- How Changes in Circumstances Affect Your Credit Score

- Can You Extend or Amend a Mortgage Offer Due to a Change in Circumstances?

- What To Do If Your Situation Changes After a Mortgage Offer

- Can You Still Get a Mortgage If Your Circumstances Change?

- What Are the Alternatives If Your Mortgage Offer Is Withdrawn?

- Key Takeaways

- The Bottom Line

How A Change of Circumstances Affect Your Mortgage

Plans don’t always go smoothly, and applying for a mortgage is no exception.

Whether it’s a new job, changed income, or something more serious, unexpected changes can happen.

This article explains how these changes might affect your mortgage offer, how to handle them, and the rules you must follow to stay on track.

What Changes Affect Your Mortgage Application?

Lenders expect your circumstances to stay the same from applying for a mortgage to completing it.

However, life doesn’t always follow the plan. Changes like these can affect your mortgage:

- Job changes – Switching jobs, becoming self-employed, or redundancy.

- Income changes – Pay rises, pay cuts, or new income sources.

- Credit score changes – New debts, missed payments, or a changed credit score.

- Property changes – Deciding to buy a different property.

- Life events – Serious illness, divorce, or other major life changes.

Tell your lender about any changes. They can affect your mortgage offer.

Some changes might mean your mortgage terms change, while others could end your mortgage offer.

Can a Change in Circumstances End Your Mortgage Offer?

Yes, changes can end your mortgage offer. Lenders base mortgage offers on the information you give when you apply.

If big changes happen that affect your ability to repay the loan, the lender might change their mind.

For example, losing your job or a big drop in income could end the offer because it’s riskier for the lender.

Even smaller changes like choosing a different house can cause problems.

If the new house is worth more or less than the old one, it can affect the loan amount the lender will give you.

How To Tell Your Lender About Changes?

The first step is to contact your mortgage broker or lender as soon as possible.

They’ll tell you what to do next. This might mean giving them new documents or reassessing your application.

For example, if you’ve changed jobs, you may need to submit a new employment contract or pay slips.

If your finances change a lot, like a pay cut, the lender might ask for new bank statements or to check if you can afford the mortgage.

Mortgage Rules When Things Change

Different lenders have slightly different rules, but most follow these basics:

- Tell the truth. You must legally notify your lender about any changes that could affect your mortgage. If you don’t, they could cancel your mortgage offer.

- Lender checks again. If you tell your lender about a change, they might look at your mortgage offer again. This could mean a new credit check, looking at your finances again, or valuing the property again.

- Credit score hit. If your lender cancels your mortgage offer, it could damage your credit score.

What Happens If You Change the Property You Want to Buy?

It’s more common than you think to change your mind about which house to buy after getting a mortgage offer.

Here’s what happens:

- Revaluation – The lender will need to conduct a new valuation on the new property to ensure it meets their criteria. If the new property is cheaper, you might be asked to maintain the same LTV ratio, which could mean putting down a larger deposit. Conversely, if it’s more expensive, you may need to increase your deposit to stay within the lender’s maximum LTV.

- New Terms – The property type can also affect the mortgage terms. For example, if you switch from a freehold house to a leasehold flat, the lender might have different rules or restrictions.

How Changes in Circumstances Affect Your Credit Score

Changes in your life don’t usually affect your credit score directly, but they can have an indirect impact.

For example, if a lender cancels your mortgage offer, it will show on your credit report as a failed application, which could lower your score.

Also, if money gets tight because of changes, and you miss payments, your credit score will suffer.

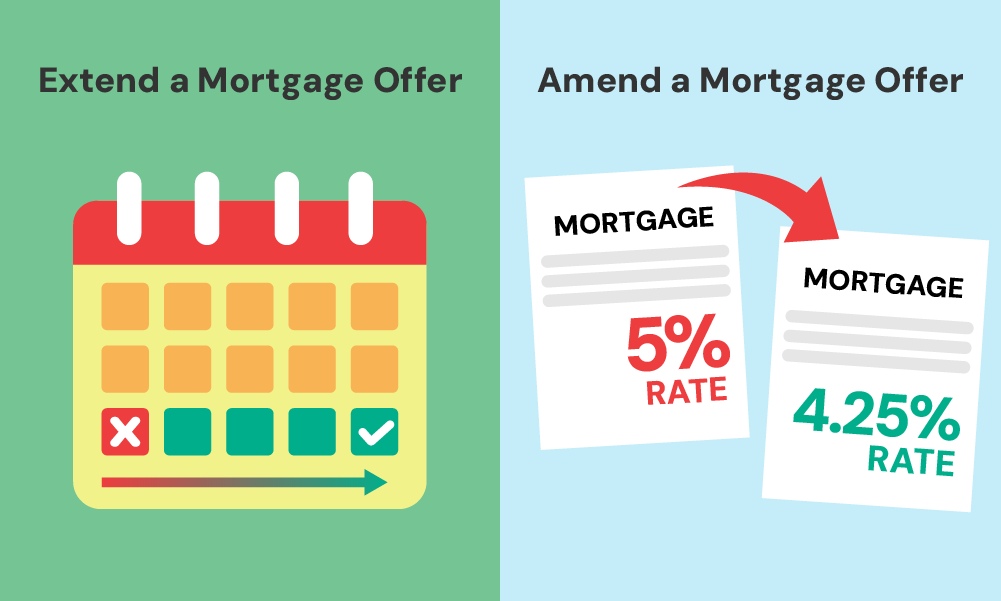

Can You Extend or Amend a Mortgage Offer Due to a Change in Circumstances?

If your life changes while you’re applying for a mortgage, you might be able to adjust the offer.

Extending a Mortgage Offer

If you think your situation will improve soon (like starting a new job), you can ask the lender for extra time to complete the mortgage.

They might agree to extend the offer by a few months if they believe your finances will become stable.

Amending a Mortgage Offer

If your changes mean you can borrow less or need to pay more upfront, the lender might change the details of the mortgage.

This could involve altering the amount you borrow, the interest rate you pay, or how long you have to repay the loan.

What To Do If Your Situation Changes After a Mortgage Offer

If your life changes after you’ve received a mortgage offer, here’s what to do:

- Tell your lender straight away. Be honest with your lender about what’s happened. The sooner you tell them, the easier it will be to deal with the situation.

- Gather your paperwork. Get together any documents that prove the changes, like a new job contract, updated bank statements, or a valuation report for a new property.

- Talk to your mortgage broker. A good mortgage broker can give you advice and help you deal with the lender. They can also find other options if needed.

Can You Still Get a Mortgage If Your Circumstances Change?

Yes, you can still get a mortgage even if your situation changes, but you might need to make adjustments.

If you earn less money, you might need to borrow less or take longer to pay it back.

If you’ve had financial problems, a specialist mortgage broker can help you find a lender who will accept you.

What Are the Alternatives If Your Mortgage Offer Is Withdrawn?

If your mortgage offer is cancelled, don’t worry. There are other things you can try:

- Try a new lender. You might be able to get a mortgage from a different lender. You might need to give them extra information or accept different terms.

- Use a specialist lender. If normal lenders won’t help, there are lenders who specialise in people with more complicated financial situations.

- Check government schemes. There are government plans that can help if your situation has changed.

Key Takeaways

- Changes like switching jobs, income adjustments, property choices, or personal life events can impact your mortgage application and offer.

- Always inform your lender about any changes to avoid issues like offer withdrawal or reassessment.

- If you change the property you want to buy, the lender will need to revalue it, which could alter your loan terms.

- Failing to notify your lender about changes can hurt your credit score if the offer is withdrawn.

- You can request to extend or amend your mortgage offer if your situation is likely to improve, such as starting a new job.

The Bottom Line

Changes in your life while you’re applying for a mortgage can be stressful, but you can handle them.

Be proactive, talk openly to your lender, and get expert advice to get the mortgage you need.

It’s really important to be honest with your lender. Whether you change jobs, decide on a different house, or your finances change, tell them straight away. This will help everything go smoothly.

If you’re unsure what to do, talk to a mortgage broker. They can give you specific advice and guide you through the process.

Need help? Get in touch, and we’ll connect you with a mortgage broker who understands your situation and helps you secure the right mortgage deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Do I need to inform my lender if I change jobs during the mortgage application process?

Yes, you must inform your lender if you change jobs. A change in employment can impact your income stability, which is a key factor in a lender’s decision.

Your lender may need to reassess your application to ensure you still meet their criteria.

Can I change the property I want to buy after receiving a mortgage offer?

Yes, you can change the property, but you must notify your lender.

They will likely need to conduct a new valuation on the new property, and this could affect your loan-to-value (LTV) ratio and the terms of your mortgage offer.

What happens if a property survey reveals problems? Can I renegotiate the purchase price?

If a survey highlights issues like structural problems, defective wiring, or other defects, you can negotiate with the seller to reduce the purchase price.

If the price is reduced, you’ll need to inform your lender, as this could affect your mortgage offer and the amount you’re borrowing.

What should I do if my personal circumstances change after receiving a mortgage offer?

If your personal circumstances change, such as a reduction in income or an increase in debt, it’s important to inform your lender immediately.

The lender may need to reassess your application, and this could lead to an amended mortgage offer or, in some cases, a withdrawal of the offer.

Can a mortgage offer be withdrawn due to a change in circumstances?

Yes, a mortgage offer can be withdrawn if there is a significant change in your circumstances that affects your ability to repay the loan.

This could include job loss, a drop in income, or adverse changes to your credit report.

How can I avoid complications if I want to renegotiate the mortgage offer?

To avoid complications, be transparent with your lender and provide all necessary documentation related to the change.

This could include new job contracts, updated financial statements, or quotes for repairs if the price is being renegotiated due to survey findings.

Is it possible to extend a mortgage offer if my situation is likely to improve?

Yes, if you expect your situation to improve, such as starting a new job soon, you can ask your lender to extend the mortgage offer. Lenders may grant extensions if they believe your financial situation will stabilise.

What are the risks of accepting cash from a seller to cover property defects?

Accepting cash from a seller to cover defects can be risky. It’s important to formalise any agreements through your solicitor to ensure the transaction is legally protected.

Informal arrangements without the knowledge of your solicitor or lender could lead to legal complications later on.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]