- Can You Get a Mortgage If You Have Cancer?

- What Should You Tell Your Mortgage Lender?

- How Does Cancer Affect Your Mortgage Application?

- What Types of Mortgages Are Available?

- The Pros and Cons of Getting a Mortgage with Cancer

- How Can You Improve Your Chances of Mortgage Approval?

- What If You’re Already a Homeowner?

- Are There Government Schemes That Can Help?

- What About Mortgage Insurance?

- Key Takeaways

- The Bottom Line: Where Can You Get Advice?

How To Get A Mortgage With Health Problems Like Cancer?

Many people think a cancer diagnosis means kissing their mortgage dreams goodbye. But that’s not true.

Lenders care more about whether you can pay back the loan than about your health.

While it’s true, cancer might make things a bit trickier as it affects your income and how much you can borrow. But it doesn’t mean you can’t get a mortgage at all.

This guide explains how to secure a mortgage with health problems, the types of mortgages available, and tips to boost your chances of approval.

Can You Get a Mortgage If You Have Cancer?

Having cancer doesn’t mean you can’t get a mortgage.

Many people worry about getting a mortgage with health problems. But it’s important to know that having cancer doesn’t automatically disqualify you from homeownership.

Lenders care more about your ability to repay the loan than your medical history.

However, your diagnosis might affect parts of the mortgage process, so it’s important to know how to handle this.

Lenders will check your income, expenses, and financial stability. If cancer has impacted your work or income, it might influence your decision.

But don’t worry – with the right approach, you can still achieve your goal of owning a home.

What Should You Tell Your Mortgage Lender?

You’re NOT legally obligated to disclose your cancer diagnosis to a mortgage lender.

However, if you think your condition might affect your ability to make repayments, it’s wise to be upfront about your situation.

Honesty can help you find the most suitable mortgage product and avoid potential issues down the line.

When discussing your circumstances with a lender, focus on your current financial situation and future prospects.

Explain any changes to your income or employment status. And provide information about your treatment plan and prognosis if you’re comfortable doing so.

This transparency can help the lender make a more informed decision and potentially offer tailored solutions.

How Does Cancer Affect Your Mortgage Application?

Cancer can impact your mortgage application in several ways.

Firstly, if you’ve had to cut back on work or take time off for treatment, your income might have dropped. This could impact how much you can borrow or meet the affordability criteria.

Secondly, some lenders might be more cautious about approving a mortgage for someone with a serious health condition.

They might ask for extra documentation or assurances about your ability to keep up with payments long-term.

Lastly, getting mortgage-related insurance, like life insurance or critical illness coverage, could be tougher or more expensive with a cancer diagnosis.

However, these insurance products are often separate from the mortgage itself.

What Types of Mortgages Are Available?

When getting a mortgage with health problems like cancer, you still have access to various mortgage types. These include:

- Repayment mortgages – You pay off both the loan and interest each month.

- Interest-only mortgages – You pay only the interest monthly and repay the loan at the end of the term.

- Fixed-rate mortgages – The interest rate remains the same for a set period.

- Variable-rate mortgages – The interest rate can fluctuate based on market conditions.

- Flexible mortgages – These allow overpayments, underpayments, and payment holidays.

For those over 55, lifetime mortgages (equity release) might be an option. These don’t require monthly repayments, as the loan and interest are repaid when you die or move into long-term care.

The best mortgage type for you will depend on your circumstances, including your cancer diagnosis, treatment plan, and financial situation.

The Pros and Cons of Getting a Mortgage with Cancer

Getting a mortgage with a cancer diagnosis can be tricky, but it’s doable.

Here’s a quick look at the upsides and downsides to help you decide.

Pros

- You get a stable home for you and your family.

- It’s a good investment that might grow in value over time, adding to your financial security.

- Owning a home can give you a sense of stability and peace of mind.

- Some insurers offer tailored policies for people with pre-existing conditions.

Cons:

- Mortgages and insurance might cost more due to higher perceived risk.

- Fewer lenders might be willing to offer you a mortgage.

- You might need a bigger deposit or face stricter checks.

- Getting life insurance or critical illness coverage could be harder and more expensive.

- Managing a mortgage during cancer treatment can add financial stress, especially if your work is affected.

How Can You Improve Your Chances of Mortgage Approval?

To increase your chances of getting a mortgage with cancer, consider these steps:

- Maintain a good credit score – Pay bills on time and manage your debts responsibly.

- Save for a larger deposit – A bigger down payment can make you a more attractive borrower.

- Provide evidence of stable income – If you’re still working, get a letter from your employer confirming your position and salary.

- Get your finances in order – Create a detailed budget showing your income and expenses.

- Consider a guarantor – A family member might be willing to act as a guarantor, which can reassure lenders.

- Speak to a specialist mortgage broker – They can help you find lenders who are more likely to consider your application.

Remember, every lender has different criteria, so don’t be discouraged if one turns you down. Keep exploring your options.

What If You’re Already a Homeowner?

If you already have a mortgage and are diagnosed with cancer, you should contact your lender if you’re worried about making repayments.

Many lenders have policies to support customers facing health challenges. They might offer options like:

- Payment holidays to temporarily suspend or reduce your payments.

- Extend your mortgage term to lower your monthly payments.

- Switching to an interest-only mortgage to reduce your monthly outgoings and mortgage payments.

It’s key to communicate with your lender early if you’re experiencing financial difficulties.

They’re required to consider ways to help you, and early intervention can prevent more serious problems later on.

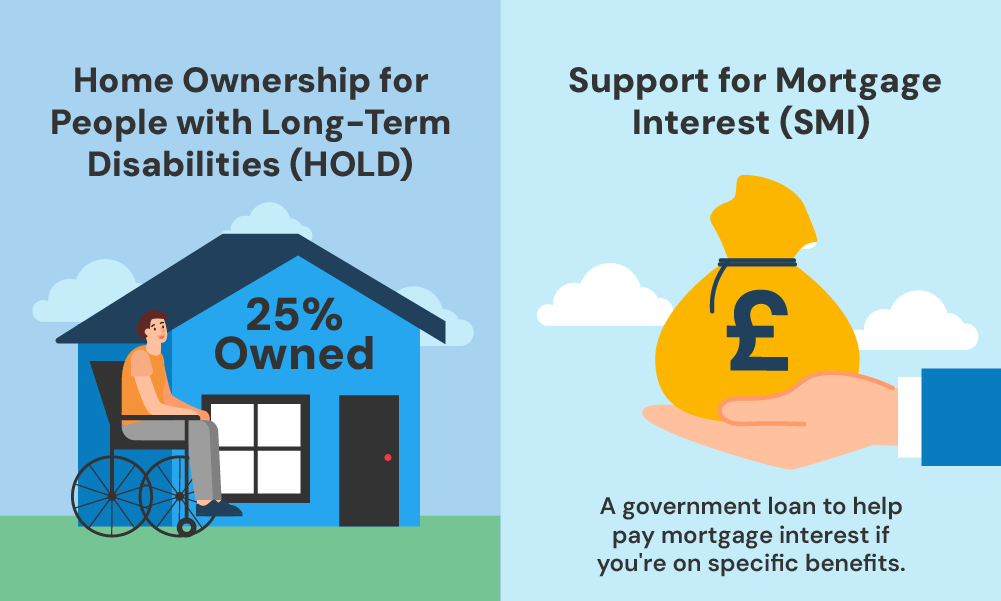

Are There Government Schemes That Can Help?

The UK government offers several schemes that might be helpful if you’re getting a mortgage with health problems:

- Support for Mortgage Interest (SMI). If you’re receiving certain benefits, you might be eligible for help with mortgage interest payments after 39 weeks.

- HOLD (Home Ownership for People with Long-term Disabilities). This shared ownership scheme allows you to buy a share of a property (between 25% and 75%) and pay rent on the remaining share.

These schemes have specific eligibility criteria, so it’s worth researching to see if you qualify.

What About Mortgage Insurance?

When getting a mortgage, lenders often recommend or require insurance to protect the loan.

Common types include:

- Life Insurance ensures that your mortgage is paid off if you pass away during the term of the policy.

- Critical Illness Cover offers a lump sum payment if you are diagnosed with a specified serious illness, such as cancer, heart attack, or stroke.

- Mortgage Payment Protection Insurance (MPPI) pays out a monthly benefit to cover your mortgage repayments if you are unable to work due to illness, injury, or unemployment.

With a cancer diagnosis, obtaining these insurances can be more challenging or expensive.

However, some specialist insurers offer policies for people with pre-existing conditions.

It’s worth shopping around and speaking to an insurance broker who specialises in this area.

If you already have insurance policies, check if they cover your mortgage repayments in case of illness. You might be able to add this coverage to existing policies.

Key Takeaways

-

- Being diagnosed with cancer doesn’t stop you from getting a mortgage.

-

- You don’t have to inform your lender about your health condition unless it affects your ability to pay your mortgage.

-

- If you’re struggling with payments, ask your lender about options like payment holidays, mortgage extensions, or switching to an interest-only mortgage to manage your repayments.

-

- Consider schemes like Support for Mortgage Interest (SMI) and HOLD (Home Ownership for People with Long-term Disabilities) for affordable homeownership.

-

- Life Insurance, Critical Illness Coverage, and Mortgage Payment Protection Insurance (MPPI) can offer peace of mind if you’re unable to repay your mortgag

The Bottom Line: Where Can You Get Advice?

Here’s where you can find help:

- Cancer charities – Organisations like Macmillan Cancer Support offer financial guidance for people affected by cancer.

- Citizens Advice – They can provide free, impartial advice on housing and financial issues.

- The Money Advice Service – This government-backed service offers free, unbiased money advice.

- Specialist mortgage brokers – These professionals can help you find lenders more likely to approve your application.

Remember, owning a home is still possible, even with a cancer diagnosis. With the right support and a bit of determination, you can do it.

Need a good broker? Get in touch. We’ll connect you with a qualified mortgage broker to help with your mortgage application.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can you get a mortgage if you are sick?

Yes, you can get a mortgage if you are sick. Lenders focus more on your ability to repay the loan rather than your medical history.

However, your illness might affect your income and financial stability, which could impact your mortgage application.

Make sure to provide detailed documentation of your income, expenses, and any benefits you receive.

A specialist mortgage broker can help you find lenders who are more accommodating to your situation.

What can stop you from getting a mortgage?

Several factors can prevent you from getting a mortgage.

A poor credit history, such as a low credit score or missed payments, can make lenders hesitant.

Insufficient income that doesn’t meet the lender’s affordability criteria can also lead to rejection.

High levels of existing debt can affect your ability to take on more borrowing, and unstable employment is another red flag for lenders who prefer applicants with secure jobs.

Additionally, not having enough savings for a deposit or providing inaccurate or incomplete information on your application can result in a denial.

How to deal with mortgage anxiety?

Dealing with mortgage anxiety involves several strategies.

Educate yourself about the mortgage process to reduce uncertainty and stress.

Seek professional advice from mortgage brokers or financial advisors to get guidance and answers to your questions.

Create a detailed budget to ensure you can afford your mortgage payments and plan for unexpected expenses.

Having mortgage protection insurance can offer peace of mind, knowing your payments are covered in case of illness or job loss.

Engage in stress-relief techniques such as exercise, meditation, or hobbies to manage anxiety. Support from professionals and loved ones can also significantly alleviate your stress.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]