- What is a Lodger Mortgage?

- How Does a Lodger Mortgage Work?

- Can You Have a Lodger With Any Mortgage?

- Which Mortgage Lenders Allow Lodgers?

- Eligibility Criteria for Lodger Mortgages

- What’s the Difference Between a Lodger and a Tenant?

- How Much Can You Earn From a Lodger?

- What is the Rent a Room scheme?

- How Does the Rent a Room Scheme Affect Mortgages?

- What are The Pros and Cons of Lodger Mortgages?

- How Do You Apply for a Lodger Mortgage?

- What Should You Consider Before Getting a Lodger Mortgage?

- Can You Get a Lodger Mortgage as a First-Time Buyer?

- What If You Already Have a Mortgage and Want to Take in a Lodger?

- The Bottom Line

The Complete Guide to Lodger Mortgages

Are you struggling to keep up with your mortgage payments? Or perhaps you’re looking to increase your borrowing power for a new home? Either way, taking in a lodger could be the solution you’re searching for.

In this guide, we’ll dive into lodger mortgages, covering the essentials, benefits, and potential pitfalls.

What is a Lodger Mortgage?

A lodger mortgage, also called a rent-a-room mortgage, lets you count income from a lodger when applying for a mortgage.

This can be a big advantage for both homeowners and those looking to buy.

It can significantly increase how much you can borrow or make your existing mortgage payments more manageable.

How Does a Lodger Mortgage Work?

With a lodger mortgage, lenders consider the extra income you expect to earn by renting out a room in your house.

This can boost your borrowing power, potentially allowing you to borrow more than you could with just your regular income.

However, not all lenders offer these mortgages, and those that do may have limitations.

Some might only count a portion of your lodger income, while others might require you to have a renter in place for a set amount of time beforehand.

Can You Have a Lodger With Any Mortgage?

Having a lodger usually isn’t against the rules of a standard mortgage in the UK.

But, not all lenders will consider the extra income you earn from renting a room when deciding how much you can borrow on your mortgage.

If you specifically want to use lodger income to increase your borrowing power, you’ll need to find a lender that offers lodger mortgages or is willing to consider your rent-a-room income

Which Mortgage Lenders Allow Lodgers?

The landscape of lodger-friendly mortgages is constantly evolving, but some UK lenders known to be more accommodating include:

- Santander

- Bath Building Society

- Swansea Building Society

- Leeds Building Society

- Hinckley & Rugby Building Society

Remember, each lender has its own criteria and policies, which can change over time.

It’s always best to consult with a mortgage broker who can provide up-to-date information on which lenders are currently offering lodger mortgages and which might be most suitable for your specific circumstances.

Eligibility Criteria for Lodger Mortgages

To qualify for lodger mortgages, you need to meet the following criteria:

- Provide proof of your regular income, like pay slips or tax returns.

- Show potential or existing lodger income with rental agreements or payment records.

- Maintain a good credit score.

- Ensure your property meets safety and legal standards for accommodating a lodger.

- Meet the lender’s Loan-to-Value (LTV) ratio requirements, typically up to 80%.

- Have a stable financial history without recent bankruptcies or major debts.

- Plan to live in the property yourself, as lenders prefer homeowners to reside with their lodgers.

- If you’re a leaseholder, check if your lease allows subletting or having lodgers.

- Have home insurance that covers lodgers.

- Meet any additional criteria set by the lender, which may include not allowing family members as lodgers, remortgaging only, and having only one lodger at a time.

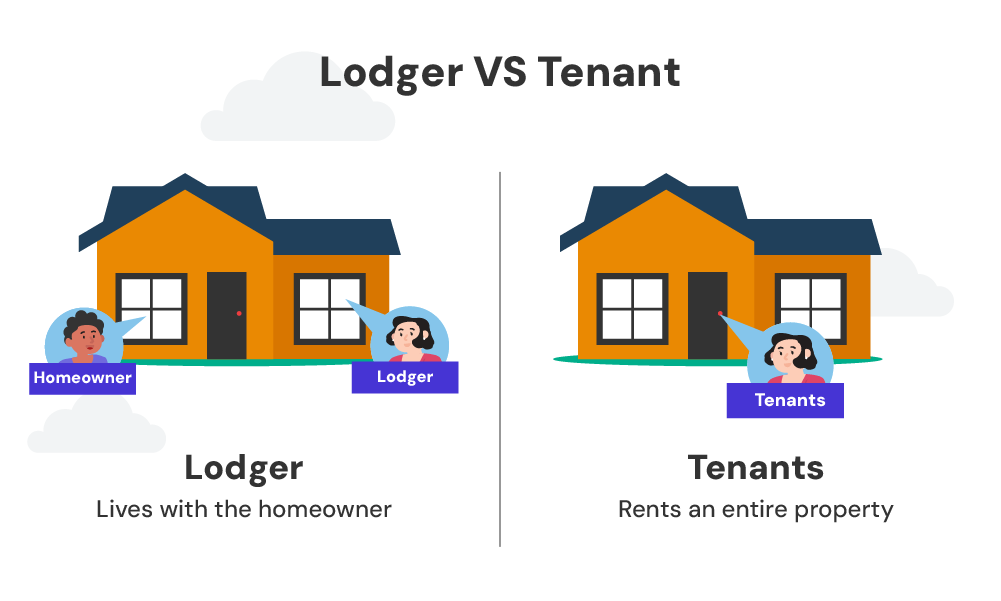

What’s the Difference Between a Lodger and a Tenant?

Knowing the distinction between a lodger and a tenant is crucial when considering a lodger mortgage:

- Lodger – A lodger lives in your home with you, typically renting a single room. You share common areas like the kitchen and living room. As the homeowner, you maintain more control over the property and the arrangement is generally more flexible.

- Tenant – A tenant rents an entire property or a self-contained part of it. They have exclusive rights to the rented space and more legal protections. If you’re looking to rent out your entire property, you’d need a buy-to-let mortgage instead.

For lodger mortgages, lenders are specifically interested in arrangements where you, as the homeowner, continue to live in the property alongside your lodger.

How Much Can You Earn From a Lodger?

The amount you can earn from a lodger varies depending on your location, the size and quality of the room, and local market rates.

In the UK, you can earn up to £7,500 per year tax-free under the Rent a Room scheme. This works out to about £625 per month.

If you charge more than this threshold, you’ll need to declare the income and pay tax on the excess.

However, even with tax considerations, the extra income can make a significant difference to your mortgage affordability.

What is the Rent a Room scheme?

The Rent a Room scheme is a UK government initiative designed to encourage homeowners to rent out spare rooms.

As discussed, under this scheme, you can earn up to £7,500 per year tax-free from letting out furnished accommodation in your main home.

Key points about the Rent a Room scheme:

- It applies to both homeowners and tenants (with their landlord’s permission).

- The room must be furnished and part of your main residence.

- You don’t need to own the property to benefit from the scheme.

- The tax exemption is automatic if you earn less than the threshold.

- If you earn more, you must complete a tax return and opt into the scheme.

>> More about the Rent a Room scheme.

How Does the Rent a Room Scheme Affect Mortgages?

Many lenders view income from the Rent a Room scheme favourably when assessing mortgage applications.

It’s seen as a reliable source of additional income, potentially boosting your borrowing power.

However, lenders’ policies vary, with some considering 100% of the income up to the £7,500 threshold, while others might only factor in a portion of it.

What are The Pros and Cons of Lodger Mortgages?

Here are the benefits and drawbacks of lodger mortgages:

Pros:

- Increased borrowing power

- Help with mortgage payments

- Tax-free income up to £7,500 under the Rent a Room scheme

- Potential for companionship

- More efficient use of your living space

Cons:

- Reduced privacy

- Potential wear and tear on your property

- Responsibilities as a live-in landlord

- Possible impact on home insurance premiums

- This may affect some means-tested benefits

How Do You Apply for a Lodger Mortgage?

Applying for a lodger mortgage is similar to a standard mortgage application, with a few key differences:

- Find lenders – Identify mortgage providers who accept lodger income.

- Gather documentation – In addition to standard mortgage documents, you may need to provide:

- Proof of lodger income (if you already have a lodger)

- A signed rental agreement (for potential lodgers)

- Evidence of long-term lodger arrangements (if applicable)

- Calculate potential income – Estimate how much you could earn from a lodger, considering local market rates and the Rent a Room scheme threshold.

- Speak to a mortgage broker – They can help you navigate the complexities of lodger mortgages and find the best deals.

- Submit your application – Your broker or chosen lender will guide you through the process.

- Property valuation – The lender will assess your property to ensure it’s suitable for accommodating a lodger.

- Offer and completion – If approved, you’ll receive a mortgage offer and can proceed to completion.

What Should You Consider Before Getting a Lodger Mortgage?

Before jumping into a lodger mortgage, consider these key factors:

- Legal and Safety Requirements – Understand your responsibilities as a live-in landlord, including compliance with local regulations, and safety standards, and having necessary safety equipment like smoke alarms and fire exits.

- Insurance – Check if your home insurance covers lodgers or if you need additional coverage. Some insurers may exclude lodgers, which could invalidate your policy.

- Council Tax – You may lose single occupancy discounts if you take in a lodger. Verify how this affects your council tax payments.

- Lease Restrictions – If you’re a leaseholder, check if your lease allows lodgers. Some lease agreements prohibit subletting, including lodgers.

- Long-Term Commitment – Consider if you’re prepared for the long-term implications of sharing your home, affecting your privacy and daily living environment.

- Lender Considerations – Not all lenders consider lodger income when assessing mortgage affordability. Find lenders who accept this type of income and may require proof of a stable lodger arrangement. Some lenders might want your lodger to be a joint owner, especially if considered a permanent lodger. Discuss your specific situation with a mortgage advisor for personalised advice.

- Tax Implications – Under the Rent a Room scheme, you can earn up to £7,500 per year tax-free. If you exceed this threshold, you must declare the extra income on your tax return.

- Credit Score – Having a lodger doesn’t directly affect your credit score. However, if you rely on their rent for mortgage payments, ensure you can cover costs if they default.

Can You Get a Lodger Mortgage as a First-Time Buyer?

Yes, some lenders do offer lodger mortgages to first-time buyers. This can be an excellent way to get onto the property ladder, especially in high-cost areas.

However, you may face stricter criteria and potentially higher interest rates compared to established homeowners.

As a first-time buyer considering a lodger mortgage, you’ll need to show:

- A solid plan for finding and managing lodgers

- Sufficient income to cover mortgage payments without relying entirely on lodger income

- A property suitable for accommodating lodgers

What If You Already Have a Mortgage and Want to Take in a Lodger?

If you already have a mortgage and want to take in a lodger, follow these steps:

- Check your mortgage terms to ensure your current mortgage allows lodgers.

- Inform your lender – Even if allowed, it’s best to notify your mortgage provider.

- Contact your insurer to update your home insurance policy.

- Consider remortgaging – If your current lender doesn’t allow lodgers or won’t consider the income, you might want to explore remortgaging options with a lodger-friendly lender.

- Prepare your property to ensure your home is ready and safe for a lodger.

- Understand your responsibilities – Familiarise yourself with landlord obligations and tax implications.

The Bottom Line

Lodger mortgages can be a great way to borrow more for your home or make your existing mortgage payments easier.

Turn your spare room into a money-maker by taking advantage of the Rent a Room scheme and choosing the right lender with the help of a whole-of-market broker.

Here’s why using a whole-of-market broker makes sense:

- You’ll get access to exclusive deals not available on the high street.

- Save time and stress by letting an expert search the entire market for you.

- Boost your chances of approval with tailored advice on lender criteria.

- Potentially save thousands over the life of your mortgage with better rates.

- Benefit from personalised guidance on complex situations like lodger mortgages.

- Stay informed about the latest market trends and opportunities.

- Receive ongoing support throughout the application process and beyond.

Looking for the right broker? Get in touch. We’ll help you get matched with a qualified whole-of-market broker to help with your mortgage application.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Is it okay not to tell my mortgage lender if I rent a room?

No, you must inform your mortgage lender if you plan to rent out a room. It’s a requirement under the terms of most mortgage agreements.

Failing to do so could violate your mortgage terms and potentially result in penalties or other consequences.

Your lender needs to know because it can affect your mortgage conditions, insurance requirements, and overall agreement.

Can I get a lodger mortgage if all my income comes from lodgers?

No, you cannot get a lodger mortgage if all your income comes from lodgers. Lenders require that your primary income comes from a stable source, such as employment or self-employment.

Lodger income can only be considered as supplementary income. Lenders view primary income from lodgers as unstable and insufficient to qualify for a mortgage.

Can I use rental income to qualify for a mortgage in the UK?

Yes, you can use rental income to qualify for a mortgage in the UK, but it depends on the lender.

Some lenders will consider rental income, including income from lodgers, as part of your overall income when assessing mortgage affordability.

However, the acceptance of rental income varies, and lenders may have specific criteria, such as a proven rental history or a formal rental agreement.

It’s best to consult with a mortgage broker to find lenders who will consider rental income for your mortgage application.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]